Case Law Details

Sangeeta Sunil Kadoo Vs ITO (ITAT Nagpur)

The appeal was filed by the assessee against the order dated 21.02.2024 passed by the Commissioner of Income Tax (Appeals) / National Faceless Appeal Centre (NFAC), Delhi for Assessment Year 2013–14. The assessee challenged the reassessment proceedings initiated under section 148 and the additions made therein on several grounds.

The assessee contended that the reassessment proceedings were invalid as no opportunity of being heard was provided before issuing the notice under section 148, and the notice did not specify the reasons for reopening the assessment. It was further argued that the transactions relied upon by the Assessing Officer did not pertain to the relevant assessment year but related to Assessment Year 2012–13 (Financial Year 2011–12). The assessee also objected to the issuance of two separate notices under section 142(1) for the same assessment year, involving amounts of ₹10,00,000 and ₹40,95,000, which was alleged to be an afterthought to meet the monetary threshold for reopening.

Additional grounds raised included that the appellate order violated principles of natural justice by not allowing adequate opportunity to submit a complete response, as the order was passed based on a partial submission. The assessee also contended that the order required production of documents relating to transactions that did not occur in the relevant assessment year, ignored submissions already made, selectively relied on documents while overlooking key facts such as the agreement to sale, and repeated the findings of the original assessment without independent consideration. It was also alleged that the order reflected a predetermined approach and was passed in haste.

During the hearing before the Tribunal, the Authorised Representative (AR) referred to material in the paper book indicating that the investment of ₹10,00,000 was not attributable to Assessment Year 2013–14. The Tribunal accepted this position and held that the addition of ₹10,00,000 was liable to be deleted.

With respect to the addition of ₹40,95,000 relating to an alleged property transaction, the assessment was based on AIR information showing a transaction dated 27.08.2012 for the said amount. The Assessing Officer had issued notices under sections 142(1) and 144 requiring the assessee to furnish details of immovable and movable properties purchased, sold, or held during Financial Year 2012–13. The assessee responded that no immovable property had been purchased or sold during that year. A notice under section 133(6) was also issued to the Sub-Registrar, Nagpur, for verification, but the reply was still awaited at the time of assessment.

Before the Tribunal, the AR submitted that the actual sale deed reflected a transaction value of ₹35,00,000. It was further explained that ₹20,00,000 had been obtained as a loan from State Bank of India and the remaining ₹15,00,000 was sourced from past savings. This explanation was presented as reasonable. The Departmental Representative (DR) did not controvert the documentary evidence submitted by the assessee.

The Tribunal accepted the explanation and held that the basis for the addition of ₹40,95,000 had been successfully dislodged. Accordingly, the addition was deleted.

The AR submitted that the other technical grounds were not being pressed, as relief had already been obtained on merits.

In conclusion, the Tribunal partly allowed the appeal, granting relief to the assessee by deleting the additions of ₹10,00,000 and ₹40,95,000 on the basis of the evidence and explanations furnished.

FULL TEXT OF THE ORDER OF ITAT NAGPUR

This appeal by the assessee is directed against the order dated 21/02/2024, passed by the learned Commissioner of Income Tax (Appeals) / National Faceless Appeal Centre (NFAC), Delhi [for short, “Id. CIT(A)”] for the Assessment Year (A.Y.) 2013-14. The assessee has raised the following grounds of appeal:

“I. The initiation of reassessment proceedings u/s 148, entire process and its manner are inappropriate and bad in eyes of law. – Assessee was not given opportunity of being heard before order u/s 148 for reopening of assessment was passed. As also the order u/s 148, that was given to assessee, did not specifically mention the reasons for reopening of assessment.

II. The reassessment proceeding is bad in law, as the purported transactions do not pertain to the relevant assessment year – The transactions that are referred to and are assessed for AY 2013-14, do not pertain to that year. In fact they pertain to AY 2012-13 i.e. FY 2011-12.

III. The manner and Issues of 2 notices for the same assessment year is improper and shows predetermined mind set and therefore bad in eyes of law-One notice U/s 142 (1) was issued on 25.09-2020 which had a mention of transaction worth Rs. 10,00,000/- The assessee duly responded the same on 12.10.2020. Another Notice for another transaction of Rs.40,95,000/- was issued on 01.09.2021 (after response for all previous notices were filed by the assessee) This is nothing but afterthought and was done just to ensure that monetary limit of Rs. 50,00,000/- be justified for reopening assessment U/s 148, without getting time barred.

