ITR filing season is on, the due date for the Individuals is 31st July 2024 and everybody has started compiling the information regarding their income & deductions. Here are some very important aspects one should consider whether they are filing their ITR by themselves or through a tax professional

1. Knowing whether you need to file ITR

This is again one of the most important aspect- knowing if you are required by law to file the ITR or not. Though it depends on a lot of factors, I am trying to list the most important ones here:

a) Your taxable income exceeds the exemption limit which is Rs 2.5 lakhs for normal taxpayers, Rs 3 lakhs for Senior citizens (i.e. aged 60-80 years) and Rs 5 lakhs for Super senior citizens (aged 80 & above). If you are earning income which is more than the exemption limit, you are required to file the ITR.

Important thing to note here is, one need to consider the income before availing any eligible deduction under Section 80C to 80U.

So, if you earn say 4 lakhs a year and you have invested 1.5 lakhs in 80C eligible instruments. So, basically you don’t have to pay any tax, still you are required to file the ITR as your taxable income (4 lakhs) is more than the exemption limit (2.5 lakhs)

b) Annual Sales turnover above Rs 60 lakhs- You need to file ITR irrespective of your income

c) Annual Professional income is above Rs 10 lakhs

d) If you have TDS/TCS exceeding Rs 25000/Rs 50000 for Senior citizens

e) If you are holding any foreign assets: Ordinary Residents holding foreign assets which requires specific disclosures in ITR. Foreign assets could be foreign bank accounts, foreign properties, financial assets, signing authority, etc.

f) Individuals paying electricity bill over Rs 1 lakh during the FY are required to file ITR mandatorily.

g) Individuals who have deposited more than Rs 50 lakhs in one or more saving bank accounts during the FY

h) Individuals who have deposited more than Rs 1 crore in one or more current bank accounts during the FY

i) Individuals who have spent more than Rs 2 lakhs on overseas travel for themselves or for any other person during the FY.

Also, one has to file ITR for the following cases:

1) You need to file ITR to claim losses

2) You need to file ITR for claiming refund of taxes (for instance: to claim refund of TDS)

3) You need to file ITR even if you don’t have any tax liability (for instance your tax liability is fully covered by the TDS deducted by employer, you are still required to file ITR)

2. Choosing between New & old regime

This is an important decision to make and there are a lot of factors around it. Everybody has to decide on case-to-case basis whether they should opt for old or new regime. New regime is the default regime set by the government. Anybody wishing to opt for old regime has to file form 10IEA.

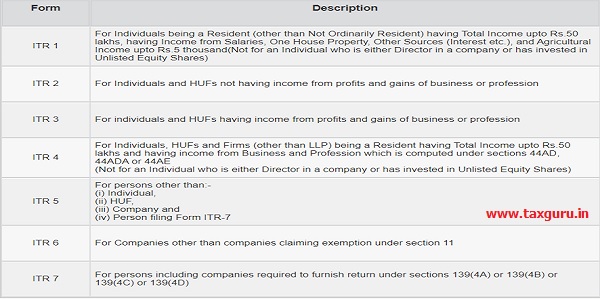

3. Choosing the correct ITR form

Choosing the correct ITR form is one of the first & most important aspect to ensure the ITR is filed accurately. There are a lot of forms available as furnished below along with the short description (these are available in the income tax e-filing portal itself). One must carefully choose the ITR form.

4. Declaring income in full and in the accurate way

One need to declare all the incomes (whether those are exempt or taxable) in the ITR accurately in order to avoid any mistakes in the ITR which warrants income tax notices. Following could be some aspects to keep in mind:

a) Declaring the income under the correct head

The most important aspect of filing an accurate ITR is to declare the income under the appropriate head. We have 5 heads of income viz. Salary, House property, Business & Profession, Capital gains and Other sources. It is pertinent to understand the nature of income one is earning which aids in accurate reporting under the correct head

b) Reconciling the income and taxes with form 16/16A, 26AS, AIS & TIS

Form 26 AS, among other things, has the details about the taxes deducted (TDS & TCS) on your income and the advance taxes paid by you. Thus, it acts as a quick reference to arrive at the taxable income. Not reporting income which are reported in 26 AS attracts income tax notices. Also, the income needs to be reported under the correct head. 26AS also states the section under which TDS is deducted, which might help in furnishing income under correct head.

Form 16/16A has the details about the tax deducted in a comprehensive way (especially for salaried individuals) as it has the details about the component of salary which helps a great deal in working out the ITR

AIS & TIS provides a lot of information about your income & things to report (which you might miss otherwise). However, it might have some erroneous, duplicate or incomplete information as well. So, a careful consideration of AIS & TIS is must.

It is important to verify & reconcile the details in 26AS in order to ascertain & get rectified any errors that might be there due to incorrect reporting in their TDS return by the deductor.

