Role of Payment of consideration in availment of Input tax credit (ITC) under GST

Objective and scope: –

1. whether the consideration for any supply can be paid by any other person other than the recipient?

2.If consideration is paid by 3rd party i.e. someone else then whether credit\exemption is available to recipient though there is no transaction between 3rd party and recipient?

Relevant extracts from CGST Act,2017 had been reproduced here below:

Sec.2(93):“recipient” of supply of goods or services or both, means-

“(a) where a consideration is payable for the supply of goods or services or both, the person who is liable to pay that consideration;

(b) where no consideration is payable for the supply of goods, the person to whom the goods are delivered or made available, or to whom possession or use of the goods is given or made available; and

(c) where no consideration is payable for the supply of a service, the person to whom the service is rendered,

and any reference to a person to whom a supply is made shall be construed as a reference to the recipient of the supply and shall include an agent acting as such on behalf of the recipient in relation to the goods or services or both supplied;”

Sec.16 of CGST Act,2017: Eligibility and conditions for taking input tax credit.

“16. (1) Every registered person shall, subject to such conditions and restrictions as may be prescribed and in the manner specified in section 49, be entitled to take credit of input tax charged on any supply of goods or services or both to him which are used or intended to be used in the course or furtherance of his business and the said amount shall be credited to the electronic credit ledger of such person.

(2) Notwithstanding anything contained in this section, no registered person shall be entitled to the credit of any input tax in respect of any supply of goods or services or both to him unless, —

(a) he is in possession of a tax invoice or debit note issued by a supplier registered under this Act, or such other tax paying documents as may be prescribed;

(b) he has received the goods or services or both.

Explanation.-For the purposes of this clause, it shall be deemed that the registered person has received the goods where the goods are delivered by the supplier to a recipient or any other person on the direction of such registered person, whether acting as an agent or otherwise, before or during movement of goods, either by way of transfer of documents of title to goods or otherwise;

(c) subject to the provisions of section 41, the tax charged in respect of such supply has been actually paid to the Government, either in cash or through utilization of input tax credit admissible in respect of the said supply; and

(d) he has furnished the return under section 39:

Provided that where the goods against an invoice are received in lots or instalments, the registered person shall be entitled to take credit upon receipt of the last lot or instalment:

Provided further that where a recipient fails to pay to the supplier of goods or services or both, other than the supplies on which tax is payable on reverse charge basis, the amount towards the value of supply along with tax payable thereon within a period of one hundred and eighty days from the date of issue of invoice by the supplier, an amount equal to the input tax credit availed by the recipient shall be added to his output tax liability, along with interest thereon, in such manner as may be prescribed:

Provided also that the recipient shall be entitled to avail of the credit of input tax on payment made by him of the amount towards the value of supply of goods or services or both along with tax payable thereon.

(3) Where the registered person has claimed depreciation on the tax component of the cost of capital goods and plant and machinery under the provisions of the Income-tax Act, 1961 (43 of 1961), the input tax credit on the said tax component shall not be allowed.

(4) A registered person shall not be entitled to take input tax credit in respect of any invoice or debit note for supply of goods or services or both after the due date of furnishing of the return under section 39 for the month of September following the end of financial year to which such invoice or invoice relating to such debit note pertains or furnishing of the relevant annual return, whichever is earlier.”

Discussion: –

1. From the Definition of recipient it is understood that recipient is the person who is liable to pay consideration to supplier.

2. Input tax credit is available to recipient only when recipient makes payment to supplier as second proviso to Sec.16(2).