IV. The order by Hon’ble CIT(Appeal) is bad in the eyes of law as it defied the principle natural justice by denying appropriate opportunity to assessee for her submission Partial response was filed by the assessee vide ack no. 111444871130224 on 13.02.2024. Without waiting for further submission of the assessee, order was passed fully keeping aside principle of natural justice and depriving assessee of making final submission.

V. The order burdens assessee to provide non-existent documents- The order by CIT(Appeal) observes that assessee had not submitted documents regarding investments of Rs. 10,00,000/-in AY 2013-14. In fact such transaction never took place in that A.Y. Therefore asking those documents is like asking proof of an event which never took place.

VI. The order seeks to deny submission of documents made by the assessee – During the course of assessment proceedings, assessee had made submission about investment of Rs. 10,00,000/-made in the FY 2011-12. Further bank details of FY 2012-13 were also submitted. The order has denied the same.

VII. The order has placed selective reliance on the documents and deliberately ignored vital facts mentioned in the same documents, that the order is relied upon, that resulted in presentation twisted facts -Transaction of investment of Rs. 40.95 Lakh was assessed on the basis of sale deed The same document has a mention of agreement to sale which took place in F.Y. 2011-12. The order selectively ignored this important fact. The order is passed as if no details about registered agreement to sale are provided

VIII. The order seeks to repeat observations made in first assessment order without applying judicial neutral mind, by ignoring facts of the case and submissions made by assessee – Without going into facts of the case, appeal order has followed same mind-set, as are mentioned in original assessment order, by faulting assessee of not providing documents and information. This is despite the fact that most of the submissions of assessee are self-explanatory and prove that purported transaction do not pertain to AY 2013-14.

IX. The order is predetermine and passed in haste with specific intention to deny genuine relief to assessee -The order is passed without giving opportunity for submission to assessee, on the basis of “Partial Response”. It clearly shows predetermined intent of denying justice to assessee. “

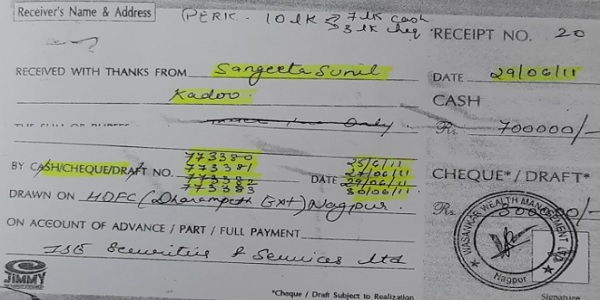

2. At the outset of hearing, the Id. Authorized Representative (AR) of the assessee invited our attention to page. 68 of the Paper Book which is reproduced below:

3. It is evident that investment was made in A.Y. 2013-14. Accordingly assessee is successful in deletion of investment of Z. 10,00,000/-.

4. As regards investment in property, it is pertinent that “during the course of assessment, it is noted that a AIR information having transaction code-06 purchase of property, transaction date of 27.08.2012 and transaction amount equal to Rs. 40,95,000/- is available on ITBA system. To furnish the details of such transaction, opportunities is given to the assessee vide notices issued u/s 142(1) and show-cause notice u/s 144 of the I.T. Act, 1961 and assessee is required to furnish details of immovable and movable properties purchased/sold/held by the assessee during the Financial Year 201213. In response, the assessee stated that she had not purchased/sold any immovable property during F.Y. 2012-13. In this regards, notice under section 133(6) of the I.T. Act, 1961 has been issued to SUB REGISTRAR NO 5/ NAGPUR CITY on 02.09.2021 for verification of information. Reply of the same is still awaiting.”

5. The Id. AR vehemently submitted that sale-deed executed is only of t. 35,00,000/-. He has also availed loan of t. 20,00,000/-from State Bank of India. The balance sum of t. 15,00,000/- can be ascribed to her past savings. The explanation is reasonable and may be accepted.

6. The Id. Sr. Departmental Representative (DR) failed to controvert the documentary evidence. Thus, assessee has successfully dislodged the basis of addition of Z. 40,95,000/-.

7. The Id. AR fairly submitted that he is not pressing other technical grounds. Since he has got relief on merits.

8. In the result, the appeal of assessee is partly allowed.

Order pronounced in the open Court on 23/02/2026

Author Bio