Also Read: Best way to file taxes as a freelancer

c) Declaring exempt income

It is often presumed that we do not need to declare the exempt income as there is no tax on it. This is not at all true, it is mandatory to report even the exempt income in the ITR. So, it is very important to determine the various components of exempt income, why the income is exempt and how to report it.

d) Declaring interest income

Interest income is one such income, which taxpayers do not pay heed to. It is often not declared especially in those cases where the TDS on interest income is not deducted. This is not at all a good & safe practice. One must declare all types of interest income in the ITR. In order to declare the interest income properly, one need to understand it’s taxability, as some type of interest incomes are not taxable, some enjoy deduction and some are fully taxable. Thus, it needs to be treated accordingly

e) Reporting income from multiple employers

Often, we change our job in the middle of the year and thus we have salary income from multiple employers. It is important to consider & report the income from all the employers in the ITR.

5. Claiming eligible deductions

Who doesn’t like to save tax? Everybody likes to and when you like it, you should know about the deductions that are there which comes to our rescue when it comes to reducing the tax liability. A proper acquaintance to available deductions could give you an edge in planning taxes in advance and aids in investing & spending the right way. Having said that, it is also very important to claim only eligible deductions, for which we have the proper receipts & proof.

6. Filing important accompanied forms

Sometimes, we need to file accompanying forms in order to claim certain deductions while filing the ITR. It needs to be ensured that those forms are filed in time. For instance, one need to file form 10BA to claim deduction under section 80GG and form 10E to claim relief for salary in arrears under section 89(1).

7. Filing the ITR on time

Filing the ITR on time is pretty important considering the repercussions that are there if we do not file it in time. Following are some:

a) Levy of penalty: Not filing the ITR on time will attract a penalty ranging from Rs 1000 to Rs 10000 depending upon the period of delay, amount of taxable income etc.

b) Levy on interest: Not only you have to pay the late fee, one also has to pay the interest for delay in filing the return & payment of taxes, so better be on time than to pay extra.

c) Ineligibility to carry forward losses: We could claim the losses under any head in ITR only if we file the ITR within the due date. A belated ITR makes us ineligible to claim any type of loss.

8. Claiming TDS

TDS is effectively & technically taxes paid by you in advance. So, why not claim it in full & utilize it towards settlement of tax liability or claim refund. In order to claim TDS one must ensure its correctness with respect to amount, section, TAN of the deduction etc. One must also ask for the TDS certificate from the deductor.

9. Set-off & carry forward of losses

One could be earning income or incurring losses from various sources. Income tax act states the rules for setting off losses under various sources & carrying it forward to future years. There are various restrictions in setting off losses under one head with income under other head and also there are time limits up to which certain losses can be carried forward in future. Thus, it is very important to understand the nature of loss, the set-off & carry forward rules around it to gain the max. benefit out of it.

10. Making proper & important disclosures

Apart from proper reporting of income & deductions, a very important aspect to an accurate ITR is to make proper disclosures. Following could be some of the instances:

a) Reporting active bank accounts

b) Reporting directorship details

c) Disclosing assets beyond a certain limit

d) Disclosing foreign assets

11. Paying taxes in full before submission

One need to ensure that the entire tax liability is paid in full & properly reported before submitting the ITR. Not doing so will make your ITR defective.

12. Verifying the filed ITR

Filing and not verifying the ITR is as good as not filing the ITR as the ITR filing process completes only once the filed ITR is verified. ITR can be verified in the following ways- net banking, Bank account, Aadhaar OTP, generating EVC through bank ATM, through Demat account and lastly by sending the copy via post to CPC.

Conclusion: Filing your ITR accurately and timely is crucial to avoid penalties and ensure compliance with tax laws. By understanding and following these key aspects, you can navigate the ITR filing process with confidence. Stay informed, make informed decisions, and ensure all income, deductions, and disclosures are correctly reported.

****

Disclaimer: The above post is only for the purpose of academic discussion and should not be construed as any legal opinion in any matter whatsoever.

The author is a CA in practice at Delhi and can be contacted at: E-mail: abhinandansethia90@gmail.com, Mobile: +91-9811741451.

(Republished with amendments)

Author Bio

Dear Sir, I have done an inspection for export goods and the company has deposited TDS on the full amount paid to me including travelling and other expenses spent by me for the visit. This created a problem that my income is over calculated under ITR. How can I rectify my income while filling the return? Say, I charged 10,000/- for inspection and expenses paid by me were 20,000/-. The company paid me full amount by deducting 3,000/- as TDS. However, my income is only 10,000/- instead of 30,000/-. I got a letter from the company about the details of TDS. How can I proceed to file my return online? Thank you

How should we calculate the Income of gig workers for ITR (applying for loan)?

If the employer does not issue Form 16 to date of FY 2019-20 what is the option left to the employee? Can he lodge a complaint with the employee’s ITO for immediate redressal?

thanks for enlightning general tax payers regarding filing Income Tax Returns.Pl clarify if it is required

to a person having net capital losses arising due to sale of equity mutual funds in November 2019 in which investment was made in May 2018 and the person does not want to carry forward the losses,to next year by filing ITR-2.regards

Respected sir,

It is very useful and important information and mostly correct time it was done sir

thank you so much sir

ch.parvateesam

Thank you

Dear Sir,

Thanks for sharing knowledgeable information

Thank you