As per sub Section 9 of Section 12 of the Companies Act, 2013 read with the Companies (Incorporation) Rules, 2014

If the Registrar has reasonable cause to believe that the company is not carrying on any business or operations, he may cause a physical verification of the registered office of the company in such manner as may be prescribed and if any default is found to be made in complying with the requirements of sub-section (1), he may without prejudice to the provisions of sub-section (8), initiate action for the removal of the name of the company from the register of companies under Chapter XVIII.

- The Ministry of Corporate Affairs (MCA) on August 18, 2022, hereby makes the following rules further to amend the Companies (Incorporation) Rules, 2014 to the Companies (Incorporation) Third Amendment Rules, 2022.

- After the rule 25A (i.e. Active Company Tagging Identities and Verification (ACTIVE)) of the Companies (Incorporation) Rules, 2014, the Rule 25B (Physical Verification of the Registered Office of the Company) shall be inserted:

Rule 25 B of the Companies (Incorporation) Rules, 2014 in a Nutshell

⇓

PHYSICAL VERIFICATION OF THE REGISTERED OFFICE OF THE COMPANY

While doing Physical Verification

- RoC shall carry out those documents filed with MCA to support the registered office of the Company

Check the Authenticity of the filed documents

- By cross verification with the copies of supporting documents collected while doing physical verification

- Supporting documents are duly authenticate from the occupant of the property

Photograph of Registered Office

- The registrar shall take a photograph of the registered office of the Company while causing physical verification of the same.

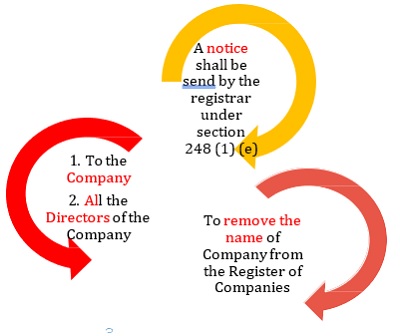

CONSEQUENCE

- If the registered office of the Company is found to be not capable of receiving and acknowledging all communications and notices after physical verification:

However, the Company and its Directors have a 30 days’ time period from the date of the notice to send their representations along with copies of relevant documents if any, after that the provision of Section 248 of the Companies Act, 2013 would apply.

Author CS Divya Goel, ACS is working as Head Manager- Company Secretary with Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India. Author can be reached at info@neerajbhagat.com.