The Indian government under the UPA II has abolished the Cost Audit and Costing methods for various industries under ( Cost Record and Audit ) Rules -2014 . In my research I went in deep into the different countries, developed as well as emerging economies over the span of last 10 years I find the development/growth & increased demand of Cost Management and improvement related to that across industries and business. I will share the research details in phased manner so that India could understand that what ‘OPPORTUNITY LOSS’ we would be facing during the next couple of years.

In the developed and emerging economies cost management has gained more importance due to the domestic and global competition getting severer by globalization, decreasing profit margins, increasing input prices due the tightening energy sources, economic crises etc. Therefore, companies which were operating in developing countries have also begun to implement cost and management accounting practices which were first adopted by companies operating in developed countries. In my research I have found that through adoption and efficient use of Cost Management and Costing methods economies and industrial revolution has taken new shapes and sizes.

Among the developing economies I will not be giving the old examples of China rather I will discuss about Turkey. Turkey economy faced one of the similar banking crises like U.S during pre-2001. Throughout the 1980s and 1990s, Turkey relied heavily on foreign investment for economic growth and there was huge burden of fiscal deficit. During the 1990s, economic growth fluctuated between -5.5% and 9.3% and the Turkey’s government ran large budget deficits, up to 7% of GDP in 1997. Interest rates on government debt exceeded the inflation rate, on average, by more than 30 percentage points. In short the economy was in the worst phase. But after 2001 getting funds from IMF and efficient use of business strategies and economic growth policies the economy made a turn around. The manufacturing back bone made a turnaround through the implementation of Cost Management methods and its various accounting aspects.

Turkish accounting profession has been in progress since the establishment of Turkish Republic. As a result of industrialization, the need for accounting profession emerged. This was also the prime reason behind adoption and implementation of Cost Management methods. Academics and Journals were flooded with the research papers on adoption of cost methods and practices depicting the growth model for their industries and economies.

Moving ahead, after conducting information from 40 industrial companies in Egypt its being found that Cost Accounting and Cost Management was being used more for external (pricing) purposes than for internal (performance) purposes. Now they have even adopted Activity Based costing for improving their cost profitability and increasing export. 12 years before in one of the research by an media institute it was found that Turkey around 51 companies out of the largest 500 industrial enterprise showed that

(1) 29.5 percent of the respondents utilize process costing, followed by activity-based costing (25.5 percent) and job costing (23.5 percent),

(2) direct materials cost has the largest portion in manufacturing costs, followed by manufacturing overhead and direct labor costs,

(3) the most widely used overhead allocation base is units produced (30 percent), followed by direct labor hours (23 percent), direct machine hours (15 percent),

(4) the most frequently used management accounting practices are cost-volume-profit analysis (72.6 percent), strategic profitability analysis (47.1 percent), flexible budgeting (45.1 percent), and customer profitability analysis (45.1 percent)

(5) Currently this statistical is present 100% in every costing method alternatively among the largest 500 companies in Turkey.

The effect of adoption of cost management and costing methods by Turkey are as follows:

- Turkey received foreign investment inflows of only US$18m 33 years ago when it started to host foreign investors. Now, the cumulative value of foreign investments has surged to US$138.3b.

- Despite the global economic crisis and the political and social issues that have afflicted neighboring regions, Turkey exported more goods in 2012 than ever before. Total exports

valued at US$152.6b were supplied to 241 countries and regions worldwide.

Better pricing and improved margins helped the Turkey industries to become competitive through judicious mix of Costing Methods and Process.

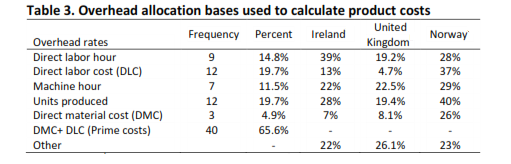

Companies have succeeded in their endeavors to reduce cost, focusing on operational efficiency, has turned pricing into an important issue for Turkish companies in achieving their sustainable growth targets as regional and global player. In my research I found out the historical use of Costing Methods in various industries in Turkey. Today that same number has grown by many folds. In 2002 when turkey started adopting cost management followed with comparison to UK & Ireland we find that overhead allocation being used to calculate the product cost are as follows:

Companies have succeeded in their endeavors to reduce cost, focusing on operational efficiency, has turned pricing into an important issue for Turkish companies in achieving their sustainable growth targets as regional and global player. In my research I found out the historical use of Costing Methods in various industries in Turkey. Today that same number has grown by many folds. In 2002 when turkey started adopting cost management followed with comparison to UK & Ireland we find that overhead allocation being used to calculate the product cost are as follows:

During the same time another research was conducted by an institute to find the level of adoption of cost management and costing methods by the various industries in Turkey. In that research it was found through statistical mean derivation that there was a huge implementation of cost methods. The importance of management accounting practices that are utilized in the business organizations in Turkey was measured on a scale of 1 (unimportant) to 5 (very important).

