Contents of Bank Audit Manual 2017-18

1. Key Points

2. Asset Classification & Provisioning – a ready reckoner

3. Income Recognition & Asset Classification Norms – at a Glance

4. Important Points

5. Asset Classification – at a Glance

6. Important Audit Checks

7. Draft Management Representation Letter

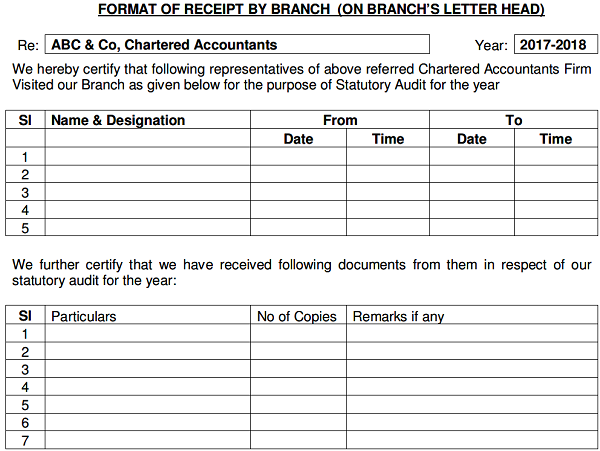

8. Format of Letter to Branch

9. Checklist for Audit of Advances accounts

10. Checklist for Audit of LFAR

11. Remuneration to Auditors

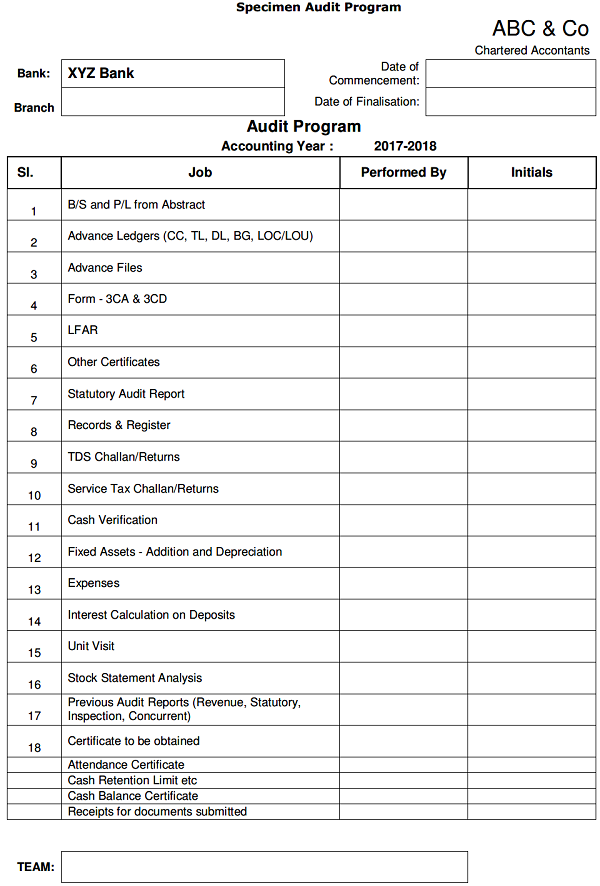

12. Overall Audit Plan- Audit Programme

13. Format of Certificate from Bank Branch

14. Audit Program for Branch Audit of a Bank

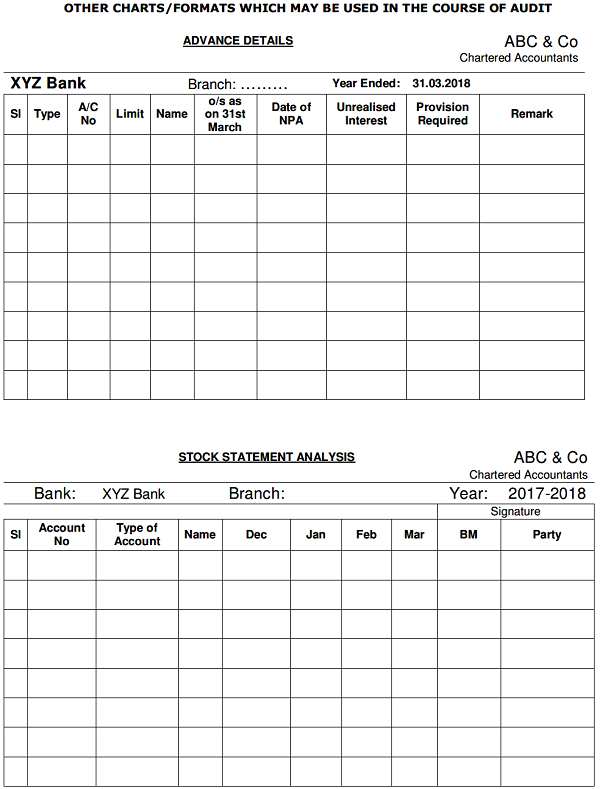

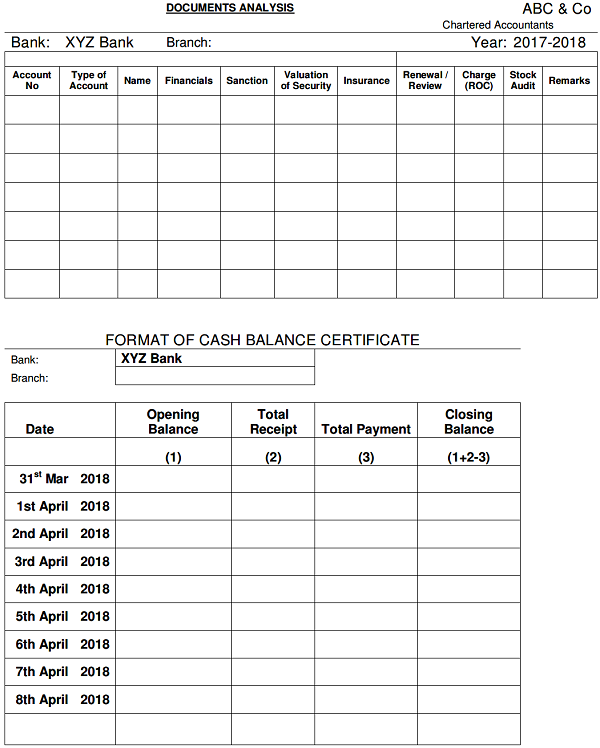

15. Other Charts / Formats (including Audit Report Format) which may be used during Audit

16. Prudential Guidelines on Restructuring of Advances by Banks

KEY POINTS

- Break Even Date for NPA is 01.01.2018 for the year 2017-2018

- Once an account has been classified as NPA, all the facilities granted to the borrower will be treated as NPA except in respect of Primary Agricultural Credit Societies (PACS)/Farmers Service Societies (FSS).

- Overdue period starts immediately on expiry of due date, concept of ‘past due’ has already been dispensed with in past years.

- Stock statements older than 3 months should not be considered

- Interest on advances (accrued and outstanding) should be calculated as on 31st March (few banks charges interest on advances few days prior to 31st March which should not be considered)

- Long outstanding entries (unexplainable and where there is no movement at all) in suspense account should be suggested for provisioning.

- ‘NIL’ MOC Certificate should be issued even if there is no MOC

- MOC should also be countersigned by Branch Manager (views of the BM if any has to be attached on a separate sheet duly signed by him)

- Submit all the REPORTS including TAX AUDIT REPORTS & LFAR immediately on completion of Audit and before leaving the branch

- Make a columnar list of documents to be submitted to branch/regional/zonal/other office before commencement of Audit. (it is advisable to get all documents in your custody duly signed by the Branch Manger at the beginning of Audit)

- Must get CERTIFICATE OF ATTENDENCE signed by Branch Manager in duplicate before leaving the branch

- Availability of security or net worth of borrower/guarantor should not be considered for the purpose of NPA recognition – it should always be based on recovery

- 100% provision is required for assets which has become doubtful for more than 3 years i.e. NPA date on or before 31.03.2014.

- To specifically report simultaneously to the CEO of the bank (and Audit Committee or Board as per the requirement of the Companies Act, 2013) and regional office of the Dept of Banking Supervision RBI where the HO of the bank is situated, any matter susceptible to be fraud or fraudulent activity or any foul play in any transactions. Any deliberate failure on part of the Auditors should render himself liable for action. If amount of fraud involve Rs 1 Crore or more – central office of the Dept of Banking Supervision, RBI, Mumbai (and Central Govt in Form ADT-4 as per the requirements of section 143(12) of the Companies Act, 2013 and Rules thereon) to be reported immediately.

