CA Nitin Gupta

1. INTRODUCTION OF REVERSE CHARGE MECHANISM

1. INTRODUCTION OF REVERSE CHARGE MECHANISM

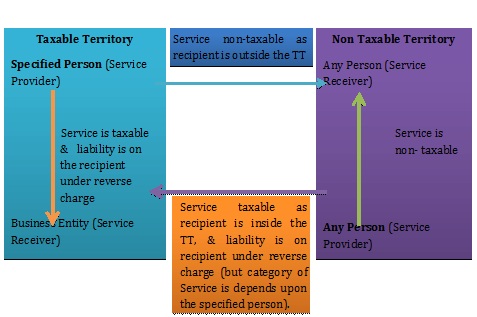

Reverse charge mechanism is not a new concept in service tax. Under the reverse charge mechanism, instead of service provider, the service receiver is liable to pay service tax. But with effect from 1.7.2012 a new scheme of taxation is being brought into effect whereby the liability of payment of service tax shall be both on the service provider and the service recipient. Usually such liability is affixed either on the service provider or the service recipient, but in specified services and in specified conditions, such liability shall be on both the service provider and the service recipient.

As per section 68 of Finance Act, 1994 (i.e. Payment of service tax)

(a) Direct charge

Every person providing taxable service to any person shall pay service tax.

(b) Full Reverse charge

Notwithstanding anything contained in sub-section (1), in respect of such taxable services as may be notified by the Central Government in the Official Gazette, the service tax thereon shall be paid by such person and in such manner as may be prescribed and all the provisions of this Chapter shall apply to such person as if he is the person liable for paying the service tax in relation to such service.

(c) Partial reverse charge

Provided that the CG may notifythe service and the extent of service tax which shall be payable by such person and the provisions of this Chapter shall apply to such person to the extent so specified and the remaining part of the service tax shall be paid by the service provider.

2. Notification No. 30/2012- ST dated 20/06/2012 notifies specified services on which provision of reverse charge is applicable.

(I) Full Reverse charge

3. Insurance Agents services

(a) Applicability of Reverse charge

In relation to service provided or agreed to be provided by an insurance agent to any person carrying on the insurance business, the recipient of the service.

Analysis

Insurance agents have been given relief from the service tax compliance to the extent of income receivable from person carrying on insurance business. However, service tax are required to be discharged by the agent as service provider on the income other than above, earned by such agent.

Rule 2 (cba) “insurance agent” has the meaning assigned to it in clause (10) of section 2 of the Insurance Act, 1938.

(b) Relevant Rule of Place of Provision of Service Rules,2012

As per rule 9 of said Rule (i.e.Place of provision of specified services): – The place of provision of following services shall be the location of the service provider:-

(a) __;

(b) __;

(c) Intermediary services;

(d) __.

Analysis

4. Goods Transport Agency

(a) Applicability of Reverse charge

in relation to service provided or agreed to be provided by a goods transport agency in respect of transportation of goods by road, where the person liable to pay freight is,—

(I) any factory registered under or governed by the Factories Act, 1948 (63 of 1948);

(II) any society registered under the Societies Registration Act, 1860 (21 of 1860) or under any other law for the time being in force in any part of India;

(III) any co-operative society established by or under any law;

(IV) any dealer of excisable goods, who is registered under the Central Excise Act, 1944 (1 of 1944) or the rules made thereunder;

(V) anybody corporate established, by or under any law; or

(VI) any partnership firm whether registered or not under any law including association of persons;

Any person who pays or is liable to pay freight either himself or through his agent for the transportation of such goods by road in a goods carriage:

Provided that when such person is located in a non-taxable territory, the provider of such service shall be liable to pay service tax.

Analysis

- Goods Transport Agency means any commercial concernwhich provides service in relation to transport of goodsby road and issues consignment note, by whatever name called.

- Taxable service means, any service provided to a customer,by a Goods Transport Agency, in relation to transport of Goods by road in a goods carriage.

- Goods carriage means any motor vehicle constructed or Adapted for use solely for the carriage of goods, or any motor vehicle not so constructed or adapted, when used for the carriage of goods.

