Input tax credit has been defined as per Act in our previous article. It means the credit of Input Taxes paid on inputs, capital goods and input services. The Input tax in relation to a registered person, means the Central-tax (CGST), State-tax (SGST), Integrated-tax (IGST) and Union Territory Tax (UTGST) charged on any supply of goods or services. It also includes the IGST paid on import of goods and tax payable under the reverse charge mechanism but excludes tax paid under composition levy. Input Tax Credit is covered by Chapter V of the CGST act through CGST Rules 36 to 45 and Form ITC 01 to ITC 04.

As per section 16 (1), Every registered person, shall be entitled to avail input tax credit if the goods and services received is used or intended to be used for business purposes and the said amount shall be credited to the electronic credit ledger of such person subject to such conditions and restrictions as may be prescribed in Rule 36 CGST Rules, 2017.

As per section 16 (2) every registered person shall be entitled to take credit only if the following conditions are satisfied:-

√ He is in possession of a debit note, tax invoice issued by the supplier or such other tax paying documents as prescribed under Rule 36 [Tax Invoice u/s 31 , Self-Invoice u/s 31(3) , Debit note u/s 34, Bill of Entry, ISD invoice or Credit note under rule 54(1)]

√ He has received the goods or services or both. As per explanation provided in the act, where the goods/services are delivered/supplied by the supplier to a recipient or any other person on the direction of such registered person, either by way of transfer of title to goods or otherwise, it shall be deemed that the registered person has received the goods or service, as the case maybe.

√ Subject to the provision of section 41 and 43A [i.e. Filing of GSTR 3B & Claim of Provisional ITC] the tax charged in respect of such supply has been actually paid to the Government, either in cash or through utilization of ITC as

√ He has furnished the return under section 39.

Note :

√ As per section 41 every registered person shall, subject to such conditions and restrictions as prescribed in Rule 69, is entitled to take the credit of eligible input tax, as self-assessed, in his return on a provisional basis. The same shall be utilised only for payment of self-assessed output tax. As per Rule 69, GSTIN of the supplier, GSTIN of the recipient, invoice or debit note number, invoice or debit note date and tax amount shall be matched after the due date for furnishing the return in Form GSTR-3. However. Where such due date of Form Gstr-1 & Gstr-2 be extended, the date of matching shall also be extended. The commissioner may further extend such date. [The matching concept is suspended presently in absence of GSTR 2 & GSTR 3]

√ As per section 43A, which lays the procedure for furnishing return and availing input tax credit, The procedure for furnishing the details of outward supplies by the supplier on the common portal, for the purposes of availing input tax credit by the recipient shall be such as may be prescribed. Also, The procedure for availing input tax credit in respect of outward supplies not furnished under details of Outward supplies shall also be such as may be prescribed and such procedure may include the maximum amount of the input tax credit which can be so availed[but not more than twenty percent of ITC available as per records furnished]

√ As per section 43A(8) the procedure, safeguards and threshold of the tax amount in relation to outward supplies, the details of which can be furnished for the purposes of availing input tax credit by a registered person within six months of taking registration and who has defaulted in payment of tax i.e in GSTR-3B for more than two months from the due date of payment of such defaulted amount shall be such as may be prescribed.

[Section 43A has been inserted by the CGST (Amendment) Act, 2018, to be in effect from a date yet to be notified ]

√ Rule 36(4) talks about ITC not exceeding twenty per cent of the input tax credit available, on the basis of details furnished by the suppliers i.e. appearing in GSTR-2A. The recovery of such excess credit claimed shall be made in such manner as may be prescribed and such procedure may provide for non-recovery of an amount of tax or input tax credit wrongly availed not exceeding one thousand rupees.

√ However, as per Notification no. 75/2019 restriction has been imposed on the ITC eligibility to maximum 10% on inward supplies for which details have not been furnished by the supplier in its GSTR1 and is not appearing in the registered person’s GSTR-2A.

Due to Covid-19 pandemic, the Government through Notification No. 30/2020- Central tax dated 03-04-2020 & CGST (Fourth Amendment Rules), has notified that the restriction shall apply cumulatively for February’2020 to August’2020 in the Gstr-3B of September’2020.

√ First Proviso to section 16 talks about invoice received for Goods received in lots or installments, in such cases, the registered taxable person shall be entitled to take credit upon receipt of the last lot or installment.

As per second proviso to section 16 read with Rule 37 the registered person claiming ITC should pay the supplier, the taxable value along with the tax within 180 days from the date of issue of invoice, failing which the amount of credit availed by the recipient would be added to his output tax liability for the month in which the details are furnished. However, once the amount is paid to the supplier, the recipient will be entitled to avail the credit again. In case part payment has been made, proportionate credit would be allowed. The registered person shall be liable to pay interest at the rate notified section 50(1) i.e. 18 percent p.a. for the period starting from the date of availing credit on such supplies till the date when the amount added to the output tax liability is paid. However, the value of supplies made without consideration as specified in Schedule I of the said Act shall be deemed to have been paid and this proviso shall not apply to such supplies. This proviso would not be applicable to supplies on which tax is payable on reverse charge basis.

