Securities and Exchange Board of India

Consultation Paper for Market Making in Corporate Bonds

Nov 16, 2021 |Reports : Reports for Public Comments

A. Background:

1. Market makers provide liquidity to facilitate efficiency in the functioning of the financial markets. Market makers as well as other liquidity providers and their role in creating liquidity in fixed income markets are of particular interest to policymakers, given the relevance of these markets to monetary policy and financial stability. The bond market is an important source of funds and a robust liquid bond market not only helps in cheaper and easier access to issuers, but also helps in widening the investor base.

2. The vast majority of bonds, in global markets, including India, are traded over the counter (OTC) rather than on the central limit order books of exchanges. The dominance of the OTC market structure reflects a number of characteristics specific to the bond market, such as:

2.1. large pool of bond issuances, which in turn reduces the probability of finding matches in investor supply and demand, for any given bond;

2.2. fixed maturity of bonds, allowing buy and hold investors to recoup their invested funds without trading in secondary markets, often resulting in ever fewer trades towards the bond’s date of maturity; and

2.3. prevalence of institutional investors who require execution of large volume transactions that could potentially have a strong price impact when trading on a fully disclosed central limit order book.

B. Need for market making in the corporate bond market:

3. In the absence of continuous two-way markets for buyers and sellers, the broker dealers such as banks and securities trading firms, facilitate bond transactions. They either fulfil client orders by finding matches in existing supply and demand (brokerage or agency trading) or step in as counterparties of their clients’ trades by committing their own balance sheet capacity.

4. The larger issue of illiquidity in the secondary market and the challenge of matching a buyer and seller, can be dealt to a certain extent, through introduction of market makers. These market makers would be akin to Primary Dealers (‘PDs’) in the G-Sec market. Market makers’ role becomes significant because it:

4.1. provides ready counterparty to clients and other market participants, ensuring market liquidity and supporting price discovery; and

4.2. contributes to the robustness of market liquidity by absorbing temporary supply and demand imbalances, dampening the impact of shocks on market volatility and quoting prices to support investors in valuing assets.

5. Market making not only assists in creating a more vibrant bond market but also helps in generation of better yields and reducing the cost of borrowing for the issuers over the long term.

6. The market maker may also endeavour to create a sustainable business model through procurement of bonds in primary market and sale in secondary market, given the prevalence of usually higher yields in secondary market vis-à-vis primary market. Further, the bid-ask spread may act as a prospective profit opportunity for the market makers.

C. Market making in other jurisdictions:

7. The concept of market making in corporate bonds in a few international jurisdictions was studied and based on the said analysis, it was, inter alia, observed that:

7.1. Market making is largely a voluntary activity.

7.2. Generally, stock brokers double up as market makers.

7.3. Each jurisdiction has prescribed different conditions for operational aspects viz. market maker shall provide quotes for certain percentage of time during the trading day, market maker shall make market in bonds across varied maturity buckets, market maker shall provide quotes such that the bid ask spread is within a reasonable range, etc.

A snapshot of a few international requirements on market making is given in the Annex.

D. Indian scenario:

8. In the Indian Corporate Bond market, both issuances and trading are limited to only a small number of highly rated papers (i.e. about 86% of the outstanding bonds is in just the top three categories of AAA, AA+ and AA1). Further, in the secondary market, a majority of the trades are undertaken by financial institutions, banks and mutual funds.2

9. The intent of SEBI is to facilitate liquidity in the secondary market for corporate bonds, as this is an essential ingredient for the overall growth and development of the bond market. SEBI is seeking to address this issue through a multi-pronged strategy including the introduction of market making, along with facilitating an active corporate bond repo market and facilitating a backstop facility, as proposed in the Union Budgets for F.Y. 20192020 and F.Y. 2021-2022, respectively.

E. SEBI Working Group:

SEBI constituted an internal working group which deliberated on the issue of introduction of market makers in the corporate bond market in a phased manner. The working group provided their recommendations for a framework on market making. The recommendations were circulated among the members of Corporate Bonds and Securitisation Advisory Committee (CoBoSAC) and some large issuers of corporate bonds. After such deliberations, it was thought fit to consult the public on the proposal for introducing market making in the Indian corporate bond market. A proposal in this regard is elaborated in the subsequent paragraphs.

