Case Law Details

Shri Shantilal B. Parekh Vs ITO (ITAT Mumbai)

BOGUS PURCHASES –

On the basis of information, huge racket of hawala dealers involved in issuing bogus invoices to allow the traders to claim tax credit was discovered. Assessee was alleged to be one of the beneficiary to who dealt with certain parties engaged in hawala racket. As per AO, assessee was engaged in bogus purchase of INR 2,00,678, wherein, only the bill was received by assessee without receipt of material. The concluded proceeding were re-opened by issuing notice dated 10.05.2013 u/s. 148 and were asked to prove the genuineness of the purchase.

Assessee submitted that all the purchases are genuine and payments has been made through cheque. The purchases was duly accounted for in the books of accounts and reconciliation of purchase and sales were duly submitted.

DISALLOWANCE OF EXPENDITURE –

Cash expenditure of INR 1,11,420 (donation, rent, and miscellaneous expenditure of printing and stationery, tea and refreshment, travelling etc.) was disallowed on account of absence of supporting documents.

HELD –

BOGUS PURCHASES –

Since the assessee couldn’t produce the parties before lower authorities and the fact that the parties have admitted to be indulging in bogus accommodation entries and even assessee couldn’t produce confirmation from the parties, it was held that the profit embedded in the purchases which is required to be brought to tax wherein the assessee had obtained bogus bills from these parties to avoid paying tax and to inflate costs. Thus, 12.5% of the alleged bogus purchase are bought to tax as an income embedded in these purchase.

DISALLOWANCE OF EXPENDITURE –

Donation couldn’t be allowed in absence of supporting bill/ details.

Rent expense of INR 54,000 was claimed as business expense, however, no details as to premises and its use for business, payer/landlord and rent deed etc. were not furnished by the assessee. Assessee only submitted self-supporting vouchers with respect to rent payment in cash without any evidence filed towards rent expense paid and therefore addition of rent expense was confirmed.

Cash expenses relating to printing & stationery, tea and refreshment, mobile charges, labour charges, travelling charges and sundry expenses are supported by self-made vouchers and it was held that it represents only 0.23% of total expense and keeping in view the preponderance of probability as also keeping in view nature of expense and also noting that the expense represents miniscule amount vis-à-vis total expense the said expenditure was allowed.

FULL TEXT OF THE ITAT JUDGEMENT

These are two appeals, filed by assessee, being ITA No. 4261 & 4262/Mum/2017 for AY 2009-10 and 2010-11 respectively , are directed against common appellate order dated 29.03.2017 passed by learned Commissioner of Income Tax (Appeals)-1, Thane (hereinafter called “the CIT(A)”) in Appeal No. 222 & 223/15-16, for assessment year’s 2009-10 & 2010-11 respectively, the appellate proceedings had arisen before learned CIT(A) from separate assessment order(s) both dated 19.01.2015 passed by learned Assessing Officer (hereinafter called “the AO”) u/s 144 r.w.s. 147 of the Income-tax Act, 1961 (hereinafter called “the Act”) for AY 2009-10 & 2010-11 respectively. Since both these appeals raises similar issues and common grounds, both these appeals were heard together and disposed of by this common order.

2. First we shall take-up appeal in ITA no. 4261/Mum/2017 for AY 2009-10 filed by the assessee . The grounds of appeal raised by the assessee in ITA no. 4261 /Mum/2017 for AY 2009-10 in memo of appeal filed with the Income-Tax Appellate Tribunal, Mumbai (hereinafter called “the tribunal”) reads as under:-

“1) In the facts and circumstances of case and in law, the learned CIT(A)-1, Thane erred in confirming the disallowance of purchases of Rs. 2,00,678/- as hawala purchase

a) without providing any opportunity of cross examination of the witnesses or documents relied upon by the Assessing Officer and thus violating the law laid down by Honorable Supreme Court in the case of Kishanchand Chellaram v, CIT (1980) 125 ITR 713 and Andaman Timber Industries v. Commissioner of Central Excise (Civil Appeal No. 4228 of 2006.)

b) on surmises and allegation that the suppliers have refunded cash to the appellant without any piece of evidence and enquiry in this regard,

c) by rejecting the books of account duly maintained by the appellant and audited u/s. 44AB merely on surmises and conjectures without pointing out any defect in the books of accounts

d) ignoring the quantitative reconciliation of purchases with corresponding sales, and

e) ignoring the Gross Profit and Net Profit margins trend of preceding years.