- Rule2 (bc) “body corporate” has the meaning assigned to it in clause (7) of section 2 of the Companies Act, 1956.

- Rule2 (cd) “Partnership Firm” Includes A Limited Liability Partnership.

(b) Relevant Rule of Place of Provision of Service Rules,2012

As Per Rule 10 of said Rule (i.e. Place of provision of goods transportation services)

The place of provision of services of transportation of goods, other than by way of mail or courier, shall be the place of destination of the goods.

Provided that the place of provision of services of goods transportation agency shall be the location of the person liable to pay tax.

Analysis

5. Sponsorship Services

(a) Applicability of Reverse charge

In relation to service provided or agreed to be provided by way of sponsorship to anybody corporate or partnership firm located in the taxable territory, the recipient of such service.

Analysis

Rule 2 (bc) “body corporate” has the meaning assigned to it in clause (7) of section 2 of the Companies Act, 1956.

Rule 2 (cd) “Partnership Firm” Includes A Limited Liability Partnership.

(b) Relevant Rule of Place of Provision of Service Rules,2012

In this service place of provision of service is depends upon the following situation:-

(i) Where “Sponsor” and “Service receiver” is situated in taxable-territory.

As per Rule 8 of Place of Provision of Service Rules, 2012

(Place of provision of services where provider and recipient are located in taxable territory).-

Place of provision of a service, where the location of the provider of service as well as that of the recipient of service is in the taxable territory, shall be the location of the recipient of service.

(ii) Where any one is (i.e. either “Sponsor” or “Service receiver”) is situated in non-taxable territory and event is held only one place.

As per Rule 6 of Place of Provision of Service Rules, 2012

(Place of provision of services relating to events).-

The place of provision of services provided by way of admission to, or organization of, a cultural, artistic, sporting, scientific, educational, or entertainment event, or a celebration, conference, fair, exhibition, or similar events, and of services ancillary to such admission, shall be the place where the event is actually held.

(iii) Where any one is (i.e. either “organizer” or “Service receiver”) is situated in non-taxable territory and event is held more than one place.

As per Rule 7 of Place of Provision of Service Rules, 2012

(Place of provision of services provided at more than one location).-

Where any service referred to in rules 4, 5, or 6 is provided at more than one location, including a location in the taxable territory, its place of provision shall be the location in the taxable territory where the greatest proportion of the service is provided.

Analysis

6. Legal Services

(a) Applicability of Reverse charge

In relation to service provided or agreed to be provided by,-

(I) an arbitral tribunal, or

(II) an individual advocate or a firm of advocates by way of legal services,

To any business entity located in the taxable territory, the recipient of such service.

Analysis

Rule 2(cca) “Legal Service” means any service provided in relation to advice, consultancy or assistance in any branch of law, in any manner and includes representational services before any court, tribunal or authority.

Sec 65B(17) “Business Entity” means any person ordinarily carrying out any activity relating to industry, commerce or any other business or profession.

(b) Also, I would like to discuss mega exemption, entry no. 6

Services provided by-

(a) an arbitral tribunal to –

(i) any person other than a business entity; or

(ii) a business entity with a turnover up to rupees ten lakh in the preceding financial year;

(b) an individual as an advocate or a partnership firm of advocates by wayof legal services to,-

(i) an advocate or partnership firm of advocates providing legal services;

(ii) any person other than a business entity; or

(iii) a business entity with a turnover up to rupees ten lakh in thepreceding financial year; or

(c) a person represented on an arbitral tribunal to an arbitral tribunal;

Analysis

(c) Relevant Rule of Place of Provision of Service Rules,2012

In this service place of provision of service is depends upon the following situation:-

(i) Where both “Service Provider” and “Service receiver” is situated in taxable-territory.

As per Rule 8 of Place of Provision of Service Rules, 2012

(Place of provision of services where provider and recipient are located in taxable territory).-

Place of provision of a service, where the location of the provider of service as well as that of the recipient of service is in the taxable territory, shall be the location of the recipient of service.

