Month: March 2026

2,081 articlesCorporate Law

Corporate Law

CCI Invites Public Comments on Conduct Rules to Safeguard Confidential Competition Data

Income Tax

Income Tax

CBDT Grants Sec 35 Research Approval to G.S.L. Medical College & General Hospital

Income Tax

Income Tax

Budget 2026 Buyback Taxation: Capital Gains Treatment for Shareholders and Additional Tax for Promoters

Income Tax

Income Tax

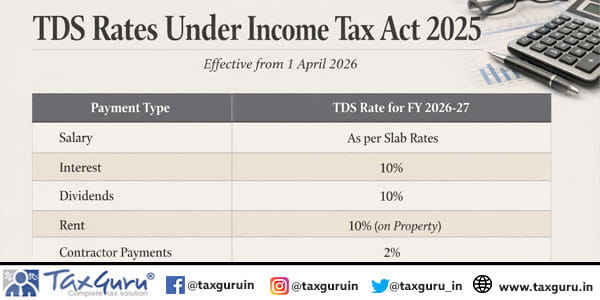

TDS Rates Under Income Tax Act 2025 from 1 April 2026

Fema / RBI

Fema / RBI

Borders, Beneficial Owners & 60-Day Promise: India’s Revised Land Border Framework

SEBI

SEBI

SEBI’s Proposed Overhaul of Nomination Norms in Securities Market

Income Tax

Income Tax

How India’s new Income Tax Act (2025) rewrites rules of assessment PART II

Income Tax

Income Tax

Reassessment Quashed as Capital Gains Taxable in Transferor Spouse’s Hands Under Clubbing Rules

Goods and Services Tax

Goods and Services Tax

AI-Hallucination – Lessons from Gujarat High Court’s Landmark Warning

Goods and Services Tax

Goods and Services Tax