2) In the facts and circumstances of case and in law, the learned CIT(A)-1, Thane erred in sustaining disallowance of expenses of Rs. 1,33,253/- as unverifiable expenses merely on surmises and conjectures,

3) Without prejudice to ground no. 2 above, in the facts and circumstances of case and in law, the learned CIT(A)- 1, Thane erred in sustaining addition of disallowance of expenses of Rs. 1,33,253/- as against 20% of such expenses as accepted by the AO in his remand report.”

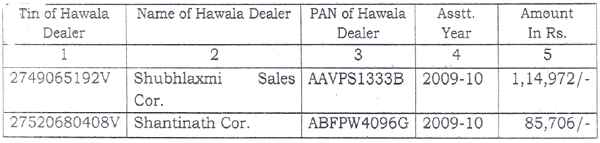

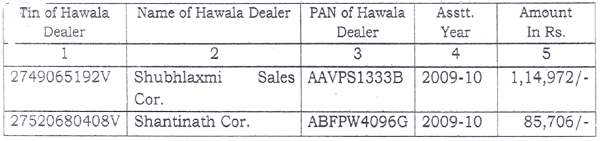

3. The assessee is reseller of Engineering Goods. The information was received by AO from DGIT (Inv.) , Pune that the Sales Tax Department, Mumbai has unearthed a racket involving more than 1935 Hawala Dealers involved in issuing bogus invoices to allow traders to claim tax credits and there are more than 37000 beneficiaries who claimed such bogus purchases and bogus tax credits. The Sales Tax Department recorded statements of these Hawala Dealers and these dealers have also filed an affidavits before Sales Tax Authorities wherein they admitted that they have not done any genuine business and stated to have been engaged in issuing bogus sales bills to various parties without supplying any material . The assessee was stated to be one of the beneficiary who had dealt with certain parties who were listed by the Sales Tax Department as hawala dealers .The information received by the AO stipulated that the assessee made following bogus purchases to the tune of Rs. 2,00,678/- which were stated to be from these alleged Hawala Dealers being bogus accommodation entry provider wherein the assessee merely obtained bogus bills without supply of any material , as detailed here under:

This information so received by the AO led to re-opening of the concluded assessment wherein notice dated 10.05.2013 was issued by the AO to the assessee u/s. 148 of the Act . The assessee was asked to produce various details in order to prove the genuineness of these purchases. The assessee denied before the AO to have taken any accommodation entries of bogus purchases. The assessee submitted that all the purchases are genuine and payments were made by cheque. It was submitted that all purchases were accounted for and genuine . It was submitted that stock of goods received vide these purchases were sold to customers and duly accounted for in books of accounts and credited to Profit and Loss Account. The assessee submitted that if purchases are disallowed then the whole corresponding sales against these purchases will become taxable which is not in accordance with law as the sale cannot happen without corresponding purchases. The assessee was asked by the AO to submit Invoices of Purchases, Bank Book, Cash Book, Ledger, Sales Register, Purchase Register , Financial Statements, Stock Register , Complete name and addresses of the parties from whom purchases were made and to whom corresponding sales were made. The AO also asked the assessee to furnish confirmation, delivery challans, lorry receipts and to produce the parties from whom purchases were made. The assessee failed to produce the aforesaid details before the AO during assessment proceedings which led the AO to make the additions to the tune of Rs. 2,00,678/- to the income of the assessee towards bogus purchases made by the assessee from these hawala dealers by invoking provisions of Section 69 of the 1961 Act. Further , additions of Rs. 65,18,663/- was made by the AO to the income of the assessee being 20% of the expenses incurred by the assessee because as per AO the assessee failed to prove the genuineness of these expenses and hence keeping in view that these expenses were not supported by documentary evidences and remained unverifiable, the AO rejected books of accounts of the assessee by invoking provisions of Section 145(3) of the 1961 Act and made addition of the income of Rs. 65,18,663/- in the hands of the assessee by invoking provisions of Section 37(1) of the Act, vide assessment order dated 19.01.2015 passed ex-parte u/s 144 read with Section 147 of the 1961 Act.