(ii) Where anyone (i.e. “Service Provider” or “Service receiver”) is situated in Non-taxable territory.

RULE 3- GENERAL RULE- LOCATION OF SERVICE RECEIVER

This is a default rule which provides that the place of provision of service shall be deemed to be the place of location of service receiver. However, this rule is applicable only when none of other rule applies.

Analysis

7. Government Service

(A) Applicability of Reverse charge

In relation to support services provided or agreed to be provided by Government or local authority except,-

(a) renting of immovable property, and

(b) services specified sub-clauses (i), (ii) and (iii) of clause (a) of section 66D of the Finance Act,1994,

To any business entity located in the taxable territory, the recipient of such service.

Analysis

Sec 65B(17) “Business Entity” means any person ordinarily carrying out any activity relating to industry, commerce or any other business or profession.

(B) Relevant Rule of Place of Provision of Service Rules,2012

Place of Provision of Service Rules, 2012 is depends upon type of services therefore in that case service is not specified i.e. (which type of support service is provided by govt. to business entity) so that Specifically Rules cannot be determined for such services.

8. Director Service

(A) Applicability of Reverse charge

In relation to service provided or agreed to be provided by a director of acompany to the said company, the recipient of such service.

Analysis

- All payments against services including part time directors’ remuneration, directors’ sitting fees, commission etc. receivable from company to the director have been subjected to service tax.

- Service tax is not applicable where employer and employee relationship is existing therefore any sum paid to whole time directors is not liable to service tax.

- This service is applicable on 7th August 2012 under the reverse charge mechanism. (Notification no.45/2012-ST dated 7/8/2012).

(B) Relevant Rule of Place of Provision of Service Rules,2012

In this service place of provision of service is depends upon the following situation:-

(i) Where both “Service Provider” and “Service receiver” is situated in taxable-territory.

As per Rule 8 of Place of Provision of Service Rules, 2012

(Place of provision of services where provider and recipient are located in taxable territory).-

Place of provision of a service, where the location of the provider of service as well as that of the recipient of service is in the taxable territory, shall be the location of the recipient of service.

(ii) Where anyone (i.e. “Service Provider” or “Service receiver”) is situated in Non-taxable territory.

RULE 3- GENERAL RULE- LOCATION OF SERVICE RECEIVER

This is a default rule which provides that the place of provision of service shall be deemed to be the place of location of service receiver. However, this rule is applicable only when none of other rule applies.

Although as per above Rules, Taxability of service is cannot change (i.e. “Taxable or Non-taxable service” decision is cannot change if follow any of said rule due to reason, taxability of service is depends upon the Location of Service Receiver as per both the said rules.)

Analysis

9. Import of Service

9. Import of Service

(A) Applicability of Reverse charge

In relation to any taxable service provided or agreed to be provided byany person which is located in a non-taxable territory and received by anyperson located in the taxable territory, the recipient of such service.

Analysis

(B) Relevant Rule of Place of Provision of Service Rules,2012

Place of Provision of Service Rules, 2012 is depends upon type of services therefore in that case service is not specified which type of services are provided by service provider to Service receiver so that Specifically Rules cannot be determined for such services.

10. Summary of applicability of Full Reverse Charge

| S.No. | IN RELATION TO SERVICEPROVIDED OR AGREED TOBE PROVIDED BY | SERVICE RECEIVER | PERSON LIABLE TO PAYSERVICE TAX |

| 1. | an Insurance Agent | to any Person Carrying On The InsuranceBusiness | the Recipient Of TheService |

| 2. | a Goods Transport Agencyin respect of transportationof goods by road | where the PERSON LIABLE TO PAYFREIGHT IS,—(a)A factory;(b)Company;(c)Corporation;

(d)Society; (e)Co-operative society; (f)Registered dealer of excisable goods; (g)Body corporate; or (h)Registered partnership firm |

any person Who PaysOr Is Liable To PayFreight either himself orthrough his agent forthe transportation of such goods by road in a goods carriage :