As per third proviso to section 16 the recipient shall be entitled to ITC once the payment is made by him of the amount towards the value of supply of goods or services or both along with tax payable thereon.

√ Section 16(3) says that if the registered taxable person has claimed depreciation on the tax component of the cost of capital goods under the provisions of the Income Tax Act, 1961, the input tax credit shall not be allowed on the said tax component.

√ As per Section 16(4) No Input Tax Credit should be claimed beyond the due date of GSTR-3B for September of the following Financial year to which invoice pertains or date of filing of annual return, whichever is [However, as Inserted by the CGST (Second Removal of Difficulties) Order, 2018, w.e.f. 31-12-2018,a registered person shall be entitled to take ITC after the due date of furnishing of the return under section 39 for the month of September, 2018 till the due date of furnishing of the return for the month of March, 2019 in respect of any invoice or invoice relating to such debit note for supply of goods or services or both made during the financial year 2017-18, the details of which have been uploaded by the supplier till the due date for furnishing the details for the month of March, 2019.]

Apportionment of credit under Section 17(1) to Section 17(4)

As per section 17(1), In a case where the goods or services or both are used by the registered person partly for the purpose of any business and partly for other purposes, the amount of credit shall be restricted to so much of the input tax as is attributable to the purposes of his business

As per section 17(2), In a case where the goods or services or both are used by the registered person partly for effecting taxable supplies including zero-rated supplies and partly for effecting exempt supplies under the respective Acts, the amount of credit shall be restricted to so much of the input tax as is attributable to the said taxable supplies including zero-rated supplies. Rule 42 and 43 as per section 17(6) shall be followed for calculation of ineligible input tax credit.

As per section 17(3), Exempt supply under 17(2) shall be such as may be prescribed, and shall include the following :

√ supplies on which the recipient is liable to pay tax on reverse charge basis

√ transactions in securities

√ sale of land

√ subject to clause (b) of paragraph 5 of Schedule II, sale of building

The value of exempt supplies shall not include the value of activities or transactions specified in Schedule III (activities neither treated as supply of goods nor service) except those specified in paragraph 5 (sale of land and building) of the said Schedule. For the purpose of Section 17(3), in the following cases, value of exempt supply shall be as follows:

√ value of land of building :- as adopted for the purpose of paying stamp duty

√ value of security :- 1% of sale value of such security

Rule 42 : Manner of determination of input tax credit in respect of inputs or input services and reversal thereof

The amount of input tax credit in respect of inputs or input services, attracting the provisions of section 17(2), shall be calculated to the purposes of business or for effecting taxable supplies in the following manner :-

| Calculation of common ITC available for apportionment | |

| Total tax paid on inputs and input service | T |

| Less : | |

| Total tax paid on inputs and input service directly attributable for non business purpose | (T1) |

| Total tax paid on inputs and input service directly attributable to exempt supplies | (T2) |

| Total input tax credit on inputs and input service which are blocked credits | (T3) |

| Total Input tax credit credited to Electronic credit ledger T- (T1+T2+T3) | C1 |

| Less : | |

| Total input tax credit on inputs and input service directly attributable for affecting taxable supplies(including zero rated) | (T4) |

| Common ITC available for apportionment | C2 |

–

| Calculation of credit attributable to exempt supplies | |

| Amount of Input tax credit attributable for exempt supplies. D1 = (E/F)*C2 | D1 |

| Calculation of credit attributable to non-business purpose | |

| Amount of Input tax credit attributable for non-business purpose. D2= 5% of C2 | D2 |

| Eligible Input tax credit attributed for the purpose of business excluding exempt but including Zero rated supply. C3=C2-(D1+D2) | C3 |

Note :

√ T1′, ‘T2’, ‘T3’ and ‘T4’ shall be determined and declared by the registered person at the invoice level in FORM GSTR-2.However, as per Central Goods and Services Tax (Second Amendment) Rules, 2019, w.e.f. 1-4-2019, the same can be declared at summary level in FORM GSTR-3B.

√ If the E & F is not available for the current tax period then such calculation shall be made after taking the E & F values of the last tax period for which such details are available

Where, ‘E’ is the aggregate value of exempt supplies during the tax period, and

‘F’ is the total turnover in the State of the registered person during the tax period.

