ACS Divesh Goyal

MEETINGS OF THE BOARD

MEETINGS OF THE BOARD

1. Frequency of Meeting:

– First Meeting:First Meeting of Board of Directors within 30 (Thirty) days from the date of Incorporation of company. –

– Subsequent Meetings:

One person Company, Small company and Dormant company:

- At least one meeting of Board of directors in each half of calendar year

- Minimum Gap B/W two meetings at least 90 days.

Other than Companies mentioned above:

- Minimum No. of 4 meetings of Board of Director in a calendar year

- Maximum Gap B/W two meetings should not be more the 120 days.

2. Calling of Meeting: Meeting of Board of Director should be called by giving 7 days notice to Directors at his registered address through:

- By hand delivery

- By post

- By Electronic means

Meeting at shorter Notice: A meeting of Board of Directors can be called by shorter notice subject to the conditions:

- If the company is require to have independent director:

– Presence of at least one Independent director is required.

– In case of absence, decision taken at such meeting shall be circulated to all the directors, and

– shall be final only on ratification thereof by at least one Independent Director

- If the company doesn’t require to have independent director: The meeting can be called at a shorter notice without any conditions to be complied with.

3. Quorum of Board Meeting:

- 1/3 rd of total strength OR 2 (Two) Directors, whichever is higher.

- Where meeting of Board could not be held for want of quorum, the meeting shall

automatically adjourn to same time, same place at next week (Not being national holiday). - If number of directors reduced below quorum, then the remaining directors may hold the meeting for the following purposes:

- To call a General meeting

- Increase the number of directors.

- Quorum in case of Interested Directors:

- If interested director exceed or equal to 2/3 of total strength the remaining directors not being less than 2 (two) shall be the quorum.

Note:

- Total strength shall not include directors whose places are vacant.

- Interested director means, a director interested in accordance with section 184(2).

- Director participating in a meeting through video conferencing or other audio visual means shall be counted for the purpose of quorum, unless he is to be excluded for any items of business under any provisions of the Act or the rules.

- OPC Having One Director: Provision of Section 173 and 174 shall not apply to an OPC having one director.

4. Participation of Directors in Board Meetings: directors may, apart from attending the meeting physically, participate in the meeting by way of video conferencing & other audio visual means.

- Matter which can’t be dealt at a meeting held though Video conferencing:

- Approval of the annual financial statements;

- Approval of the Board’s report;

- Approval of the prospectus;

- Audit Committee Meetings for consideration of accounts; and

- Approval of the matter relating to amalgamation, merger, demerger, acquisition and takeover.

- Procedure for conducting of meeting through Video Conferencing:

Requirements before Meeting:

- The notice of the meeting shall, inform regarding the option available to participate through video conferencing mode and provide all the necessary information to enable the directors to participate through video conferencing.

- A director intending to participate through video conferencing or audio visual means shall communicate prior intimation sufficiently in advance to the Chairperson or the company secretary of the company, so that company is able to make suitable arrangements in this behalf.

- Alternatively a director may intimate at the beginning of the calendar year his desire, to participate through the electronic mode, which shall be valid for that calendar year.

Duties of

COMPANY: to make necessary arrangements to avoid failure of video or audio visual Connection.

CHAIRMAN & COMPANY SECRETARY:

(I) To safeguard the integrity of the meeting by ensuring sufficient security and Identification procedures;

(II)To ensure availability of proper equipment or facilities for providing transmission of the communications for effective participation at the Board meeting;

Requirement during the Meeting:

- The Chairperson shall take a roll call where every director participating through video conferencing shall state Name, Location, confirmation of receipt of agenda and non-presence of any person other than the concerned director.

- Chairperson or Company Secretary shall, inform the Board about persons other than the directors who are present for the said meeting with the request of the chair and confirm the presence of quorum.

- Every participant shall identify himself for the record before speaking on any item of business on the agenda.

