As we all aware that due date for filing monthly GST returns is 10th and 20th of each month. Now due to COVID-19, it is not able to even step out of house, then how can we file our returns?

Is there any relaxation given by Government for this problem?

We are very much in confused state about COVID-19 and sitting idle without any other option to do, but just to sit at home and stay safe. Meanwhile, an alert to all the businessman, Chartered Accountants and to all other professionals about GST from Government…….

Now the question arises to all the businessman “What is the situation of our GST returns and beloved ITC? What is the due date to file? After Corona or before Corona ?”

Government came at right time and gave some Notifications starting from 31 to 35/2020 dated 03-04-2020. Now all the tax payers as well as professionals were puzzled whether to fight with the Corona Virus or to understand this notification since the notification issued was that much tricky!!!!

And once again Government came into picture and issued circular vide No. 136/06/2020-GST dated 03rd Apr,2020 and cleared some puzzles of taxpayers.

Now We will discuss it in brief by charts and illustration

Chart on due dates released by CBIC

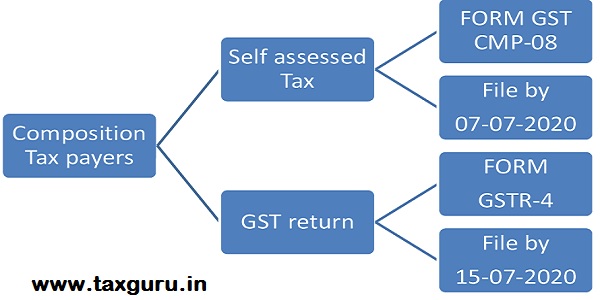

Composition Tax payers

♦ furnish the statement of details of payment of self- assessed tax in FORM GST CMP 08 for the quarter January to March, 2020 by 07.07.2020; and

♦ furnish the return in FORM GSTR-4 for the financial year 2019-20 by 15.07.2020.

In addition to the above, taxpayers opting for the composition scheme for the financial year 2020-21 have to,-

♦ file an intimation in FORM GST CMP-02 by 30.06.2020; and

♦ furnish the statement in FORM GST ITC-03 till 31.07.2020.

Normal Tax Payers – GSTR 3B

Due dates of GSTR 3B

1. If the turnover is below 5cr then interest as well as late fee will not get charged, if GST returns for the period Feb 20 to Apr 20 filed before 24-06-2020. In case GST returns filed after such date then interest @ 18% p.a, late fee along with penalty will also be levied.

2. If the turnover is above 5cr, two rates of interest applicable, 9 %and 18%. In this case, due date for GSTR 3B return has not changed i.e on 20th of succeeding month, but with respect to rate of interest ;

a. Nil – For first 15days

b.9% or 18% p.a – for further delay in days

Important Condition for Reduced interest

Reduced interest @ 9% applies only if such person files his GSTR 3B returns before 20thJune,2020 for the period Feb to Apr 2020. In case GST returns filed after such date then interest @ 18% p.a, late fee along with penalty will also be levied.

Illustration:- Calculation of interest for delayed filing of return for the month of March, 2020 (due date of filing being 20.04.2020) may be illustrated as per the below Table:

| Sl No | Date of Filing GSTR-3B | No. of days Of delay | Interest condition fulfilled? | Interest |

| 1 | 02.05.2020 | 11 | Yes | Zero Interest |

| 2 | 20.05.2020 | 30 | Yes | Zero interest for 15 days + interest rate @9% p.a. for 15 days |

| 3 | 20.06.2020 | 61 | Yes | Zero interest for 15 days + interest rate @9% p.a. for 46 days |

| 4 | 24.06.2020 | 65 | Yes | Zero interest for 15 days + interest rate @9% p.a. for 50 days |

| 5 | 30.06.2020 | 71 | No | Interest rate @18% p.a. for 71 days (i.e. no benefit of Reduced interest) |

3. No late fee will be levied if GSTR 1 filed for the period Mar to May 2020 before 30th June

Late fee leviable under section 47 has been waived for delay in furnishing the statement of outward supplies in FORM GSTR-1 under Section 37, for the tax periods March, 2020, April 2020, May, 2020 and quarter ending 31st March 2020 if the same are furnished on or before the 30th day of June, 2020.

4. No ITC matching required for GSTR 3B and GSTR 2A for the months Feb to Aug 20– Government suspends the operation of Rule 36(4) of CGST rules which restrict the ITC availment based on GSTR 2A. This relaxation is applicable for the months February to August 2020. For this period ITC can be availed whether or not your counterpart uploaded invoices.

BUT all the ITC not uploaded and claimed shall be reconciled while filing the GSTR3B for the month of September 2020.

5. In case of E-way bill, if e-way bill period expires during 20th march to 15th apr, then the period of e way bill will get extended till 30th Apr,2020.

6. Taxpayers who are required to deduct tax at source under section 51, Input Service Distributors and Non-resident Taxable persons can furnish the respective returns for the months of March, 2020 to May, 2020 on or before the 30th day of June, 2020.

7. Taxpayers who are required to collect tax at source under section 52, can furnish the respective returns for the months of March, 2020 to May, 2020 on or before the 30th day of June, 2020.

The important point to note is that due date for GSTR 3B is not extended but only the late fee and interest charges got relaxed, subject to the above conditions.

Hope you got cleared with all your puzzles!!!!

Stay Home & Stay Safe… Let’s Unite and Fight for CORONA

Author Bio