1. INTRODUCTION

There has been so much euphoria with regard to Indian E-commerce story and is on track to become the world’s fastest growing e-commerce market. This growth story is being driven by robust investment activity by VCs, Angels and the rapid increase in internet users. Internet users in India have gone up from 50 million in 2007 to 300 million in 2014. As per Morgan Stanley, size of the Indian internet market is expected to rise from $11 billion in 2013 to $137 billion by 2020 and market capitalization of these internet businesses could touch $160-200 billion from the $4 billion at present.

Let’s understand various e-commerce models from the indirect Tax perspective:-

Let’s understand various e-commerce models from the indirect Tax perspective:-

I) SUPPLY OF GOODS

E-commerce Platforms have entered into Memorandum of Understanding with seller to promote the business of seller. This type of business has several models and service tax to be levied accordingly. Following models have been explained herein.

A) Direct Supply from Seller to Customer

Seller have own website for soliciting their business and not relying on online aggregators like Flipkart, Amazon, Snapdeal for listing of goods. In this case, VAT shall be charged by seller in case of intrastate transaction and CST in case of inter-state movement of goods.

EXAMPLE

Mr Karan orders a Service book from the Website poojalawhouse.com. Online website shall be maintained by the seller Pooja law House. The invoice of the Book would generate by the Pooja Law which shall levy VAT on the product sold which will look something like this:

II) Supply from Seller to Customer via online Intermediary/Aggregators

II) Supply from Seller to Customer via online Intermediary/Aggregators

Products of sellers are listed on websites like Flipkart, Amazon, Snapdeal who have entered into MOU with ecommerce Platforms. These orders are in turn given to the Seller for delivery of the goods. Seller shall make the invoice and deliever the same to customer directly. Invoice shall contain name of the company/firm, Reg. Address, TIN/CST no. etc. In present case only, Interface is being provided by the online portal.

Example:

Mr Gaurav Agarwal orders iPhone 4s from the Online Website Snapdeal.com. Snapdeal will book order on the behalf of the Seller named WS Retailer. So, Snapdeal will contact with the WS Retailer to deliver the goods to the customer. The seller shall levy VAT on the goods sold by seller which shall look something like this:

Now these online portals Flipkart, Snapdeal etc. shall generate an invoice of such services like Booking, Commission, Courier, Shipping charges etc. in the name of Seller, as these charges are covered under the definition of taxable services as per the provisions of Finance Act, 1994. In continuation of above example, Snapdeal will generate an invoice and service tax to be charged which will look something like this:

Now these online portals Flipkart, Snapdeal etc. shall generate an invoice of such services like Booking, Commission, Courier, Shipping charges etc. in the name of Seller, as these charges are covered under the definition of taxable services as per the provisions of Finance Act, 1994. In continuation of above example, Snapdeal will generate an invoice and service tax to be charged which will look something like this:

Bill to be charged shall vary according to terms and conditions contained in Memorandum of Understanding with sellers. For example- If the goods are delivered by e-commerce platform to customer then shipping charges shall be charged by platform in the bill. Shipping charges shall also be charged in bill and liable to service tax.

Bill to be charged shall vary according to terms and conditions contained in Memorandum of Understanding with sellers. For example- If the goods are delivered by e-commerce platform to customer then shipping charges shall be charged by platform in the bill. Shipping charges shall also be charged in bill and liable to service tax.

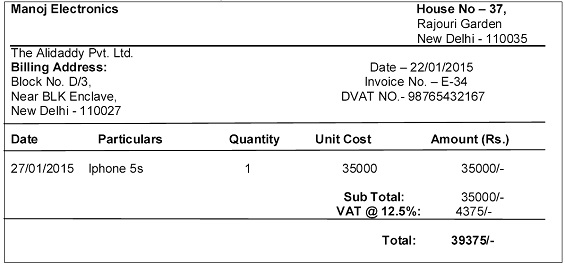

III) Seller to Online Portals to Customer

In this case , seller shall sell goods to e-commerce platform who in turn sells to final customer. Role of e-commerce site shall not be limited to provide interface but becomes the owner of the goods.

For Example:

Mr Sushant Kapil orders iPhone 5s from the Online Website www.alidaddy.com. This site will book order on the behalf of the seller and purchase the goods from Manoj Electronics to deliver the goods to Customers. The invoice of iPhone 5s would be generated by the Manoj Electronics including TIN No. and address to the Website. Now, this site will issue an invoice to Customer.

This site will generate an additional invoice of such services like Booking, Commission, Courier, Shipping charges etc. in the name of Seller XYZ Enterprises which will be exactly the same as discussed in Model 2.

This site will generate an additional invoice of such services like Booking, Commission, Courier, Shipping charges etc. in the name of Seller XYZ Enterprises which will be exactly the same as discussed in Model 2.

2. RENDERING OF SERVICES

Let’s first define service as per Service Tax

Section 65B(44) of ST Act ‘Service’ means any activity carried out by a person for another for consideration, and includes a declared service, but shall not include –

(a) An activity which constitutes merely,––

(i) A transfer of title in goods or immovable property, by way of sale, gift or in any other manner; or

(ii) A transaction in money or actionable claim

Many E-portals websites are in existence to promote the business of rendering services on behalf of service provider. Various Service model are mentioned below:-

A) Service rendered by Online Portals ( like Makemytrip, Expedia etc) to the Service Recipient

If the service provider is providing service to the customer with help of intermediary (Online Aggregator),in that case service tax shall be levied on the bill raised by Service Provider to the customer. Online Aggregator /intermediary shall raise bill towards service provider and service tax to be levied on same.