NOTE- when such person is located in a non-taxable territory, the provider of such service shall be liable to pay service tax. |

| 3. | by way of Sponsorship | to any Body Corporate Or PartnershipFirm located in the taxable territory, | the Recipient of suchservice; |

| 4. | (I) an Arbitral Tribunal, or(II) an Individual Advocateor a Firm Of Advocates byway of LEGAL SERVICES | to any Business Entity located In TheTaxable Territory, | the Recipient of suchservice; |

| 5. | Government or localauthority BY way of supportservices EXCEPT,-(a) Renting of immovableproperty, and

(b) services specified subclauses (i), (ii) and (iii) of clause (a) of section 66D of the Finance Act, 1994, |

to any Business Entity located In TheTaxable Territory, | the Recipient of suchservice; |

| 6. | a Director of a company | to the said Company, | the Recipient of suchservice; |

| 7. | any person which islocated in a non-taxableterritory | any Person Located In The TaxableTerritory, | the Recipient of suchservice; |

(II) Partial Reverse charge

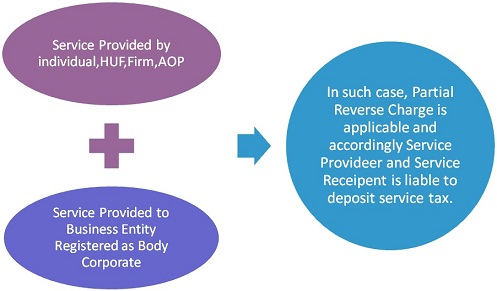

1. Manpower Supply Service

(A) Applicability of Reverse charge

In relation to services provided or agreed to be provided by way of supply of manpower for any purpose or security services by any individual, Hindu Undivided Family or partnership firm, whether registered or not, including association of persons, located in the taxable territory to a business entity registered as a body corporate, located in the taxable territory, both the service provider and the service recipient to the extent notified under sub-section (2) of section 68 of the Act.

Analysis

- “Supply of manpower” means supply of manpower, temporarily or otherwise, to another person to work under his superintendence or control.

- Security Service, cleaning service, piece basis or job basis contract can be ‘manpower supply service’ only if the labour work under superintendence or control of Principal Employer.

(B) Percentage to be deposit

75% of ST shall be paid by service receiver, if service provider is an individual, HUF, proprietary or partnership firm or AOP. Balance 25% of ST shall be paid by service provider.

(C) Relevant Rule of Place of Provision of Service Rules,2012

Place of Provision of Service in case of Manpower or security Service except Personal Security Service.

In this service place of provision of service is depends upon the following situation:-

(i) Where both “Service Provider” and “Service receiver” is situated in taxable-territory.

As per Rule 8 of Place of Provision of Service Rules, 2012

(Place of provision of services where provider and recipient are located in taxable territory).-

Place of provision of a service, where the location of the provider of service as well as that of the recipient of service is in the taxable territory, shall be the location of the recipient of service.

(ii) Where anyone (i.e. “Service Provider” or “Service receiver”) is situated in Non-taxable territory.

RULE 3- GENERAL RULE- LOCATION OF SERVICE RECEIVER

This is a default rule which provides that the place of provision of service shall be deemed to be the place of location of service receiver. However, this rule is applicable only when none of other rule applies.

Although as per above Rules, Taxability of service is cannot change (i.e. “Taxable or Non-taxable service” decision is cannot change if follow any of said rule due to reason, taxability of service is depends upon the Location of Service Receiver as per both the said rules.)

Analysis

12. Rent-a-cab Service

(A) Applicability of Reverse charge

In relation to services provided or agreed to be provided by way of renting of a motor vehicle designed to carry passengers, to any person who is not engaged in a similar business by any individual, Hindu Undivided Family or partnership firm, whether registered or not, including association of persons, located in the taxable territory to a business entity registered as a body corporate, located in the taxable territory, both the service provider and the service recipient to the extent notified under sub-section (2) of section 68 of the Act.

