Sabka Vishwas (Legacy Dispute Resolution) Scheme, 2019 as introduced vide THE FINANCE (NO.2) ACT, 2019 wef 1-9-2019

Objectives

♦ One time measure for liquidation of past disputes of central excise and service tax

♦ To provide an opportunity of voluntary disclosure to,non-compliant taxpayers.

Cases covered under the Scheme…

√A show cause notice or appeals arising out of a show cause notice pending as on the 30th day of June, 2019

√An amount in arrears

√An enquiry, investigation or audit where the amount is quantified on or before the 30th day of June, 2019

√A voluntary disclosure

Download this Article / PPT in PDF Format

Exclusions from the Scheme…

√ Cases in respect of excisable goods set forth in the Fourth Schedule to the Central Excise Act, 1944 (this includes tobacco and specified petroleum products)

√ Cases for which the taxpayer has been convicted under the Central Excise Act, 1944 or the Finance Act, 1944

√ Cases involving erroneous refunds

√ Cases pending before the Settlement Commission

Benefits under the Scheme…

√ Total waiver of interest and penalty

√ Immunity from prosecution

√ Cases pending in adjudication or appeal, a relief of 70% from the duty demand if it is Rs. fifty lakh or less and 50% if it is more than Rs. fifty lakhs.

√ The same relief for cases under investigation and audit where the duty involved is quantified on or before 30th June, 2019.

√ In case of an amount in arrears, the relief offered is 60% of the confirmed duty amount if the same is Rs. fifty lakhs or less and it is 40% in other cases.

√ In cases of voluntary disclosure, the declarant will have to pay full amount of disclosed duty.

Other features of the Scheme…

√Facility for adjustment of any deposits of duty already made

√ Settlement dues to be paid in cash electronically only and cannot be availed as input tax credit later

√ A full and final closure of the proceedings in question. The only exception is that in case of voluntary disclosure of liability, there is provision to reopen a false declaration within a period of one year.

√ Proceedings under the Scheme shall not treated as a precedent for past and future liabilities

√ Final decision to be communicated within 60 days of application

√ No final decision without an opportunity for personal hearing in case of any disagreement

√ Proceedings under the Scheme will be fully automated

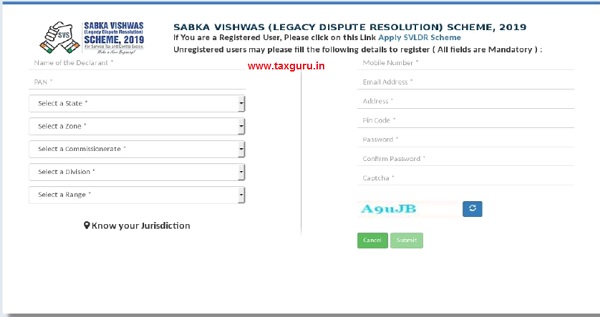

How to Apply for SVLDRS, 2019…

√ The taxpayer can apply for this scheme from https://cbic-gst.gov.in

√ The taxpayer already registered under CE/ST can login and fill Part- B of SVLDRS Form-1.

√ The unregistered taxpayer can register himself by filling Part-A of SVLDRS Form -1.

How to Apply for SVLDRS, 2019…

If the taxpayer selects the jurisdiction from know your jurisdiction then value of the fields

i.e. State/ Zone/ Commissionerate/ Division/ Range will auto populated.

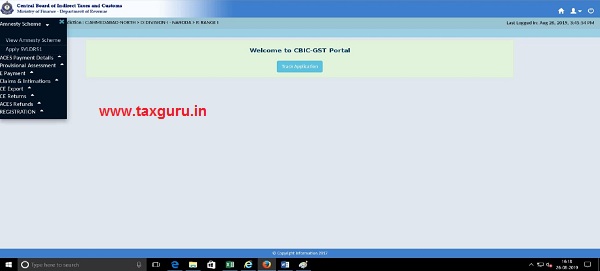

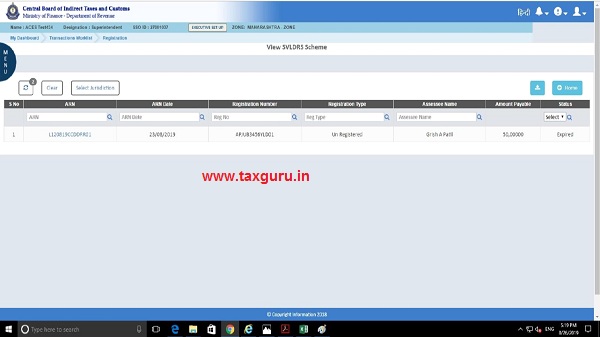

Dashboard of the registered taxpayer

Taxpayer select the scheme

The answer to first four question should be “No” in order to apply for this scheme.

