Accounting for Deferred Tax Assets and Liabilities: A Comparative Analysis under Ind AS 12 and IAS 12

Abstract / Executive Summary

This article provides an expert-level examination of accounting for deferred tax assets and liabilities under Ind AS 12 – Income Taxes and the corresponding international framework IAS 12 – Income Taxes . Using practical numerical illustrations and corporate-style case studies for manufacturing, banking, NBFC and IT entities, the discussion explains the identification of temporary differences, measurement of deferred tax, interaction with the Indian Income-tax Act, and implications for presentation, disclosure and accounting policies. The paper adopts a balance-sheet approach, focusing on the tax base of assets and liabilities, and highlights how differences between accounting profit and taxable profit must be analysed to ensure faithful representation and prudence in recognising deferred tax assets.

Keywords:

Deferred tax asset; Deferred tax liability; Ind AS 12; IAS 12; temporary differences; tax base; carry forward losses; MAT; sector case studies.

1. Conceptual Framework of Deferred Tax under Ind AS 12 and IAS 12

Financial reporting. Tax reporting. Two frameworks with overlapping but not identical objectives. Accounting standards seek faithful representation of performance and position. Tax law seeks revenue mobilisation, administrative simplicity and policy outcomes. Deferred tax is the bridge between these two worlds.

Under Ind AS 12 and IAS 12 , the core idea is the balance sheet approach . An entity compares the carrying amount of each asset and liability in the financial statements with its tax base under applicable tax law. Any difference that will reverse in future and affect taxable profit creates a temporary difference . Taxing that difference at the applicable tax rate yields a deferred tax asset (DTA) or deferred tax liability (DTL).

Permanent differences — such as expenses never allowable for tax or income permanently exempt — do not give rise to deferred tax. Only timing / temporary differences that eventually reverse are considered.

2. Temporary Differences – Classification and Recognition Rules

Taxable temporary differences give rise to deferred tax liabilities . These arise when carrying amount of an asset exceeds its tax base, or the tax base of a liability exceeds its carrying amount. Future taxable profit will be higher when the difference reverses.

Deductible temporary differences give rise to deferred tax assets . These arise when carrying amount of an asset is lower than its tax base, or when liabilities / provisions are recognised for accounting purposes but allowed as deduction only on payment basis under tax law.

Recognition of a DTL is almost universal except for specific initial recognition exemptions . Recognition of a DTA, however, is conditioned on probable availability of future taxable profits against which the deductible temporary differences can be utilised. Prudence. Evidence-based estimates. Business plans. Past profitability records.

3. Numerical Illustration – Deferred Tax Liability on Accelerated Depreciation

Consider an Indian manufacturing company purchasing plant and machinery for ₹10,00,000 on 1 April Year 1. For accounting under Ind AS 16, it depreciates the asset on a straight-line basis over 5 years. For tax under the Income-tax Act, assume accelerated depreciation of 40% WDV in Year 1 and subsequent years.

At the end of Year 1, the carrying amount for accounting purposes is ₹8,00,000 (cost ₹10,00,000 less ₹2,00,000 straight-line depreciation). For tax purposes, written-down value is ₹6,00,000 (cost less 40% = ₹4,00,000 tax depreciation).

Thus, carrying amount (₹8,00,000) > tax base (₹6,00,000). A taxable temporary difference of ₹2,00,000 arises. If the applicable tax rate is 25%, the entity must recognise a Deferred Tax Liability of ₹50,000.

Journal entry at the end of Year 1:

Income Tax Expense (P&L) …………….. Dr ₹50,000

To Deferred Tax Liability (Balance Sheet) ₹50,000

The total income tax expense disclosed in the statement of profit and loss will therefore include both current tax (based on taxable income as per return) and deferred tax (arising from temporary differences).

4. Numerical Illustration – Deferred Tax Asset on Provision Allowed on Payment Basis

Assume the entity recognises a provision for leave encashment of ₹4,00,000 in Year 1 as per Ind AS 19. However, under the Income-tax Act, such provision is allowed as deduction only when actually paid. Therefore, for Year 1 tax computation, this ₹4,00,000 is disallowed and added back.

Carrying amount of the liability in books: ₹4,00,000. Tax base: nil , because no deduction has yet been claimed. This creates a deductible temporary difference of ₹4,00,000. At a tax rate of 25%, the entity recognises a Deferred Tax Asset of ₹1,00,000, subject to assessment of future taxable profits.

Journal entry:

Deferred Tax Asset (Balance Sheet) …….. Dr ₹1,00,000

To Deferred Tax Income (P&L) ₹1,00,000

5. Sector-Specific Case Studies

5.1 Banking Company – Provisioning and Stage-wise ECL under Ind AS 109

A scheduled commercial bank applies Ind AS 109 – Financial Instruments to compute Expected Credit Loss (ECL) on its loan portfolio. Accounting provisions are often higher and earlier than provisions permitted under the Income-tax Act or regulatory norms. For tax, specific NPA provisions may be deductible only to the extent prescribed, and general provisions may be disallowed.

Result. Carrying amount of loans (net of ECL) is lower than the tax base (loans less limited tax-allowable provisions). This creates deductible temporary differences , typically resulting in significant DTAs. Management must evaluate the bank’s capital position, profitability trends and regulatory environment before recognising DTAs in full.

5.2 NBFC – Ind AS Transition and Volatility in Deferred Tax

Many NBFCs experienced large fair value adjustments on adoption of Ind AS – particularly on financial assets classified at fair value through profit or loss (FVTPL) or other comprehensive income (FVOCI). Where tax continues to follow realisation or accrual principles without fair value, substantial temporary differences appear on the balance sheet date.

Example. An NBFC holds a bond portfolio carried at fair value of ₹50 crore with tax base of ₹42 crore. Unrealised fair value gain of ₹8 crore sits either in profit or loss or OCI. For tax, this gain is not yet taxable. The entire ₹8 crore is a taxable temporary difference and gives rise to a DTL. Classification of the related deferred tax in P&L or OCI must follow the classification of the underlying gain.

5.3 Manufacturing Entity – Revaluation Surplus and Deferred Tax

A manufacturing company elects the revaluation model under Ind AS 16 for its land and buildings. On revaluation, the carrying amount of land increases from ₹5 crore to ₹8 crore, with revaluation surplus of ₹3 crore recognised in Other Comprehensive Income and accumulated in equity.

Tax base remains at historical cost less depreciation (if any), say ₹5 crore. The temporary difference of ₹3 crore is taxable in nature. The entity recognises a DTL (for example at 25%, ₹0.75 crore) with a corresponding charge to OCI, since the underlying revaluation gain is also in OCI. This maintains consistency of recognition.

5.4 IT Services Company – Share-based Payments and Deductibility Mis-match

An IT company grants employee stock options (ESOPs). Under Ind AS 102 – Share-based Payment , it recognises employee compensation expense over the vesting period based on grant-date fair value. For tax, deduction may be linked to intrinsic value on exercise or to amounts recorded in books, depending on law / rulings.

Where tax deduction differs from accounting charge — in amount or timing — temporary differences arise. The entity must compute the tax base of the related equity or liability component and recognise a DTA or DTL. Careful tracking is required because some portion may be credited directly to equity, affecting the location of deferred tax recognition.

6. Comparison of Ind AS 12 and IAS 12 – High Level Perspective

| Area | Ind AS 12 | IAS 12 |

| Approach | Balance sheet approach; tax base vs carrying amount; largely converged with IAS 12. | Balance sheet approach; global benchmark for deferred tax. |

| Initial recognition exemptions | Similar exemptions, including certain assets and liabilities on initial recognition. | Same principle; practical guidance widely available. |

| Presentation | Current vs deferred tax split; offsetting subject to legal enforceability. | Broadly similar presentation and offsetting requirements. |

| OCI / Equity items | Deferred tax recognised in OCI or equity in line with underlying item. | Same principle – follow the underlying line item. |

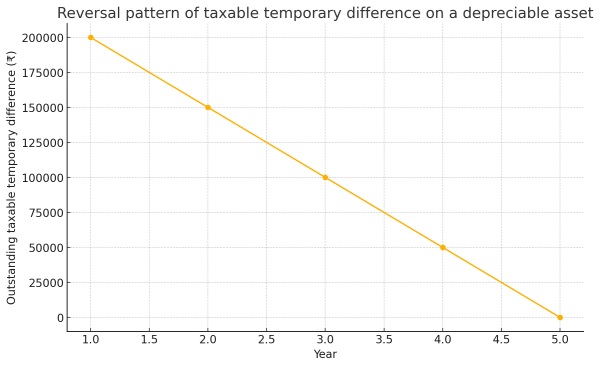

7. Illustrative Chart – Reversal of Taxable Temporary Difference over Time

The following chart illustrates a simplified pattern of a taxable temporary difference on a depreciable asset gradually reversing over five years. Actual profiles may vary depending on useful life, tax rate changes and additional capital expenditure.

8. Compliance Checklist – Deferred Tax under Ind AS 12 / IAS 12

| Key Question | Yes / No / Remarks |

| Have all material temporary differences been identified by comparing tax base and carrying amount? | |

| Are DTAs recognised only to the extent that future taxable profits are probable? | |

| Is the tax rate used consistent with enacted or substantively enacted rates at the reporting date? | |

| Are DTAs and DTLs appropriately classified and offset only where legally enforceable? | |

| Is deferred tax relating to OCI or equity items recognised in the same component? | |

| Have significant judgements and assumptions around DTAs been disclosed in notes? | |

| Are prior-period deferred tax balances reconciled and analysed for reversals and new differences? |

9. Presentation, Disclosure and Accounting Policies

In the statement of profit and loss, total tax expense is split into current tax and deferred tax . Reconciliation between accounting profit and tax expense is presented, often as a note reconciling the effective tax rate with the statutory rate.

In the balance sheet, DTAs and DTLs are generally presented as non-current. Offsetting is allowed only when the entity has a legally enforceable right to set off current tax assets against current tax liabilities and the deferred taxes relate to the same taxation authority and taxable entity.

Notes to accounts typically include: (a) breakdown of deferred tax by major types of temporary differences; (b) movement schedule of DTAs and DTLs; (c) details of unrecognised DTAs on losses or credits; and (d) disclosure of significant judgements around recoverability of DTAs.

Illustrative Accounting Policy Extract – Income Taxes and Deferred Tax

“Income tax expense comprises current and deferred tax. Current tax represents the expected tax payable on taxable profit for the year, using tax rates enacted or substantively enacted at the reporting date, and any adjustment to tax payable for previous years. Deferred tax is recognised on temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the corresponding tax bases. Deferred tax assets are recognised to the extent that it is probable that future taxable profits will be available against which the temporary differences can be utilised. Deferred tax is measured at tax rates expected to apply when the temporary differences reverse, based on laws enacted or substantively enacted at the reporting date. Deferred tax relating to items recognised outside profit or loss is recognised outside profit or loss, in line with the underlying item.”

10. Conclusion

Deferred tax accounting is no longer a mere compliance exercise. It is an analytical discipline that connects management’s view of business performance with the realities of tax law. Under Ind AS 12 and IAS 12, the focus on temporary differences and the balance sheet approach demands robust data, cross-functional coordination between finance and tax teams, and clear documentation of judgements.

Well-designed processes around deferred tax — identification, measurement, review and disclosure — enhance the credibility of financial statements and help users understand how current tax strategies will affect future cash outflows and earnings. For entities in banking, NBFC, manufacturing and IT sectors, the stakes are even higher because the magnitude and volatility of temporary differences can be substantial.

Author Bio