- If a motion is objected to and there is a need to put it to vote, the Chairperson shall call the roll and note the vote of each director.

- At the end of discussion on each agenda item, the Chairperson of the meeting shall announce the summary of the decision taken on such item along with names of the directors, if any, who dissented from the decision taken by majority.

- PLACING & SIGNING OF STATUTORY REGISTERS: The statutory registers which are required to be placed in the meeting shall be placed at the scheduled venue and where registers are required to be signed by the directors, the same shall be deemed to have been signed by the directors participating through electronic mode, if they have given their consent to this effect and it is so recorded in the minutes of the meeting.

Post Meetings Requirements:

- The minutes shall disclose the particulars of the directors who attended the meeting through video conferencing.

- CIRCULATION OF DRAFT MINUTES & COMMENTS THEREON: The draft minutes shall be circulated among all the directors within fifteen days of the meeting either in writing or in electronic means.

- Every director who attended the meeting shall confirm or give his comments in writing, about the accuracy of recording of the proceedings of the meeting in the draft minutes, within seven days or some reasonable time as decided by the Board. If no confirmation or comments received within the stipulated period, approval shall be presumed.

- DUTIES OF COMPANY SECRETARY: To record proceedings and prepare the minutes of the meeting; To store for safekeeping and marking the tape recording(s) as part of the records of the company at least before the time of completion of audit of that particular year.

Note:

- Persons who are differently abled may make request to the Board to allow a person to accompany him.

- If a statement of a director in the meeting through video conferencing or is interrupted, the Chairperson or Company Secretary shall request for a repeat or reiteration by the Director.

- Meeting of Committees can also be conducted through video conferencing.

5. Passing of Resolution by Circulation: A company may get approval on a resolution by Board of Director without conducting a board meeting; company can do it by passing of resolution by circulation. PROCEDURE OF PASSING OF RESOLUTION BY CIRCULATION:

i. The company will circulate draft resolution along with necessary papers, if any to all the directors at their registered address through.

- Hand Delivery

- Post

- Electronic Means

ii. Resolution should be approved by majority of Directors, who are entitled to vote on the resolution.

iii. Resolution passed by circulation shall be noted at a subsequent meeting of the Board and made part of the minutes of such meeting.

Note: If before passing of resolution request is made by 1/3 of total number of directors to decide such matter at meeting, the chairperson shall put the resolution to be decided at meeting of the Board.

6. POWER EXERCISABLE BY BOARD:

- The Board of Directors of a company shall be entitled to exercise all such powers, and to do all such acts and things, as the company is authorized to exercise and do. In exercising such power or doing such act or thing, the Board shall be subject to the provisions of this Act, or the memorandum or articles, or regulations made by the company in general meeting:

- POWERS TO BE EXERCISED ONLY AT BOARD MEETING:

– UNDER THE ACT:

- Make calls on shareholders in respect of money unpaid on their shares;

- Authorize buy-back of securities under section 68;

- Issue securities, including debentures, whether in or outside India;

- Borrow monies;

- Invest the funds of the company;

- grant loans or give guarantee or provide security in respect of loans;

- Approve financial statement and the Board’s report;

- Diversify the business of the company;

- Approve amalgamation, merger or reconstruction;

- Take over a company or acquire a controlling or substantial stake in another company;

– UNDER RULES:

- Make political contributions;

- Appoint or remove key managerial personnel (KMP);

- Take note of appointment(s) or removal(s) of one level below the Key Management Personnel;

- Appoint Internal auditors and secretarial auditor;

- Take note of the disclosure of director’s interest and shareholding;

- Buy, sell investments held by the company (other than trade investments), constituting five percent or more of the paid up share capital and free reserves of the investee company;

- Invite or accept or renew public deposits and related matters;

- Review or change the terms and conditions of public deposit;

- Approve quarterly, half yearly and annual financial statements or financial results as the case may be.

