The Hon’ble Finance Minister Shri Arun Jaitley while presenting Union Budget for the year 2015-16 on 28th February, 2015 had introduced a new cess to be named as Swachh Bharat Cess to be levied and collected on taxable services. Unfortunately, the manner in which the legislation has been introduced, it has created mess out of cess and is prone to lots of litigations. If the government is serious about ease of doing business, then it must immediately issue clarification on various issues. The objective of this article is to identify various issues/queries relating to Swachh Bharat Cess (SBC) and try to clarify the same in simple language in FAQ format.

1. What is Swachh Bharat Cess (SBC)?

An enabling provision was incorporated in the Finance Act, 2015 vide Chapter VI to empower the Central Government to impose a Swachh Bharat Cess on ALL or ANY of the taxable services at a rate of 2% on the value of such taxable services. Section 119(2), which is the charging section of the Act, is reproduced below:-

“(2) There shall be levied and collected in accordance with the provisions ofthis Chapter, a cess to be calledthe Swachh Bharat Cess, AS SERVICE TAX on all or any ofthe taxable services at the rate oftwo per cent on the VALUE of such services for the purposes of financing and promoting Swachh Bharat initiatives or for any other purpose relating thereto.”

Thus, the objective of the levy is to finance and promote the Swachh Bharat initiatives of the Central Government, which is a dream project of Prime Minister Shri Narendra Modi. Undoubtedly, the objective of CLEAN INDIA is holy and pious and needs to be supported by every Indian. The cleanness is directly associated with hygiene and health of the residents and promotes international image of the nation.

2. Whether SBC is chargeable on import or manufacture of goods, like done earlier for Education Cesses?

No, SBC is not chargeable on goods. Unlike education cesses, the levy has been subjected only on taxable services. The rationale behind the differentiation between goods and services is not known, especially when dirt, pollution and environmental damages are mainly attributed to manufacturing activity, industrialization and relatively more directly related with goods than services. Hence, the levy is not based on principles of equality and the service sector has been discriminated and penalized for no fault of theirs. Yet, the parliament is constitutionally empowered to legislate and enforce the same.

3. What is the date of implementation of SBC?

The Central Government was empowered under sub-section (1) of Section 119 of the Finance Act, 2015 to appoint a date for the implementation of SBC. The Central Government has issued Notification No. 21/2015-ST dated 06-11-2015 to implement SBC from November 15, 2015. The reason for implementation during festive season and from the middle of the month is unknown especially when the government could have appointed the date anytime after 14th May, 2015 when the Act received the assent of the President of India.

4. Ok, so w.e.f. 15-11-2015, Swachh Bharat Cess @ 2% should be charged extra in the invoice?

As clearly evident from Section 119(2) as quoted above, the levy of SBC is @ 2% only. However, The Central Government has issued another Notification No. 22/2015-ST dated 06-11-2015 whereby it has exempted from payment of SBC calculated in excess of 0.50%. Therefore, the effective rate of SBC is 0.50% and not 2% due to exemption of 1.50% granted by the government.

5. A ‘Cess’ is a ‘tax on tax’. bo we need to calculate SBC @ 0.50% on the amount of service tax like we were earlier doing for calculating Education Cess and SHE Cess?

No, unlike surcharge, which is a ‘tax on tax’, every cess need not necessarily be a ‘tax on tax’. In the Indian context, the Hon’ble Supreme Court, in a ruling in Shinde Brothers Vs. Commissioner, Raichur reported in 1967, said that the word cess means a tax and is generally used when the levy is for some special administrative expense” citing various examples suggesting the name of the cess explains the object. Thus, cess is a tax which can be collected in any manner but to be utilized only for purposes specified at the time of levy.

The new provision, as quoted above at point 1, clearly says that the levy of SBC shall be @ 2% on the VALUE of such services. So, unlike education cesses, which were levied not on value of services but on service tax thereon, SBC is not a tax on service tax. Thus, SBC @ 0.50% should be calculated on the same value upon which service tax is calculated.

6. What would be the effective rate of service tax w.e.f. 15-11-15?

The effective rate of service tax, including SBC, w.e.f. 15-11-2015 would be 14.50%. However, for some services, where Valuation Rules or Abatement is applicable, the effective rate is less than 14.50% as tabulated at Point 11.

7. Whether SBC is levied on all or selected services?

The Central Government was empowered to impose the new levy on either all the taxable services or on few services. According to some media reports, it was expected that the government may impose SBC @ 2% only on few services which are contributing maximum share of service tax (like telecommunication services). However, the Central Government has not specified any particular service(s) which are chargeable to SBC. The taxable services, except below as notified vide Notification No. 22/2015-ST dated 06-11-2015 are leviable to SBC:

- Services covered under Negative List u/s 66b

- Services exempt from service tax under any notification issued u/s 93(1) of the Finance Act, 1994

In other words, the following types of services are not chargeable to SBC:-

- Services excluded from the definition of service as per Section 65B (44) like services provided by an employee to the employer, etc.