Analysis

(B)Percentage to be deposit

(C) Relevant Rule of Place of Provision of Service Rules,2012

CASE 1- Place of Provision of Service in case of “Rent-a-cab Service”upto a period of one month

As per rule 9 of said Rule (i.e.Place of provision of specified services): – The place of provision of following services shall be the location of the service provider:-

(a) __;

(b) __;

(c) __;

(d) Service consisting of hiring of means of transport, upto a period of one month.

CASE 2- Place of Provision of Service in case of “Rent-a-cab Service” more than period of one month

In this service place of provision of service is depends upon the following situation:

- Where both “Service Provider” and “Service receiver” is situated in taxable-territory.

As per Rule 8 of Place of Provision of Service Rules, 2012

(Place of provision of services where provider and recipient are located in taxable territory).-

Place of provision of a service, where the location of the provider of service as well as that of the recipient of service is in the taxable territory, shall be the location of the recipient of service.

- Where anyone (i.e. “Service Provider” or “Service receiver”) is situated in Non-taxable territory.

RULE 3- GENERAL RULE- LOCATION OF SERVICE RECEIVER

This is a default rule which provides that the place of provision of service shall be deemed to be the place of location of service receiver. However, this rule is applicable only when none of other rule applies.

13. Work Contract Service

(A) Applicability of Reverse charge

In relation to services provided or agreed to be provided by way service portion in execution of a works contract by any individual, Hindu Undivided Family or partnership firm, whether registered or not, including association of persons, located in the taxable territory to a business entity registered as a body corporate, located in the taxable territory, both the service provider and the service recipient to the extent notified under sub-section (2) of section 68 of the Act.

Analysis

(B)Percentage to be deposit

(C) Relevant Rule of Place of Provision of Service Rules,2012

In this service place of provision of service is depends upon the following situation:

- Where both “Service Provider” and “Service receiver” is situated in taxable-territory.

As per Rule 8 of Place of Provision of Service Rules, 2012

(Place of provision of services where provider and recipient are located in taxable territory).-

Place of provision of a service, where the location of the provider of service as well as that of the recipient of service is in the taxable territory, shall be the location of the recipient of service.

- Where anyone (i.e. “Service Provider” or “Service receiver”) is situated in Non-taxable territory.

As per Rule 4 of Place of Provision of Service Rules, 2012

(Place of provision of performance based services).-

The place of provision of following services shall be the location where the services are actually performed, namely:-

(a) services provided in respect of goods that are required to be made physically available by the recipient of service to the provider of service,or to a person acting on behalf of the provider of service, in order to provide the service:Provided that when such services are provided from a remote location byway of electronic means the place of provision shall be the location where goods are situated at the time of provision of service:

Provided further that this sub-rule shall not apply in the case of a service provided in respect of goods that are temporarily imported into India for repairs, reconditioning or re engineering for re-export, subject to conditions as may be specified in this regard.

(b) ___.

Analysis

14. Summary of applicability of Partial Reverse Charge

| S.No. | IN RELATION TO SERVICE PROVIDED OR AGREED TO BE PROVIDED BY | SERVICE RECEIVER AND SERVICE PROVIDER | % OF SERVICE TAX PAYABLE BY SERVICE PROVIDER | % OF SERVICE TAX PAYABLE BY SERVICE RECEIVER |

|

1. |

RENTING OF A MOTOR VEHICLE DESIGNEDTO CARRY PASSENGERS TO ANY PERSON WHO IS NOT ENGAGED IN A SIMILAR BUSINESS | Service Provider

Service Receiver

|

||

| Service tax paid ON ABATED VALUE |

NIL |

100% |

||

| Service tax paid ON NON-ABATEDVALUE |

60% |

40% |

||

|

2. |

SUPPLY OF MANPOWER FOR ANY PURPOSE OR SECURITY SERVICES |

25% |

75% |

|

|

3. |

SERVICE PORTION IN EXECUTION OF AWORKS CONTRACT |

50% |

50% |

15. Common Points for all of the services under Reverse Charge

I. Invoice compliance

The service provider shall issue an invoice complying with Rule 4A of the Service Tax Rules 1994. Thus the invoice shall indicate the name, address and the registration number of the service provider; the name and address of the person receiving taxable service; the description and value of taxable service provided or agreed to be provided; and the service tax payable thereon. As per clause (iv) of sub-rule (1) of the said rule 4A “the service tax payable thereon’ has to be indicated. The service tax payable would include service tax payable by the service provider only.