During the same time another research was conducted by an institute to find the level of adoption of cost management and costing methods by the various industries in Turkey. In that research it was found through statistical mean derivation that there was a huge implementation of cost methods. The importance of management accounting practices that are utilized in the business organizations in Turkey was measured on a scale of 1 (unimportant) to 5 (very important).

It’s quite surprising that the India being such an broad economy followed with a plan of GDP growth of 9% in the coming few years has dropped Cost Audit and Costing methods. Indian economy is quite running on the same tracks of Turkey’s economic crisis and this point of time it has been decided that by removing the Cost Management and Costing Methods it would be fruitful for the economy to grow. Industry might think that removing Costing Methods would help them to price their products better. But the biggest hurdle going forward will be intense competition of global markets. We all know that US and European markets are trying hard to come out of the recession. Now their manufacturing has started picking up but to gather momentum into the same they need to exploit markets and resources like India and other developing economies. Now if they start dumping their goods in India as these economies use Cost Management and methods as bible to their product manufacturing. Now the questions comes who Indian companies would sustain this dumping process of goods. If we Indian find cheap goods coming to India compared to domestic manufactured products would you not opt for the foreign brands? Global trade is required but not at the cost of domestic industries.

It’s quite surprising that the India being such an broad economy followed with a plan of GDP growth of 9% in the coming few years has dropped Cost Audit and Costing methods. Indian economy is quite running on the same tracks of Turkey’s economic crisis and this point of time it has been decided that by removing the Cost Management and Costing Methods it would be fruitful for the economy to grow. Industry might think that removing Costing Methods would help them to price their products better. But the biggest hurdle going forward will be intense competition of global markets. We all know that US and European markets are trying hard to come out of the recession. Now their manufacturing has started picking up but to gather momentum into the same they need to exploit markets and resources like India and other developing economies. Now if they start dumping their goods in India as these economies use Cost Management and methods as bible to their product manufacturing. Now the questions comes who Indian companies would sustain this dumping process of goods. If we Indian find cheap goods coming to India compared to domestic manufactured products would you not opt for the foreign brands? Global trade is required but not at the cost of domestic industries.

Cost Audit have been marked that sharing of technical cost related details and hence leakage of valuable information. Now just tell me that if there is no cost audit then how companies would be able to analyze their competitiveness and face the Technology related extension of their products and services from the market over the long term. How government will be able to stop dumping of goods by global competitors. How the FICCI,CII, ASSOCHAM,AMCHAM and other business houses would be able to present report of their respective trade and industries competiveness. How these houses would justify their cost of production with global standards. If, globally Costing methods and Cost Management is being adopted and practiced, in that context, India where the same have been abolished- how the Industry houses would justify the prices.

Now being a journalist I find that is the abolishment of Cost Audit and Costing Methods by UPAII is the master of plans of some dangerous foul play for the Indian economy. Is this abolishment is to attract the inflow of capital to Indian market to their own markets like US and Europe. By making the Indian industry weak through intense price competition with global products, asking Indian manufactures to close their shops in India and open manufacturing hub in US and Europe and route the inflow of capital back into their own economy (US & Europe). Well tell me how many war tanks you would buy every year compared to how many foot wear the Indian population buys (Said by Mr. Vijendra Sharma). Are we planning to close the domestic industries and make Indian economy a fragmented economy in the long term? While writing this I came across questions by my wife where I was asked that if you’re Costing Methods are so powerful then why not the inflation coming down. Well with costing methods inflation is around 10% zone without that it would have been more than 20%. What we are trying to make India understand is that without Cost Management the condition of India would be like US where US companies manufacture products and in China and sell in US itself.

A special thank to Mr. Amit Apte, Mr.Sanjay Bharghav & Mr. Vijendra Sharma for their inputs support & inspiration.

Indraneel Sen Gupta (neel19414@gmail.com )

Indraneel Sen Gupta (neel19414@gmail.com )

Global Macro Economic Researcher and Business Strategist

Master of Economics, MBA in International Business Management, ICWAI (Final)/CWM Final/Journalist

Author Bio

Great Article. Keep it up Indraneel