Earlier, payment for exports was to be received from the overseas buyer named in the Export Declaration (EDF) and currency of such payment should be as per the final destination of the goods/services irrespective of residential status of the buyer.

Similarly, payment for import should be made to the original overseas seller of the goods and importer needs to satisfy that goods equivalent to remittance have been imported.

While this is great news, it is still a struggle for exporters in India to send their goods overseas. Many of the difficulties they face have been around for years, decades even. Unless these are urgently addressed, India might never reach its full export potential.

With a view to liberalize the procedure relating to payments for exports/imports and taking into account evolving international trade practices Reserve Bank of India had incorporated regulatory measure on third-party payments for export / import transactions vide circularA. P. (DIR Series) Circular No.70 dated 8th November 2013. Further Foreign Trade Policy 2015-2020 has incorporated provisions for Third party exports vide para 9.60 and 2.42.

What is Third-Party:

A third party is someone who is not one of the main people involved in a business agreement or legal case but who is involved in it in a minor role. Third-party does not have a direct connection with a legal transaction but he might be affected by it.

An assessee who supplies goods and services may not have the infrastructure to undertake the export. Hence, the assessee may utilize the services of an intermediary for carrying out the export transaction. The intermediary is known as the third-party exporter and the supplier of the exported goods and services is known as the manufacturer exporter.

Understanding of Third-party transactions:

When a buyer and seller enter into a business deal, they may decide to use the services of an intermediary or third party who manages the transaction between both parties. For example: If a company X sells inventory to its subsidiary, company Y, a third-party transaction occurs when company Y sells those final goods to company Z. A third-party transaction often involves a seller, a buyer and intermediary.

Para 9.60 of FTP 2015-2020

“Third-party exports” means exports made by an exporter or manufacturer on behalf of another exporter(s). In such cases, export documents such as shipping bills shall indicate names of both manufacturer exporter/manufacturer and third-party exporter(s). Bank Realisation Certificate (BRC), Self-Declaration Form (SDF), export order and invoice should be in the name of third-party exporter.

Para 2.42 of FTP 2015-2020

Third party exports (except Deemed Export) as defined in Chapter 9 shall be allowed under FTP. In such cases, export documents such as shipping bill shall indicate name of both manufacturing exporter/manufacturer and third-party exporter(s). Bank Realization Certificate (BRC), Export Order and Invoice should be in the name of third-party exporter.

So, in third-party exports an individual or entity (exporter) makes an export on the behalf of another individual or entity (exporter or manufacturer). In such cases, export documents such as shipping bills shall indicate name of both exporter and third-party exporter. BRC, FIRC, GR Declaration, export order and invoice should be in the name of third-party exporter.

Advantages of Third-party Exports:

In case of third-party exports manufacturer need not register with Reserve Bank of India because the third-party who are obtaining foreign exchange receipts should register with the Reserve Bank of India. Under a third-party export, the foreign inward remittance from the customer is received by the third-party exporter. The inward remittance is received in foreign currency. However, the settlement between the third-party exporter and the manufacturer exporter is made in Indian rupees. Hence, the manufacturer exporter need not undertake the procedure for conversion of foreign exchange. By making use of the services of the third-party exporter, the manufacturer exporter can concentrate on the core business activities. The manufacturer exporter can make use of the expertise of the third-party exporter. The third-party exporter helps the manufacturer exporter to procure orders from the customers.

How Third-party Export works:

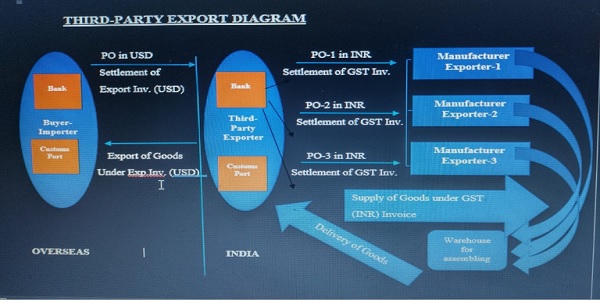

1. The third-party exporter obtains export order from the final buyer (Importer)

2. After obtaining the purchase order from the overseas buyer, the third-party exporter will raise back-to-back purchase order to the manufacturer exporter at a lesser price.

3. Manufacturer exporter will despatch goods from their warehouses to defined destination.

4. After getting delivery of goods from the manufacturer exporter, the third-party exporter will finally despatch goods to the final buyer in his name and obtains foreign exchange from overseas buyer (importer).

