Reassessment of Income Escaping Assessment: Pending reassessment proceedings on 1st April 2026 under Income Tax Act, 1961; issuance of fresh notices post-1st April 2026; Transition to the reassessment framework for Tax Year 2026-27 onwards under Income Tax Act, 2025

The document explains the reassessment framework under the Income Tax Act, 2025, covering provisions for reopening cases of income escaping assessment and the transition from the earlier law. Sections 279 to 286 of the new Act correspond to existing provisions but introduce a more structured process, including mandatory show-cause notice, consideration of taxpayer response, and approval-based decision-making before issuing reassessment notices. It defines “information suggesting escaped income” and clarifies circumstances where procedural steps may be skipped with prior approval. The Act extends time limits for issuing notices compared to the earlier law and prescribes a one-year limit for completing reassessment. Importantly, the transition framework ensures that reassessment proceedings for earlier years continue under the Income-tax Act, 1961, even after 1 April 2026. Parallel proceedings under both Acts are permitted, and approvals, penalties, and compliance for earlier years remain governed by the old law, ensuring continuity and avoiding disruption.

REASSESSMENT OF INCOME ESCAPING ASSESSMENT

A. REASSESSMENT FRAMEWORK UNDER THE NEW ACT

Q5.1 What are the provisions for reopening of assessment (income escaping assessment) under the Income-tax Act, 2025?

Ans. The provisions for assessment or reassessment of income which has escaped assessment are contained in Sections 279 to 286 of the Income-tax Act, 2025. These correspond to Sections 147, 148, 148A, 148B, 149, 150, 151, and 153 of the Income-tax Act, 1961. The framework has been streamlined and made more structured:

| Subject | Old Act Section | New Act Section |

| Power to assess/reassess escaped income | 147 | 279 |

| Issue of notice for reassessment | 148 | 280 |

| Procedure before issuance of notice (show cause) | 148A | 281 |

| Time limit for notices | 149 | 282 |

| Assessment in pursuance of appellate/court orders | 150 | 283 |

| Sanction for issue of notice | 151 | 284 |

| Other provisions (rate of tax, dropping of reassessment proceedings) | 152 | 285 |

| Time limit for completion of assessment, reassessment and recomputation | 153 | 286 |

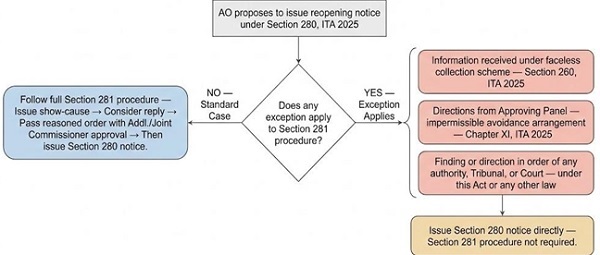

Q5.2 Briefly explain the procedure for issuing reopening notice under the Income Tax Act, 2025.

Ans: The procedure for issuing a notice under section 280 of the Income Tax Act, 2025, where income has escaped assessment for the relevant tax year is briefed as under:

i) Information — The assessing officer must have information suggesting income has escaped assessment.

ii) Show-cause notice — Before issuing notice u/s 280 of the Act, Assessing officer must provide an opportunity of being heard to the assessee by issuing a show-cause notice under section 281(1) of the new Act, providing the information which suggests that income chargeable to tax has escaped assessment and giving an opportunity to respond within the prescribed time.

iii) Consider reply — AO must consider the assessee’s response.

iv) Reasoned order — Pass an order under section 281(3) with the prior approval of the Additional commissioner or Joint Commissioner, deciding whether it is a fit case for reassessment.

v) Issue of reopening notice under section 280 of the Act.

Note: Under some situations as provided in Section 281(4) of the Act, the assessing officer is not required to follow the procedure provided in section 281 of the Act. However, even in such cases, the approval of Additional commissioner or Joint Commissioner is mandatory before notice under section 280 is issued.

Q5.3 For the purposes of reopening of assessment under the new Act, what is considered to be ‘information suggesting that income has escaped assessment’?

Ans. Section 280(6) of the Act provides that following will be considered to be information suggesting that income has escaped assessment:

i. Information identified under the Board’s risk management strategy for the relevant year.

ii. Audit objections indicating the assessment was not done as per the Act.

iii. Information received under any agreements with the Government of any foreign country or specified territory as referred to section 159 of the Act.

iv. Information made available to Assessing Officer under any scheme notified under section 260 of the Act for the purposes of collection of information.

v. Information requiring action in consequence of a Tribunal or Court order.

vi. Information emanating from surveys conducted under section 253 (except subsection 4).

vii. Directions from the Approving Panel under section 274(6).

viii. Findings or directions contained in an order passed by any authority, Tribunal, or Court in proceedings under the Income Tax Act, 2025 or by a Court in any proceedings under any other law.

Q5.4 Can the AO make any assessment, reassessment or recomputation without issuing a notice to the assessee under section 280 of the new Act?

Ans. No, the AO shall not make any assessment, reassessment or recomputation under section 279 without issuing a notice under section 280 which is corresponding to section 148 of the Income Tax Act, 1961.

Q5.5 In which specific circumstances the Assessing Officer is not required to follow the procedure under section 281, before issuing a notice under section 280 of the new Act?

Ans. As per the provisions of the new Act, generally, the AO shall complete the procedure laid down in section 281 and he shall issue notice under section 280 along with the order under section 281(3). However, the AO shall skip the procedure laid down in section 281 in the cases where the AO has received:

i. information under the scheme for faceless collection of information as notified under section 260 of the new Act; or

ii. directions issued by the Approving Panel in respect of the declaration of the arrangement as an impermissible avoidance arrangement as per the provisions of Chapter XI, specifying the tax year or years to which such declaration of an arrangement as an impermissible avoidance arrangement shall apply, under section 274(6); or

iii. any finding or direction contained in an order passed by any authority, Tribunal or court in any proceeding under this Act by way of appeal, reference or revision, or by a Court in any proceeding under any other law.

When Can the AO Skip Section 281 Procedure? —

Exceptions to Standard Reopening Process

Q5.6 For which tax years will the reassessment provisions of the new Act apply?

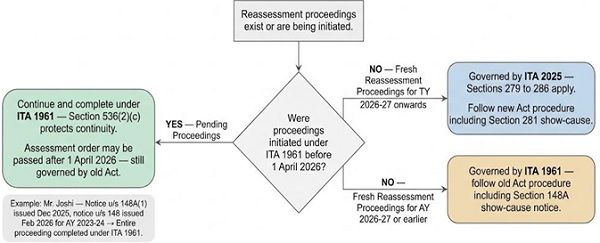

Ans. The reassessment provisions of the Income-tax Act, 2025 (Sections 279-286) will apply to Tax Year 2026-27 and subsequent tax years. For any tax year beginning before 1st April, 2026, only the old Act provisions will apply for reassessment.

Q5.7 What are the time limits under the old Act for issuing reassessment notices for earlier years?

Ans. Under Section 149 of the Income-tax Act, 1961 (as applicable after the amendment vide the Finance Act, 2025):

| Time Limit from end of AY | Condition | Monetary threshold |

| Issuing notice under Section 148A :

(as amended w.e.f. 01-09-2024) |

If the escaped assessment amounts to or likely to amounts to — | |

| (i) less than Rs. 50,00,000 | Within 3 years from end of relevant assessment year | |

| (ii) Rs. 50,00,000 or more

If the escaped assessment amounts to or likely to amounts to — |

Within 5 years from end of relevant assessment year |

|

| (i) less than Rs. 50,00,000 | Within 3 years and 3 months from end of relevant assessment year | |

| (ii) Rs. 50,00,000 or more | Within 5 years and 3 months from end of relevant assessment year |

Q5.8 What are the time limits for issuing reassessment notices under the Income Tax Act, 2025?

Ans. Section 282 of the Income-tax Act, 2025 prescribes the following time limits:

| Notice Type | General Time Limit | Extended Time Limit (if income escaping assessment ≥ Rs. 50 lakh) |

| Notice u/s 281 (show cause notice) | 4 years from end of Tax Year | 6 years from end of Tax Year |

| Notice u/s 280 (reassessment notice) | 4 years and 3 months from end of Tax Year | 6 years and 3 months from end of Tax Year |

Additionally, Section 282(3) provides that no notice under Section 280 or 281 shall be issued within one year from the end of any tax year.

Time Limits for Reassessment Notices — ITA 1961 vs. ITA 2025

| Notice Type | Condition | ITA 1961 — Section 149 Time Limit | ITA 2025 — Section 282 Time Limit |

| Show-cause / Pre-notice (148A / Section 281) | Escaped income ≤ ₹50 lakhs | Within 3 years from end of AY | Within 4 years from end of Tax Year |

| Show-cause / Pre-notice (148A / Section 281) | Escaped income > ₹50 lakhs | Within 5 years from end of AY | Within 6 years from end of Tax Year |

| Reassessment notice (Section 148 / Section 280) | Escaped income ≤ ₹50 lakhs | Within 3 years 3 months from end of AY | Within 4 years 3 months from end of Tax Year |

| Reassessment notice (Section 148 / Section 280) | Escaped income > ₹50 lakhs | Within 5 years 3 months from end of AY | Within 6 years 3 months from end of Tax Year |

Q5.9 What is the time limit for completion of reassessment under the Income Tax Act, 2025?

Ans. Section 286(1) [Table: SI. No. 4] provides that the reassessment order under Section 279 must be passed within one year from the end of the financial year in which the notice under Section 280 was served. Various extensions and exclusions are provided for specific situations (e.g., transfer pricing references, ITAT/court stay orders, etc).

B. TRANSITION – REASSESSMENT OF ASSESSMENT YEARS GOVERNED BY THE OLD ACT

Q5.10 If reassessment proceedings for an earlier assessment year were initiated under Section 147/148 of the old Act and are pending as on 01.04.2026, will they continue under the old Act?

Ans. Yes. Section 536(2)(c) of the Income-tax Act, 2025 expressly provides that the provisions of the repealed Act shall continue to apply to any proceeding pending on the date of commencement of the new Act. Therefore, reassessment proceedings already initiated under the old Act will continue to be governed by the provisions of the Income Tax act, 1961.

Example: The Assessing Officer issued a notice under Section 148A(1) of the old Act to Mr. X for AY 2023-24 in December 2025 and subsequently issued a notice under Section 148 in February 2026. The reassessment will be completed under the old Act, even though the assessment order may be passed after 01.04.2026.

Governing Act for Reassessment Proceedings — Pending vs. Fresh as on 1 April 2026

Q5.11 After 01.04.2026, can the Income-tax Department initiate fresh reassessment proceedings for earlier assessment years (such as AY 2022-23 or AY 2024-25) under the old Act?

Ans. Yes, even after 1 April 2026, proceedings such as assessment, reassessment, rectification, penalty, revision, etc. can still be initiated and completed under the old Act for earlier Assessment Years till A.Y.2026-27.

For example, in FY 2027-28, the department can reopen an assessment for AY 202324 under the old Act, if the conditions regarding reopening as prescribed in the Income Tax Act, 1961 are met.

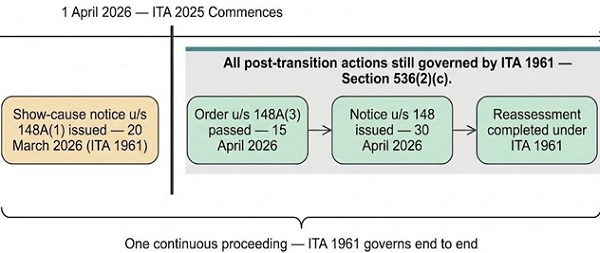

Q5.12 If a notice under Section 148A (1) of the old Act was issued before 01.04.2026, but the notice under Section 148 is yet to be issued, can it be issued after 01.04.2026?

Ans. Yes. Section 536(2)(c) of the Income-tax Act, 2025 expressly provides that the provisions of the repealed Act shall continue to apply to any proceeding pending on the date of commencement of the new Act. Since the proceedings were initiated under the Income-tax Act, 1961 through issuance of a notice under section 148A (1), the entire sequence of consequential actions — including the order under section 148A (3) and notice under section 148 — shall be governed by the provisions of the 1961 Act. However, such continuation is subject to compliance with the limitation period prescribed under section 149 of the Income Tax Act, 1961.

Example: The AO issued a show cause notice under Section 148A(1) to a taxpayer for AY 2022-23 on 20th March, 2026. After considering his response, the AO passes an order under Section 148A (3) on 15th April, 2026 and issues the notice under section 148 of the old Act on 30th April, 2026. All these actions are valid even though the new Act commences on 1st April, 2026.

Section 148A(1) Notice Issued Before 1 April 2026 — Entire Sequence Governed by ITA 1961

Q5.13 After the new Act comes into force on 01.04.2026, whose approval will be required to issue reassessment notices for AY 2026-27 or any earlier assessment year?

Ans. Since the assessment proceedings for AY 2026-27 or for any earlier assessment year are governed by the old Act, the approval hierarchy prescribed in Section 151 of the old Act will apply and therefore, Additional Commissioner, Additional Director, Joint Commissioner or Joint Director is the specified authority for the purposes of section 148 and 148A of the Income Tax Act, 1961.

Q5.14 If a reassessment notice under Section 148 of the old Act was issued for AY 2022-23 in February 2026, and the assessee has not yet furnished the return in response, can the return be filed after 01.04.2026?

Ans. Yes. Since the entire reassessment proceeding is governed by the old Act (as per Section 536(2)(c)), the assessee must furnish the return in response to the Section 148 notice under the old Act’s framework, within the time specified in the notice, not exceeding three months from the end of the month in which notice under section 148 is issued. The form in which ITR is to be filed will be corresponding to the Income Tax Act, 1961.

Q5.15 Can the Assessing Officer simultaneously conduct reassessment for AY 2024-25 (under the old Act) and assessment for Tax Year 2026-27 (under the new Act) for the same assessee?

Ans. Yes. These are independent proceedings under two different Acts for two different income periods. The Department can run parallel proceedings where necessary. The old Act will govern the reassessment proceedings for AY 2024-25 while the new Act will govern the assessment proceedings for TY 2026-27.

Q5.16 Which Act will govern the penalty proceedings relating to any tax year beginning before 1st April, 2026?

Ans. Section 536(2)(d) expressly provides that any proceeding for imposition of penalty for any tax year beginning before 1st April, 2026 may be initiated and the penalty imposed under the old Act, as if the new Act had not been enacted. Therefore, penalties arising from reassessment of earlier years will follow the framework for penalties as provided in the Income Tax Act, 1961.