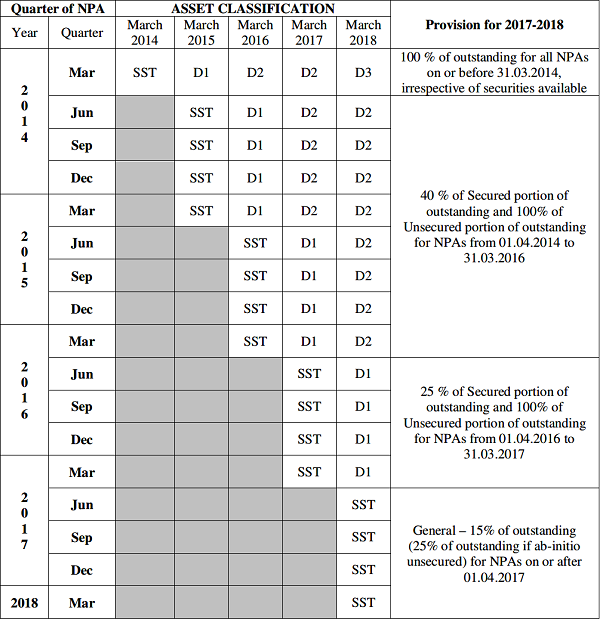

Asset Classification & Provisioning as on 31.03.2018 – A Ready Reckoner

INCOME RECOGNITION AND ASSET CLASSIFICATION NORMS – AT A GLANCE

1. An asset, including a leased asset, becomes non performing when it ceases to generate income for the bank.

2. Banks should, classify an account as NPA only if the interest due and charged during any quarter is not serviced fully within 90 days from the end of the quarter.

3. FACILITY WISE CHART:

| Credit Facility | Basis for treating a Credit Facility as NPA | Remarks |

| Term loans | Interest and/or instalment of principal remain overdue for a period of more than 90 days.

Agricultural Advances: Position upto 29th Sept 2004: In respect of advances granted for agricultural purposes where interest and/or instalment of principal remains overdue for a period of more than two harvest seasons but for a period not exceeding two half years, the advance should be treated as NPA. Position wef 30th Sept 2004: A loan granted for short duration crops will be treated as NPA, if the instalment of principle or interest remain overdue for two crop season and a loan granted for long duration crops will be treated as NPA, if the instalment of principle or interest remain overdue for one crop season Long duration crops means crops with crop season longer than one year Short duration crops are those other than long duration crops |

Overdue: An amount due to the bank under any credit facility is ‘Overdue’ if it is not paid on the due date fixed by the bank.

Crop Season: The crop season for each crop, which means the period up to harvesting of the crops raised, would be as determined by the State Level Bankers’ Committee in each State. |

| Cash Credits and Overdrafts | The account remains continuously “out of order” for a period of more than 90 days; i.e., outstanding balance remains continuously in excess of the sanctioned limit/drawing power

or there are no credits continuously for a period of 90 days as on the date of Balance Sheet or credits are not enough to cover the interest debited during the same period. |

Banks may not classify an account merely due to existence of some deficiencies, which are of temporary nature such as non-availability of adequate drawing power, balance outstanding exceeding the limit, non-submission of stock statements and non-renewal of the limits on the due date, etc.

However, generally stock statements older than three months would be deemed irregular and the working capital borrowal account will become NPA if such irregular drawings are permitted in the account for a continuous period of 90 days even though the unit may be working or the borrower’s financial position is satisfactory. Regular and ad hoc credit limits need to be reviewed/ regularised not later than three months from the due date/date of ad hoc sanction. In case of constraints such as non-availability of financial statements and other data from the borrowers, the branch should furnish evidence to show that renewal/ review of credit limits is already on and would be completed soon. In any case, delay beyond six months is not considered desirable as a general discipline. Hence, an account where the regular/ ad hoc credit limits have not been reviewed/ renewed within 180 days from the due date/ date of ad hoc sanction will be treated as NPA. |

| Bills Purchased and Discounted | The bills purchased/discounted remains overdue for a period of more than 90 days. | Overdue interest should not be charged and taken to income account in respect of overdue bills unless it is realised. |

| Securitisation Transaction | The amount of liquidity facility remains outstanding for more than 90 days | Securitisation Transaction undertaken in terms of guidelines dated 01.02.2006. |

| Derivative Transactions | the overdue receivables representing positive mark-to-market value of a derivative contract, if these remain unpaid for a period of 90 days from the specified due date for payment. | |

| Other Accounts | Any amount to be received in respect of that facility remains overdue for a period of more than 90 days. | |

| Government guaranteed advances | As on 31.03.2018, State government guaranteed advances and investment in State government guaranteed Securities would attract asset classification and provisioning norms if interest and/or principle or any other amount due to the bank remains overdue for more than 90 days.

|

The credit facilities backed by guarantee of Central government though overdue may be treated as NPA only when the government repudiates its guarantee when invoked. However, income shall not be recognised if the interest or instalment has remained overdue or the account has remained continuously out of order or the bills or any other facility has remained overdue for a period of more than 90 days. |

Important Points

| Key Words | Particulars | ||||||

| Exclusion | Undernoted categories of advances should be excluded, as NPA norms are not normally applicable to them:

|

||||||

| All Facilities | Once an account has been classified as NPA, all the facilities granted by a bank to a borrower and investment in all the securities issued by the borrower will have to be treated as NPA/NPI except in respect of advances granted under on-landing facility to Primary Agricultural Credit Societies (PACS)/Farmers Service Societies (FSS). Also, in respect of additional facilities sanctioned as per package finalised by BIFR and/or term lending institutions, provision may be made after a period of one year from the date of disbursement in respect of additional facilities sanctioned under the rehabilitation package. The original facilities granted would however continue to be classified as sub-standard/doubtful, as the case may be | ||||||

| Adequate Margin | Interest on advances against term deposits, NSCs, IVPs, KVPs and Life policies may be taken to income account on the due date, provided adequate margin is available in the accounts. Advances against gold ornaments, government securities and all other securities are not covered by this exemption. | ||||||

| Reversal of Income | Till the time the account is identified as NPA, income is recognised irrespective of whether realised or not. Where an account is identified as NPA during the year, unrealised income should not be recognised for the year. Banks should reverse the interest already charged and not collected by debiting Profit and Loss account, and stop further application of interest. However, banks may continue to record such accrued interest in a Memorandum account in their books. For the purpose of computing Gross Advances, interest recorded in the Memorandum account should not be taken into account. This will apply to Government guaranteed accounts also.

In respect of NPAs, fees, commission and similar income that have accrued should cease to accrue in the current period and should be reversed with respect to past periods, if uncollected. Leased Assets The finance charge component of finance income [as defined in ‘AS 19 Leases’ issued by the Council of the Institute of Chartered Accountants of India (ICAI)] on the leased asset which has accrued and was credited to income account before the asset became nonperforming, and remaining unrealised, should be reversed or provided for in the current accounting period. |

||||||

| Regularised before balance sheet date | The asset classification of borrowal accounts where a solitary or a few credits are recorded before the balance sheet date should be handled with care and without scope for subjectivity. Where the account indicates inherent weakness on the basis of the data available, the account should be deemed as a NPA. In other genuine cases, the banks must furnish satisfactory evidence to the Statutory Auditors/Inspecting Officers about the manner of regularisation of the account to eliminate doubts on their performing status. | ||||||

| Upgradation of loan accounts classified as NPAs | If arrears of interest and principal are paid by the borrower in the case of loan accounts classified as NPAs, the account should no longer be treated as non-performing and may be classified as ‘standard’ accounts. With regard to upgradation of a restructured/ rescheduled account which is classified as NPA contents please check master circular of RBI at the end of this booklet. | ||||||

| Fees and commissions (re-negotiations) | Fees and commissions earned by the banks as a result of re-negotiations or rescheduling of outstanding debts should be recognized on an accrual basis over the period of time covered by the re-negotiated or rescheduled extension of credit. | ||||||

| LOC or guarantees | If the debits arising out of devolvement of letters of credit or invoked guarantees are parked in a separate account, the balance outstanding in that account also should be treated as a part of the borrower’s principal operating account for the purpose of application of prudential norms on income recognition, asset classification and provisioning. | ||||||

| Appropriation of recovery in NPAs | Interest realised on NPAs may be taken to income account provided the credits in the accounts towards interest are not out of fresh/ additional credit facilities sanctioned to the borrower concerned.

