#NAA

Log in to FollowEvery article filed under the “NAA” tag — analysis, news and updates.

454 articlesGoods and Services Tax

Goods and Services Tax

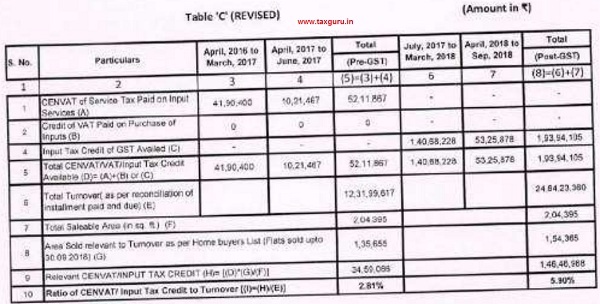

Builder Guilty of Profiteering as not passed ITC benefit to Flat Buyers

Goods and Services Tax

Goods and Services Tax

Builder guilty of profiteering as not passed additional ITC benefit to buyers

Goods and Services Tax

Goods and Services Tax

Builder profiteered by not passing ITC benefit to flat purchasers

Goods and Services Tax

Goods and Services Tax

Developer not passed additional ITC benefit to buyers post-GST implementation: NAA

Goods and Services Tax

Goods and Services Tax

Seller guilty of not passing ITC Benefit to Customers on Sanitary Napkin

Goods and Services Tax

Goods and Services Tax

Builder found Guilty of Not Passing Benefit of Pre-GST ITC

Goods and Services Tax

Goods and Services Tax

Gurugram Builder found guilty of not passing ITC Benefit to Flat Buyers

Goods and Services Tax

Goods and Services Tax

NAA found Builder guilty of not passing benefit of ITC to buyers of flats

Goods and Services Tax

Goods and Services Tax

No question of profiteering if no GST was charged: NAA

Goods and Services Tax

Goods and Services Tax