Defaults under the Companies Act, 2013 provides for certain liabilities and the registrar of a company has powers to initiate prosecution against the company and its directors and other officers in accordance with the provisions of the law. When a provision has been violated or a default or delay has occurred, the directors may, instead of allowing the launching of a prosecution or contesting any prosecution already launched against the company and its directors and officers who are liable, apply to get the offence compounded, if the offence in question is a compoundable offence.

Section 441 of the Companies Act, 2013 deals with Compounding of offence. Compounding of offences is not new under the Company Law; similar provisions were also presents in Section 621A of the Companies Act 1956.

You can read Section 441 of the Companies Act, 2013 here: http://ebook.mca.gov.in/default.aspx

Compounding of offences is a settlement mechanism, by which, the offender is given an option to pay money in lieu of his prosecution, thereby avoiding a prolonged litigation. While there is no definition of the word “compounding” provided either in the Act 1956 or the Act 2013. However legal meaning of compounding of offence is “Doing good the default/non-compliance”. Therefore, the first and foremost step in compounding is to make the default good.

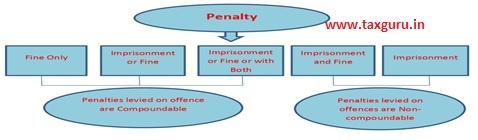

Types of Penalties:

There are five types of penalties that can be levied on the commission of the offences that have been contemplated under the Companies Act, 2013.

Which offences are compoundable?

According to Section 441(1), as amended by the Companies (Amendment) Act 2017 and the Companies (Amendment) Ordinance, 2018, any offence punishable under the Companies Act (whether committed by a company or any officer thereof) not being an offence punishable with imprisonment only, or punishable with imprisonment and also with fine, may, either before or after the institution of any prosecution, be compoundable.

Any offence covered under Section 441(1) by any company or its officer shall not be compounded if the investigation against such company has been initiated or is pending under this Act.

According to Sub-Section (6), any offence which is punishable under this Act with imprisonment only or with imprisonment and also with fine shall not be compoundable.

Thus, the following offences under the Companies Act cannot be compounding by the NCLT or the Regional Director:

> An offence which is punishable with imprisonment only.

> An offence which is punishable with imprisonment and also with fine.

Jurisdiction to handle cases for the compounding:

A significant pre-requisite for filing application for compounding is to know where the application should be filed. The National Company Law Tribunal shall exercise the power of compounding an offence in accordance with and subject to the provisions of the Companies Act and the Rules prescribed under it.

But according to clause (b) of Sub-section (1), as amended, where the maximum amount of fine which may be imposed for such offence does not exceed twenty-five lakh rupees, by the Regional Director or any officer authorised by the Central Government.

Procedure to compound an offence under Companies Act, 2013:

Procedure to compound an offence under Companies Act, 2013:

a) Calling of Board Meeting Company will call the Board Meeting as per Companies Act, 2013 and SS1.

b) Calculate the amount of offence Board will calculate the amount of the penalty as per the relevant section.

c) Holding of Board Meeting Pass a resolution to file application with authority for compounding of offence and authorize director of the Company and for preparation and signing of documents including application. Company will authorize any professional for follow up the matter with authority.

d) Preparation of Compounding Application Company will prepare the application of compounding as per NCLT Rules.

e) Filling of Form with ROC Procedure for making application:

Application for compounding shall be submitted electronically in eform GNL1. This form will be forwarded by ROC to NCLT/Regional Director as applicable. The Schedule of fees under the National Company Law Tribunal Rules 2016 has prescribed a fee of Rs, 1,000/- on an application for compounding of certain offences.

In GNL – 1, the application can be filed for Company, Director or Manager/Secretary or CEO/CFO or other officers of the Company (even jointly). Details of only 8 persons can be entered in the e Form. If number of persons is greater than 8, then additional details can be provided in optional attachment.

f) Hearing before Authority. There is no specific provision in the Act, normally, NCLT/Regional Director will give personal hearing and then pass a speaking order giving reasons. The hearing can be attended by Director/secretary/ officer of Company or by authorized representative like advocate or a practicing CS/ CA/ CMA.

Where any offence is compounded, intimation thereof shall be given by the company to the Registrar within seven days from the date on which the order is made available to the petitioner/applicant.

Permission of Special Court No More required:

As per sub-section (6)(a) of section 441 as stood before being amended by the Companies (Amendment) Ordinance 2018, permission of the Special Court was required for compounding of any offence which is punishable under this Act, with imprisonment or fine, or with both. Such offences can now be compounded without the permission of the special Court in view of the said amended effective from 2nd November, 2018.

Discretionary power to reject the Application?

The Compounding application cannot be rejected without due consideration. The Company Law Board (now NCLT) in the case of Amadhi Investments Ltd., held that neither of the CLB or the Regional Director has been authorized with discretionary power to reject a compounding application without due consideration.

Whether NCLT has powers to review its own decision?

The NCLAT in the case APC Credit Rating Private Limited Vs. Registrar of Companies, NCT of Delhi and Haryana, [2018] 143 CLA 166 (NCLAT) had answered the above question, the NCLAT held that;

“it is clear that there is no inherent power to review, as is under Order 47 Rule 11 of the Code of Civil Procedure, 1980 but the Tribunal has power conferred by sub-section (2) of Section 420 of the Act, 2013 to rectify any mistake apparent from the record and to amend the order accordingly.”

Therefore, we can categorically say that NCLT has power to review its own orders unless the statue is amended to make way for such review. From the above decision of NCLAT it is clear that inherent powers under Rule 11 of the NCLT Rules can’t be said to be empowering NCLT with a power to review.

(Any query and suggestion kindly contact the author at: sandy673711@gmail.com or +918077133617)

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness, and reliability of the information provided, I assume no responsibility, therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not professional advice and is subject to change without notice. I assume no responsibility for the consequences of the use of such information.

Author Bio

Read. Thanks for the writing.

Contrary to your comments it is stipulated in the Companies (Ammendment) Ordinance,2018 that offence punishable for imprisonment only or imprisonment with fine shall not be compoundabe.

Please make it clear.