- Services provided or deemed to be provided outside the taxable territory. It means SBC is not chargeable even on services provided in the state of J&K as it is Non-Taxable Territory.

- Services exempted under Mega Exemption Notification No. 25/2012-ST.

- Services abated under Notification No. 26/2012-ST to the extent of abatement.

- Services exempted under Notification No. 33/2012-ST to the extent of threshold of Rs. 10

- Services provided to SEZ exempted under Notification No. 12/2013-ST

In simple words, if a person is liable to pay service tax, he becomes liable to pay SBC @ 0.50% on the same value upon which service tax is calculated @ 14%.

In view of the author, since the levy is on taxable service and services covered under negative list are anon-taxable service’, the above notification exempting negative list services is clarificatory in nature and even in the absence of such exemption, the levy was never on those services. One cannot exempt something which was never taxable.

8. What is the significance of the phrase all or any of the taxable service” used in the charging section 119(2)?

At the time of introduction and passage of the Act, the Central Government was not sure whether it should levy the tax on all taxable services or on few selective services. By use of the phrase, ‘all or any” the Central Government has enabled itself to keep any service outside the scope of charging section!! With due respect, the author is of the view that the words or any has been used unnecessarily in the charging section, as it leads to vagueness and uncertainty to the subject of the levy. The charging section should be clearly worded without any deficiency as regards the subject or person to be taxed. In the instant case, whether the legislation has levied SBC on all the services or on any particular services is unknown and unclear. The subject of the levy cannot be left open to be imposed at the option of the executive.

The Hon’ble Supreme Court in the case of A4athuram Agrawalv. State of A4adhya Pradesh [(1999) 8 SCC 667] observed: The statute should clearly and unambiguously convey the three components ofthe tax law ie. the subject ofthe tax, the person who is liable to pay the tax and the rate at which the tax is to be paid. If there is any ambiguity regarding any of these ingredients in a taxation statute then there is no tax in law. Then it is for the legislature to do the needfulin the matter.”

A taxing statute must be couched in express and unambiguous language. [Banarsi bebi v. .TTO – (1964) 7SCR 539].

The Act must be strictly construed in order to find out whether a liability is fastened on a particular subject. The subject is not to be taxed without clear words for that purpose; and every Act of Parliament must be read according to its natural construction of words. [A.P. Board far Water Pollution Control v. A.P. Rayons Ltd., (1989)1SCC 44; Re Nick-lethwait – (1855) HExch 452; Tennant v. Smith – (1892) AC 150; St. Aubyn v. A.5. -(1951) 2 All ER 473].

Words must say what they mean, nothing should be presumed or implied, they must say so. The true test must always be the language used. [6oodyear India Ltd. v. State ofHaryana – (1990) 2 SCC71].

If the intention of the government was to exempt from SBC any particular service or to exempt the services covered under mega exemption notification and other notifications issued u/s 93(1), as it has done vide N/N-22/2015-ST, the same objective could have been achieved even without the use of the words or any in the section 119(2) of the Finance Act, 2015. Section 119(5) has clearly empowered the government to use powers u/s 93 of Finance Act, 1994 to exempt any service from SBC.

9. Whether SBC needs to be charged separately in invoice, like education cesses?

NO!! Upon strict interpretation of law, there is no need to charge, collect, account or pay SBC independent of service tax. The entire tax can be charged and paid @ 14.50%. The plain reading of the charging section states that SBC shall be levied and collected as service tax. The bifurcation of service tax and SBC can be easily done at the end of the department. In fact, CBEC has not yet notified separate accounting code for SBC.

Having said that, to avoid unnecessary disputes, it is advisable to charge SBC separately after service tax as a different line item in invoice. It can be accounted and treated similarly to Education cesses. If distinct accounting code is not notified, it can be paid in the main code and if distinct accounting code is notified, it shall be paid in newly notified code.

10. Whether reverse charge is applicable on SBC?

Yes, if a person is liable to pay service tax under reverse charge, then SBC shall also be paid under reverse charge, because the levy is on taxable value and not on the person liable to pay service tax. In case of reverse charge u/s 68(2), the liability has been simply shifted from service provider to service receiver without any change in gross tax liability. Also, according to section 119(5) of the Finance Act, 2015, the provisions of Chapter V and the rules made thereunder are applicable to 5BC. Thus reverse charge created u/s 68(2) which is a provision under Chapter V is made applicable to 5BC. The service tax and 5BC shall be treated equally for all practical purposes as they are one and same. By use of the words, as service tax in the charging section itself, the legislation has made it abundantly clear that 5BC is nothing but service tax with the only difference that the proceeds shall be used only for Swachh Bharat initiatives.

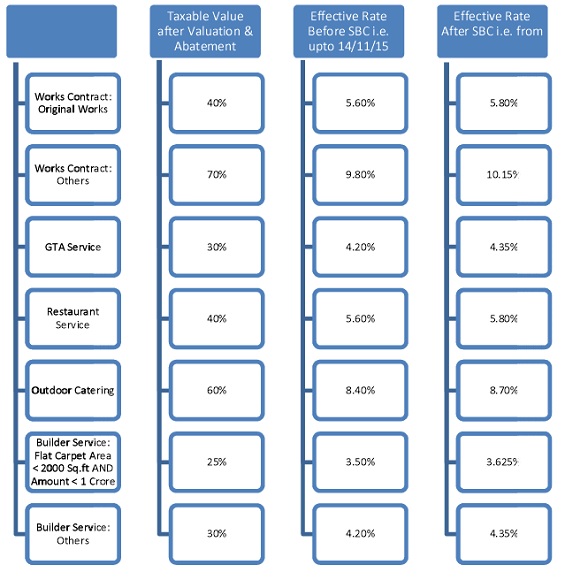

11. What is the effective rate of service tax on services subject to abatement or valuation rules?

12. The moot question is whether Cenvat Credit is available on SBC?

12. The moot question is whether Cenvat Credit is available on SBC?

Most of the subject experts are of the view that since SBC is not specifically covered under Rule 3 of Cenvat Credit Rule, 2004, cenvat credit is unavailable, unless Rule 3 is amended to this effect. With due respect, the author differs in opinion and is of the view that cenvat credit can be availed on SBC. However, unless the government clarifies the issue and allow cenvat credit, the same would be subject to litigation. The issue requires detailed analysis and may be taken up in subsequent write-up.

Author : Manoj Agarwal

Author : Manoj Agarwal

Address : Ganpati Campus, Lal Building Road, Rourkela – 769012

Contact : +91-9937041788

E:mail : ServiceTaxExpert@yahoo.com

Disclaimer: This article is the property of the author. No one shall publish, reproduce or use it in any manner, for any purposes, without the permission of the author. The author shall not be responsible or liable for anything done or omitted to be done on the basis of this article.

Author Bio

How to deal with sbc paid extra in previous month, like in earlier cases Rules 6(3) and Rule 6 (4) came in picture , but what in case of SBC paid in extra

Thank you for the very useful inputs on SBC. We had a simple query – in case we are receiving an amount(say Rs.100) from a client then the total amount including ST & SBC (14.5%) would be Rs. 114.5. Now out of this amount we allocate fees(assume Rs. 50)to one sub-consultant (who is part of the same project).So we have to pay them Rs. 50 + 7.25 (14.5%) = Rs.57.25.

So when we are paying our quarterly service tax, do we take ST exemption of Rs. 7.25 (14.5%) or only the service tax component without SBC- that is 14%?

I have a query.

Is swachh bharat cess applicable if services provided before 15-11-2015, bill raised before 15-11-2015 & payment released after 15-11-2015?

Is SBC is applicable in following case ?

Wok done and invoice raised before 15/11 but payment is released after 15/11.

Sir,

I’ve a question regarding SBC.

We are a Software Licenses Importer and in this case how to calculate SBC and pay to the department.

Also, if you can specify type of Account Head to create for SBC on Import of Services and accounting entry to be passed then it will be very helpful and this will help us in keeping our company in compliance to law.

Kindly note that this article was published here on 11th November, 2015 and subsequently on 12/11/15 the Central Govt. has issued Notification No. 23, 24 & 25 whereby most of the issues discussed in the article has been clarified in the same manner as mentioned by me and my views have been validated. Some issues are yet to be clarified by the CG.

Sir, we are service provider in respect of renting of immovable properties. We prepare rent invoice on 1st day of every month for the respective month & deposit the service tax raised in the invoice. Kindly clear me whether we will have to pay the .5% cess for the period 15/11 to 30/11. How should we deal the situation. Sanjay goyal

Whether SBC exemption is available to units in SEZ unlike service tax exemption? Please clarify.

Sir a very good article shared by you.

Nice article sir,

But , under which code we deposit this cess after collecting and how we shown this in return.

How Calculate SBC? Is it 0.50% on 14% or simply add 0.50 with 14%?

There is no clarity in this working becaue the Govt. is charging 0.50% SBC. Please give advice for calculation of SBC w.e.f 15/11/2015.

It may welcome litigation if Cenvat credit on SBC is taken unless notification is issued in this regard.

Very Good Article sir, Thanks for sharing.