For Example- Online service providers (like makemytrip, booking.com) provide the relevant information on destinations, hotels and Airports. They have entered into MOU with hotels and airlines. Invoice is raised by the Service provider (hotel) on the customers. Makemytrip acting as online aggregator raises invoices towards hotel. Service Tax shall be levied on the amount of bill issued by online aggregator.

B) Direct rendering of Service from Service Provider to Service Receiver

If the service provider is rendering the online services, then service provider shall be liable to charge service tax from the customer. For example – Online Repairing of computer being provided by the company then it shall be liable to charge Service tax from the customer.

C) Service being provided from Customer to Customer

In case of customer to customer transactions, website does not sell anything but provides a platform for the customers for doing sale and purchase .In turn charges for the commission for the service provided and same shall be liable to service tax . No chargeability of Sales Tax in such transactions.

D) Crowdfunding Websites

Crowdfunding is the practice of funding a project or venture by raising monetary contributions from a large number of people, typically via the internet. These have been becoming very popular of late. People have been able to raise large capital for their venture. These platforms like pikaventure.com, Indiegogo.com and many others are helping entrepreneurs to raise capital for their project. In turn charge minimum fees for raising such amount if target funding is achieved. Amount of fee to be charged shall be liable for service tax.

Issues

The current dispute has arisen in case of e-commerce companies that undertake storage of goods procured from various sellers in their warehouse before dispatching them to the respective buyers. It appears that Karnataka VAT authorities are of the view that in such cases, the e-commerce companies are involved in supplying and distribution of goods and, therefore, would qualify as ‘dealers’.. The authorities are also of the view that these companies act as commission agents or consignment agents of sellers. Therefore, these companies are covered under the definition of ‘dealers’ and, therefore, are liable to discharge VAT. “The Karnataka Government plans to amend the Value Added Tax Act and bring transactions from e-commerce marketplaces under its ambit, reports The Times of India. The government says the amendment will deal with transactions on e-commerce sites that follow the marketplace model like Flipkart, Amazon India and Snapdeal and it is expected to be passed during the upcoming winter session of the state legislature. This action by one state government will change the whole scenario, wherein this industry would be greatly demotivated. Also the position of service tax law would need to be re-assessed after this.

Even though it has been decided issue that levy of tax would arise on occurrence of a taxable event. In the case of levy of VAT, the taxable event is sale or purchase of goods. In the case of e-commerce transactions, the companies are not involved in sale of goods at all. The primary object of the companies is to offer online portals where the buyer and the seller meet and the buyer places an order for goods advertised on the portal. The invoice is raised by the seller on the buyer. No invoice whatsoever is issued by the e-commerce company on the buyer in respect of sale of goods. Clearly, e-commerce companies are service providers.

Conclusion

There has been clarity with regards to levy of indirect taxes on ecommerce transactions. Government of the day needs to incentives this sector and assist to make it competitive keeping in view their vision of “MADE IN INDIA CAMPAIGN” rather than burden with taxes.

Author Bio

Sir ,Please solve my problem.

I am a seller on snapdeal,amazon and shopclues,started just 4 months ago on feb 2017.

Sir I want to know what are the taxes that i have to fill?what is tds?If i have to file tds return?

If i have to file ITR and GSTR?

Dear Sir

i Have a Question Pls Clarify ?

Example

I am selling products my own website

for example

i sold one electric stove 1000/-

My invoice will show

Product Cost 900/-

VAT 5 % = 45

Shipping Charges = 55/- = Total amount = 1000/-

My Question is this invoice i add shipping charges rs 55/-

this shipping need to applicable for Service tax

Product Cost 894/-

VAT 5 % = 44.70

Shipping Charges = 55/-

Service tax 12.36 = 6.79 ( Service tax for shipping cost )

Total = 1000.49

Which on is correct if i include shipping charges in bill need to add service tax ?

Dear Sir,

The article is very helpful but subject to one problem related to sales in other states and applicability of CST and its compliances.

Pl advice, if possible.

Regards

CMA Md Shakil

Dear All,

The above examples are very helpful but lacking the inter-state sales i.e. applicability of CST.

Pl advice with the above example having inter-state sales.

i.e From Delhi to Kolkata and vise-vesa.

Regards

Md Shakil

Hello sir

Where from we can register sole proprietorship and service tax registration.it has any office at district headquarters or any les.

for online payment, payment gateway is free or paid.

Please guide.

Hi ,

While selling books online on ecommerce sites , do we have to still file a TAX file. Books I believe are exempted from Taxation under Schedule 1

Dear Sir,

Few questions:

1. What taxation system will be applicable to coupon / deal, discount offering site? ( VAT / Service tax etc)

2. In case, on behalf of merchant for whom we are promoting offers / deals on our website DealHungama.com, how we should proceed ? Shall we ask for service tax from coustomers / or VAT?

Need taxation related help and solutions.

sir,

I recently happened to notice that flipkart/WS retail is charging VAT in their bill. However, their track order mechanism reveals that goods are moving from Banglore warehouse to Chennai Warehouse. So, ideally they should have charged CST right? Is this legal?

Dear taxguru,

What about applicability of service tax on cab aggregators like OLA / operators like Meru & shippers of goods like shippr.in or theporter.in

In case of sale of book vat shall be levied in case of intra state transaction and CST to be charged in interstate. Exemption to be given only in following case

1) Holy Books i.e. Bible,gita

2) Book published by trust which have seek exemption from the department.

DEAR SIR

I HAVE QUERY REGARDING SALES OF BOOKS ONLINE. WHETHER VAT/CST IS TO BE CHARGED IN CASE OF SELLING OF ALL BOOKS OR IS THERE ANY EXCEPTION IN REGARD TO BOOK TYPE?

THANKS IN ADVANCE

REGARDS

VICKY KAPOOR