II. CENVAT Credit utilization

CENVAT Credit balance cannot be utilized by service receiver for discharging service tax liability under reverse charge.

III. CENVAT Credit Taken

IV. Whether SSI Exemption is applicable to Service Receiver or not

Notification No. 33/2012-ST which provides that whereby the Central Government, being satisfied that it is necessary in the public interest so to do, hereby exempts taxable services of aggregate value not exceeding ten lakh rupees in any financial year from the whole of the service tax leviable thereon under section 66B of the said Finance Act:

Provided that nothing contained in this notification shall apply to,-

- taxable services provided by a person under a brand name or trade name, whether registered or not, of another person; or

- Such value of taxable services in respect of which service tax shall be paid by such person and in such manner as specified under sub-section (2) of section 68 of the said Finance Act read with Service Tax Rules, 1994.

V. Point of Taxation Rule under Reverse Charge

For Payment made of Service Tax under Reverse Charge

Can service receiver avail CENVAT credit on tax paid under reverse charge mechanism?

What are the consequences on non/short collection on service provider and service receiver(under reverse charge mechanism)?

Sir,

What are consequences of non-collection/short collection of service tax and what are the consequences faced by service receiver if service provider has applied percentage wrongly(i.e.,has collected the portion for which receiver is liable to pay)?

and can service receiver can avail CENVAT credit on tax paid under reverse charge mechanism?

Dear all

In case of hiring of motor vehicle if service provider has not mentioned SERVICE Tax payable by him in Invoice or he is not registered under Service tax then whether service tsx is payable by recipient of service under reverse charge mechanism

This analysisi is just excellent

Vert good not able to study at one go and unable to save with pops which are not coming when we copy them

Very good presentation. It is very useful to all.

Dear Sir,

Very good presentation with diagram.

Thanks

Dear Sir

The way of explain is very good.

Thanks

B S. NEGI

Dear, Very well explained article. Good Job. Thanks.

Dear Sir,

Good Article.

Thanks.

Anesh Patil

This comment does not refer to the step missed by the authour.

I HAVE A PERTINENT COMMENT TO MAKE & WHICH AUTHORITY will answer it?

1% deduction OK, as a seller WHEN WILL I GET back my 1%?

What about the interest lost on my 1%? Who will compensate me?

WHAT about my LTCG parameters where i fall short of 1%?

What is the position of joint purchaser & jt. seller? [individuals under 50L]

Has it being defined as COMPOSITE limit? Is it not arbitrary?

What is the position to ANSWER THE ONLINE FORM [26QB] of jt parties?

In which manner 16B will be issued? i’m not talking of composite aspects.

Will not banks financing be covered as purchaser? Even if they merely discharge purchase obligation, the purchase cum borrower will have to deduct 1%! Right.

THE BANK IS FINANCING THAT 1% to be put in the Govt treasury while the borrower will pay interest on it!

Many issues are their with this idiotic aspect ‘UNDER THE GUISE TO CURB’, undervaluation & cash transactions. DISTRESS PROPERTY SALE overlooked & valuation invoked. Thereby both the buyer & seller are in a fix!?

I’m going to put it up in various professional forums to enforce that the ‘SELLER IS SHORT CHANGED’ under the guise of the 1% taxation.

The views will be appreciated by me, if any, vinay.joshi3@gmail.com

Regards,

Will you please re-submit the article as an attachment so that some of the illustrations that are not visible may be made clearly visible. A very useful article could not be fully understood as some of the illustrations are simply presented,for example, as POPS 13, POPS 17, POPS 20 in a small box.

Thank you

padmanabhan_prakash@yahoo.com

Very good & detailed article

Dear Sir

An excelent and very useful Article. Thank yo very much.

With Regards

e n ananthanarayanan

Excellent presentation: