Case Law Details

Aakash Developers Vs ACIT (ITAT Mumbai)

ITAT Quashes Reassessment Because AO Relied on Investigation Wing Report Without Independent Inquiry; ITAT Deletes On-Money Addition Because Revenue Failed to Produce Seized Evidence; Reassessment Set Aside Because Borrowed Satisfaction Cannot Confer Jurisdiction Under Section 147; ITAT Rules Denial of Cross-Examination Violated Principles of Natural Justice; ITAT Holds Reassessment Cannot Be Based Solely on Investigation Wing’s Excel Sheet.

The Income Tax Appellate Tribunal (ITAT), Mumbai, allowed the appeal of the assessee and quashed the reassessment proceedings initiated under Section 147 of the Income-tax Act, 1961, holding that the reopening was based on borrowed satisfaction and lacked independent application of mind by the Assessing Officer (AO). Consequently, the addition of ₹45 lakh towards alleged unexplained investment in the form of cash on-money and the reassessment order itself were held to be invalid.

The assessee, a partnership firm engaged in the business of builders and developers, had originally filed its return declaring total income of ₹88.45 lakh. Subsequently, the assessment was reopened through notice issued under Section 148 dated March 31, 2017, on the basis of information received from the Investigation Wing alleging that the assessee had paid ₹45 lakh in cash as on-money to Cosmos Group for the purchase of a flat. The information was stated to have emerged from search proceedings conducted in the case of Cosmos Group.

During reassessment proceedings, the assessee objected to the reopening and repeatedly sought copies of the seized material and statements of Cosmos Group directors that formed the basis of the proceedings. The assessee also requested an opportunity to cross-examine those persons whose statements were proposed to be used against it. However, according to the Tribunal, the relevant documents and statements were never furnished to the assessee, either during assessment proceedings or before the Commissioner of Income Tax (Appeals) [CIT(A)].

The Tribunal noted that the entire reassessment was founded on an excel sheet prepared by the Investigation Wing based on certain information allegedly retrieved from email accounts concerning advances and bookings relating to Cosmos Group properties. The excel sheet reflected the assessee’s name and alleged cash payments of ₹25 lakh and ₹20 lakh on different dates. However, the Tribunal observed that the excel sheet itself had been prepared by the Investigation Wing and that there was no reference to any original seized material directly evidencing payment of on-money by the assessee. The Tribunal found that no independent inquiry or verification had been undertaken by the AO either before issuing notice under Section 148 or during the reassessment proceedings.

Relying on the Supreme Court decision in ITO v. Lakhmani Mewal Das, the Tribunal reiterated that reassessment proceedings require a rational connection or live link between the material available with the AO and the belief that income chargeable to tax has escaped assessment. The expression “reason to believe” cannot be equated with “reason to suspect.” The Tribunal held that vague, indefinite, or remote material cannot justify reopening of completed assessments. Applying these principles, it concluded that the primary jurisdictional condition for invoking Section 147 was absent in the present case.

The Tribunal further observed that there was no evidence demonstrating that the assessee had actually paid on-money to Cosmos Group. It also noted discrepancies in the excel sheet relied upon by the Revenue, observing that the alleged payments related to different financial years, thereby raising doubts regarding the basis for reopening the assessment for the year under consideration. The Tribunal found that the AO had issued notice under Section 148 without proper application of mind and solely on the basis of information supplied by the Investigation Wing.

Another significant issue considered by the Tribunal was the denial of cross-examination. The assessee had consistently requested an opportunity to cross-examine the promoters and directors of Cosmos Group whose statements were allegedly relied upon by the Revenue. The Tribunal held that failure to provide such opportunity amounted to a serious violation of the principles of natural justice. Referring to the Supreme Court judgment in Andaman Timber Industries v. CCE, it observed that where statements of third parties form the basis of adverse conclusions, denial of cross-examination renders the proceedings legally unsustainable.