4. The assessee filed first appeal before Ld. CIT(A) and made detailed submissions as also filed additional evidences before learned CIT(A). The remand report was called by Ld. CIT(A) from AO. The AO submitted in its remand report that the assessee has now submitted ledger extracts, invoices, delivery challans and proof of making payments by cheque. The assessee furnished bank account statement and sated that all payments to these Hawala Dealers were made by cheque. However, the assessee failed to produce these parties before the authorities below for verification. The assessee also could not file confirmation letter from these parties regarding purchases made which led AO to conclude in its remand report that it is not possible to verify whether goods alleged to be purchased from these parties were infact received by the assessee. Thus, the AO rejected in its remand report, the additional evidences filed by the assessee and concluded that it is not possible to verify these purchases and to conclude that these purchases were genuine as only accommodation bills were obtained by the assessee from Hawala Dealers. The assessee in rejoinder reiterated its stand before the learned CIT(A) and prayed that these purchases are genuine by relying on various decisions of the Courts/Tribunal as cited in learned CIT(A) order, but Ld. CIT(A) did not agree with the contention of the assessee and entire additions of Rs. 2,00,678/- was confirmed by Ld. CIT(A) so far as alleged purchases made by the assessee from Hawala Dealers is concerned , vide appellate order dated 29.03.20 17 passed by learned CIT(A).Similar additions on account of alleged bogus purchases from hawala dealers were confirmed by Ld. CIT(A) for AY 2010-11 , vide common appellate order dated 29.03.20 17 , by holding as under:-

“8. The appellant in response to this addition has made very detailed submissions placed in the paper book filed with the submissions. The appellant also filed the following chart to show the gross profit and net profit rate for the year under consideration and the preceding and succeeding years –

| Particulars | 2008-09 | 2009-10 | 2010-11 |

| Sales | 3,27,97,864 | 3,31,94,606 | 3,78,21,332 |

| G.P. | 12,16,462 | 12,07,794 | 13,78,447 |

| GP Ratio | 3.71% | 3.64% | 3.64% |

| Expenses | 8,67,015 | 8,09,994 | 9,86,123 |

| NP | 3,50,730 | 4,00,610 | 3,96,026 |

| NP Ratio | 1.07% | 1.21% | 1.05% |

9. The appellants submissions alongwith additional evidence filed by the appellant were forwarded to the AO for his comments. The AO submitted his remand report dated 28.02.2017, making following observations –

“05. The assessee was also asked to produce the above mentioned parties for verification in support of genuineness of purchases of Rs. 3,45,048/-. The assessee furnished ledger extract, invoices, delivery challans and proof of payment made by cheque. In this regard the assessee furnished bank account statement and stated that all payment towards purchases made from Havala parties were made by cheque. However, the assessee failed to produce these parties for verification. The assessee also failed to furnish any confirmation letter from these persons regarding purchases made. Therefore, it is not possible to verify whether the goods purchased from these persons was actually received by the assessee. Therefore, for the reason mentioned by the AO in the assessment order the purchases made by the assessee amounting to Rs. 3,45,048/- are not genuine and only accommodation bills were obtained. In view of these facts, the additional evidence submitted by the assessee in support of purchases made of Rs. 3,45,048/- is not acceptable.

10. The appellant in his rejoinder submitted as under –

“1. Addition of Rs. 3,45,048/- in respect of alleged hmvala purchases

1.1 In this respect, we reiterate our earlier submissions before your good self that the purchases are genuine and are evidenced by payment through banking channels and the corresponding sales of such goods.