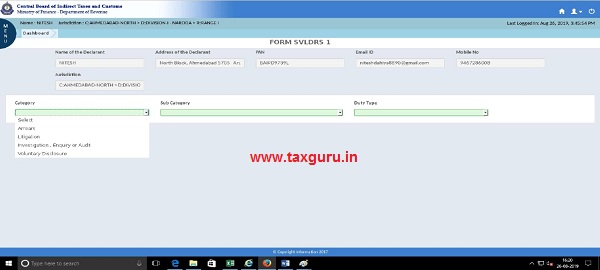

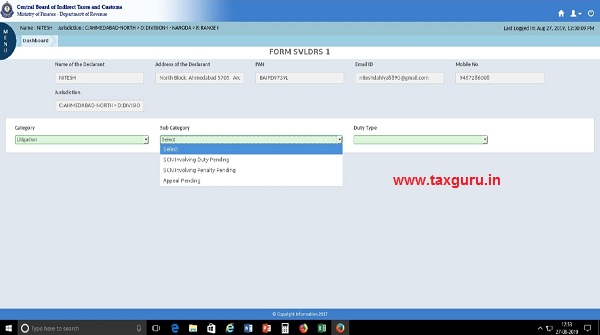

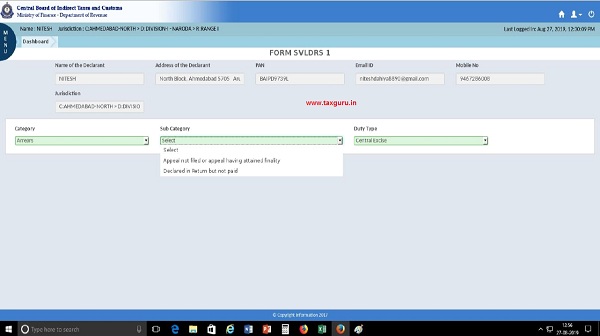

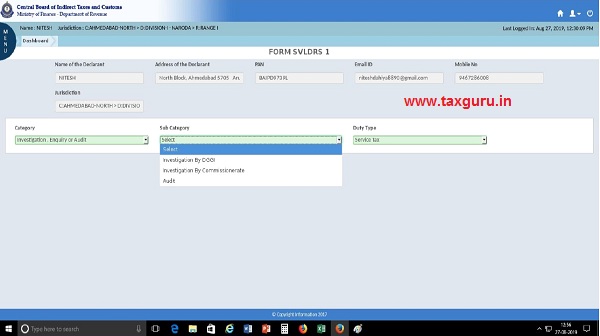

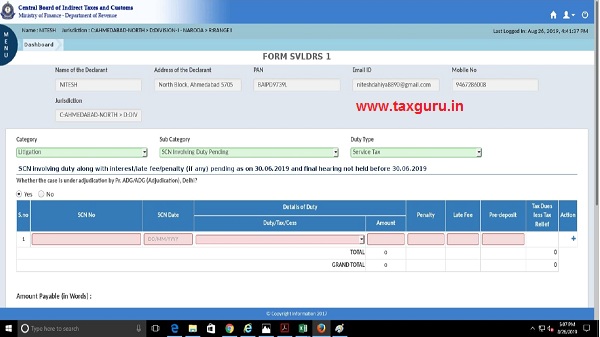

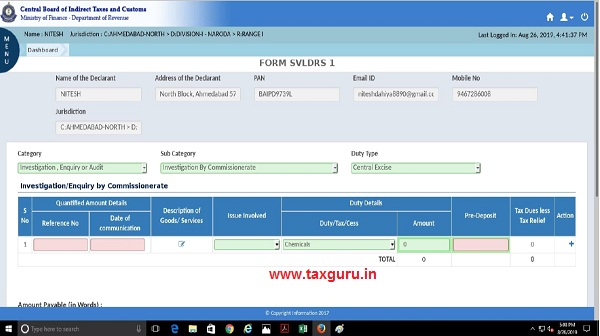

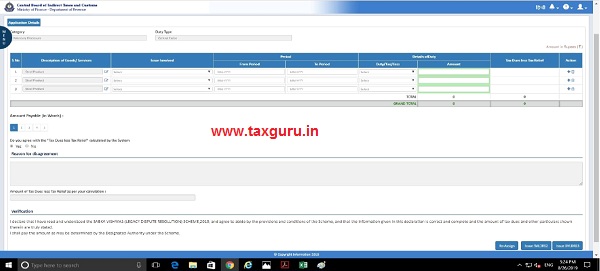

Different categories available under this scheme.