5. The third-party exporter then pays the value of goods to the manufacturer exporter against GST invoice in Indian rupees.

THIRD-PARTY EXPORT DIAGRAM

Conditions of Third-party Exports:

1. The manufacturer exporter and third-party exporter both should be resident of India.

2. The exports needs to be completed within 90 (ninety) days from the date of GST invoice.

3. In export documents the manufacturer and the third-party exporter should be mentioned jointly.

4. The concessional rates of GST are available on the export of goods only.

5. Both the third-party exporter and the manufacturer exporter should have a valid GST Registration.

6. The third-party exporter and the manufacturer exporter should not have made a consecutive default in filing GST returns. The condition should be satisfied for the preceding six months.

7. The supply of goods from the manufacturer exporter to the third-party exporter should take place through a GST invoice.

8.The GST registration particulars of both the third-party explorer and the manufacturer explorer should be available in the shipping bill.

9. The third-party exporter should be registered with an Export Promotion Council (EPC). The registration should be approved by Department of Commerce.

10. The third-party exporter should move the goods from the premises of the manufacturer exporter to any of the following places:

a) The port, airport, land customs station or inland container depot from which the export is scheduled to take place

b) A registered warehouse as a temporary transit point before the goods are moved to a port, land customs station, inland container depot or airport from which the export is scheduled to take place.

11. If the registered recipient intends to aggregate supplies from multiple registered suppliers and then export, the goods from each registered supplier shall move to a registered warehouse and after aggregation, the registered recipient shall move goods to the Port, Inland Container Deport, Airport or Land Customs Station from where they shall be exported.

12. In case of situation referred to in condition 11, the registered recipient shall endorse receipt of goods on the tax invoice and also obtain acknowledgement of receipt of goods in the registered warehouse from the warehouse operator and the endorsed tax invoice and the acknowledgment of the warehouse operator shall be provided to the registered supplier as well as to the jurisdictional tax officer of such supplier

13. When goods have been exported, the registered recipient shall provide copy of shipping bill or bill of export containing details of Goods and Services Tax Identification Number (GSTIN) and tax invoice of the registered supplier along with proof of export general manifest or export report having been filed to the registered supplier as well as jurisdictional tax officer of such supplier.

14. The registered supplier shall not be eligible for exemption if the registered recipient fails to export the said goods within a period of ninety days from the date of issue of Tax invoice.

15. The export invoice should be made in foreign currency based on purchase order received from overseas buyer(importer).

16. The consecutive purchase order(s) to be placed by the third-party exporter to manufacturer exporter should be in Indian Rupees.

17. The overseas buyer will remit export proceeds against export of goods to the third-party exporter and the same will be knocked off by the third-party exporter against FOB value mentioned in shipping bill.

18. On receipt of funds from overseas buyer the third-party exporter will settle GST invoice raised by the manufacturer exporter in Indian Rupees.

19. To avail the benefit under RoSCTL/RoDTEP incentive scheme all players must have valid IEC and need to register in ICEGATE.

20. A Duty Credit Scrip is issued by the Director General of Foreign Trade (DGFT) and can be used to pay various duties/taxes to the Central Govt but cannot be used for payment of GST. These are issued to both Exporters of Goods as well as Exporters of Service.

21. These duty credit scrips are issued is to offset the infrastructural inefficiencies and associated costs involved in the export of goods/products which are produced/ manufactured in India.

22. These scrips are freely transferable and there is no conditionality attached with these scrips. If the holder of the scrip does not intend to use these scrips for any of the above-mentioned purpose or is not able to use the duty credit scrips during the validity period, he may sell them to any other person interested in using them for any of the above-mentioned purpose.

23. If the holder of these Duty Credit Scrips does not intend to use them for any of the above-mentioned purposes, he may sell them in the open market. These scrips usually sell at a discount to their face value and can be sold either directly to a buyer or through an agent who will help you find a buyer.

24. For eg: If you have a Duty Credit Scrip worth Rs. 1,00,000, it means that it can be used to pay duties/ taxes equivalent to Rs. 1,00,000. If the holder of the scrip does not intend to use them – he may sell them.

- The sub-vendors of these scrip will not pay full face value for these scrips but will buy them at a discount. He may buy these scrips for Rs. 95,000 instead of Rs. 1,00,000. Although, he has purchased them for Rs. 95,000 – these scrips still have a face value of Rs. 1,00,000 and can be used for payment of duties/taxes equivalent to Rs. 1,00,000.

1. Benefit of the sub-vendor – He saved Rs. 5,000 in the above-mentioned transaction as instead of paying Rs. 1,00,000, he only had to pay Rs. 95,000.

2. Benefit to the main vendor – He got a benefit of Rs. 95,000 because if he would not have sold these scrips – they would have expired and therefore useless.

25. The holder of these scripts mainly use them either for payment of customs duty or sell them to an Importer in cash and the importer then uses these scripts for the payment of his own custos duty.

26. Duty credit scripts can only be passed on to main vendors and sub-vendors electronically.

27. Similarly main vendors can also pass on duty credit scripts to sub-vendors electronically at discounted rate.

28. Discounted duty credit scripts can be transferred to main vendor account in cash.

29. Face value of duty credit script would remain same, and the beneficiary can utilize the same to settle expenses as explained earlier.

30. If the main vendor has partial capacity and placed simultaneous PO to sub-vendor shipping bill to be filed in two parts. One shipping bill should be exclusively in the name of main vendor as he had produced entire quantity and second shipping bill where the main vendor is dependent on sub-vendor shipping bill should be prepared jointly so that duty credit scripts can be transferred to sub-vendor easily.

31. For refund of discounted duty script value if one shipping bill is generated the main vendor and sub-vendor can enter into an agreement or through advance depending on term. Otherwise, incentives should go to sub-vendors on proportionate basis.

32. Every player must have valid IEC, GST number and registration at ICEGATE portal.

33. If the merchant exporter doesn’t have full capacity to meet the export order , he may place subsequent purchase order to manufacturer exporter for balance quantity but in that case it is advisable to prepare all export documents (commercial invoice, packing list, shipping bill) separately for part supply of goods. It will give the merchant exporter an added advantage to pass on benefit under duty credit scripts.

If a manufacturer exporter gets an order from merchant exporter /third party exporter and the merchant exporter asks the manufacturer exporter to ship, on their behalf, goods they manufacturer, in that case question arises how the merchant exporter will realize the payment against the exports?

Para 9.60 of FTP says that “third-party exports” means exports made by an exporter or manufacturer on behalf of another exporter(s). So, in this case the manufacturer can use their own IEC to ship goods and state in the shipping bill that the export is on behalf of the merchant exporter giving his name and address. However, the manufacturer exporter must furnish the pre-shipment invoice (shipping bill and Export declaration form) to the merchant exporter and give his AD code so that the shipping bill details go to his bank in the EDPMS.

GST on Third-Party Exports

A third-party export is a transaction in which the manufacturer makes an export through another person. Third-party exports are eligible for concessional rates of GST. The concessional rates were introduced by the Central Board of Indirect Taxes and Customs (CBIC). The manufacturer who supplies goods and services may not have the infrastructure to undertake the export. Hence, the manufacturer may utilise the services of an intermediary for carrying out the export transaction. The intermediary is known as the third- party exporter. The supplier of the exported goods and services is known as the manufacturer exporter. In the export documents, the name of the manufacturer exporter and the third-party exporter are mentioned. Hence, both the manufacturer exporter and the third-party exporter are understood to be making the export jointly. As per the notifications provided by the CBIC, the concessional rates can be availed by manufacturer who fulfil the above-mentioned specified conditions.

GST Rate for Third-Party Exports:

The concessional GST rate which is available for third party exports is available in Notification No. 41/2017-IT(R) and Notification No. 40/2017-CT(R) dated 23rd October 2017.

The applicable rates are the following:

a) For intra-State supply, GST should be applied at the rate of 0.05 per cent.

b) For inter-State supply, GST should be applied at the rate of 0.1 per cent.

Normally payment for exports should be received from the overseas buyer named in the EDF. It shall be received in a currency appropriate to the place of final destination mentioned in the EDF irrespective of the country of residence of the buyer. Payments for imports should be made to the original overseas seller of the goods and the importer should furnish relevant documents. This has now been liberalised by allowing receipt of payments from / effecting payments to third parties also, considering the evolving international trade practices.

Reserve Bank of India has allowed third party payments for import and export transactions. As per A.P. DIR Circular No. 70, dated 8-11-2013, such transactions shall be subject to the conditions such as availability of tripartite agreement, declaration in Export Declaration Form (EDF), mention in bill of entry and invoice, reporting of outstanding, etc. These third-party payments further should come from, or made to, a Financial Action Task Force (FATF) compliant country and through the banking channel only.

Conditions incorporated by Reserve Bank of India for third-party payments for import and export transactions are as follow vide circular A.P. DIR Circular No. 70, dated 8-11-2013:

I. EXPORT TRANSACTIONS

AD banks may allow payments for export of goods / software to be received from a third party (a party other than the buyer) subject to conditions as under:

a. Firm irrevocable order backed by a tripartite agreement should be in place.

b. Third party payment should come from a Financial Action Task Force (FATF) compliant country and through the banking channel only.

c. The exporter should declare the third-party remittance in the Export Declaration Form.

d. It would be responsibility of the Exporter to realize and repatriate the export proceeds from such third party named in the EDF.

e. Reporting of outstanding, if any, in the XOS would continue to be shown against the name of the exporter. However, instead of the name of the overseas buyer from where the proceeds have to be realised, the name of the declared third party should appear in the XOS; and

f. In case of shipments being made to a country in Group II of Restricted Cover Countries, (e.g., Sudan, Somalia, etc.), payments for the same may be received from an Open Cover Country.

Note: Restricted cover Group II country is country which experiences chronic political and economic problems as well as balance of payment difficulties.

II. IMPORT TRANSACTIONS

AD banks are allowed to make payments to a third party for import of goods, subject to conditions as under:

a. Firm irrevocable purchase order / tripartite agreement should be in place.

b. Third party payment should be made to a Financial Action Task Force (FATF) compliant country and through the banking channel only.

c. The Invoice should contain a narration that the related payment has to be made to the (named) third party.

d. Bill of Entry should mention the name of the shipper as also the narration that the related payment has to be made to the (named) third party.

e. Importer should comply with the related extant instructions relating to imports including those on advance payment being made for import of goods; and

f. The amount of an import transaction eligible for third party payment should not exceed USD 100,000. This limit will be revised as and when considered expedient.

In 2014 Reserve Bank of India had amended few clauses regarding third-party payments for exports and imports vide circular A.P. (DIR Series) Circular No.100 dated February 4,2014 .

1) In view of the difficulties faced by exporters / importers in meeting the condition “firm irrevocable order backed by a tripartite agreement should be in place” specified in the abovementioned Circular, it has been decided that this requirement may not be insisted upon in case where documentary evidence for circumstances leading to third party payments / name of the third party being mentioned in the irrevocable order/ invoice has been produced. This shall be subject to conditions as under:

(i) AD bank should be satisfied with the bona-fides of the transaction and export documents, such as, invoice / FIRC.

(ii) AD bank should consider the FATF statements while handling such transaction.

2. Further, with a view to liberalising the procedure, the limit of USD 100,000 eligible for third party payment for import of goods, stands withdrawn.

3. All other terms & conditions mentioned in the A. P. (DIR Series) Circular No.70 dated November 8, 2013, remain unchanged.

What is Firm irrevocable purchase order?

Irrevocable Corporate Purchase Order (ICPO) is a document drawn up by commercial buyers. It contains: the quantities of products required. the type of products required. other conditions that the buyer wants the sale to proceed under. Once the ICPO is issued, it must be honoured by both parties, the buyer and supplier. If either party does not honour this commitment, this will be considered as a major offense. An ICPO is a legally BINDING document. We can differentiate purchase order from the irrevocable purchase order based on content.

Sample of content of irrevocable purchase order: “We, (name of the buyer), hereby state and represent that it is our intention to purchase, and we hereby confirm that we are ready, willing and able to purchase the following commodity as per the specification and in the quantity and for the price as specified in the terms and conditions as stated below.” The irrevocable purchase order should contain, name of the commodity, name of the third-party in case of third-party transaction, quality, quantity, contract term, price, commission, loading port, delivery term, packaging, payment method, inspection, etc.

What is Financial Action Task Force (FATF) Statement?

The Financial Action Task Force (FATF) is the global money laundering and terrorist financing watchdog. Its aim is to protect the global financial system against money laundering, terrorism financing and other related threats to the integrity of the international financial systems. Authorised dealers should set up their own KYC to maintain FATF guideline.

Author Bio