Appointment for 5 Years: {Section: 139(1)}

Every company shall, at the first annual general meeting, appoint an individual or a firm as an auditor who shall hold office from the conclusion of that meeting till the conclusion of its sixth annual general meeting and thereafter till the conclusion of every sixth meeting.

Ratification of Auditor: {First Provision of 139(1)}

Act Language: The Company shall place the matter relating to such appointment for Ratification by members at every Annual General Meeting.

Rule 3(7) Proviso: Appointment of Statutory Auditor shall be subject to ratification in every annual general meeting till the sixth such meeting by way of passing of an ordinary resolution

As per the above proviso Companies are required to ratify the appointment of Statutory Auditors who was appointed in last AGM for 5 financial years. Therefore from this year, every year in AGM an Ordinary Resolution is to be passed for ratification to continue as Statutory Auditor of the Company.

| QUESTION & ANSWERS | |

| A. | Whether it is Special Business or Ordinary Business. |

| Appointment or Re appointment of Auditor is Ordinary Business so in line with that Ratification to continuation of Auditor will be ORDINARY BUSINESS. | |

| B. | Whether it is Appointment or Re-appointment? |

| This is neither appointment nor re-appointment. It is confirmation of continuation of Statutory Auditor. Appointment has already been made. | |

| C. | Whether ADT-1 will file for ratification of auditor or Not? |

| There is NO need to file ADT-1 for ratification of Auditor. | |

| D. | Whether Special Resolution or Ordinary Resolution will pass for ratification of Auditor? |

| As per proviso of Rule 3(7) – ORDINARY RESOLUTION will pass for ratification of auditor. | |

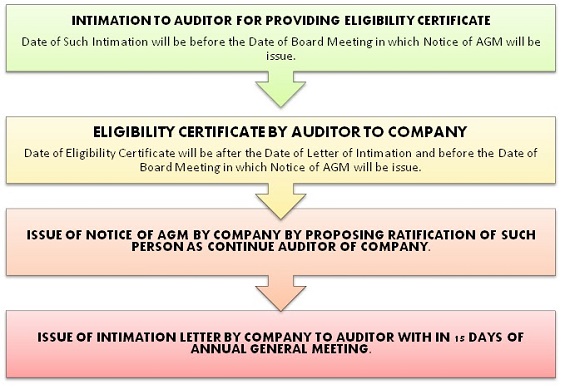

| E. | Whether Company needs eligibility Certificate from auditor? |

| As per Section 139(1) Proviso III read with section 141

Before placing the business for ratification of auditor before AGM the Company will obtain an Eligibly certificate from the Auditor. |

|

| F. | Whether Explanatory Statement required to give for Ratification of Auditor? |

| As per Section 102 Explanatory Statement required for the Special business to be transacted in General Meeting. Therefore, ratification of auditor is Ordinary Business.

But it is advisable to give Explanatory Statement in Notice of AGM for Ratification of Auditor. |

PROCESS FOR RATIFICATION OF AUDITOR

DRAFTS FOR THE REFERENCE:

DRAFTS FOR THE REFERENCE:

♠ Draft board resolution:

ITEM NO: To consider the ratification of m/s (name of firm), chartered accountants as statutory auditors of the Company:

The Chairman informed that M/s (Name of Statutory Auditor Firm), Chartered Accountants, (FRN-___________________) were appointed by the shareholders at the (No. Of last Annual General Meeting) Annual General Meeting to hold office until the conclusion of the (Five years from last Annual General Meeting) Annual General Meeting subject to ratification by shareholders at each Annual General Meeting. He further informed that Company has obtained from the Auditors, a certificate as required under Section 139 of the Companies Act, 2013 to the effect that they are eligible to continue as statutory auditor of the Company. The Board considered the matter and thereafter decided that the ratification of the above named Auditors be recommended to the shareholders at the forthcoming Annual General Meeting.

After discussions the following resolution was passed unanimously:

“RESOLVED THAT subject to approval of shareholders at their forthcoming Annual General Meeting, M/s (Name of Statutory Auditor Firm), Chartered Accountants, (FRN-___________________) from whom certificate pursuant to section 139 of the Companies Act, 2013 has been received be and hereby ratified to continue as Statutory Auditors of the Company to hold office from the conclusion of this Annual General Meeting till the conclusion of the next Annual General Meeting of the Company at a remuneration to be mutually decided.”