The taxpayer will select category , subcategory and duty type.

–

–

–

–

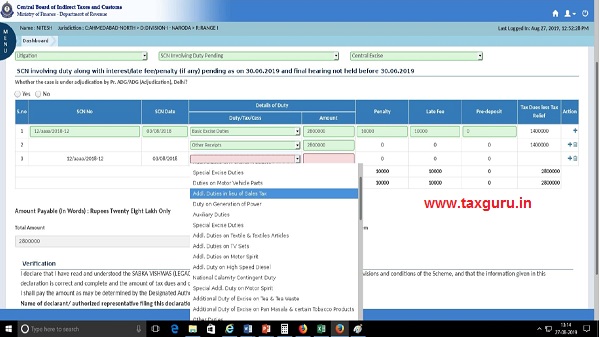

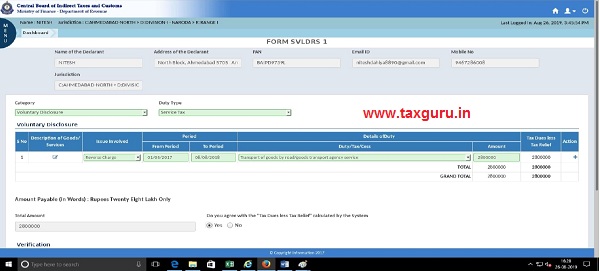

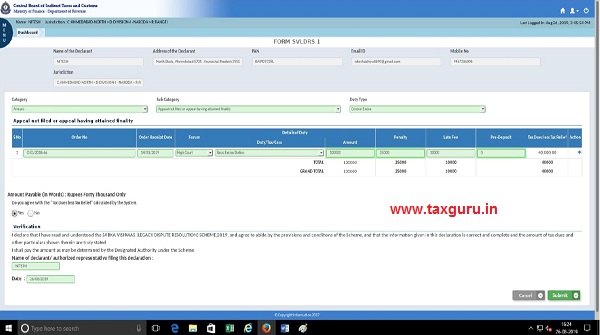

According to selection , table for entering data will appear

–

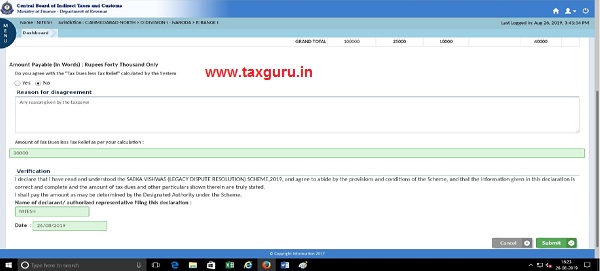

If the taxpayer doesn’t agree with the computer generated amount then the taxpayer can enter amount as per his calculation.

By clicking the submit button, Form SVLDRS-1 will be submitted to concerned Committee. ARN

will generated and the taxpayer will be informed via email and SMS.