NOTE:

- The power to invest, borrow and grant loan / guarantee / security can be exercised by a committee duly authorize by the board.

- The resolution in pursuance of powers of the board mentioned above shall be filed with the registrar in form MGT-14 within 30 days of passing such resolution.

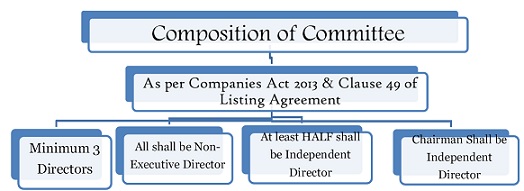

COMMITTEES:

MANDATORY COMMITTEES AND THEIR THRESHOLDS & COMPOSITIONS:

1. AUDIT COMMITTEE:

Meeting of Audit Committee:

- Audit Committee should meet at least four times in a year.

- Maximum Gap between 2 Meetings is 4 Months.

- Minimum 2 Director must be present.

COMPOSITION OF AUDIT COMMITTEE:

NOTE:

- THE FREQUENCY OF AUDIT COMMITTEE IS PROVIDED AS PER REVISED CLAUSE 49 OF LISTED AGREEMENT (Applicable from 1st October 2014)

- Chairman of the Audit Committee shall be present at Annual General Meeting to answer shareholder queries.

- The Auditor of a company and the key managerial personnel shall have a right to heard in the meeting of audit committee when it consider the auditor’s report but shall not have right to vote.

- VIGIL MECHANISM:

- Every LISTED company and company, which has:

-Accepted deposits from public;

– Borrowed money from Bank and Public Financial Institution in excess of Rs. 50 crore shall establish a Vigil Mechanism.

- The Mechanism shall, be established for director and employee to report genuine concerns and also provide for adequate safe guards against victimization of persons using such mechanism.

- The companies which are required to constitute an audit committee shall oversee the vigil mechanism through the committee and if any of the members of the committee have a conflict of interest in a given case, they should recuse themselves and the others on the committee would deal with the matter on

- In case of other companies, the Board of directors shall nominate a director to play the role of audit committee for the purpose of vigil mechanism.

2. NOMINATION & REMUNERATION COMMITTEE:

COMPOSITION OF REMUNERATION & NOMINATION COMMITTEE:

Note:

- The Chairman of the nomination and remuneration committee could be present at the Annual General Meeting, to answer the shareholders’ queries.

- NO SPECIFIC FREQUENCYOF MEETING OF NOMINATION & REMUNERATION COMMITTEE PROVIDED UNDER THE ACT.

GESTATION PERIOD FOR AUDIT, NOMINATION & REMUNERATION COMMITTEE:

According to the Companies (Meeting and Powers of Board) Amendment Rules, 2014 companies which were not required to have Audit Committee under CA-1956, but required under CA-2013 shall constitute the same within one year from 12th June, 2014 or appointment of independent director,whichever is earlier.

Similarly, Public Companies which are required to have Nomination & Remuneration committee under CA-2013 shall constitute the same within one year from 12th June, 2014 or appointment of independent director, whichever is earlier.

3. STAKEHOLDERS RELATIONSHIP COMMITTEE: Every company having more than 1000 (One thousand) Share Holders + Debenture Holders + Deposit Holders + Other Security Holders shall constitute a Stakeholders Relationship Committee, which shall consider & resolve the grievance of security holders.

Composition:

- Chairperson: Non-Executive Director

- Members: As may be decided by the Board–

4. CORPORATE SOCIAL RESPONSIBILITY COMMITTEE: Every Company:

- having net worth of Rs. 500 crore or more, or

- turnover of Rs. 1000 crore or more or

- a net profit of Rs. 5 crore or more during any financial year shall constitute a Corporate Social Responsibility Committee of the Board

COMPOSITION OF COMMITTEE:

- At least 3 (three) directors, out of which at least 1 (one) director shall be an Independent Director.