√ Aggregate values of exempt supplies and total turnover shall not include duties on excisable goods manufactured or produced in India as per Entry 84, CST as per entry 92. State Excise as per entry 51 and taxes on sale or purchase of goods other than interstate supply as per entry 54 of list II of the said schedule. Aggregate value of exempt supplies shall also exclude the value of services by way of accepting deposits, extending loans or advances in so far as the consideration is represented by way of interest or discount, except in case of a banking company or a financial institution including a non-banking financial company, engaged in supplying services by way of accepting deposits, extending loans or advances; and the value of supply of services by way of transportation of goods by a vessel from the customs station of clearance in India to a place outside India.[Inserted by CGST (Second Amendment) Rules,2018]

√ If the yearly D1 and D2 exceeds D1 and D2 calculated on a monthly basis then such excess shall reversed through Form GSTR-3B or DRC-03 of the registered person in the month not later than the month of September following the end of the financial year to which such credit relates along with interest @ 18% on the said excess amount for the period starting from the first day of April of the succeeding financial year till the date of payment. However, if yearly D1 and D2 is less than D1 and D2 calculated on a monthly basis, such excess shall be claimed by the registered person in the month not later than the month of September following the end of the financial year to which such credit relates.

√ According to the first proviso to Rule 42, In case of Supply of services covered by clause (b) of paragraph 5 of Schedule II of the Act, the value of E and F for a tax period shall be calculated for each project separately, taking value of E and F as under :

E= aggregate carpet area of the apartments, construction of which is exempt from tax plus aggregate carpet area of the apartments, construction of which is not exempt from tax, but are identified by the promoter to be sold after issue of completion certificate or first occupation, whichever is earlier

F= aggregate carpet area of the apartments in the project.

The apportionment of ITC under rule 42 and 43 shall be made every month, project-wise. The apportionment in such a case, shall be made on the basis of estimated carpet area of flats which may be sold during construction and estimated carpet area which may be sold after completion. It is hereby clarified that in case of supply of services covered by clause (b) of paragraph 5 of Schedule II of the said Act, value of T4 shall be zero during the construction phase because inputs and input services will be commonly used for construction of apartments booked on or before the date of issuance of completion certificate or first occupation of the project, whichever is earlier, and those which are not booked by the said date.

Rule 43 : Manner of determination of input tax credit in respect of capital goods and reversal thereof

The amount of input tax credit in respect of capital goods, attracting the provisions of section 17(2), shall be calculated to the purposes of business or for effecting taxable supplies in the following manner :-

a) The amount of input tax in respect of capital goods used or intended to use exclusively for non-business purposes or exclusively for effecting exempt supplies shall be indicated in FORM GSTR-2 or FORM GSTR-3B and the same shall not be credited to the electronic credit ledger

b) The amount of input tax in respect of capital goods used or intended to use exclusively for taxable supply including zero-rated supplies shall be indicated in FORM GSTR-2 or FORM GSTR-3B and shall be credited directly to the electronic credit ledger.

c) The amount of input tax in respect of capital goods not covered under clauses mentioned above to be denoted as Thus, it would indicate the ITC that is commonly used for exempt supply/ non business. Assuming life of Capital goods to be 5 years from the date of invoice.

Tc = summation of A + any capital goods covered under (a) or (b) above which subsequently get covered under A reduced by 5% per quarter or part thereof.

Tc as calculated above shall be credited directly to the electronic credit ledger. Common credit for a capital goods for a tax period during it’s useful life shall be denoted as Tm.

Tm = Tc/60

Tr= Tm of earlier Capital good + Tm of current tax period

Te = E/F *Tr

E= the aggregate value of exempt supplies made during the tax period

F= the total turnover in a state of the registered person during the tax period

Note :

√ If the E & F is not available for the current tax period then such calculation shall be made after taking the E & F values of the last tax period for which such details are available.

√ Aggregate values of exempt supplies and total turnover shall not include duties on excisable goods manufactured or produced in India as per Entry 84, CST as per entry 92. State Excise as per entry 51 and taxes on sale or purchase of goods other than interstate supply as per entry 54 of list II of the said schedule. Aggregate value of exempt supplies shall also exclude the value of services by way of accepting deposits, extending loans or advances in so far as the consideration is represented by way of interest or discount, except in case of a banking company or a financial institution including a non-banking financial company, engaged in supplying services by way of accepting deposits, extending loans or advances; and the value of supply of services by way of transportation of goods by a vessel from the customs station of clearance in India to a place outside India.[Inserted by CGST (Second Amendment) Rules,2018]

√ It is hereby clarified that in case of supply of services covered by clause (b) of paragraph 5 of the Schedule II of the said Act, the amount of input tax in respect of capital goods used or intended to be used exclusively for effecting supplies other than exempted supplies but including zero rated supplies, shall be zero during the construction phase because capital goods will be commonly used for construction of apartments booked on or before the date of issuance of completion certificate or first occupation of the project, whichever is earlier, and those which are not booked by the said date. The value of E and F for a tax period shall be calculated for each project separately, taking value of E and F as under :

E= aggregate carpet area of the apartments, construction of which is exempt from tax plus aggregate carpet area of the apartments, construction of which is not exempt from tax, but are identified by the promoter to be sold after issue of completion certificate or first occupation, whichever is earlier

F= aggregate carpet area of the apartments in the project.