1.2 Appellant is a trader, Sales out of the above purchases are evidenced by the delivery challans, sale invoices and confirmation letters of buyers from the appellant. There cannot be any sales without purchases as held by Honorable Bombay High Court in the case of CIT v. Nikunj Eximp Enterprises (P) Ltd. (2013) 216 Taxman 171 (Bom).

1.3 The Learned Assessing Officer has commented in the remand report that the appellant has not produced the parties before him. We would like to submit that purchases were made in FY 2009-10. It is very difficult to produce the parties after a lapse of 7-8 years for a small purchases of Rs 50,000 to Rs.1,50,000/-. Purchases made though banking channels cannot be disallowed merely because the suppliers could not be presented before Assessing Officer.

Reliance is placed in this regard on the following decisions ;

i) Babulal C. Borana v. Third ITO (2006) 282ITR 251 (Bom) .

ii) CIT v. M.K. Brothers (1987) 163 ITR 249 (Guj)

ii) HI Lux Automotive (P.) Ltd v. ITO (2007) 163 Taxman 90 (Delhi)(Mag)

v) Jagdamba Trading Co. v. ITO (2007) 16 SOT 66 (Jodh)

v) ITO v. Permanand (2008) 25 SOT 11 (Jodh) (URO)

1.4 Further the Assessing Officer relying upon information received from Sales-tax department and affidavit alleged to be submitted by these parties before sales tax authorities. The learned Assessing Officer has not provided us opportunity to cross examine the witnesses and documents relied upon by him. Therefore the assessment order passed by AO is a nullity as held by Honorable Supreme Court in Andaman Timber Industries v. Commissioner of Central Excises (Civil Appeal No. 4228 of 2006), Kishanchand Chellaram v. CIT (1980) 125 ITR 713 and Bombay High Court in CIT v. Ashish International (Bom HC – IT Appeal No. 4299 of 2009).

1.5 Honorable M umbai has deleted the similar additions made solely on the basis of information received from sales tax department in the following cases :

i) DCIT v. Rajeev G. Kalathil ITA No. 6727/M um/2012 [2014] 51 com514 (M umbai – Trib.)

ii) Ramesh Kumar & Co. v. ACIT 21(1) [ITA No. 2959/M um/201 4]

iii) ITO v. Shri Deepak Popatlal Gala [ITA No 5920/M um/201 3]

iv) ACIT v. Shri Ramila Pravin Shah [ITA No. 5246/M um/201 3]

v) DCIT v. Shri Shivshankar R, Sharma [ITA No. 5149/M um/2014 &

vi) ITA No. 4260/M um/2015]

vii) ACIT v. Tristar Jewellery Exports Private Limited [ITA No. 7593/M um/2011]

viii) M /s. Imperial Imp & Exp. v. ITO 20(1)(5) [ITA 5427/ M um/2015]

ix) ITO vs. Shri Paresh Arvind Gandhi [ITA No. 5706/M um/201 3]

x) Shri Ganpatraj A. Sanghavi v/s. ACIT [ITA No 2826/M um/201 3]

xi) Shri Hiralal Chunilal Jain vs. ITO (ITA No. 45470/M um/201 4 dated 01.01.2016)

We therefore request your good self to kindly delete the addition of Rs. 3,45,048/- in respect of alleged bogus purchases.

11. I have carefully considered the appellant’s submissions, observations of the AO in the assessment order and remand report and the facts of the case. The appellant had shown purchases amounting to Rs. 3,45,048/- from the above listed parties which were appearing in the list of hawala dealers as per information received from the Sales-tax authorities of Maharashtra Government. The hawala dealers had admitted before the Sales-tax authorities in their statement / affidavit that they were providing only accommodation bills without there being any actual purchase/ sale of goods. Though the payment was received by the said parties from their customers through banking channels, however, after clearing of the cheques cash was withdrawn and handed over to the customers after deduction of nominal commission charges. On being asked to establish the genuineness of the purchases shown from the above listed parties, the appellant did not attend the proceedings before the AO. The details of various notices/ letters issued by the AO to the appellant and the appellants compliance to the same, has already been reproduced above in the form of a table. During the course of remand proceedings though the appellant has filed various documentary evidences like copies of purchase bills, copy of the appellants bank account showing payment to the parties through banking channels but the appellant has not placed on record any evidence to show that the goods had been delivered from the premises of the said parties to the appellant’s premises. No confirmation has been filed from the said parties. The parties have not been produced before the AO for verification. Thus the very existence of the parties has not been established by the appellant. Therefore, the facts of the appellants case are different from the facts of various case laws relied upon by him. The appellant does not maintain any day-to-day stock register. In the audit report no quantitative details of opening stock, purchases, sales and closing stock have been mentioned in column No. 28(a) which has been blank. Thus ii cannot be established that the goods shown as purchased from the above listed parties have been reflected into sales. For all these reasons it is held that the AO has rightly rejected the appellant’s books of accounts u/s. 145(3) of the IT. Act. The addition of Rs. 3,45,048/-made by the AO on account of unproved purchases is therefore, confirmed.

