Month: March 2026

2,081 articlesCorporate Law

Corporate Law

Kerala HC Set Aside Building Permit Denial as Conversion Was Permitted

Goods and Services Tax

Goods and Services Tax

GST on Real Estate in India: Key Rates, Rules and Compliance Framework

Corporate Law

Corporate Law

SC Disappointed as High Courts Repeatedly Postpone Bail Pleas Affecting Personal Liberty

Corporate Law

Corporate Law

RTI Information Request on Insolvency Valuation Records Rejected by IBBI

Company Law

Company Law

ROC Imposes Penalty Because Company Failed to File Annual Return for FY 2022–23

Company Law

Company Law

ROC Imposes Penalty Because Company Failed to File Annual Return for FY 2021–22

Goods and Services Tax

Goods and Services Tax

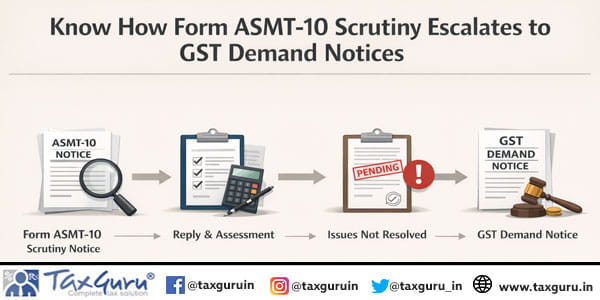

Know How Form ASMT-10 Scrutiny Escalates to GST Demand Notices

Corporate Law

Corporate Law

DRT Disallows Prepayment Charges After Loan Recall as Borrower Did Not Seek Early Repayment

Corporate Law

Corporate Law

Securitization Application Dismissed as Writ Petition Was Withdrawn Without Liberty

Income Tax

Income Tax