Month: March 2026

2,081 articlesCorporate Law

Corporate Law

Confirmation of Auction Sale Does Not Bar Judicial Scrutiny of Reserve Price: SC

Income Tax

Income Tax

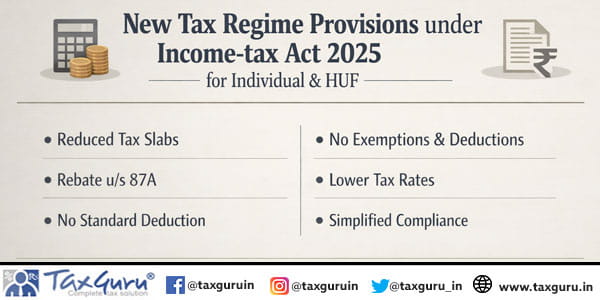

New Tax Regime Provisions under Income-tax Act 2025 for Individual & HUF

Income Tax

Income Tax

Section 264 Powers Are Wide and Meant to Correct Genuine Errors: Bombay HC

Fema / RBI

Fema / RBI

SAFEMA Tribunal Upholds CFO Liability in FEMA Case, Reduces Penalty

Fema / RBI

Fema / RBI

PMLA Tribunal: Share Investment Not ‘Proceeds of Crime’; Attachment Limited to Mining Profits

Fema / RBI

Fema / RBI

SAFEMA Tribunal: FERA Penalty Unsustainable Without Evidence in Hawala Case

Fema / RBI

Fema / RBI

SAFEMA Tribunal: Online Forex Trading Through Overseas Portal Violates FEMA; Penalty Reduced Considering Losses

Fema / RBI

Fema / RBI

PMLA Tribunal Upholds Freezing of Bank Accounts & FDR in Manesar Land Scam; Lien or Bank Guarantee No Bar

Fema / RBI

Fema / RBI

SAFEMA Tribunal Reduces FEMA Penalty For Unauthorized Handling of Foreign Currency

Fema / RBI

Fema / RBI