ACS Divesh Goyal

Section: 184 Disclosures of Interest by Directors:

Section: 184 Disclosures of Interest by Directors:

(1) Every Director Shall disclose his Concern or interest in any

- company

- Companies

- Body Corporate

- Firms

- Other Associations of Individuals

by giving a Notice In Writing In Form MBP 1.

- At First BM in which he participate as director

AND

- Thereafter, At First BM of Every Financial Year

OR

- Whenever, Any change come in the Disclosure already made, then First BM held after such change.

Note:It is Duty of Director to give notice of interest, so it can be take note at the meeting held immediately after the date of Notice. (Rule)

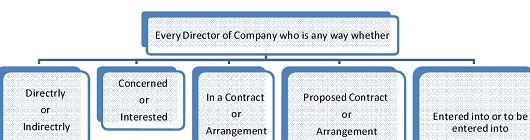

2. Every Director of Company Who is any way Whether,

- With Body Corporate in which such director or such director in association with any other director

i. Hold More than 2% of Shareholding or

ii. Is a Promoter or

iii. Manager,

iv. CEO of the body corporate

- With a Firm or Other Entity in which, such director

i. Is a Partner,

ii. Owner or member

Shall disclose nature of his interest at the meeting of Board in which such contract or arrangement is discussed and shall not participate in such meeting.

Note:

- If director or director associated with other director hold 2% or less than 2% of shareholding interest in other body corporate than this section will not apply.

- If company enter into such contract without getting disclosure from the director and with participation of director than such contract shall be voidable at the option of the company.

Conclusion of 184:

- If Directors give disclosures under this section it will help to create trust of stake holders on company and will show loyalty of directors and will help in growth of company, because all transaction will be for growth of company and its stake holders.

Section: 188 RELATED PARTY TRANSACTION:

Applicability:

- This is applicable for Private Company and Public Company.

Approval:the Transaction of a company with Related Parties which are Not in the Ordinary Course of Business and which is Not on Arm Length Price require following approval for Entering into Such Transactions with Related Party:-

1- Board Approval

- For enter into transactions mention under this section Consent of Board of Directors is Require by Passing of Resolution in the Meeting of Board of Directors.

Note:Such resolution can’t be pass by circulation of resolution to the Board of Directors.

2- General Meeting

For entering Transactions with related parties mention below SR is required to be passed in GM:

- When Paid up Share Capital of Company is 10 Crore or More. or

| NATURE OF RELATED PARTY TRANSACTION | THRESHOLD LIMIT |

| Sale, purchase or supply of any goods or materials directly or through appointment of agents (or) | Exceeding 25% of Annual Turnover |

| Selling or otherwise disposing of, or buying, property of any kind directly or through appointment of agents (or) | Exceeding 10% of Net worth |

| Leasing of property of any kind (or) | Exceeding 10% of Annual Turnover ORExceeding 10% of Net worth |

| Availing or rendering of any services directly or through appointment of agents (or) | Exceeding 10% of Net worth |

| Appointment to any office or place of profit in the company, its subsidiary company or associate company (or) | Monthly Remuneration Exceeding Rs. 2.5 lakhs |

| Remuneration for underwriting the subscription of any securities or derivative | Exceeding 1% of Net worth |

Note:*Turnover and Net worth as per Audited Financial Statement of Preceding Financial Year.

* If any member is interested in any transaction, than such member shall not cast vote in meeting regarding such resolution.

* Exemption:No resolution is required to be passed by WOS, when Special Resolution is passed by holding company to enter into transaction with Wholly Own Subsidiary Company.

* Every Transaction enter into section 188 shall be enter into Director Report along with Justification.

Voidable Contract (Section 188 (3) :

According to the section 188, sub section (1), any contact or arrangement must be passed through Board Meeting or Shareholders Meeting, as case may be,

Suppose, the Contact has been made but the approval has not taken either in the Board Meeting or Shareholders Meeting within 3 months from the date of Contract, In that case the Contract shall be voidable at the option of the Board.

In case of Loss in Result of Contract:

If a director or employee entered into any contract and arrangement in contravention of provision of this section then company can proceed against such director and employee for recovery of any loss sustained by it from such contract.

Penalty:

Any director who enter any contact or any employee who is authorized to enter any contact make any default for compliance of this provisions shall be penalized in case of:

Listed Company:-

- Imprisonment for a term which may extend to 1 Year

OR

- fine which shall not be less than 25000/-but which may extend Rs. 5,00,000/- or

- Both

Unlisted Company: – Fine which shall not be less than 25000/- but which may extend Rs. 5,00,000/- or both

FOR LISTED COMPANIES CORPORATE GOVERNANCE IN LISTED COMPANIES:

Note:

1. Clause 49 (VII)as given in Part-B shall be applicable to all PROSPECTIVE Transactions.

2. All EXISTING Material related party contracts& arrangements as on 17th April, 2014,which will continue beyond 31st March 2015, Shall be require Share Holder Approval in the First GM held after 01st October, 2014.But companies may get approval of share holder even before 01st Oct, 2014.

Meaning of Related Party Transaction under clause 49:

- A related party transaction is a transfer of resources, services or obligations between a company and a related party, regardless of whether a price is charged.

- A ‘Related Party’ is a person or entity that is related to the company. Parties are considered to be related if one party has the ability to control the other party or exercise significant influence over the other party,directly or indirectly, in making financial and/or operating decisions and includes the following:

Material Related Party Transaction:if the transaction / transactions to be entered into individually or taken together with previous transactions during a financial year

Exceeds 5% percent of the annual turnover OR

20% percent of the net worth of the company

As per the last audited financial statements of the company,whichever is higher.

- All Related Party Transactions shall require prior Approval of the Audit Committee.

- All material Related Party Transactions shall require Approval of the Shareholders through Special Resolution and the related parties shall abstain from voting on such resolutions.

Disclosures of Related Party Transactions:

- Company shall disclose policy of dealing with related party Transactions on its

- Website AND

- In the Annual Report

- Details of Material Related Party Transaction shall be disclosed quarterly along with the compliance report on Corporate Governance.

Section 189: Register of Contract and Arrangement in Director are interested

- Every Company shall maintain one or more register in Form MBP-4

- Giving separately the particulars of Contract or arrangement to which section 184(2) or188 applies.

- After entering the particulars, such register shall be Placed before the next Board Meeting and Signed by all the directors Present at the meeting.

- Entry shall be made in chronological order, authenticated by Company secretary of Company and person authorized by board.

- The register shall be kept at the registered office of the Company and preserved permanently.

- Members may also take extracts from this register

*Exemption:

- No entry required to be done in register if contract is for sale, purchase or supply of goods, material or services , the value of such materials or the cost of such services does not exceed Rs. 5 lakh in the aggregate in any year.

- Any contract or arrangement by banking company for the collection of bills in the ordinary course of its business.

- Where in any company or companies or Bodies corporate in which a director together with any other director holds 2% or less of the paid-up share capital.

Check Point for Section 188:

If company going to enter in contract or arrangement with related parties as mention in section 2(76) for the transaction mention under section 188(1) following is the procedure:

- First Check party is Related as per section 2(77)

- Second check Transaction cover under section 188(1) If both the conditions mention above is satisfied then:

- Call a Board Meeting:

a) Consent of Board of Director by Passing of Board Resolution for contract

b) Issue notice of General Meeting, if require

- Passing of Special Resolution in GM, if require

- Filling of Resolution with Roc within 30 days

- Disclosure of transaction with complete justification in Board of Directors Report

- Entry of such transaction in register maintain under section 189

- Register shall be place before next BM and signed by all the directors present at the meeting

(Author can be reached at csdiveshgoyal@gmail.com )

Author Bio

Hi

Divesh

what is the source of this article actually i didn’t find out the prior approval of member if the paid up share capital is more than 10 crores (Section 188 of the Companies Act, 2013)

Mr. Divesh,

Request your input on following points:

1. Does a company needs to maintain register even if all the related party transaction are in ordinary course of business & at arms length (as for such transactions neither Board nor Shareholders resolution is required)?

If yes, then in which Board meeting register will have to be signed ?

2. Wrt disclosure u/s 184, MBP-1 is obtained from directors but none of the directors is interested. Hence, entry in MBP-4 is not required ?

Pls confirm.

Thanks,

your posts are really very easy to understand and helpful in preparing varous ssignments.

Dear Sir(s),

We want to sale our Excisable Inputs to our sister concerned unit, under rule 3(5) CCR 2004,(AS SUCH SALES). pl clarify whether this type of transaction also comes under sec 188 of CA 2013. if so how to acertain complaince CCR 2004 vs CA 2013.