In view of these findings, the Tribunal held that the notice issued under Section 148 was invalid and liable to be quashed. Since the reassessment proceedings themselves were held to be void ab initio, the consequential addition of ₹45 lakh towards alleged unexplained investment in cash on-money could not survive. The appeal of the assessee was accordingly allowed.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

The present appeal filed by the assessee arises out of order dated 17/01/2025 passed by NFAC, Delhi for assessment year 2010-11 on following grounds of appeal :

“1. The Hon CIT(A) erred in upholding the re-opening of assessment u/s 147 of the I. Tax Act 1961, by issue of the notice u/s 148 dt. 31.03.2017, not appreciating that there was total lack of independent and valid reason on the part of the Id AO to believe that any income chargeable to tax had escaped assessment and for this reason the re-opening of assessment u/s 147 was bad-in-law and the asst. order flowing therefrom, being the order u/s 143(3) r.w.s. 147 was also invalid and bad in law and required to be struck down on that count.

2. The Hon CIT(A) erred in upholding addition of Rs. 45,00,000/- as unexplained investment on account of alleged cash on-money paid for purchase of flat no. 3, PH-2, Bloc KD, Cosmos Hawaiian, Thane (W) from Cosmos Group, not appreciating that when such addition was without any evidence and ignoring all the contentions made in the course of appeal proceedings by the appellant. The addition Rs. 45,00,000/- as undisclosed investment is not warranted and is required to be deleted.

3. The Hon CIT(A) erred in dismissing the ground of the appellant that the information relied upon by the Id AO i.e. the statements of the members of the Cosmos Group was without affording your appellant with opportunity to cross examine the said persons, inspite of specific request for the same and thereby the salient principles of equity, fair play and natural justice were breached and for this reason no cognizance should be taken of such adverse information, if any, unless reasonable opportunity of cross examination was granted to the appellant.

4. The appellant craves leave to add, alter, amend, delete and/or vary any of the above grounds of appeal/relief claimed at any time before the decision of the appeal.”

Brief facts of the case are as under:

2. The assessee is a partnership firm engaged in the business of Builders and Developers originally return of income was filed by the assessee on 22/09/2020 and letter on revised on 20/08/2011, declaring total income of Rs. 88,45,423/-.

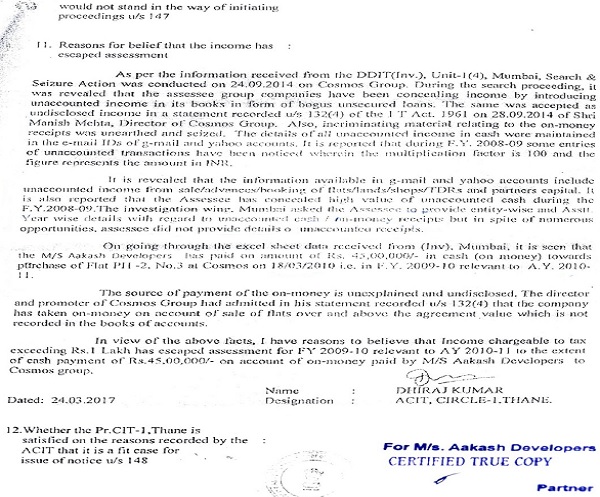

2.1 The assessment of the assessee was reopened by issuing notice u/s. 148 dated 31/03/2017 based on the information received from DDIT(INV.) unit, 1(4) Mumbai holding that the assessee advanced Rs. 45,00,000/- in cash as on money towards purchase of flat from Cosmos Group during the year under consideration.

2.2 The Ld.AO upon receipt of the information recorded reasons by observing as under :

2.2 Subsequently, notice u/s. 143(2) was issued and the assessee was provided with the copy of the reasons recorded. In response to the notice assessee file a letter dated 18/09/2017 objecting the reopening of the assessment for the year under consideration. The assessee also sought for the documents seized from the searched premises and the statement of the directors of Cosmos Group based on which the assessment was reopened. The Ld.AO there after completed assessment on 28/12/2017 making addition of alleged cash money of Rs.45,00,000/- paid to Cosmos Group towards purchase of premises.

Aggrieved by the order of the Ld.AO assessee preferred appeal before the Ld.CIT(A).

3. Before the Ld.CIT(A) assessee challenged reopening of the assessment as well as additions made on merit. The Ld. CIT(A) upheld the action of the Ld.AO.

Aggrieved by the order of the Ld.CIT(A) the assessee is in appeal before this Tribunal.