12. The facts of the appellant’s case for A.Y 2009-10 are similar to the facts of the A.Y 2010-11 as discussed above. The observations of the Assessing Officer in the remand report dated 26.03.2017 are also similar to the observations of the AO in the remand report dated 28.02.2017 for A.Y. 2010-11 discussed above. Therefore, for the detailed reasons discussed above, the addition on account of unproved purchases amounting to Rs.2,00,678/- made for AY 2009-10 is confirmed.”

5. The matter has now reached tribunal at the behest of the assessee and it was submitted by learned counsel for the assessee that the assessee has sale of Rs. 3,31,94,606/- for AY 2009-10 and small fraction of an amount of Rs. 2,00,678/- was added by Revenue to the income of the assessee on account of alleged bogus purchases from alleged Hawala Dealers. It was submitted that payments for these purchases were made through banking channel and reconciliation of purchases and sales were duly made. Our attention was drawn to submissions filed by the assesssee before Ld. CIT(A) which are placed in paper book filed with tribunal (page 2-13/pb) wherein chart of reconciliation of purchases with sales were also submitted, as under:-

Thus, it was claimed that purchases and sales were duly reconciled with complete detailed quantitative reconciliation of these purchases with corresponding sales. The Ld. DR on the other hand relied upon the appellate order of the Ld. CIT(A).

6. We have considered rival contentions and have perused the material on record. We have observed that the assessee is reseller of Engineering Goods . The information was received by AO from DGIT (Inv.) , Pune that the Sales tax Department,Mumbai has unearthed a racket involving more than 1935 Hawala Dealers involved in issuing bogus invoices to allow traders to claim tax credits and there are more than 37000 beneficiaries who claimed such bogus purchases and bogus tax credits. The Sales Tax Department recorded statements of these Hawala Dealers and these dealers have also filed an affidavits wherein they admitted that they have not done any genuine business and stated to have been engaged in issuing bogus sales bills to various parties without supplying any material . The assessee was stated to be one of the beneficiary who had dealt with certain parties who were listed by the Sales Tax Department as hawala dealers .The information received by the AO stipulated that the assessee made following bogus purchases to the tune of Rs. 2,00,678/- which were stated to be from these alleged Hawala Dealers being bogus accommodation entry provider wherein the assessee merely obtained bogus bills without supply of any material , as detailed hereunder:

This information so received by the AO led to re-opening of the concluded assessment wherein notice dated 10.05.2013 was issued by the AO to the assessee u/s. 148 of the Act . The assessee could not produce these parties before the authorities below nor confirmation could be filed by the assessee. The Sales Tax Department has recorded the statement of these parties wherein these alleged bogus accommodation entry providers have confirmed that they were indulging in providing bogus accommodation entries without supplying any material. The assessee however have submitted reconciliation statement of purchases from these alleged hawala entry operators with sales made . The payments were also made through banking channels. The assessee could not produce these parties before the authorities below and also the facts remains that these parties have admitted to be indulging in bogus accommodation entries without supplying of any material wherein only bogus accommodation bills were only issued by these parties to several beneficiaries without supplying any material. The assessee could not produce confirmations from these parties before the authorities below . Under these circumstances , it is the profit embedded in these purchases which is required to be brought to tax wherein the assessee had obtained bogus bills from these parties to avoid paying taxes and to inflate costs , while the material/goods were actually purchased from grey market at lower costs and also without paying taxes while the sales were made by the assessee which is recorded in books of accounts and reconciliation statement also reveals that purchases of these materials were supported by sales. The estimation of embedded profits in these purchases has to be an fair & honest estimation as stipulated by Hon’ble Supreme Court in the case of Kachwala Gems v. JCIT reported in (2007) 288 ITR 10(SC) . Keeping in view factual matrix of the case , we are of the considered view that if 12.5% of these alleged bogus purchases are brought to tax as an income embedded in these purchases in addition to and over & above income declared by the assessee will meet end of justice and will be an fair and honest estimation of income. Thus, we confirm additions to the tune of 12.5% of these purchases as an addition to income over and above what is declared by the assessee in return of income filed with Revenue. We order accordingly.

7. The second issue in these appeals concerns itself with disallowance of 20% of the aggregate expenditure of Rs. 3,25,93,318/- (after adjusting for disallowance of Rs. 2,00,678/- towards bogus purchases) wherein it led to the addition of Rs. 65,18,663/- to the income of the assessee made by the AO by rejection of books of accounts of the assessee u/s. 145(3) of the Act as the assessee did not filed details with the AO as we saw in preceding para’s of this order. The assessee filed first appeal with learned CIT(A) and submitted that these details were never called for by learned AO during assessment proceedings and the additions were made to the income of the assessee by the AO without calling for requisite details and the assessee was denied opportunity to explain its stand before the AO during assessment proceedings. The assessee filed details with Ld. CIT(A) along with additional evidences during the course of appellate proceedings . The learned CIT(A) forwarded these details and additional evidences to the AO and called for remand report from the AO . The AO submitted his remand report to learned CIT(A). The AO after considering the details and additional evidences filed by the assessee observed that the assessee had failed to submit documentary evidences in support of the expenses to the tune of Rs. 1,33,253/- for AY 2009-10 which were incurred in cash, for which the AO proposed to learned CIT(A) that the additions to this extent of Rs. 1,33,253/- towards disallowance of expenditure be sustained. Similarly for AY 2010-11, the AO proposed confirmation of additions by way of disallowance of expenditure to the tune of Rs. 1,11,420/- in the hands of the assessee as these expenses were incurred in cash and no documentary evidences were submitted by the assessee. The learned CIT(A) confirmed the additions to this extent by holding as under:

“ 13. As already discussed above, the appellant had not attended the assessment proceedings before the AO in response to various notices. The AO held that in the absence of documentary evidence, the various expenses claimed by the appellant remained unverified. He therefore, made a further addition of Rs.74,16,051/- being 20% of the expenses claimed by the appellant at Rs. 3,70,80,258/- (i.e. Rs. 3,74,25,306 – 3,45,048/-).

14. During the course of present proceedings the appellant submitted that the disallowance out of expenses had been made without asking for requisite details. It was submitted that the appellant had complete details of all expenses claimed in the Profit & Loss account alongwith necessary documentary evidence. The appellant’s submissions were forwarded to the AO for his comments. The AO submitted his remand report vide his letter dated 28.02.2017 making the following observations –

06. The AO also made addition of Rs. 74,16,051/- being 20% of total expenses of Rs. 3,70,80,258/- which were unverifiable as the assessee did not furnish any documentary evidence during scrutiny proceedings. The assessee was therefore, asked to furnish all ledger extract of expenses along with bills and invoices. In response to this the assessee submitted copy of ledger extract, bills, invoices etc. in support of some expenses but failed to furnish documentary evidence in support of some expenses as discussed herein-under :

07. On going through the profit and loss account it is seen that the assessee has debited following expenses :

| Donation | Rs.2,500/- |

| Printing & Stationary | Rs.4,576/-. |

| Rent | Rs. 54.000/- |

| Sundry Expenses | Rs. 5,701/- |

| Tea & Refreshment | Rs. 22,284/- |

| Travelling charges | Rs. 22,359/- |

| Total | Rs. 1,11,420/- |

The above mentioned expenses of Rs. 1,11,420/- were incurred in cash and no supporting bills are produced. The assessee simply produced self made vouchers without any supporting bills. Therefore, the AO had correctly disallowed 20% of these expenses as the same are not properly verifiable. In view of these facts the additional evidence produced by the assessee in support of expenses of Rs. 1,11,420/-is not acceptable.”