In the absence of a clear agreement between the bank and the borrower for the purpose of appropriation of recoveries in NPAs (i.e. towards principal or interest due), banks should adopt an accounting principle and exercise the right of appropriation of recoveries in a uniform and consistent manner. |

||||||

| Income recognition | Income on NPA accounts to be recognized on realisation basis (conservative approach). However, banks may recognise income on accrual basis in respect of the projects under implementation, which are classified as ‘standard’. Funded Interest: Income recognition in respect of the NPAs, regardless of whether these are or are not subjected to restructuring/ rescheduling/ renegotiation of terms of the loan agreement, should be done strictly on cash basis, only on realisation and not if the amount of interest overdue has been funded. If, however, the amount of funded interest is recognised as income, a provision for an equal amount should also be made simultaneously. In other words, any funding of interest in respect of NPAs, if recognised as income, should be fully provided for. | ||||||

| Loans with moratorium for payment of interest

|

i. In the case of bank finance given for industrial projects or for agricultural plantations etc. where moratorium is available for payment of interest, payment of interest becomes ‘due’ only after the moratorium or gestation period is over. Therefore, such amounts of interest do not become overdue and hence do not become NPA, with reference to the date of debit of interest. They become overdue after due date for payment of interest, if uncollected.

ii. In the case of housing loan or similar advances granted to staff members where interest is payable after recovery of principal, interest need not be considered as overdue from the first quarter onwards. Such loans/advances should be classified as NPA only when there is a default in repayment of instalment of principal or payment of interest on the respective due dates. |

||||||

| Credit Card Accounts | In credit card accounts, the amount spent is billed to the card users through a monthly statement with a definite due date for repayment. Banks give an option to the card users to pay either the full amount or a fraction of it, i.e., minimum amount due, on the due date and roll-over the balance amount to the subsequent months’ billing cycle.

A credit card account will be treated as non-performing asset if the minimum amount due, as mentioned in the statement, is not paid fully within 90 days from the next statement date. The gap between two statements should not be more than a month. Banks should follow this uniform method of determining over-due status for credit card accounts while reporting to credit information companies and for the purpose of levying of penal charges, viz. late payment charges, etc., if any. |

||||||

| Signs of Stress

|

Illustrative list of signs of stress for categorising an account as SMA-0 1. Delay of 90 days or more in (a) submission of stock statement / other stipulated operating control statements or (b) credit monitoring or financial statements or (c) Non-renewal of facilities based on audited financials. 2. Actual sales / operating profits falling short of projections accepted for loan sanction by 40% or more; or a single event of non-cooperation / prevention from conduct of stock audits by banks; or reduction of Drawing Power (DP) by 20% or more after a stock audit; or evidence of diversion of funds for unapproved purpose; or drop in internal risk rating by 2 or more notches in a single review. 3. Return of 3 or more cheques (or electronic debit instructions) issued by borrowers in 30 days on grounds of non-availability of balance/DP in the account or return of 3 or more bills / cheques discounted or sent under collection by the borrower. 4. Development of Deferred Payment Guarantee (DPG) instalments or Letters of Credit (LCs) or invocation of Bank Guarantees (BGs) and its non-payment within 30 days. 5.Third request for extension of time either for creation or perfection of securities as against time specified in original sanction terms or for compliance with any other terms and conditions of sanction. 6. Increase in frequency of overdrafts in current accounts. 7. The borrower reporting stress in the business and financials. 8. Promoter(s) pledging/selling their shares in the borrower company due to financial stress. |

||||||

| Wilful Defaulters | The provisioning in respect of existing loans/exposures of banks to companies having director/s (other than nominee directors of government/financial institutions brought on board at the time of distress), whose name/s appear more than once in the list of wilful defaulters will be 5% in cases of standard accounts; if such account is classified as NPA, it will attract accelerated provisioning. This is a prudential measure since the expected losses on exposures to such borrowers are likely to be higher. It is reiterated that no additional facilities should be granted by any bank/FI to the listed wilful defaulters, in terms of paragraph 2.5 (a) of Master Circular of RBI on Wilful Defaulters dated July 1, 2014.

With a view to discouraging borrowers/defaulters from being unreasonable and non-cooperative with lenders in their bonafide resolution/recovery efforts, banks may classify such borrowers as non-cooperative borrowers, after giving them due notice if satisfactory clarifications are not furnished. Banks will be required to report classification of such borrowers to CRILC. Further, If any particular entity reported as non-cooperative, any fresh exposure to such a borrower will by implication entail greater risk necessitating higher provisioning. Banks/FIs will therefore be required to make higher provisioning as applicable to substandard assets in respect of new loans sanctioned to such borrowers as also new loans sanctioned to any other company that has on its board of directors any of the whole time directors/promoters of a non-cooperative borrowing company or any firm in which such a non-cooperative borrower is in charge of management of the affairs. However, for the purpose of asset classification and income recognition, the new loans would be treated as standard assets. This is a prudential measure since the expected losses on exposures to such non-cooperative borrowers are likely to be higher. |

ASSET CLASSIFICATION — AT A GLANCE

| Category | Conditions to be satisfied | Provision amount | Remarks |

| Standard Assets | Does not disclose any problem and which does not carry any more than normal risks attached to business | Agriculture/SME Adv – 0.25%

Commercial Real Estate (CRE) – 1% CRE-Residential Housing Sector – 0.75% HL (teaser rate period) – 2% Other Loan & Advances – 0.4% [ Special rates for restructured advances as mentioned in remarks column] |

Such an asset is not a NPA. [Provision requirement in case of Restructured account from Standard – 4.25% for 2014-15 ( for two years from restructuring /moratorium date), Restructured (upgraded from NPA to Standard) – as prescribed from time to time ( for one year from the date of upgradation)] |

| Sub-Standard Assets | Classified as NPA for a period not exceeding Twelve months.

Such an asset will have well defined credit weaknesses that jeopardise the liquidation of the debt and are characterised by the distinct possibility that the banks will sustain some loss, if deficiencies are not corrected. Classification of an asset should not be upgraded merely as a result of rescheduling, unless there is satisfactory compliance of the required conditions at least for one year. |

Unsecured Exposure means exposure where realizable value of security is not more than 10%, ab-initio, of the outstanding exposure. |

In respect of accounts where there are potential threats of recovery on account of erosion in the value of security or non-availability of security and existence of other factors such as frauds committed by borrowers, it will not be prudent for banks to first classify them as sub-standard and then as doubtful after expiry of 12 mths from the date the account has become sub-standard. Such accounts should be straightaway classified as doubtful or loss asset, as appropriate, irrespective of the period for which it has remained as NPA.

a. Erosion in the value of security can be reckoned as significant when the realisable value of the security is less than 50 per cent of the value assessed by the bank or accepted by RBI at the time of last inspection, as the case may be. Such NPAs may be straightaway classified under doubtful category. b. If the realisable value of the security, as assessed by the bank/ approved valuers/ RBI is less than 10 per cent of the outstanding in the borrowal accounts, the existence of security should be ignored and the asset should be straightaway classified as loss asset. |

| Doubtful Assets | Remained Substandard for a period of Twelve months. | 100% to the extent to which the advances are not covered by the realisable value of the security to which the bank has a valid recourse and the realizable value is estimated on realistic basis. Over and above the aforesaid, depending upon the period for which the asset has remained doubtful, provision on the secured portion to be made on the following basis:

1. Up to 1 year 25% 2. 1 to 3 years 40% 3. Over 3 years: 100% |

It has all the weaknesses inherent in that of a sub- standard asset with the added characteristic that the weaknesses make the collection / liquidation in full, highly questionable and improbable, on the basis of current known facts, conditions and values.

Stock Audit required in cases involving NPAs balances above 5 Crores. Valuation of Security to be done every three years. |

| Loss Assets | Loss asset is one where loss has been identified by the bank, external or internal auditors or the RBI inspection, but the amount has not been written off (wholly/partly). | 100% of the outstanding should be provided for/written off. | Such an asset is considered uncollectible and of such little value that its continuance as a bankable asset is not warranted although there may be some salvage or recoverable value. |

IMPORTANT AUDIT CHECKS

Deposit

(Term/Saving /Current /FCNR/NRE/NRNR)

- Verify transactions during the year relating to: New Accounts opened; Accounts closed; Dormant Accounts; Interest calculations; Scrutiny of account statements for unusual/large/overdraft transactions; Overdue Term deposits & its policies and practices of renewal; Accrual of interest; RBI Norms for Non-resident deposits & its operations – giving due importance to opening and operation of accounts like NRE, NRNR, FCNR, RFC, etc.; interest on various types of deposits; Tax Deducted at Source.

- Large deposits placed at the end of the year (probable window dressing).

- Examine unusual trend in account opening or account closing, dormant accounts that have suddenly been reactivated by heavy cash withdrawals or deposits, overdrawings, etc.

- Examine interest trends as compared to average annual deposits (monthly average figures).

ADVANCES

- Review monitoring reports (irregularity reports) sent by the branch to the controlling authorities in respect of irregular advances.

- Review appraisal system, Files of large as well as critical borrowers, sanctions, disbursement, renewals, documentation, systems, securities, etc.