4. The Ld.AR at the outset submitted that in spite of specific return request made by the Ld.AO during the course of the assessment proceedings copies of the alleged incrementing evidences based on which the Ld.AO presume payment of Rs. 45,00,000/- in cash to Cosmos Group was not shared with the assessee. He submitted that, assessee made request vide letters dated 18/09/2017, 07/11/2017, 14/12/2017, 18/12/2017 placed in the paper book filed before this Tribunal. He submitted that the assessee sought for the materials that formed bases for reopening of the assessment. It is submitted that, alleged incrementing seized materials were never provide to the assessee either during the assessment proceedings or before the Ld. CIT(A). He submitted that entire addition of 45,00,000/- made by the Ld.AO is based on an excel sheet prepared by the Investigation wing, and no further verification was carried out by the Ld.AO, neither before issuance of notice u/s.148 nor during the assessment proceedings. The Ld.AR thus emphasised that, based on borrowed satisfaction reopening of the assessment was done in the case of assessee for the year under consideration.

4.1 The Ld.AR submitted that, statements of the member of Cosmos Group recorded by the Investigation wing does not implicate the assessee having made any payment of on-money in cash as alleged by the authorities below. He submitted that there is no evidences against assessee with the revenue authorities to establish that on-money at Rs. 45,00,000/- was paid in cash by the assessee to the Cosmos Group. The Ld.AR emphasised that, the assessing officer solely relied on the information provided by the Investigation wing without independent opinion having established that income escaped assessment the year under consideration.

4.2 The Ld.AR further submitted that, cross-examination of the persons whose statement were used to make addition in the hands of the assessee was been provided at any stage by the Ld.AO and was denied it in the assessment order. The Ld.AR thus submitted that there is a gross violation of principle of natural justice in the present facts of the case.

4.3 He placed reliance on following decision in support of this contention:

“i) ITO-vs-Lakhmani Mewal Das (1976) 103 ITR 437 (SC) [1976]

ii) PCIT-vs-Shodiman Investments (P.) Ltd., 422 ITR 337 (Bombay) [2018]

iii) PCIT-vs-Meenakshi Overseas (P.) Ltd., 395 ITR 677 (Delhi) [2017]”

4.4 On the contrary, the Ld.DR relied on the orders passed by the authorities below.

We have perused the submissions advance by both sides in the light of record placed before us.

5. Perusal of the reasons recorded reveals that the assessing officer received information from the Investigation wing stating that some incrementing materials was found during the search proceedings at Cosmos Group relating on-money receipts from assessee before us.

5.1 It is noted that, based on the information that was seized from the mail account regarding sales/advances/booking of flat/land/shops, and excel sheet was prepared wherein the assessee’s name is reflected. On perusal of the excel sheet placed at page 22 and 23 of the paper book, it is noted that, assessee is alleged to have paid Rs.25,00,000/- on 18/03/2010 and 20,00,000/- on 26/06/2010 totalling to Rs.45,00,000/-. It is noted that the two dated noted in the excel sheet falls in 2 different financial years relevant to assessment years 2010-11 and 2011-12. Admittedly, the excel sheet is prepared by the Investigation wing and the assessment was reopened in the case of assessee.

5.2 In our considered opinion, relevant seized material to the formation of belief that income escaped assessment is absent. It is noted that there is no tangible material that forms the basis of such belief, is very much evident from the reasons recorded. The prima facie condition before forming reason to believe to assume jurisdiction u/s.147 of the Act, is not satisfied in the present facts of the case. There is no reference to any document except for the excel sheet prepared by the Investigation wing and statement recorded of the promoters and directors of Cosmos Group. At this juncture we refer to categorical observation of Hon’ble Supreme Court in case of ITO vs. Lakhmani Mewal Das that reads as under :

“As stated earlier, the reasons for the formation of the belief must have a rational connection with or relevant bearing on the formation of the belief. Rational connection postulates that there must be a direct nexus or live link between the material coming to the notice of the Income-tax Officer and the formation of his belief that there has been escapement of the income of the assessee from assessment in the particular year because of his failure to disclose fully and truly all material facts. It is no doubt true that the court cannot go into the sufficiency or adequacy of the material and substitute its own opinion for that of the Income-tax Officer on the point as to whether action should be initiated for reopening assessment. At the same time we have to bear in mind that it is not any and every material, howsoever vague and indefinite or distant, remote and farfetched, which would warrant the formation of the belief relating to escapement of the income of the assessee from assessment. The fact that the words “definite information” which were there in section 34 of the Act of 1922, at one time before its amendment in 1948, are not there in section 147 of the Act of 1961, would not lead to the conclusion that action can now be taken for reopening assessment even if the information is wholly vague, indefinite, farfetched and remote. The reason for the formation of the belief must be held in good faith and should not be a mere pretence.)

The powers of the Income-tax Officer to reopen assessment, though wide, are not plenary. The words of the Statute are “reason to believe” and not “reason to suspect”. The reopening of the assessment after the lapse of many years is a serious matter. The Act, no doubt, contemplates the reopening of the assessment if grounds exist for believing that income of the assessee has escaped assessment. The underlying reason for that is that instances of concealed income or other income escaping assessment in a large number of cases come to the notice of the income-tax authorities after the assessment has been completed. The provisions of the Act in this respect depart from the normal rule that there should be, subject to right of appeal and revision, finality about orders made in judicial and quasi-judicial proceedings. It is, therefore, essential that before such action is taken the requirements of the law should be satisfied. The live link or close nexus which should be there between the material before the Income-tax Officer in the present case and the belief which he was to form regarding the escapement of the income of the assessee from assessment because of the latter’s failure or omission to disclose fully and truly all material fact was missing in the case. In any event, the link was too tenuous to provide a legally sound basis for reopening the assessment. The majority of the learned judges in the High Court, in our opinion, were not in error in holding that the said material could not have led escaped assessment because of his failure or omission to disclose fully and truly all material facts. We would, therefore, uphold the view of the majority and dismiss the appeal with costs.”

5.3 Admittedly, in the present facts of the case there is no evidence with the assessing officer to establish that assessee paid any on-money to the Cosmos Group towards the purchase of the flat. It is also noted that the Ld.AO issued the notice for opening without application of mind. If one look into the excel sheet, prepared by the Investigation wing, the income that could be alleged to have escaped assessment is Rs.24,00,000/-. It is further noted that, the assessee was not granted opportunity to cross examine the promoter and the directors of the Cosmos Group whose statement formed basis and was used against assessee to make addition. Hon’ble Supreme Court in case of Andman Timbers Industries vs. CCE reported in (2015) 62 taxmann.com 3 observed as under :

“6. According to us, not allowing the assessee to cross-examine the witnesses by the Adjudicating Authority though the statements of those witnesses were made the basis of the impugned order is a serious flaw which makes the order nullity inasmuch as it amounted to violation of principles of natural justice because of which the assessee was adversely affected. It is to be borne in mind that the order of the Commissioner was based upon the statements given by the aforesaid two witnesses. Even when the assessee disputed the correctness of the statements and wanted to cross-examine, the Adjudicating Authority did not grant this opportunity to the assessee. It would be pertinent to note that in the impugned order passed by the Adjudicating Authority he has specifically mentioned that such an opportunity was sought by the assessee. However, no such opportunity was granted and the aforesaid plea is not even dealt with by the Adjudicating Authority. As far as the Tribunal is concerned, we find that rejection of this plea is totally untenable. The Tribunal has simply stated that cross-examination of the said dealers could not have brought out any material which would not be in possession of the appellant themselves to explain as to why their ex-factory prices remain static. It was not for the Tribunal to have guesswork as to for what purposes the appellant wanted to cross-examine those dealers and what extraction the appellant wanted from them.”

7.1 Based on the above discussion we do not find any reasons to uphold the validity of the notice issued u/s.148 dated 31/03/2017. Accordingly the notice issued u/s.148 dated 31/03/2013 as herein above quashed as consequence the reassessment order passed dated 28/12/2017 becomes bad in law as void ab initio. As the entire assessment proceeding has been quashed the advance made by the assessing officer does not survive and deserves to be deleted.

Accordingly the grounds raised by the assessee stands allowed.

In the result the appeal filed by the assessee stands allowed.

Order pronounced in the open court on 29/08/2025

Author Bio