15. The appellant in his rejoinder to the remand report submitted as under –

2. Addition of Rs. 74,16,051/- (20% of entire expenses).

2.1. In this respect, we reiterate our earlier submissions that the scope of reassessment cannot be extended to matters other than arising out of reasons recorded u/s. 148 unless some other income escaping assessment comes to the knowledge of Assessing Officer in the course of reassessment. It is not the case of the Assessing Officer that during the course of reassessment, some other income escaping assessment has come to his knowledge. He has simple made an ad hoc addition of 20% of entire expenses (including purchases).

2.2. Without prejudice to above legal submission, during the remand proceedings, we have submitted all the evidences in respect of the expenses debited in accounts and Assessing Officer has verified the same. The learned Assessing Officer has commented that no supporting bills are produced in respect of the following expenses:

| Donation | 2,500/- |

| Printing & Stationary | 4,576/- |

| Rent | 54,000/- |

| Sundry Expense | 5,701/- |

| Tea & Refreshmen | 22,284/- |

| Travelling Charges | 22,359/- |

| Total | 1,11.420 |

In this respect, we have to submit that, in the course of business, such expenses are routinely incurred in cash and it is not possible to produce any evidence other than voucher for such expenses. In para 11.1 of our earlier submission, we have submitted the GP and NP ratio of the preceding years. The, NP ratio of the current year is in line with the preceding year and hence there is no suppression of profits. Further, reliance is placed on ACIT v. Arthur Anderson & Co. [2006] 5 SOT 393 (Mum) that no ad hoc disallowances can be made by the AO.

2.3 Further the appellant has already disallowed donation of Rs. 2,500/- in this computation of income, while filing return of income.

We therefore request your goodself to kindly delete the ad hoc addition of Rs. 74,16,051/- and oblige. “

I have carefully considered the appellant’s submissions, observations of the AO in the assessment order and remand report and the facts of the case. As far as the appellant’s contention that the scope of reassessment cannot be extended to matters other than those arising out of reasons recorded u/s. 148 unless some other income escaping assessment come to the knowledge of Assessing Officer in the course of reassessment is concerned, it is seen that once the assessment is re-opened the whole assessment is opened before the AO and the AO is not barred from carrying out investigation with respect to any matter related to the return of income. As far as the disallowance of expenses is concerned, it is seen that the AO during the course of remand proceedings after verification of the documentary evidence filed by the appellant has substantially accepted the appellant’s claim of expenses and has held only an amount of Rs. 1,11,420/- as disallowable as the appellant failed to produce supporting bills for claim of these expenses. The expenses had been incurred in cash without being supported by bills and other documentary evidence. Therefore, the disallowance on account of non-allowable expenses is restricted to Rs. 1,11,420/-. The AO is directed accordingly.

17. For A.Y. 2009-10 also in the remand report dated 26.03.2017 the

| AO has held an amount of Rs. 1,33,253/- on account of following expenses having been incurred in cash and without being supporting bills etc – | |

| Donation | Rs4,001/- |

| Printing & Stationery | Rs6,238/- |

| Rent | Rs54,000/- |

| Sundry expenses. | Rs4,370/- |

| Tea & Refreshment | Rs23,282/- |

| Mobile Charges | Rs 8,095/- |

| Labour Charges | Rs 12,985/- |

| Travelling Charges | Rs.20,282/- |

| Total | Rs 1,33,253/- |

18. Therefore, the disallowance on account of non-allowable expenses for A.Y. 2009-10 is restricted to Rs. 1,33,253/-. The Assessing Officer is directed accordingly.

8. Thus in nutshell additions of Rs. 1,33,253/- was upheld by the Ld.CIT(A) which is a matter of challenge by the assessee before the tribunal as second appeal is filed by the assessee challenging confirmation of additions to the tune of Rs. 1,33,253/- by learned CIT(A). The learned counsel for the assessee has vehemently argued that these expenses are business expenses which have been incurred for business of the assessee although they were incurred in cash and are supported by self made vouchers . On the other hand Ld. DR relied upon on the order of the Ld. CIT(A).

9. We have considered rival contentions and perused the material on We have also considered the nature of these expenses and we are of the considered view that out of these expenses of Rs. 1,33,253/- disallowed by the authorities below , an amount of Rs. 4,001/- incurred towards Donations could not be allowed in the absence of supporting bills/details and its connection with business of the assessee or in the absence of requisite confirmatory details to be eligible for allowability as deduction u/s 80G or other relevant provisions of the 1961 Act. In the absence of supporting invoice/details , the disallowance of expense of donation of Rs. 4,001/- stood confirmed. We order accordingly.

We have also observed that rent expenses of Rs. 54,000/- was paid and claimed as business expenses but no details as to premises and its user for business, payer/landlord and rent deed etc. were furnished by the assessee before authorities below and in our considered view, in the absence of details of premises taken on rent by the assessee and its user wholly and exclusively for business purposes, these rent expenses cannot be allowed as business deduction. The assessee has only submitted self supporting vouchers with respect to payment of rent in cash without any details as to the premises on which rent its paid and its user for business purposes and under these circumstances, we disallow the claim of the assessee and confirm additions to the tune of Rs. 54,000/- claimed to be incurred by the assessee for alleged rent of which no details are filed even before us. This is the third stage of litigation before us after framing of assessment by the AO and first appeal adjudicated by learned CIT(A) wherein at both the stages claim of the assessee was rejected by authorities below. Before us also there is no evidence filed towards rent expenses paid by the assessee. Thus , under these circumstances, we confirm the additions as were made by authorities below. We order accordingly.

So far as rest of the expenses to the tune of Rs. 75,252/- are concerned which were claimed as business expenses but were disallowed and added back by authorities below, the same relates to expenses on account of Printing and Stationary, Tea and Refreshment, Mobile charges, Labour charges, Travelling charges and Sundry Expenses. These expenses were claimed to be incurred in cash and are supported by self made vouchers. These expenses were claimed to have been incurred for business purposes. We have observed that the assessee has incurred total expenses of Rs. 3,25,93,318/-(after adjusting disallowance of Rs. 2,00,678/- towards alleged bogus purchases) and these expenses of Rs. 75,253/- disallowed by the AO are minor expenses vis-a-vis aforesaid total expenses incurred by the assessee and represents only 0.23% of the total expenses incurred by the assessee . These expenses were incurred in cash and the assessee had produced self made vouchers but it is claimed by the assessee that these expenses were incurred for business purposes. Keeping in view preponderance of probability as also keeping in view nature of these expenses and also noting that these expenses represents miniscule amount vis-a-vis total expenses incurred by the assessee , we found no reason and justification for doubting the contentions of the assessee as the assessee in any case submitted supporting self made vouchers prepared by the assessee. Thus we accept contention of the assessee keeping in view factual matrix of the case and keeping in view smallness of the amount involved and our decision shall not have precedential value for adjudicating appeals in the case of other assessee’s. Thus , these expenses of Rs. 75,253/- stood allowed. We order accordingly.

10. In the result, appeal of the assessee in ITA No.4261/Mum/2017 for AY 2009-10 stood partly allowed as indicated above.

11. Our decision in ITA no. 4261/Mum/2017 for AY 2009-10 shall apply mutatis mutandis to appeal of the assessee in ITA no. 4262/Mum/20 17 for AY 2010-11 as the facts are similar.

12. In the result, appeal of the assessee in ITA No.4262/Mum/2017 for AY 2010-11 stood partly allowed as indicated above.

13. In the result, appeal of the assessee in ITA No.4261/Mum/2017 for AY 2009-10 and in ITA no. 4262/Mum/2017 for AY 2010-11 stood partly allowed as indicated above.