A detailed analysis on supplies covered under clause (b) of paragraph 5 of the Schedule II and their treatment under Rule 42 & 43 will be covered in the articles which will follow in future.

Illustration on Rule 42 & Rule 43

XYZ Ltd is engaged in providing exempt as well as taxable supplies. The detail of the same has been given below for the month of October, 2019:-

| Particulars | Amount |

| Value of exempt supplies | 15,00,000 |

| Value of zero rated supplies | 4,00,000 |

| Value of taxable supplies | 26,00,000 |

| Supplies made for personal use | 5,00,000 |

The details of input tax credit for the same has been given below as follows:-

| Particulars | CGST | SGST |

| Total input tax credit for inputs and input services | 1,75,000 | 1,75,000 |

| Total Input tax credit determined above includes the following :- | ||

| Credit of input services used for providing exempt supplies | 32,000 | 32,000 |

| Credit of input services used for providing taxable supplies including zero rated | 72,000 | 72,000 |

| Credit of input services used for providing supplies for personal use | 25,000 | 25,000 |

| Credits u/s 17(5) which have been availed | 15,000 | 15,000 |

| Particulars | CGST | SGST |

| Credit of capital goods used for providing exempt supplies | 10,800 | 10,800 |

| Credit of capital goods used for providing taxable supplies including zero rated | 45,000 | 45,000 |

| Credit of capital goods used for providing supplies for non-business purpose | 11,700 | 11,700 |

| Particulars | CGST | SGST |

| Capital Goods A | 50,400 | 50,400 |

| Capital Goods B | 23,040 | 23,040 |

| Capital Goods C | 41,040 | 41,040 |

Capital goods C was purchased during the month of October 2019. However, all others were purchased during earlier months.

Solution:

Eligible credit for inputs and input services as per Rule 42

| Calculation of common ITC available for apportionment | CGST | SGST | |

| Total tax paid on inputs and input service | T | 1,75,000 | 1,75,000 |

| Less : | |||

| Total tax paid on inputs and input service directly attributable for non business purpose | (T1) | (25,000) | (25,000) |

| Total tax paid on inputs and input service directly attributable to exempt supplies | (T2) | (32,000) | (32,000) |

| Total input tax credit on inputs and input service which are blocked credits | (T3) | (15,000) | (15,000) |

| Total Input tax credit credited to Electronic credit ledger T- (T1+T2+T3) | C1 | 1,03,000 | 1,03,000 |

| Less : | |||

| Total input tax credit on inputs and input service directly attributable for affecting taxable supplies(including zero rated) | (T4) |

(72,000) |

(72,000) |

| Common ITC available for apportionment | C2 | 31,000 | 31,000 |

| Calculation of credit attributable to exempt supplies | |||

| Value of exempt supplies | E | 15,00,000 | |

| Total Turnover for the period | F | 50,00,000 | |

| CGST | SGST | ||

| Amount of Input tax credit attributable for exempt supplies. D1 = (E/F)*C2 | D1 | 9,300 | 9,300 |

| Calculation of credit attributable to non-business purpose | |||

| Amount of Input tax credit attributable for non-business purpose. D2= 5% of C2 | D2 | 1,550 | 1,550 |

| Total ineligible common credit of inputs and input services | 10,850 | 10,850 | |

| Net eligible common credit of inputs and input services

C3= C2-(D1+D2) |

C3 | 20,150 | 20,150 |

| Total eligible credit of inputs and input services = C3 + T4 | 92,150 | 92,150 | |

Eligible credit for capital goods as per Rule 43

| Calculation of common ITC available for apportionment | CGST | SGST |

| Total input tax credit on capital goods which are exclusively used for taxable supplies(including zero rated) | 45,000 | 45,000 |

| Input tax credit on capital goods which are used for taxable as well exempt supplies = Tc | 41,040 | 41,040 |

| Tr= Aggregate Tm of all capital goods (Note 2) | 1,908 | 1,908 |

| Credit attributable to exempt supplies for the month of October 2019

Te = Tr * E/F { E= 15,00,000 F=50,00,000) |

572 | 572 |

| Total credit attributable for capital goods for the month of October 2019

(45000+41040-572) |

85,468 | 85,468 |

Note:

1. ITC of capital goods exclusively used for the supplying exempt services as well as for non-business purpose shall not be eligible for ITC

2. Calculation of Tr has been given as follows :

| Particulars | CGST | SGST |

| Capital Goods A [50,400/60] | 840 | 840 |

| Capital Goods B [23040/60] | 384 | 384 |

| Capital Goods C[41040/60] | 684 | 684 |

| Total | 1,908 | 1,908 |

As per section 17(4), a banking company or a financial institution including a non-banking financial company, engaged in supplying services by way of accepting deposits, extending loans or advances shall have the option to either –

√ comply with the provisions of 17(2) read with Rule 42 & 43 or

√ avail every month an amount equal to 50%. of the eligible input tax credit on inputs, capital goods and input services in that month and the rest shall lapse as per Rule 38.

The option once exercised shall not be withdrawn during the remaining part of the financial year and the restriction of 50% shall not apply to the tax paid on supplies made by one registered person to another registered person having the same Permanent Account Number, i.e. 100% ITC available.

Rule 38 says that the Financial or Banking Company shall not avail the credit of tax paid on inputs and input services that are used for non-business purposes and those ITC as blocked u/s 17(5). Only fifty per cent of the remaining amount of input tax shall be the input tax credit admissible to such assessees.

As per section 17(5), Notwithstanding anything contained in section 16(1) and section 18 (1), Input tax credit shall not be availed in respect of the following :

| Section reference | Situations where ITC cannot be claimed | Exception |

|

17(5)(a) |

Motor vehicles for transportation of persons having approved seating capacity of not more than 13 persons (including driver) including leasing and renting | ITC of such motor vehicle used for transportation of persons can be availed if they are used for making the following taxable supplies, namely :-

|

|

17(5)(aa) |

Vessel & Aircraft including leasing and renting | ITC of such Vessel & Aircraft can be availed if they are used for transportation of goods or when they are used for making the following taxable supplies namely :-

|

|

17(5)(ab) |

Services of general insurance, servicing, repair and maintenance of aforesaid motor vehicles, vessels and aircrafts. | ITC of the said services can be availed:

|

Note : The following points can be summarized :-

√ ITC on motor vehicles for transportation of persons having approved seating capacity of more than 13 persons can be availed.

√ ITC on motor vehicles, aircraft & vessel for transportation of goods can be availed.

√ ITC on motor vehicles used for future supply of such vehicles, transportation of persons can be availed.

√ ITC on aircraft & vessel for transportation of persons cannot be availed.

√ Services of general insurance, servicing, repair and maintenance of aforesaid motor vehicles, vessels and aircrafts where they are used for making further supply of such vehicle, vessel & aircraft, further transportation of passenger, importing training on driving, flying, navigating can be availed.

√ ITC would further be admissible for leasing, renting or hiring of motor vehicles when such motor vehicles are used for above said purposes.

| Section reference | Situations where ITC cannot be claimed | Exception |

|

17(5)(b) |

Supply of

|

|

|

||

Note: ITC would be admissible where it is obligatory for an employer to provide such supplies to its employees under any law for the time being in force.

| Section reference | Situations where ITC cannot be claimed | Exception |

|

17(5)(c) |

Works contract service when supplied for construction of an immovable property (other than plant and machinery) |

|

Let us understand the above provision with the help of examples.

Example 1 : Works contract service used by main contractor who further supplies work contract service.

In this case, ITC can be availed.

Example 2 : Works contract service used for construction of building by manufacturer or service provider[other than the provider of Works Contract Service.]

ITC on the same cannot be availed by the same.

| Section reference | Situations where ITC cannot be claimed |

|

17(5)(d) |

Goods or services or both received by a taxable person for construction of an immovable property (other than plant or machinery)

|

Note:

√ Construction includes re-construction, renovation, additions, alterations or repairs, to the extent of capitalization, to the said immovable property.

√ Plant and machinery means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services or both and includes such foundation and structural supports but excludes :-

√ land, building or any other civil structures

√ telecommunication towers and

√ pipelines laid outside the factory premises

Example 1 : Construction service and material used for construction of plant and machinery.

In this case, ITC can be availed.

Example 2 : Construction service used for construction of building of manufacturer or service provider[other than provider of works contract service]

ITC on the same cannot be availed by such persons.

Example 3 : Construction service and material used for construction of Telecommunication power.

ITC on the same cannot be availed.

| Section reference | Situations where ITC cannot be claimed |

| 17(5)(e) | Goods or services or both on which tax has been paid under section 10 i.e. Composition Scheme |

| 17(5)(f) | Goods or services or both received by a non-resident taxable person except on goods imported by him |

| 17(5)(g) | Goods or services or both used for personal consumption |

| 17(5)(h) | Goods lost, stolen, destroyed, written off or disposed of by way of gift or free samples |

| 17(5)(i) | Any tax paid in accordance with the provisions of sections 74, section 129 and section 130 |

Note:

√ As per Circular no 92/11/2019 dated 07/03/2019 it has been clarified that free samples which are given without any consideration do not amount to supply except where such activity falls in the course of Schedule I of the CGST Act. Thus, where such activity amounts to supply in accordance with schedule 1, the supplier would be eligible to claim ITC on the same.

√ As per Circular no 92/11/2019 dated 07/03/2019 it has been clarified that in case of buy one get one offer, it would be treated as two goods supplied at the cost of one. In such a case, depending on whether such goods are classified as composite supply or mixed supply, rate would be determined. Also, ITC used in relation to such goods would also be available to the supplier .

√ Section 74 : Tax not / short paid due to fraud, willful misstatements or suppression of facts or confiscation and seizure of goods

√ Section 129 : Detention , seizure and release of goods and conveyance in transit

√ Section 130 : Confiscation of goods or conveyance and levy of penalty.

Summary of relevant clauses of section 17(5) has been given below :

| Section Reference | Particulars |

|

Section 18(1)(a) |

Any person who has

|

|

Section 18(1)(b) |

A person who has taken voluntary registration

|

|

Section 18(1)(c) |

In a case where any registered person ceases to pay tax under Composition scheme i.e. switches from such scheme to normal scheme

|

|

Section 18(1)(d) |

In case where an exempt supply of goods or services or both by a registered person becomes a taxable supply, such person can take credit of

|

Note :

√ Inputs on such Capital Goods will not be available under section 18(1)(a) and 18(1)(b)

√ Inputs on such Capital Goods held in stock will be available under section 18(1)(c) and 18(1)(d). Inputs on such capital goods would be reduced by 5% per quarter or part thereof from the date of invoice.[Rule 40(1)(a)]

√ As per Rule 40(1)(b), a declaration in Form GST ITC-01 needs to be submitted containing the details of all the inputs held in such stock within a period of thirty days from the date of becoming eligible to avail the input tax credit. However, any extension of the time limit is to be notified by the Commissioner of State or Union territory tax .

√ The details furnished in the declaration shall be duly certified by a practicing chartered accountant or a cost accountant if the aggregate value of the claim on account of Central tax, State tax, Union territory tax and integrated tax exceeds two lakh rupees

√ The declaration shall clearly specify the details relating to the inputs held in stock, inputs contained in semi-finished or finished goods held in stock, or as the case may be, capital goods on the day immediately preceding the date from which he becomes liable to pay tax under the provisions of the Act, i.e. in the case of a claim under section 18(1)(a), on the day immediately preceding the date of the grant of registration, in the case of a claim under section 18(1)(b),on the day immediately preceding the date from which he becomes liable to pay tax under section 9, in the case of a claim section 18(1)(c),on the day immediately preceding the date from which the supplies made by the registered person becomes taxable, in the case of a claim under section 18(1)(d). [Rule 40(1) (c)]

√ The input tax credit claimed in accordance with the provisions of clauses 18(1)(c) and 18(1)(d) shall be verified with the corresponding details furnished by the corresponding supplier in FORM GSTR-1 or as the case may be, in FORM GSTR- 4, on the common portal.

- As per Section 18(2), A registered person will only be entitled to take input tax credit under 18(1) in respect of any supply of goods or services or both to him within one year from the date of issue of tax invoice relating to such supply. This means that for any input held in stock over a period of 1 year, will not be eligible.

- As per Section 18(3), In case of a change in the constitution of a registered person on account of sale, merger, demerger, amalgamation, lease or transfer of the business with the specific provisions for transfer of liabilities, the said registered person shall be allowed to transfer the input tax credit which remains unutilized in his electronic credit ledger to such sold, merged, demerged, amalgamated, leased or transferred business in accordance with Rule 41. Such details would be furnished in Form ITC-02.

- As per Rule 41

- in the case of demerger, the input tax credit shall be apportioned in the ratio of the value of assets of the new units as specified in the demerger scheme.[Value of assets means the value of entire assets irrespective of whether ITC has been availed thereon or not]

- Transferor shall also submit a copy of a certificate issued by a practicing CA/CMA certifying that the sale, merger, demerger, amalgamation, lease or transfer of business has been done with a specific provision for the transfer of liabilities.

| Section Reference | Particulars |

|

Section 18(4) |

In a case where any registered person who has availed of input tax credit opts composition scheme thereafter or where the goods or services or both supplied by him become wholly exempt

|

Note :

√ As per Rule 44, a declaration in Form GST ITC-03 and in Form GSTR-10, in case of cancellation of registration, needs to be submitted.

√ Where the tax invoices related to the inputs held in stock are not available, the registered person shall estimate the amount based on the prevailing market price of the goods on the effective date of the occurrence of any of the events specified section 18 (4) [Rule 44(3)]

√ The details furnished shall be duly certified by a practicing chartered accountant or cost accountan

Rule 44 specifies for inputs held in stock and inputs contained in semi-finished and finished goods held in stock, the ITC shall be calculated proportionately on the basis of the corresponding invoices on which credit had been availed.

For capital goods held in stock, the input tax credit involved in the remaining useful life in months shall be computed on pro rata basis, taking the useful life as five years.

Illustration:

Capital goods of the assessee has been in use for 3 years and 6 months. Now, the useful remaining Life is 1.5 years i.e. 18 months.

Suppose, Input tax credit taken on such capital goods= Rs. 1, 00,000/-

Input tax credit attributable to remaining useful life= Rs. 1, 00,000*18/60 which is Rs. 30,000/-

Therefore, Rs. 30,000/- is to be reversed by the assessee.

- As per Section 18(6), In case of supply of capital goods or plant and machinery, on which input tax credit has been taken , the registered person shall pay an amount equal to higher of :

√ the input tax credit taken on the same reduced by 5% per quarter or part thereof or

√ the tax on the transaction value

However, where refractory bricks, moulds and dies, jigs and fixtures are supplied as scrap, the taxable person may pay tax on the transaction value of such goods.

> Input tax credit in respect of Inputs and Capital goods sent for Job work : Section 19

According to section 19, a principal can take ITC on inputs as well as Capital goods sent to the Job worker provided

√ Such inputs are received back within 1 year of being sent out or date of receipt by the job worker in case they are directly sent to the job worker’s place of business

√ Such capital goods are received back within 3 year of being sent out or date of receipt by the job worker in case they are directly sent to the job worker’s place of business

Note :

√ As per Rule 45, a declaration in Form GST ITC-04 needs to be submitted.

√ If such inputs and capital goods are not received back within 1 year or 3 years respectively, the same shall be deemed to have been supplied by the principal on the date when it was sent to the job worker.

√ The condition of receiving back the goods within 1/3 years shall not apply to moulds, dies, jigs, fixtures and tools.

Section 20 talks about the Manner of distribution of credit by Input Service Distributor through FORM GSTR 6 which are subject to following conditions-

(a) the credit can be distributed to the recipients of credit against a document containing such details as mentioned in Rule 54 of CGST Rules.[Invoice / Credit note issued by ISD]

(b) the amount of credit distributed shall not exceed the amount of credit available for distribution

(c) the credit of tax paid on input services attributable to a recipient shall be distributed only to that recipient;

(d) the credit of tax paid on input services attributable to more than one recipient of credit shall be distributed amongst such recipients to whom the input service is attributable pro rata on the basis of the turnover in a State/UT of such recipient, to the aggregate of the turnover of all such recipients to whom such input service is attributable and which are operational in the current year.

(e) Similarly, the credit of tax paid on input services attributable to all recipients of credit shall be distributed amongst such recipients on the basis of the turnover in a State/Union territory of such recipient, to the aggregate of the turnover of all recipients.

√ Such inputs are received back within 1 year of being sent out or date of receipt by the job worker in case they are directly sent to the job worker’s place of business

√ Such capital goods are received back within 3 year of being sent out or date of receipt by the job worker in case they are directly sent to the job worker’s place of business

Note :

√ As per Rule 45, a declaration in Form GST ITC-04 needs to be submitted.

√ If such inputs and capital goods are not received back within 1 year or 3 years respectively, the same shall be deemed to have been supplied by the principal on the date when it was sent to the job worker.

√ The condition of receiving back the goods within 1/3 years shall not apply to moulds, dies, jigs, fixtures and tools.

Section 20 talks about the Manner of distribution of credit by Input Service Distributor through FORM GSTR 6 which are subject to following conditions-

| (a) | the credit can be distributed to the recipients of credit against a document containing such details as mentioned in Rule 54 of CGST Rules.[Invoice / Credit note issued by ISD] |

| (b) | the amount of credit distributed shall not exceed the amount of credit available for distribution |

| (c) | the credit of tax paid on input services attributable to a recipient shall be distributed only to that recipient; |

| (d) | the credit of tax paid on input services attributable to more than one recipient of credit shall be distributed amongst such recipients to whom the input service is attributable pro rata on the basis of the turnover in a State/UT of such recipient, to the aggregate of the turnover of all such recipients to whom such input service is attributable and which are operational in the current year. |

| (e) | Similarly, the credit of tax paid on input services attributable to all recipients of credit shall be distributed amongst such recipients on the basis of the turnover in a State/Union territory of such recipient, to the aggregate of the turnover of all recipients. |

Relevant period means the financial year preceding the year during which credit is to be distributed

Recipient of credit means the supplier of goods or services or both having the same PAN as that of the ISD

Section 21 deals with situations where the Input Service Distributor distributes the credit in contravention of Section 20 resulting in excess distribution of credit, such excess credit so distributed shall be recovered from the recipients along with interest, and the provisions of section 73 or 74, as the case may be, shall, mutatis mutandis, apply for determination of amount to be recovered.

Rule 44A specifies the Manner of reversal of credit of Additional duty of Customs in respect of Gold dore bar. It mentions that the Central Tax in the credit ledger as attributable to the carry forward of CENVAT Credit on account of payment of the additional duty of customs u/s 3(1) of Customs Tariff

Act,1975 paid at the time of Import of the Dore Bars shall be restricted only one-sixth of such credit and five-sixth of such credit shall be debited from the electronic credit ledger at the time of supply of such gold dore bar or the gold or the gold jewellery made there from and where such supply has already been made, such debit shall be within one week from the date of commencement of these Rules.

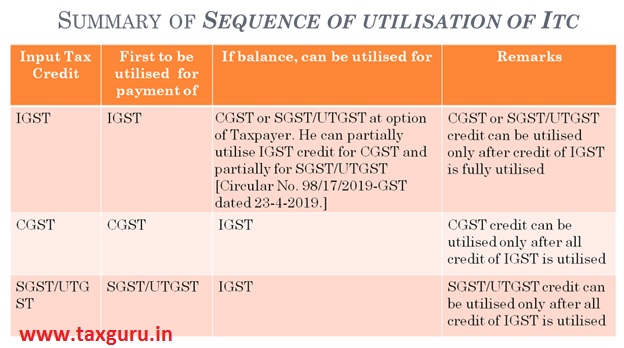

Order of utilization of ITC u/s 49(5) and 49A of CGST Act.

- As per section 49B of CGST Act, subject to the provisions of clause (e) and clause (f) of Section 49(5), the Government may, on the recommendations of the Council, prescribe the order and manner of utilization of the input tax credit on account of IGST,CGST,SGST or UTGST as the case may be, towards payment of any such tax.[inserted videCGST (Amendment) Act, 2018 inserted w.e.f. 1-2-2019]

- Order of utilization of input tax credit as per rule 88A –Normally, section prevails over the rules. However, in this case, rule 88A of CGST Rules, will override provisions of section 49(5)(a) in view of section 49B of CGST Act. Hence, order of utilization of Input Tax Credit w.e.f. 1-4-2019 will be as explained below.

- Payment of IGST – The ITC of IGST should first be utilised fully for payment of IGST through electronic credit ledger. If the credit is insufficient, balance IGST can be paid through ITC of CGST and SGST/UTGST.

- Utilisation of excess ITC of IGST (if any)– If after payment of entire IGST through electronic credit ledger, there is balance of IGST in electronic credit ledger, if any may be used either for payment of CGST or SGST/UTGST in any order[rule 88A of CGST Rules [overrides sec 49(5)(a) of CGST Act].]

- The taxable person can partially utilise IGST credit for CGST and partially for SGST/UTGST as per his choice (after first utilising fully for payment of IGST) [CBI&C circular No. 98/17/2019-GST dt. 23-4-2019.]

- Thus, credit of IGST should be fully exhausted before utilising credit of CGST and SGST/UTGST.

- After full payment of SGST/UTGST, if some ITC of SGST/UTGST is available in electronic credit ledger, that can be utilised for payment of IGST (if payable) – section 49(5)(c) of CGST Act for SGST and section 49(5)(d) of CGST Act for UTGST.

- ITC of SGST/UTGST can be utilised for payment of IGST only when ITC of CGST is not available for utilization and Credit of IGST has to be utilized before utilizing any other credit [Sec. 49(5)(e)] & Credit of CGST cannot be used for SGST/UTGST and vice versa. Sec. 49(5)(f)

Declaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice or a formal recommendation. While due care has been taken in preparing this document, the existence of mistakes and omissions herein is not ruled out. The author does not accept any liabilities for any loss or damage of any kind arising out of any inaccurate or incomplete information in this document nor for any actions taken in Reliance thereon. No part of this document should be distributed or copied without express written permission of the author.

Author Bio

Excellent! The article covered all the relevant provisions in a simplified manner.

Exhaustively covered. A bit lengthy but it is OK. After all getting tax credit from Govt. is not so easy.

Very good effort. You have spent lots of time to prepare this from original Act etc.

There are some companies who could not even pay their input suppliers with in 180 days.

Suppose in the month of Sept of succeeding year I have identified that at least 50 suppliers were not paid. But if I do not take these credit with 20th Oct of succeeding year I will loose the ITC for unpaid input suppliers. Considering this type of situation What is the best practice.

However, I must appreciate your efforts

CMA ASIM SAHA KOLKTA

30 years of Costing journey

Very exhaustive article no need to see anywhere else. Thanks you very much.