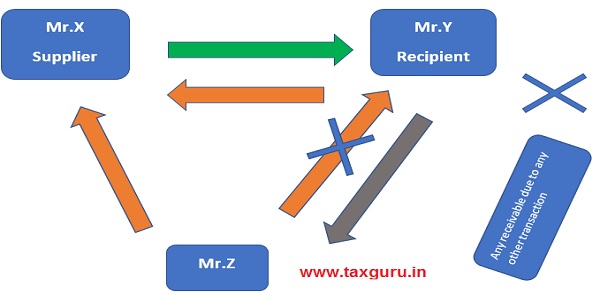

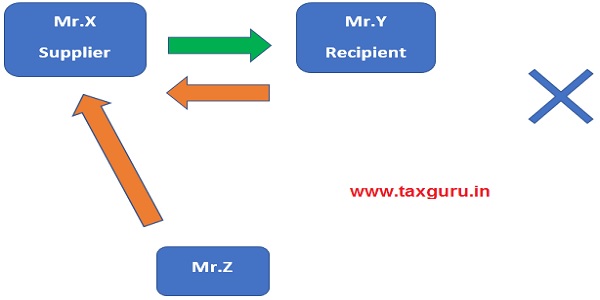

Scenario: -1

Mr. X is the supplier of service to Mr. Y however the invoice issued by Mr. X has been paid by Mr.Z.

In the above example there can be a transaction between Mr.Y and Mr.Z where in Mr.Z is liable to pay a consideration to Mr.Y. upon direction from Mr.Y , Mr.Z may make the payment to Mr.X who is not related to Mr.Z in any manner.

In this case the receivable from Mr.Z will be adjusted against liability towards Mr.X in the books of Mr.Y and hence it is deemed as paid by Mr.Y to Mr.X.

And, in the books of Mr.Z the liability towards Mr.Y will be adjusted against the payment made to Mr.X.

Scenario-2:-

In the above example, Mr. Y and Mr.Z does not have any business transaction. However, if Mr.Z pays to Mr.X for the transaction between Mr.X and Mr.Y then it will not be treated as payment made by Mr.Y to Mr.X.

ITC availability

Since, Mr. Y has not made any payment to Mr.X the credit on account of taxes charged by Mr.X will not be available to Mr.Y.

In the books of accounts of Mr.Y also the said transaction can never be nullified unless there is any receivable from Mr.Z in the books of Mr.Y.

There is no contractual obligation for Mr.Z to pay Mr.X. the contractual obligation is between Mr.X and Mr.Y and hence liability to pay to Mr.X is always with Mr.Y. in this backdrop the credit is not available to Mr.Y.

however if there is any other contractual obligation to Mr.Z to pay to Mr.Y then in such scenario if Mr.Z makes payment to Mr.X and gets relieved from his obligation to pay to Mr.Y by virtue of arrangement and also he make Mr.Y gets relieved from obligation of payment to Mr.X. in this scenario the credit is available to Mr.Y.

Zero rated benefit to SEZ availability

If Mr.Y is an SEZ and receives services from Mr.X which is qualified for zero rated benefit.

Scenario-1:-

If the consideration is not paid by SEZ i.e Mr.Y then the said service is deemed not to have been taken by SEZ as the consideration is not paid by Mr.Y. If the same is paid by Mr.Z without having contractual obligation to pay to Mr.X the same can not be treated as service received by Mr.Z.

By doing above transaction ;

1.Mr.X will relieve Mr.Y from his liability in his books of account

2.Mr.Y will not be able to record the transaction as the same is paid by Mr.Z and there is no other contractual obligation to Mr.Z to pay to Mr.Y.

Hence, in this case, it can not be said to be incurred or received by Mr.Y and hence benefit is not available.

Scenario-2:- In case of scenario 2 , Mr.Y and Mr.Z has a business transaction and Mr.Z is liable to pay to Mr.Y .

Now, Mr.Y can direct Mr.Z to make payment on behalf to Mr.X This relieves,

1. Mr.Z from his liability towards Mr.Y.

2. Mr.Y from his liability towards Mr.X

3. Mr.Z from his liability towards Mr.Y.

In the above scenario benefit is available as Mr.Y can be able to record the expense and able to discharge the liability.

Conclusion: –

Without having any contractual obligation with service recipient if any 3rd party makes the payment to supplier then the ITC or zero-rated benefit is not available.