♠ Draft of Notice of AGM:

ORDINARY BUSINESS:

1. Ratification of Auditor:

To consider and if thought fit to pass with or without modification(s) the following resolution as an Ordinary Resolution:

“RESOLVED THAT pursuant to Sections 139, 142 and other applicable provisions, if any, of the Companies Act, 2013 (the “Act”) and the Companies (Audit and Auditors) Rules, 2014 (“Rules”) (including any statutory modification or re-enactment thereof, for the time being in force), the Company hereby ratifies the appointment of M/s (Name of Firm), Chartered Accountants, (Firm Registration No. __________), as Auditors of the Company to hold office from the conclusion of this Annual General Meeting (AGM) till the conclusion of the next AGM of the Company to be held in the year 2016.”

♠ Draft Ordinary resolution:

RATIFICATION OF AUDITOR-ORDINARY RESOLUTION

Proposed by: (Name of Member)

Seconded by: (Name of Member)

The ordinary resolution set at item no. 2 of the notice pertaining to the ratification of Auditor and their remuneration, proposed and seconded by the afore mentioned shareholders and taken up for consideration with the consent of the Members present.

“RESOLVED THAT pursuant to Sections 139, 142 and other applicable provisions, if any, of the Companies Act, 2013 (the “Act”) and the Companies (Audit and Auditors) Rules, 2014 (“Rules”) (including any statutory modification or re-enactment thereof, for the time being in force), the Company hereby ratifies the appointment of M/s (Name of Firm), Chartered Accountants, (Firm Registration No. ________), as Auditors of the Company to hold office from the conclusion of this Annual General Meeting (AGM) till the conclusion of the next AGM of the Company to be held in the year 2016.”

The above Ordinary Resolution was thereafter put to vote and on a show of hands was declared carried unanimously.

ELIGIBILITY CERTIFICATE:

LETTER HEAD OF AUDITOR

To Date: (before the date of Issue of Notice of Board Meeting)

The Board of Directors,

(NAME OF COMPANY)

(Registered Office Address of Company)

Dear Sirs/Ma’am,

Ref: Certificate u/s 139 for ratification to continue as statutory auditor under the Companies Act, 2013

We were appointed as statutory auditors of (Name of Company) from the conclusion of (No. of Last AGM) Annual General Meeting (AGM) till the conclusion of the (5th AGM from last AGM).

AGM of the Company to be held in the year 2019 (subject to ratification of our appointment at every AGM).

In pursuance of requirement of section 139 of the Companies Act, 2013 and rule (4) of Companies Audit and Auditors) Rules, 2014, we hereby confirm that:

1) The firm is eligible for ratification and is not disqualified to continue as statutory auditor under section 141 of the Companies Act, 2013, the Chartered Accountant Act, 1949 and rules and regulations made there under;

2) Our ratification would be as per the terms provided under the Act;

3) There are no proceedings pending against either of the partners or the firm with respect to professional matters of conduct.

Thanking you,

Yours Sincerely,

(NAME OF FIRM)

Chartered Accountants

Firm Registration No. ___________

(Name of Auditor)

Proprietor

Membership No. _______

(Author – CS Divesh Goyal, ACS is a Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com)

(Author – CS Divesh Goyal, ACS is a Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com)

Author Bio

Hi.. recently 1 amendment came. Jisme ye ratification proviso was omitted.. is it true??

IF WE APPOINT AUDITOR FOR 5 YEARS IN AGM BUT IN FORM ADT 1 TENURE OF APPOINTMENT IS WROTE ONLY FOR 1 YEAR.

THEN FORM ADT 1 VALID FOR 1 YEAR OR FOR 5 YEAR.

IS NEED TO FILE ADT 1 ,NEXT YEAR FOR 4 YEARS.

PLS REPLY ITS URGENT

I called the ROC at Chandigarh and they said that we have to file ADT-1 for both ratification as well as appointment of auditor. Though, I’d still like clarification on what is to be done.

What to do if members did not ratify the appointment

There is requirement to file any form to file that resoultion for ractification of auditor

What if shareholder in annual general meeting not passed the resolution regarding ratification/appointment of statutory auditor. whether the same is considered as removal or casual vacancy.

Hi, what if the company does not receive eligibility certificate in timr

Hi..!

if in a company an Auditor’s firm is auditing since 2007-08 and they are being reappointed for 1 year at every AGM i mean AGM to AGM instead of 5 years den is dis correct as per law?? can a company appoint firm for less than 5 years?

Hi

Last year the Form ADT-1 was a manual form which was required to be e-filed as an attachment to Form GNL-2. None of these forms had any provision for mentioning the number of years for which the appointment was made. Though the Notice did mention that the auditors are being considered for appointment for a a period of 5 years.

What should be the course of action then ?

Hi,

Should Form ADT-1 be filed for each year even though we have filed it once indicating that the appointment is for 5 years?