- In case of UNLISTED PUBLIC COMPANY Not required to have an Independent Director, the committee can be constituted without an Independent Director.

- In case of PRIVATE COMPANY, the committee can be constituted without an Independent Director. Further, in case of a Private Company having 2 (two) Directors, the committee can be constituted with only 2 (two) Directors.

(CS DIVESH GOYAL, ACS-35817, +91-8130757966, csdiveshgoyal@gmail.com)

Author Bio

Since a section 8 company is required to hold one board meeting within every 6 calendar months, can there be a gap of 11 months between two board meetings ?

our company have pass many board resolutions so can we required all the board resolutions minutes

What are the consequences and procedures if in a private company,

1) directors reduces to one, and

2) members reduces to only one person??

There is no time interval as much but it shall be form within the next f.y when the CSR applicable on company and amount shall be spent in that FY.

less than 90 days is not an issue. bt it shall not extend beyond 90 days gap

Financial year

90 days criteria is only for opc, Small company & dormant company

can any one help me out what are the common subject matters we discuss in different board meetings. Example;- in first meeting we should mention disclosure of directors Section 184 of the Companies Act, 2013…etc (this is for pvt. ltd company)

Can a company secretary call for AGM without consent of authorisation of BOD?? Is it valid??

Mr Divesh,

A superb compilation but..

No where it is mentioned in the current provisions of the Companies Act 2013 that the Chairperson of Audit Committee shall attend the AGM of the Company.

Please correct me if I am wrong.

If one particular Director fails to attend all board meetings for 2 years in continuation, then what is the course of action against him. Does he automatically cease to be director.

Minium gap between 2 board meeting is 120 days not 90 days.

notice of board meeting was given for 35 items. however in the meeting due to shortage of time and urgent requirement of approval of quarterly accounts board meeting was conducted and only accounts was approved. other items were not even discussed.

then my question is, in the minutes of the meeting all items should be mentioned as deferred? or any other comments pertaining to actual situation should be given.

What the implications of non discussing the items of the board meeting which were already circulated with notice?

Can approval for resolution by circulation be taken electronically and maintained with the company or should it be taken physically?

Can we have the frequency and the timing of conveying the Committee meetings?

HI,

I have some resolutions with me. i want to check the relevant dates in that resolutions. on which circumstances i have check or need to check whether there is any mismatch in those resolutions.

can we have some similar note on RISK MANAGEMENT COMMITEE

what happens if a company has only 3 meetings instead of mandatory 4 in a year

What is the interval in which CSR committee has to be done.

Section 135 and rules doesnot say anything about it.

Hi,

I would like to differ from the below statement made by you in the above article:

Subsequent Meetings:

At least one meeting of Board of directors in each half of calendar year

Minimum Gap B/W two meetings at least 90 days.

I believe the Act does not prohibit the company from holding a board meeting within 90 days of the before board meeting.

hi

can anybody help in this…..

What if there are only 2 directors in a Pvt ltd co. and one of them is interested as he is giving loan to company.

How to comply with Quorum requirements?

Section 173 of The companies Act 2013 states that “Every company shall hold the first meeting of the Board of Directors within

thirty days of the date of its incorporation and thereafter hold a minimum number of four

meetings of its Board of Directors every year in such a manner that not more than one

hundred and twenty days shall intervene between two consecutive meetings of the Board”

Now “EVERY YEAR” is a “CALENDAR YEAR” or “FINANCIAL YEAR”???

What happen is gap between 2 board meetings of a small companies is less than 90 days.

sec. 118(10) of the companies act, 2013 talks about the secretarial standards. do we need to follow the same and baord meeting to be conducted in every quarter

Thanks a lot for giving such a thorough coverage. Could you please post similar compilation for other topics as well – general meetings, Directors provisions etc.

A very good compilation.

A very good compilation.

Please check the chart on Audit Committee composition- there seems to be error and random words in the chart.