- Review on test check basis operations in the Advances Accounts.

- Compliance of sanction terms and conditions in the case of new advances.

- Whether the borrower is regular in submission of stock statements, book debt statements, insurance policies, balance sheets, half yearly results, etc. and whether penal interest is charged in case of default/delay in submission of such data.

- Charge of interest and recovery for each quarter or as applicable to be verified.

- Review the monitoring system, i.e. monitoring end use of funds, analytical system prevalent for the advances, cash flow monitoring, branch follow-up, consortium meetings, inspection reports, stock audit reports, market intelligence (industry analysis), securities updation, etc.

- Check classification of advances, income recognition and provisioning as per RBI Norms/Circulars.

- Examine interest trends as compared to average annual advances (monthly average figures).

- Scrutinize the final advances statements with regard to assets classification, security value, documentation, drawing power, outstandings, provisions, etc.

- Check whether Non-Fund based (Letter of Credits/Bank Guarantees) exposure of the borrowers is within the sanctioned limits.

- Compare projected financial figures given at the time of project appraisal with actual figures from audited financial statements for relevant period and ascertain reasons for large variance.

Profit & Loss Account

- Income/Expenditure: Verify:

- Short debit of interest/commission on advances;

- Excess credit of interest on deposits;

- In case the discrepancies are existing in large number of cases, the auditor should consider the impact of the same on the accounts;

- Determine whether the discrepancies noticed are intentional or by error;

- Check whether the recurrence of such discrepancies are general or in respect of some specific clients;

- Proper authority in sanction and disbursement of expenses as also the correctness of the accounting treatment given as to revenue/capital/deferred expenses.

- Check accrual of income/expenditure especially for the last month of the financial year.

- Divergent Trends:

- Divergent trends in income/expenditure of the current year may be analysed with the figures of the previous year.

- Wherever a divergent trend is observed, obtain an explanation along with supporting evidences like monthly average figures, composition of the income/expenditure, etc.

Balance Sheet

Cash & bank balances

- Physically verify the cash balance/ATM cash balance as on March 31, 2017 or reconcile the cash balance from the date of verification to March 31, 2017.

- Confirm and reconcile the balances with banks as on March 31, 2017.

Investments

- Physically verify the investments held by the branch on behalf of Head Office and issue certificate of physical verification of investments to bank’s Investments Department.

- Check receipt of interest and its subsequent credit to be given to Head Office.

Advances provisioning

- As per RBI norms, unrealised interest on NPA accounts should be reversed and not charged to “Advance Accounts”. Reversal of unrealised interest of previous years in case of NPA accounts is required to be checked.

- Partial recovery in respect of NPA accounts should be generally appropriated against principal amount in respect of doubtful assets.

Fixed assets

Check inter-branch transfer memos relating to fixed assets and whether they have been correctly classified in the accounts and depreciation accounting thereof.

Inter Branch Reconciliation (IBR)

- Understand the IBR system and accordingly prepare an audit plan to review the IBR transactions. The large volume of Inter Branch Transactions and the large number of unreconciled entries in the banking system makes the area fraud-prone.

- Check up head office inward communication to branch to ascertain date up to which statements relating to inter-branch reconciliation have been sent.

Check and report

- Reversal of any large/old/unexplained entries, which had remained outstanding in IBR.

- Items of revenue nature, cash-in-transit (for example, cash meant for deposit into currency chest) which remains pending for more than a reasonable period.

- Double responses to the entries in the accounts.

- Test check accuracy and correctness of “Daily statements” which are prepared by the branch and sent to IOR department.

The auditor should duly consider the extent of non-reconciliation in forming his opinion on the financial statements. Where the amounts involved are material, the auditor should suitably qualify his audit report. Attention is drawn on the paper on “Certain Significant Aspect of Statutory Audit of banks” issued by the Council of ICAI in March 1994, published in the C. A. journal.

Further, vide its circular No. BP.BC.22/21.04.018/99 dated March 24, 1999, the Reserve Bank of India (RBI) advised the banks to maintain category-wise (head-wise) accounts for various types of transactions put through inter-branch accounts so that the netting can be done category-wise. Further, RBI advised banks to make 100 percent provision (category-wise) for net debit position in their inter-branch accounts arising out of the unreconciled entries, both debit and credit, outstanding for more than two years.

Suspense accounts, sundry deposits, etc.

Suspense accounts are adjustment accounts in which certain debit transactions are temporarily posted whose authorisation is pending for approval.

Sundry Deposit accounts are adjustment accounts in which certain credit transactions are temporarily posted whose authorisation is pending for approval.

As and when the transactions are duly authorised by the concerned officials they are posted to the respective accounts and the Suspense account/Sundry Deposit account is credited/debited respectively.

- Ask for and analyse their year-wise break-up.

- Check the nature of entries parked in such Accounts.

- Check any movement in such old balances and whether the same is genuine and has been properly authorised by the competent authority.

- Check for any revenue items lying in such accounts and whether proper treatment has been given for the same.

Auditors Report & Memorandum of Changes

- The Auditors Report should be a self contained document and should contain no reference of any point made in any other report including the LFAR;

- Include Audit Qualifications in the Auditors Report and not in the LFAR;

- Quantify the Audit Qualifications for a better appreciation of the point made to the reader;

- For suggesting any changes in the financial statements of the branch, quantify the same in the Memorandum of Changes (MOC) and make it a subject matter of qualification and annexe it to the Auditors Report. Summary of Memorandum of Changes (MOC) is required to be given in Auditors Report as per revised format as issued by ICAI.

Long Form Audit Report (LFAR)

- Study the LFAR Questionnaire thoroughly;

- Plan the LFAR work along with the statutory audit right from day one;

- The LFAR questionnaire is a useful tool for planning the statutory audit of a bank’s branch;

- Complete and submit the Auditors Audit Report as well as the LFAR simultaneously;

- Be specific while replying the LFAR;

- Give instances of shortcomings/weaknesses existing in the respective areas of the branch functioning in the LFAR;

- Advances check-list for giving list of accounts with adverse features;

- The LFAR should be sufficiently detailed and quantified so that they can be expeditiously consolidated by the bank.

System

- Review off-site backup and daily backup procedure of Bank

- Exception reports viz. password errors, limit verification, irregular advances

- Custodian of pass word and unauthorized access of password, computer room

- Periodical report to controlling authority on functioning of computerised system and compliance of controlling authority instructions in this respect

General

- Send a letter of your requirements to the branch before commencing the audit.

- Obtain the latest status of cases involving fraud, vigilance and matters under investigation having effect on the accounts and its reporting requirement.

- Obtain a Management Representation Letter (MRL)

- Obtain a certificate from Branch-in-charge on specific issues (format as per page 33 )

Draft of Management Representation Letter to be obtained from the Branch Management

Date: ____________

M/s. XYZ & Co.

Chartered Accountants

Mumbai

Dear Sirs,

Sub.: Audit for the period ended 31-3-2018

This representation letter is provided in connection with your audit of the financial statements of _____________ branch of _______________ BANK for the period ended 31-3-2018 for the purpose of expressing an opinion as to whether the financial statements give a true and fair view of the financial position of ___________ branch of _______________ BANK as of 31-3-2018 and of the results of operations for the period then ended. We acknowledge our responsibility for preparation of financial statements in accordance with the requirements of the Reserve Bank of India and recognised accounting policies and practices, including the Accounting and Auditing Standards issued by the Institute of Chartered Accountants of India.

We confirm, to the best of our knowledge and belief, the following representations:

ACCOUNTING POLICIES

1. The accounting policies, which are material or critical in determining the results of operations for the period or financial position are set out in the financial statements and are consistent with those adopted in the financial statements for the previous period. The financial statements are prepared on accrual basis except as stated otherwise in the financial statements.

ASSETS

2. The branch has a satisfactory title to all assets and there are no liens or encumbrances on the company’s assets.

FIXED ASSETS

3. The net book values at which fixed assets are stated in the balance sheet are arrived at:

- after taking into account all capital expenditure on additions thereto, but no expenditure properly chargeable to revenue;

a. after eliminating the cost and accumulated depreciation relating to items sold, discarded, demolished or destroyed;

b. after providing adequate depreciation on fixed assets during the period.

CAPITAL COMMITMENTS

4. At the balance sheet date, there were no outstanding commitments for capital expenditure excepting those disclosed in Note No. ___ to the financial statements.

INVESTMENTS

5. The current investments as appearing in the balance sheet consist of only such investments as are by their nature readily realisable and intended to be held for not more than one year from the respective dates on which they were made. All other investments have been shown in the balance sheet as `long-term investments’.

6. Current investments have been valued at the lower of cost or fair value. Long-term investments have been valued at cost, except that any permanent diminution in their value has been provided for in ascertaining their carrying amount.