–

–

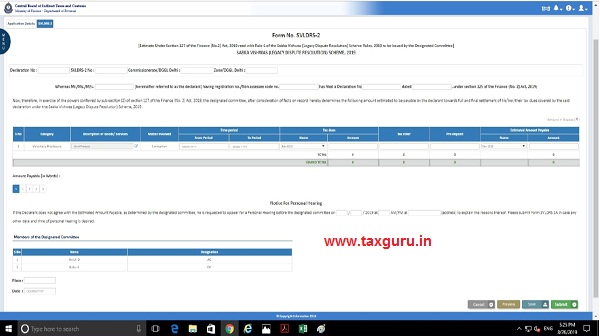

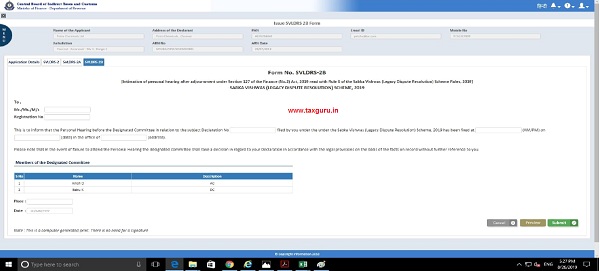

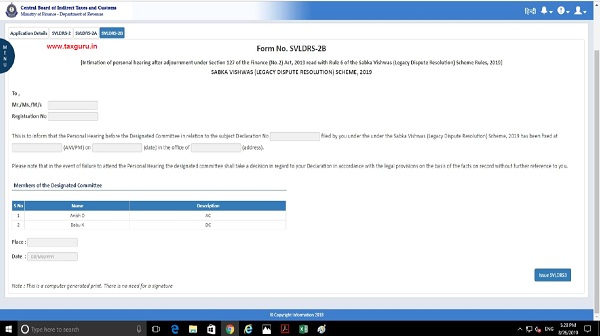

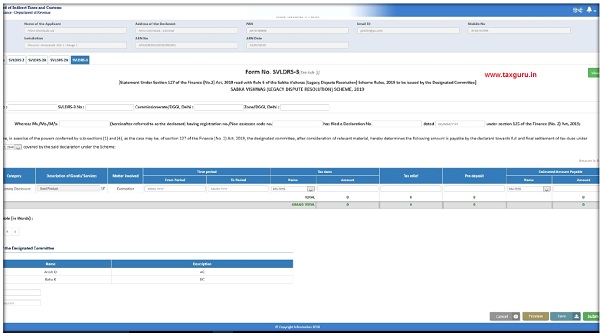

The tax officer will be shown options to issue SVLDRS 2 & SVLDRS 3.

–

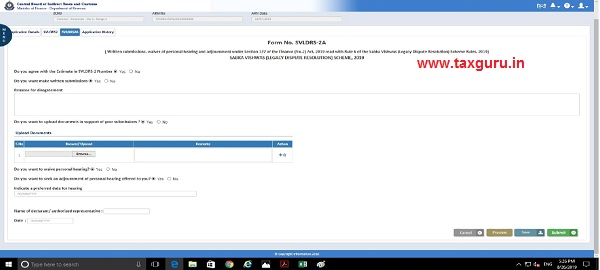

If the taxpayer doesn’t agree with SVLDRS-2 and in case want adjournment.

Adjournment of PH by the tax officer.

–

–

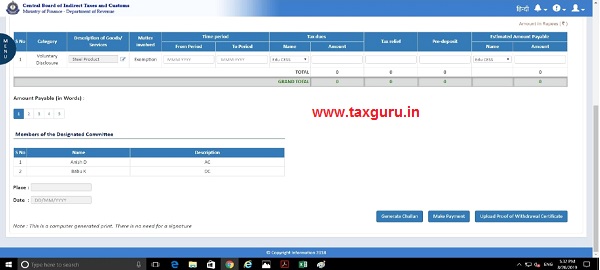

Challan generation and gateway to make payment window.

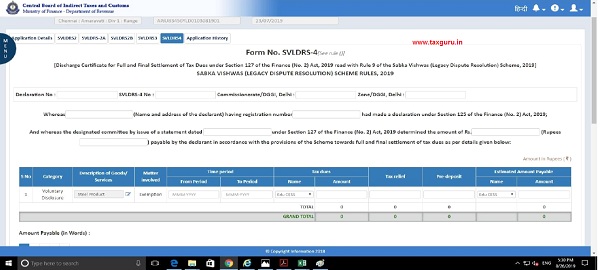

SVLDRS-4 issued by the officer after payment

| Helpline No.

CBIC Mitra Helpdesk Toll Free No. 1800-1200-232 Cbecmitra.helpdesk@icegate.gov.in Cbec-gst.gov.in>HELP>SELF SERVICE |

POLICY ISSUES:

Smt. V. Usha Principal Commissioner v.usha@gov.in |

IT ISSUES

S.K. Rahman Commissioner – IT & CV rahman.shaik@icegate.gov.in

|

Respected Sir,e

The following query need to be addressed before deciding my application.” Whether non-recoverable arrears owing to Liquidation of Main Noticee (the company ) duly approved by High Court , wherein the arrears have now become non-recoverable, will qualify for SVLDRS for co-noticee under Section 124(1)(b) of the Act.” and Secondly ,In Circular No 1071/4/2019-CX8 dated 27.08.2019 in para 10(d) the clause reproduced below :”Moreover, there can be a show cause notice that originally also involved a duty demand, and the amount of duty in the said notice became ‘nil’ on account of the fact that same has been paid under this scheme or otherwise. Such cases are also covered under Section 124(1)(b). ”

” Otherwise” in last line will cover the Non-recoverable arrears also, as in the instant case the demand against the main noticee owing to Liquidation approved by High Court, wherein after sale of entire assets, the departmental (C.Ex dues) dues have become non-recoverable and there is no proceeds left with Liquidator to distribute to revenue against the outstanding dues and hence the dues are to be treated as ” NIL” and hence whether the benefit extended to co-noticee under Section 124(1)(b) will be available to the applicant, being co-noticee.

Regards

Manoj Chandravanshi ARN No LD2611190000141dated 26.11.2019

What will be the user id after registering in the webseite.