7. In respect of offers of right issues received during the year, the rights have been either been subscribed to, or renunciated, or allowed to lapse. In no case have they been renunciated in favour of third parties without consideration which has been properly accounted for in the books of account.

8. All the investments produced to you for physical verification belong to the entity and they do not include any investments held on behalf of any other person.

9. The entity has clear title to all its investments including such investments which are in the process of being registered in the name of the entity or which are not held in the name of the entity. There are no charges against the investments of the entity except those appearing in the records of the entity.

LOANS AND ADVANCES

10. The following items appearing in the books as at 31st March, 2017 are considered good and fully recoverable with the exception of those specifically shown as “doubtful” in the Balance Sheet:

Loans and Advances Rs.

OTHER CURRENT ASSETS

11. In the opinion of the Board of Directors, other current assets have a value on realization in the ordinary course of the company’s business, which is atleast equal to the amount at which they are stated in the balance sheet.

CASH & BANK BALANCES

12. The cash balance as on 31st March, 2017 is Rs.______.

The bank balances as on ________________ is as under:

__________________ Bank Rs.______________

__________________ Bank Rs.______________

__________________ Bank Rs.______________

LIABILITIES

13. We have recorded all known liabilities in the financial statements.

14. We have disclosed in notes to the financial statements all guarantees that we have given to third parties and all other contingent liabilities.

15. Contingent liabilities disclosed in the notes to the financial statements do not include any contingencies, which are likely to result in a loss and which, therefore, require adjustment of assets or liabilities.

PROVISIONS FOR CLAIMS AND LOSSES

16. Provision has been made in the accounts for all known losses and claims of material amounts.

17. There have been no events subsequent to the balance sheet date, which require adjustment of, or disclosure in, the financial statements or notes thereto.

PROFIT AND LOSS ACCOUNT

18. Except as disclosed in the financial statements, the results for the period were not materially affected by:

- Transactions of a nature not usually undertaken by the bank;

a. Circumstances of an exceptional or non-recurring nature;

b. Charges or credits relating to prior years;

c. Changes in accounting policies.

GENERAL

19. The following have been properly recorded and, when appropriate, adequately disclosed in the financial statements:

Losses arising from sale and purchase commitments.

a. Agreements and options to buy back assets previously sold.

b. Assets pledged as collateral.

20. There have been no irregularities involving management or employees who have a significant role in the system of internal control that could have a material effect on the financial statements.

21. The financial statements are free of material misstatements, including omissions.

22. The company has complied with all aspects of contractual agreements that could have a material effect on the financial statements in the event of non-compliance. There has been no non-compliance with requirements of regularity authorities that could have a material effect on the financial statements in the event of non-compliance.

23. We have no plans or intentions that may materially affect the carrying value or classification of assets and liabilities reflected in the financial statements.

24. The branch has not received any notice, show cause, inspection advice, etc. from Government of India, Reserve Bank of India or any other monitoring authority of India that could have a material effect on the financial statements.

For & on behalf of

___________ branch of _______________ Bank

Authorised Signatory

Draft Letter of Requirements to be sent to the Branch

April 1, 2017

The Branch Manager

_____________ Bank

_____________ Branch

Mumbai

Dear Sir:

Sub.: Statutory Audit of your branch for the year 2017-2018

As you are aware, we have been appointed as the Statutory Auditor to report on the accounts of your Branch for the year 2017-2018.

Our Tentative Program for Branch Visit is as below:

………………………………………………………………………………………………..

In order to enable us to finalise the audit programme and furnish our report on the audit of the accounts for the year 2017-2018 of your branch, may we request you to keep ready the information/clarification as stated below and make the same available to our audit team at the earliest.

a. Latest Reports The following latest reports on the accounts of your bank, and compliance by the bank on the observations contained therein may be kept ready for our perusal:

a. Latest RBI Inspection Report;

b. Internal/Concurrent Audit Reports;

c. Previous Statutory Audit Report

d. Head Office Inspection Reports;

e. Internal Inspection Reports;

f. Revenue Audit Report (if any);

g. Income and Expenditure Control Report (if any);

h. Report on any other Inspection/Audit that may have been conducted during the course of the year relevant to the financial year 2017-2018.

b. Circulars in connection with accounts

Please let us have a copy of the Head Office circulars/instructions in connection with the closing of your accounts for the year, to the extent not communicated to us or incorporated in our letter of appointment.

c. Accounting policies

Kindly confirm whether, as compared to the earlier year, there are any changes in the accounting policies during the year under audit.

If so, please let us have a list and a copy of the accounting policy/ies amended by the bank during the year covered by the current audit and compute the financial effect thereof to enable us to verify the same.

d. Balancing of books

Kindly confirm the present status of balancing of the subsidiary records with the relevant control accounts. In case of differences between balances in the control and subsidiary records, please give the details thereof and let us know the efforts being made to reconcile/balance the same. This information may be given head-wise for the relevant control accounts, indicating the date when the balances were last tallied.

e. Deposits

a. Please let us have the interest rate structure, applicable for the current year, for all the types of deposits accepted by the branch.

b. Kindly confirm having transferred Overdue/Matured Term Deposits to Current Account Deposit. If not, details/particulars of credit balances comprising Overdue/Matured Term Deposits as at the year-end which continue to be shown as Term Deposit, particularly where the branch does not have any instructions/communication for renewal of such deposits from the account holder and amount of provision of interest made on such overdue/matured term deposits, should be separately marked out and be kept ready for our reference.

b. Advances

a. Kindly confirm whether in respect of the advances against tangible securities, the branch holds evidence of existence and latest market value of the relevant securities as at the year-end.

b. Kindly inform the year-end status of the accounts, particularly those which have been adversely commented upon in the latest reports of RBI/Internal Auditors/Concurrent Auditors/Statutory Auditors, etc. on the branch as also accounts in respect of which provisions have been made/recommended as at the previous year-end.

Information in relation to such advances accounts where provision computed/recommended may please be prepared indicating:

a. Name of the borrower

b. Type of facility

c. * Total amount outstanding as at the year-end (both for principal and interest) specifying the date up to which interest has been levied and recovered.

d. Particulars of securities and value on the basis of latest report/statement.

e. Nature of default and action taken.

f. Brief history and present status of the advance.

g. * Provision already made/recommended.

h. NPA since when (please specify the date)

* Corresponding figures for the previous year-end may please be given.

c. Kindly confirm whether the borrowers’ account have been categorised according to the norms applicable for the year into Standard, Sub-standard, Doubtful or Loss assets, with special emphasis on Non-Performing Assets (NPA) and whether such classification has also been made applicable by the branch to advances with balances of less than Rs. 25,000 each.

Kindly confirm whether you have examined the accounts and applied the norms borrower-wise and not account-wise for categorising the accounts. Please let us have the particulars of provisions computed/recommended in respect of the above during the financial year under audit.

d. A list of all advances accounts which have been identified as bad/doubtful accounts and where pending formal sanction of the higher authorities, the relevant amount have not been re-classified/re-categorised in the book of the branch for provision/write off. This covers all account identified by the branch or internal/external auditor or by RBI inspectors but the amount has not been written-off wholly or partly.

In case the bank has recommended action against the borrowers or for initiating legal or other coercive action for recovery of dues, a list of such borrowers’ accounts may be furnished to us.

e. Please let us have a list of borrowers’ accounts where classification made as at the end of the previous year has been changed to a better classification, stating reasons for the same.

f. Kindly also confirm whether any income has been adjusted/recorded to revenue, contrary to the norms of income recognition notified by the Reserve Bank of India and/or Head Office circulars issued in this regards; and particularly where the chances of recovery/realisability of the income are remote.

Kindly also confirm whether any income has been recorded on Non-Performing Accounts other than on actual realisation.

c. Outstanding in Suspense/Sundry Account

Kindly let us have a year-wise/entry-wise break up of amounts outstanding in Suspense/Sundry accounts as on 31-3-2018. Kindly explain the nature of the amounts in brief. Supporting evidences relating to the existence of such amounts in the aforesaid accounts may be kept ready at the branch for verification. Reasons for non-adjustment of items included in these may be made known.

d. Inter-branch/Office Accounts/Head Office Account

a. Please let us have a statement of entries (head-wise) which originated prior to the year-end at other branches, but were responded during the period after 31-3-2018 at the branch.

b. Date-wise details of debits in various sub-heads relating to Inter-Branch transactions and reasons for outstanding amounts particularly those, which are over 30 days as at the Balance Sheet date.

e. Contingent liabilities

a. Kindly confirm whether other than for advances, there are any matters involving the bank in any claims in litigation, arbitration or other disputes in which there may be some financial implications, including for staff claim, municipal taxes, local levies etc. If so, these may be listed for our verification, and you may confirm whether you have included these as contingent liabilities.

b. Kindly confirm whether guarantees are being disclosed net of margins, or otherwise as at the year-end, and whether the expired guarantee where the claim year has also expired, continue to be disclosed in the branch return. Please confirm specifically.

f. Interest provision

a. Kindly confirm whether interest provision has been made on deposits etc. in accordance with the latest instruction of the RBI/interest rate structure of the bank. A copy of such instructions/rate structure may be made available for our scrutiny.

b. Kindly confirm whether any amount recorded as income up to the year-end, which remains unrecovered or not realisable, has been reversed from any of the income heads or has been debited to any expenditure head during the financial year. If so, please let us have details to enable us to verify the same.

c. Kindly confirm the accounting treatment as regards reversal, if any of interest/other income recorded up to the previous year-end; and the amount reversed during the year under audit; i.e., income of earlier years derecognised during the year.

g. Foreign currency outstanding transactions

a. Kindly confirm whether amount outstanding as at the year-end have been converted as at the year-end rates prescribed by FEDAI. An authenticated copy of the FEDAI rates applied may be given for our records.

b. Kindly confirm the amount of inward value of foreign currency parcels, if any, which originated prior to the year-end from other banks, but could not be recorded as these were in transit and for which entries were made after the year end.

h. Investment/Stationery

For Investment held by the branch:

a. These may be produced for physical verification and/or evidence of holding the same be made available.

b. Stock of unused security paper stationery/numbered forms like B/Rs, SGL forms, etc. may please be produced for physical verification.

c. It may be confirmed whether income accrued/collected has been accounted as per the laid down procedure.

d. It may be confirmed whether Investment Valuation has been done as per the extant RBI guidelines.

i. Long Form Audit Report – Branch response to the Questionnaire

In connection with the Long Form Audit Report, please let us have complete information as regards each item in the questionnaire, to enable us to verify the same for the purpose of our audit.

j. Tax Audit in terms of section 44AB of the Income-tax Act, 1961

Please let us have the information required for the tax audit under section 44AB of the Income-tax Act, 1961 to enable us to verify the same for the purpose of our report thereon.

k. Other certification

Please furnish us the duly authenticated information as regards other matters, which as per the letter of appointment require certification.

l. Bank reconciliation and confirmations

Please let us have the duly reconciled statements for all Nostro as well as Local bank accounts. A copy of the year-end balance confirmation statements should also be called for and kept ready for our review.

m. Books of account and records

Kindly keep ready all the books of accounts and other records like vouchers, documents, fixed assets register, etc. for our verification.

We shall appreciate your kind co-operation in the matter.

Thanking you,

Yours truly,

Chartered Accountants

Check-list for Audit of Advance Accounts

1. Name of the borrower

2. Address

3. Constitution

4. Nature of business/activity

5. Other units in the same group

6. Total exposure of the branch to the Group – Fund based (Rs. in lakhs) – Non-fund based (Rs. in lakhs)

7. Name of Proprietor/Partners/Directors

8. Name of the Chief Executive, if any

9. Asset classification by the branch

a. during the current year

b. during the previous year

10. Asset classification by the Branch Auditor

a. during the current year

b. during the previous year Are there any adverse features pointed out in relation to asset classification by the Reserve Bank of India Inspection or any other audit.

11. Date on which the asset was first classified as NPA (where applicable)

12. Facilities sanctioned:

| Date of Sanction | Nature of facilities | Limit (Rs. in Lakhs) |

Margin% | Balance outstanding at the year-end | Prime security | Collateral security | |

| Current Year | Previous Year | ||||||

| Provision made: Rs.________ lakhs | |||||||

13. Whether the advance is a consortium advance or an advance made on multiple-bank basis

14. If Consortium,

a. names of participating banks with their respective shares

b. name of the Lead Bank in Consortium

15. If on multiple banking basis, names of other banks and evidence thereof

16. Has the Branch classified the advance under the Credit Rating norms in accordance with the guidelines of the controlling authorities of the Bank

17. a. Details of verification of primary security and evidence thereof;

b. Details of valuation and evidence thereof

| Date verified | Nature of security | Value | Valued by |

| Insured for Rs. _______ lakhs (expiring on ________) | |||

18. i. Details of verification of collateral security and evidence thereof

ii. Details of valuation and evidence thereof

| Date verified | Nature of security | Value | Valued by |

| Insured for Rs. _______ lakhs (expiring on ________) | |||

19. Give details of the guarantee in respect of the advance

a. Central Government guarantee;

b. State Government guarantee;

c. Bank guarantee or financial institution guarantee;

d. Other guarantee

Provide the date and value of the guarantee in respect of the above.

20. Compliance with the terms and conditions of the sanction Terms and Conditions

Compliance

I. Primary Security

i. Charge on primary security

ii. Mortgage of fixed assets

iii. Registration of charges with Registrar of Companies

iv. Insurance with date of validity of policy

II. Collateral Security

i. Charge on collateral security

ii. Mortgage of fixed assets

iii. Registration of charges with Registrar of Companies

iv. Insurance with date of validity of policy

III. Guarantees – Existence and execution of valid guarantees

IV. Asset coverage to the branch based upon the arrangement (i.e., consortium or multiple-bank basis)

V. Others:

i. Submission of Stock Statements/Quarterly Information Statements and other Information Statements

ii. Last inspection of the unit by the Branch officials: Give the date and details of errors/omissions noticed

iii. In case of consortium advances, whether copies of documents executed by the company favouring the consortium are available

21. Key financial indicators for the last two years and projections for the current year (Rs. in lakhs)

| Indicators | Audited year ended 31st March___ | Audited year ended 31st March___ | Estimates for year ended 31st March ___ |

| Turnover | |||

| Increase in turnover % over previous year | |||

| Profit before depreciation, interest and tax | |||

| Less: Interest | |||

| Net Cash Profit before tax | |||

| Less: Depreciation | |||

| Less: Tax/Net Profit after | |||

| Depreciation and Tax | |||

| Net Profit to Turnover Ratio | |||

| Capital (Paid-up) | |||

| Reserves | |||

| Net Worth | |||

| Turnover to Capital Employed Ratio (The term capital employed means the sum of Net Worth and Long Term Liabilities) | |||

| Current Ratio | |||

| Stock Turnover Ratio | |||

| Total Outstanding Liabilities/total Net Worth Ratio | |||

| In case of listed companies, Market Value of Shares

a. High; b. Low; and c. Closing |

|||

| Earnings Per Share | |||

| Whether the accounts were audited? If yes, up to what date; and are there any audit qualifications |

22. Observations on the operations in the account:

| Excess over drawing power | Excess over limit | |

| 1. No of occasions on which the Balance exceeded the drawing power/sanctioned limit (give details) | ||

| Reasons for excess drawings, if any | ||

| Whether excess drawings were reported to the Controlling Authority and approved |

–

| Debit summation (Rs. in lakhs) |

Credit summation (Rs. in lakhs) |

|

| 2. Total summation in the account during the year | ||

| Less: Interest | ||

| Balance |

23. Adverse observations in other audit reports/Inspection Reports/Concurrent Auditor’s Report/Internal Audit Report/Stock Audit Report/Special Audit Report or Reserve Bank of India Inspection with regard to:

1. Documentation;

2. Operations;

3. Security/Guarantee; and

4. Others

24. Branch Manager’s overview of the account and its operation.

25. 1. In case the borrower has been identified/classified as Non-performing Asset during the year, whether any unrealised income including income accrued in the previous year has been accounted as income, contrary to the Income Recognition Norms.

2. Whether any action has been initiated to recover accounts identified/classified as Non-performing Assets.

Date:

Signature and Seal

of Branch-in-Charge

Advances checklist for LFAR

a) In respect of common irregularities, the Auditors can give their comments borrower-wise in the format given hereunder:

| Name of borrower | Name of branch | Region | IRAC status | Sanctioning authority | Facility | Limit | Amount o/s. as at the year end | Irregularity No. |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

b) In respect of Column 9 above, “Irregularity No.”, the number as given in the “Glossary to Irregularities” in Point 5, under the head “Item” below should be given for the irregularity applicable to respective borrower.

In case the auditors feel that in spite of the list of irregularities given below, there are some other irregularities, which the auditor would like to bring to notice, the auditor may separately disclose under the given head by giving “appropriate number”.

For the aforesaid purpose, “appropriate number” would mean, for example, if the auditors feels that in case of “Review/Monitoring/Supervision”, which has the number “4”, any additional irregularity has to be incorporated, he may give a number after the last number appearing in the list such as “4.52”, and onwards. Similarly in case of “Credit Appraisal” which has the number “1”, any additional irregularity may be given “1.14”, and so on.

c) The borrower-wise details may be given in descending order based on the Amount outstanding.

d) In addition to the above, auditors wanting to give notes in respect of Critical Advances (large or small) with gross irregularities should give the same as per the format given in “Point 6” below.

e) GLOSSARY TO IRREGULARITIES

Item REMARK

1. Credit Appraisal

1.1 Loan application not on record at branch.

1.2 The appraisal form was not filled up correctly and thereby the appraisal and assessment was not done properly.

1.3 Loan application is not in the form prescribed by Head Office.

1.4 The bank did not receive certain necessary documents and Annexures required with the application form.

1.5 Basic documents such as Memorandum & Articles of Association, Partnership deed, etc., which are a pre-requisite to determine the status of the borrower, not obtained.

1.6 Certain adverse features of the borrower not incorporated in the appraisal note forwarded to the management.

1.7 Industry/group exposure and past experience of the bank is not dealt in the appraisal note sent to the management for sanction.

1.8 The level for inventory/book-debts/creditors for finding out the working capital is not properly assessed.

1.9 Techno-economic feasibility report, which is required to know the technical aspects of the borrower’s business, is not obtained from Technical Cell.

1.10 Credit report on principal borrowers and confidential report from their banks are not insisted from the borrowers.

1.11 The opinion reports of the associate and/or sister concerns of the borrower are not scrutinised.

1.12 The opinion reports of the associate and/or sister concerns of the borrower are not called for.

1.13 The opinion reports of the associate and/or sister concerns of the borrower are not updated.

1.14 The opinion reports of the associate and/or sister concerns of the borrower are not satisfactory.

1.15 The opinion reports of the associate and/or sister concerns of the borrower are not scrutinised/called for/not updated/not satisfactory.

1.16 The procedure/instructions of head office regarding preparation of proposals for grant not followed.

1.17 The procedure/instructions of head office regarding preparation of proposals for renewal of advances not followed.

1.18 The procedure/instructions of head office regarding preparation of proposals for enhancement of limits, etc. not followed.

1.19 No exposure limits are fixed for forward contract for foreign exchange sales/purchase transactions.

2. Sanctioning and disbursement

2.1 Credit facility sanctioned beyond the delegated authority or limit of the branch

2.2 Certain proposals were sanctioned pending approval of higher authorities wherever required.

2.3 Ad hoc limits were granted for which sanctions were pending since long.

2.4 Facilities were disbursed before completion of documentation.

2.5 Facilities were disbursed without following sanction terms.

2.6 Facilities were disbursed without any sanction.

2.7 Sanction letter was missing in the branch.

2.8 Guarantor as required in the sanction letter was not obtained.

2.9 Required promoters stake not invested before disbursement of loan.

2.10 Sanctions were made without proper appraisal.

2.11 Security charge not created before disbursement as required by sanction letter/renewed letter.

2.12 Full disbursement of the facility not made.

2.13 Sanction terms were not complied with or were not recorded.

2.14 Disbursement made without proper sanction.

2.15 Term loan was disbursed by creating the cash credit or savings account of the borrower.

3. Documentation

3.1 The security against which the advance was sanction was not available/was not on record.

3.2 Mortgage for the property given as security is not created.

3.3 Mortgage for the property given as security created, was inadequate, as compared to terms of sanction.

3.4 Second charge as required, on assets is not created in favour of the bank.

3.5 Documents of second charge on assets is not on the record.

3.6 Documents pertaining to registration of charges with ROC or any other concerned authority requiring charging of assets is not obtained.

3.7 Copies evidencing lodgment of the original conveyance/sale deeds with the Sub-Registrars for registration not on record.

3.8 Authority letter/Power of Attorney to the bank to collect the original documents from the Sub-Registrar not on record.

3.9 Documents pertaining to consortium advances not yet executed/not available with bank.

3.10 Documents signed by persons not duly authorised to sign or who have signed in other capacity accepted by the bank.

3.11 Signatures of the executants were not found on all the pages of the documents

3.12 Some of the documents on record were blank, without signatures of Branch Manager, witnesses, or guarantors, etc.

3.13 Revival letters in respect of documents to be reviewed from the borrowers not received.

3.14 Guarantors have expired.

3.15 Guarantors not on record.

3.16 uarantors not renewed.

3.17 Guarantors not assigned.

3.18 Worth of the guarantors not available.

3.19 Stamping not as per the amended Stamps Act.

3.20 Documents have become mutilated, soiled, time barred or not obtained.

3.21 Opinion report by the field officer for the borrowers not found on record.

3.23 “Nil Encumbrance Certificate/s” or “No Dues Certificate/s” or “No Lien Letters” not obtained for the mortgage/s.

3.24 Advances for vehicle loans, Registration certificate, transfer certificate, etc. not obtained.

3.25 Work completion certificate, sale deeds, share certificates in societies, etc. not on record for housing loans.

3.26 Documents are not duly attested/signed by concerned officials/not renewed.

3.27 The agreements for hypothecation do not contain details regarding goods hypothecated.

3.28 Copy of Bills/receipts, on the basis of which the amount was disbursed not found on record. For example Vehicle Loans, Plant and Machinery.

3.29 Charge on main &/or collateral securities not created in terms of sanction letter.

3.30 Original security papers/sale deed/lease deed/title deed/agreement of sale not available on record.

3.31 TDR are not discharged or renewed.

3.32 Control returns not sent to the H.O.

3.33 The branch has not taken any action for not compliance with terms of agreement

3.34 No documents executed for enhancement of limit/document not on record.

3.35 ECGC post shipment policy not obtained.

3.36 Credit facility released without execution of all necessary documents.

3.37 Common Seal not affixed on Letter of Comfort.

3.38 Confirm orders for export credit not found on record for facilities released.

4. Review/Monitoring/Supervision

4.1 The account is frequently overdrawn.

4.2 The account is continuously overdrawn.

4.3 The account is overdrawn and the branches have not taken sufficient steps to regularise the accounts promptly.

4.4 The balance outstanding have exceeded the drawing power.

4.5 Balance confirmation and acknowledgment of debt not obtained.

4.6 The stock, book-debts statements not received regularly/promptly.

4.7 The FFI/financial statements/audited statements/FFR 1 & 2/other operational data, etc., not received regularly/promptly.

4.8 The stock, book-debts statements, etc., not scrutinised and no suitable action is taken.

4.9 The FFI/financial statements/audited statements/FFR 1 & 2/other operational data, etc., not received regularly/promptly/not scrutinised and no suitable action is taken.

4.10 Non-moving stock is not deducted to arrive at the drawing power.

4.11 The age-wise break-up of debtors is not found on record. The borrowers are allowed to draw money on entire outstanding debt, which must rather be for the recent debts as prescribed for particular industries and as per margin prescribed in the sanction letter.

4.12 Wide discrepancies observed in the stock statements and stock figures in the annual audited financial statements.

4.13 No penal interest has been charged for delay in submission of various statements as per the terms of agreement depending upon the type of loan/credit availed by the borrower.

4.14 Many branches have not adhered to the prescribed frequency of physical verification of securities given against loans and advances.

4.15 Drawing power limits are not revised as per market value of shares for advances against security of shares.

4.16 End-use of funds not ensured/not known funds utilised for purpose other than for which granted.

4.17 The projections submitted by the borrower stay far beyond the actual performance. Further, no explanation for the same is taken from the borrower.

4.18 Major sale proceeds of the borrower not routed through the bank.

4.19 Audited statements of non-corporate borrowers having limit beyond Rs. 10 lakhs not received.

4.20 Renewal proposals of advances not received on time and in many cases the limits are not renewed.

4.21 Application of wrong rate of interest, processing charges, commission, other charges, etc. resulting in income leakage/excess booking of interest of the Bank.

4.22 Insurance cover for stock/property is inadequate/not on record/not renewed/not endorsed in favour of the Bank.

4.23 Inspection/physical verification of security charged, not been carried out.

4.24 xpired bills/foreign currency sight bills which are outstanding, have not been crystallised.

4.25 EBW statements on write-off of overdue export bills of ECM not found on record.

4.26 Confirmation as to genuineness of export transactions not obtained from Bank’s foreign offices/correspondents/customs department.

4.27Import credit, bill of entry evidencing import of goods not found.

4.28 Documents are not obtained for bills discounted under Letter of Credit.

4.29 Advances, which are eligible for whole turnover packing credit guarantee cover of ECGC, are not brought under its cover.

4.30 Though government guaranteed accounts are irregular since long, the issue of invocation of guarantee does not seem to have been considered.

4.31 Prescribed margins not maintained as per sanctions.

4.32 Allocated limits, full terms of sanctions, stock statements, inspection reports, margin, etc. not available at monitoring branches.

4.33 For allocated limits, inordinate delays were noticed in responding to transfer by the allocator branch.

4.34 Regular meetings not held with other consortium members to review the performance of borrowers and to assess the current state of affairs/not been held as per norms.

4.35 Individual members of the consortium are not advised about the quarterly operating limits/D. P. allocated to each one of them.

4.36 Minutes of the consortium meetings not found on record/not been held as per norms.

4.37 Inspection report from the consortium members not obtained.

4.38 The capital of the borrower has eroded/networth is negative/decreasing. Close monitoring needs to be done.

4.39 The drawing power is calculated wrongly and/or hence the borrower is allowed to enjoy excess credit than actually eligible.

4.40 Signboard of SBI is not displayed in godown, where the pledged/hypothecated stock is stored.

4.41 Limit not fully utilised by the borrower/No commitment charge is levied for the limit not fully utilised by the borrower.

4.42 Loan against TDR/STDR, which is matured, is neither renewed nor credited to loan account.

4.43 The Stock and Debtors Audit Report not found on record. No audit has been done for accounts of the borrower.

4.44 The valuation report in respect of tangible security from government approved valuer have not been obtained.

4.45 Guarantees, Opinion Reports Financial statements, IT assessment orders and etc. of the guarantor are not found on record.

4.46 Opinion report on guarantor is not obtained.

4.47 For small Government sponsored loan accounts, security cover could not be ascertained since neither any record was available at branch nor physical verification conducted by the branch.

4.48 Pre-sanctions and/or post-sanctions inspection reports were not on record.

4.49 The account was overdue for repayment and/or no credit was received from the borrower for a long time.

4.50 The borrower is absconding or deceased and legal formalities are incomplete and there is wilful default from the borrower. Either establishment was closed or security was disposed of or no action taken by the branch.

4.51 Subsidy claim process was incomplete or subsidy was yet to be received or needs follow-up.

4.52 Security disposed of/entity closed by borrower and no action taken by the branch.

4.53 Irregularity not advised to controllers.

4.54 Letter of subordination of deposits not taken.

4.55 Secured and unsecured portion not segregated properly in advance return of the branch.

4.56 Renewal of limits was done before the receipt of financial statements.

4.57 Heavy cash withdrawal for which consent of corporate Guarantor is not taken.

4.58 Proper valuation of stock not done/needs critical scrutiny.

4.59 Security obtained is inadequate/lower as compared to amount of outstanding/no collateral security.

4.60 The party was dealing with other bank also tough it was not permitted.

4.61 Sticky accounts require close follow-up by the management.

5. Bad and doubtful advances

5.1 The IRAC norms for classification of advances were not followed and the same is implemented through Memorandum of Changes by auditors during audit.

5.2 Instalments were not received from the borrowers.

5.3 Interest was not received from the borrowers.

5.4 Legal action for recovery of advances was not taken although authorised by the Board/Controlling Authority.

5.5 Discontinuance of application of interest not followed although authorised by the Board/Controlling Authority.

5.6 Government guarantees have expired and fresh guarantees not obtained/not renewed.

5.7 Terms of the BIFR scheme not complied.

5.8 Payment from government not received although guarantees were unconditional, irrevocable and payable on demand.

5.9 Delays in the settlement/repayment in respect of sanctioned proposals.

5.10 The repayment accepted in case of compromise cases inadequate vis-à-vis value of security.

5.11 Compromise proposals pending at various levels where local government/outside agencies are involved as guarantors.

5.12 Copy of Search Report not on record.

5.13 Decree awarded but no further steps taken for recovery.

5.14 DI&CGC claims submitted/rejected/pending data not available.

5.15 Irregular/sticky advance not reported to the controlling authority promptly.

5.16 Compromise/OTS proposal is recommended and is under negotiation since long but not finalised. Suit is filed in the court/DRT and pending to be finalised.

5.17 ECGC claim not submitted/lodged for recovery.

f) Format for reporting Large/Irregular Advances

Name of the Branch & Region :

Name of the Borrower :

Asset Classification (IRAC Status) :

(Rupees in lakhs)

| Facility | Sanctioned Limit | Drawing Power | Outstanding as on 31.3.2015 |

| Fund based: | |||

| Non-Fund based: | |||

g) Security :

h) Primary :

i) Collateral :

Financial performance :

Operational comments :

Other comments (if any) :

Remuneration payable to the Statutory Central and Branch Auditors from the year 2012-2013 as per RBI circular No. DBS.ARS.No.BC. 08/ 08.92.001/ 2012-13 June 25, 2013

A. Remuneration for Branch Audit work of the Bank

| Category of bank branch

(on the basis of quantum of advances) |

Rates of audit fees

(Rs.) |

| Up to Rs. 10 crore | 40250/- |

| Above Rs. 10 crore up to Rs. 20 crore | 57500/- |

| Above Rs. 20 crore up to Rs. 30 crore | 79350/- |

| Above Rs. 30 crore up to Rs. 50 crore | 120750/- |

| Above Rs. 50 crore up to Rs. 75 crore | 138000/- |

| Above Rs. 75 crore up to Rs. 125 crore | 182850/- |

| Above Rs. 125 crore up to Rs. 175 crore | 228850/- |

| Above Rs. 175 crore up to Rs. 300 crore | 287500/- |

| Above Rs. 300 crore up to Rs. 500 crore | 324300/- |

| Above Rs. 500 crore up to Rs. 1000 crore | 359950/- |

| Above Rs. 1000 crore up to Rs. 5000 crore | 395600/- |

| Above Rs. 5000 crore | 431250/- |

The main operating office of the bank (irrespective of the fact whether it is attached to Head / Central Office of the bank or functions as a separate unit), CPUs/LPUs/and other centralized hubs by whatever nomenclature called which are taken up for the purpose of statutory branch audit during a particular year so as to cover 90% of advances of a bank will be treated as any other branch and the fees admissible for the audit work thereof will be on the basis of the above mentioned schedule.

For branches where there is no advances portfolio such as service branches, specialised branches etc., or those operating as NPA recovery branches the banks, in consultation with the Audit Committee of the Board, should propose the revised fees depending on the volume of business of the branches, existing fee, etc. for the approval of RBI on a case to case basis.

B. Fees for LFAR

| Head Office / Controlling Offices | 25% of the basic audit fee excluding fee for scrutiny and incorporation of branch returns. |

| Branches | 10% of the basic audit fee payable for audit of respective branch. |

In respect of branches below the cut-off point of the threshold limit of branches to be taken up for statutory audit, as stipulated from time to time, which may not generally be subjected to statutory audit but are subjected to concurrent audit by chartered accountants and where LFARs and other certifications done earlier by SBAs are required to be submitted by the concurrent auditors, the fees payable to the concurrent auditors may be based on the above prescription.

No separate TA/HA shall be payable for LFAR / Tax Audit of Head / Controlling Offices and branches.

C. Fees for additional certifications

It has been decided that an additional remuneration @ 12% of the basic audit fees shall be payable for the following certifications/validations required to be made in terms of various circulars/guidelines issued by RBI and any other certification/validation included from time to time as per RBI requirements.

i) Verification of SLR requirements under Section 24 of BR Act, 1949 on 12 odd dates in different months in a year, not being Fridays.

ii) A certificate to the effect that the bank has been following RBI guidelines regarding (a) asset classification, (b) income recognition (c) provisioning, and also to the effect that the bank has followed RBI guidelines in regard to the investment transactions/treasury operations.

iii) A certificate in respect of reconciliation of bank’s investments (on own account as also under PMS).

iv) A certificate for compliance in key areas by the banks.

v) A certificate in respect of custody of unused BR forms.

vi) Authentication of bank’s assessment of Capital Adequacy Ratio in the ‘Notes on Accounts’ attached to the balance sheet and various other ratios / items to be disclosed in the ‘Notes on Accounts’.

vii) Certificate regarding loan portfolio review if the bank seeks World Bank assistance (Capital Restructuring Loan).

viii) Certification regarding DICGC items.

ix) Verification of SLR and CRR returns submitted by the bank to RBI during the period under audit and confirming the same to RBI and the bank under audit.

x) To comment upon the status of compliance by the bank as regards the implementation of the recommendations of the Ghosh Committee and the Working Group on internal controls.

xi) Commenting upon the credit deposit ratio in the rural areas as per the instructions of Government of India.

xii) Reporting of instances of suspected fraud if any, noticed during the course of statutory audit as per Mitra Committee Recommendations.

As hitherto, no fee is payable to branch auditors for additional attestations.

D. Fees for additional certifications required by Securities and Exchange Board of India (SEBI)

As regards fee for additional certificates / attestations prescribed by SEBI and other regulators, the banks may decide in consultation with the Audit Committee of the Board/ Board.

E. Fees for auditing of consolidated financial statements