F. Proposal:

11. The following broad framework may be considered for market making in the corporate bond market:

11.1. Applicability:

a. The framework is to be made applicable to every listed issuer which has listed its non-convertible debt security(ies) and has outstanding value of listed non-convertible debt security(ies) of Rs. 500 crore and above, as on the last date of the previous financial year (cut-off date).

b. The proposed framework will be applicable for all prospective issuances, irrespective of the rating assigned thereof, by such eligible issuers.

11.2. Entities eligible to act as market makers:

SEBI-registered Stock Brokers or Merchant Bankers (including Scheduled Banks or primary dealers who are registered with SEBI either as stock brokers and/ or merchant bankers), may be authorized by SEBI to conduct market making in corporate bond market subject to the following minimum net-worth requirements:

a. SEBI (Stock Brokers) Regulations, 1992 and SEBI (Merchant Bankers) Regulations, 1992 already require a minimum net-worth requirement for stock brokers and merchant bankers, respectively.

b. To ensure the capital adequacy of a market maker, only those stock brokers/ merchant bankers may be authorized to act as market makers that have an additional net-worth of Rs. 10 crores over-and-above the requirements of their respective SEBI Regulations.

11.3. Responsibilities of the Issuer:

An eligible issuer shall have the following obligations:

a. Make arrangements for market making corresponding to at least 25% of the amount to be raised (through fresh issuances – new/ old ISINs) during each quarter.

b. Accordingly, the issuer can identify ISINs, for which market making activity will be arranged, based on criteria viz. rating buckets, tenors and liquidity.

c. For such identified ISINs, the issuer shall appoint at least two market makers before listing. The details of the market making arrangement shall be disclosed accordingly in the offer document.

d. The issuer shall enter into an agreement with the market maker. This agreement shall specify details of the ISINs in which market making facility will be permitted. Such agreement shall contain relevant terms and conditions including conditions for revocation, after giving prior notice.

e. The Issuer shall continue to make arrangements for market making in such identified ISINs for at least 5 years from the date of issuance or the tenure of the bond, whichever is earlier. During this period, if the issuer and/ or market maker decide to discontinue their arrangement, due to contractual issues or otherwise, both the parties shall ensure that their respective obligations are fulfilled.

f. The agreement between the issuer and the market maker shall include terms and conditions in order to provide the discretion to the market maker to operate freely without interference from the issuer on a day-to-day basis, to avoid conflict of interest/ insider trading.

g. In case the issuer makes a reservation in primary issuance or keeps treasury stock, for providing securities to the market maker, it shall make necessary disclosures in the offer document.

11.4. Inventory for market making in identified ISINs:

a. The market maker may create initial inventory of bonds for market making, directly from the market or with the assistance of the issuer. Some suggested options in this regard are given below:

Option 1 (Reservation in Primary issuance):

1. A portion of the primary issuance, whether public issuance or private placement, shall be earmarked for subscription by the market maker(s).

2. The market maker will make market in secondary market with this inventory.

3. The market maker buys bonds, receives coupon and earns from the spread from the transactions.

Option 2 (Secondary market):

Model I:

1. The issuer will subscribe to its own issuance, to the extent reserved for the market maker, in the form of treasury stock and keep the same in an escrow account. Hence, ownership of bonds remains with the issuer.

2. The issuer will make this inventory available to the market maker, who in turn will make market in secondary market, for pre-agreed fees/ commission.

3. Proceeds from these transactions will be passed on by the market maker to the issuer.

4. The issuer buys bonds, receives coupon and earns from the spread from the transactions. The market maker earns the fees/ commission.

Model II:

1. Market maker will create its inventory by purchasing bonds in the secondary market and make market in secondary market.

2. The market maker buys bonds, receives coupon and earns from the spread from the transactions.

b. On an ongoing basis, issuer may further assist the market maker for managing excess/ short fall of inventory.

11.5. Funds for market making:

a. The issuer may make funds available to the market maker in lieu of the ISIN-wise inventory, as per mutually agreed terms and conditions/ agreement; towards this, the issuer shall ensure that the Articles/ necessary resolutions are in place to enable such funding.

b. Alternately, market maker may approach Banks or Financial institutions for funds, as per mutually agreed terms and conditions/ agreement. Issuer may also assist in the same.

11.6. Responsibilities of market maker:

A market maker shall have the following responsibilities:

a. Make market, through trades, only on the Request for Quote (RFQ) platform, through their proprietary accounts.

b. Provide two-way quotes during such minimum time frame (say 75% of the time during market hours on a trading day).

c. Be present in the best buy/ sell order/ quotes for e.g. top 5 buy/ sell order/ quote. This will ensure that a balance is maintained between the supply and demand in the bond market. The stock exchanges shall assist in providing necessary systems for implementing the same.

d. Guarantee execution of orders at quoted yield and quantity for quotes given by it. Market maker shall be responsible to ensure successful completion of the settlements.

e. For each below AAA rated ISIN that market maker makes, it can make market in maximum two AAA rated ISINs, on half yearly basis. The said requirement can be fulfilled by it across issuers with whom it enters into an arrangement with.

f. The market maker also has the option of selecting ISINs across varied maturity buckets viz. 1-3 years, 3-5 years, 5-7 years and over 7 years.

11.7. Compliance requirements for a market maker:

a. Risk Management:

i. A market maker should aim to minimize the risk taken while at the same time being able to maintain an active market.

ii. A market maker shall ensure development of adequate infrastructure especially pertaining to Risk Management System

iii. All risks to which the market maker is exposed on account of its market making business in corporate bonds shall be identified and risk tolerance level should be set.

iv. Processes shall be established to manage such risks and a clear and comprehensive set of limits shall be established to manage such risks.

v. Stress testing of risk positions shall be conducted.

b. Governance:

i. A market maker shall formulate a policy to prevent conflict of interest arising from its role as a market maker and any other activity. Such policy shall be disclosed publicly.

ii. A market maker shall maintain arms-length relationship between its market making activity and any other activity.

iii. The Board of Directors and the compliance officer of the market maker shall ensure implementation of:

-

- Adequate and effective risk management and internal control policies and procedures;

- Appropriate organization structure (with clear lines of responsibility and accountability), staff and other resources for prudent conduct of the market making business, risk management function, internal control function and internal audit;

- Adequate and effective measures towards regulatory compliance; and

- Adequate and effective measures to address observations from internal and external audits.

iv. The board of directors shall approve written policies which define the overall framework within which the market making business shall be conducted, and the related risks managed. Such framework shall include, but not be limited to, the following aspects:

-

- Establish the entity’s overall appetite for taking risk and ensure that it is consistent with its strategic objectives, capital strength and capability to manage risk effectively;

- Specify permitted activities and limits for the business of market making in corporate bonds;

- Detail the type and frequency of reports which are to be made available to the Board of Directors and its committees.

c. Other compliances:

i. The market maker shall continue to comply with SEBI (Stock Brokers) Regulations, 1992 or SEBI (Merchant Bankers) Regulations, 1992, as applicable.

ii. Internal audits of these intermediaries shall also cover the market making business of the stock broker/ merchant banker and review the compliance with SEBI’s norms on market making including testing the adequacy and effectiveness of the risk management system and internal controls.

iii. The market maker (stock broker/ merchant banker) shall preserve all records related to its market making activity including business, control and monitoring, as per the timelines prescribed under their respective Regulations.

11.8. Incentives, dissemination and monitoring by stock exchanges:

a. Incentives:

Stock exchanges may consider providing incentives/ relaxation in transaction charges as an incentive for market makers. Any scheme on waiver/ rebate of fees given by the stock exchanges to market makers/ issuers shall be adequately disclosed prior to offering the same.

b. Dissemination:

Stock exchanges shall disseminate the following information at the end of each trading day:

i. Total quantity traded by the market maker in a particular ISIN and its percentage to total quantity traded in the market for that ISIN.

ii. Minimum, maximum and median spread at which the market maker has provided the quotes.

iii. Minimum, maximum and median prices at which the market maker has executed the trades.

iv. Comparison of the above disclosures (viz. opening price, high price, low price, close price, traded quantity and amount) with corresponding figures of other similar ISINs where there is no market making.

c. Compliance and Monitoring:

i. Compliance by the issuer and the market maker with their obligations, shall be monitored by the stock exchanges in the manner as prescribed by SEBI from time to time.

ii. The obligations of the issuer and the market maker may be relaxed in case of bespoke deals and market disruptions, as may be decided by SEBI or stock exchanges.

11.9. Implementation:

The issuers and market makers’ responsibilities shall be on a ‘comply or explain’ basis for one financial year to start with and may be reviewed thereafter.

G. Public Comments:

12. The Indian market for corporate debt needs buoyancy and this has been high on the agenda of SEBI. As mentioned earlier, market making is a significant cog in the wheel which will not only enhance liquidity, but also provide a fillip to facilitate market efficiency

and functioning. A vibrant secondary market in corporate bonds can come about if market making mechanism is introduced; which, in turn will give issuers an opportunity to gain from improved liquidity premium, better price discovery and consequent lowering of the

cost of debt.

13. Considering the implications of the said matter on the market participants including the issuers, public comments are invited on the proposal. The comments/ suggestions may be provided as per the format given below:

| Name of the person/entity providing comments: | |||

| Name of the organization (if applicable): | |||

| Contact details: | |||

| Category: market intermediary/ participant (mention type/ category) or public (investor, academician, etc.) | |||

| Sr. No. | Proposal | Comments/ Suggestions | Rationale |

14. Kindly mention the subject of the communication as, “Comments on Consultation Paper for Market Making in Corporate Bonds”.

15. Comments as per aforesaid format may be sent, latest by December 16, 2021, in any of the following manner:

a. By email to: pradeepr@sebi.gov.in; divyah@sebi.gov.in; chaitalik@sebi.gov.in; and kirand@sebi.gov.in; or

b. By post to:

Pradeep Ramakrishnan,

General Manager,

Department of Debt & Hybrid Securities

Securities and Exchange Board of India,

SEBI Bhavan, C4-A, G-Block,

Bandra Kurla Complex, Bandra (East),

Mumbai – 400051

Issued on: November 16, 2021

Annex

Snapshot of Market Making requirements in a few jurisdictions

1. London Stock Exchange3:

On the London Stock Exchange, brokers are eligible to be market makers.

a. Market makers will be required to enter 2-way prices within the applicable maximum spread and the applicable minimum quote size.

b. Market makers in order book securities will not be able to enter executable quotes that are wider than the maximum spread required. The maximum spread varies according to four percentage bands, 1.5%, 3%, 5% and 15%.

c. Market makers must maintain an Executable Quote or single pair of Named Limit Orders in each security in which it is registered for at least 90% of continuous trading during the mandatory period.

d. Market maker quotes are to be maintained throughout the mandatory period until the end of the closing auction which includes any price monitoring extensions and random end periods.

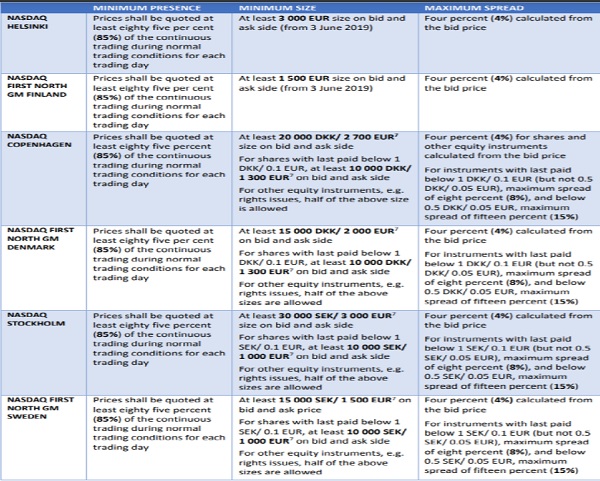

2. Liquidity provider program of NASDAQ Europe: 4

Trading members are eligible to be market makers. A snapshot of the liquidity provider program of NASDAQ Europe, which is similar to market making, is provided in the following table:

3. Administrative Rules on Market Makers in the Inter-bank Bond Market in The People’s Bank of China5:

“Financial institutions” incorporated within China that meet stipulated requirements can be market makers. Currently, registered market makers are primarily Banks, along with merchant bankers and brokers. Stipulated requirements include Net/Registered Capital requirements (>130 bn USD), entities to be actively trading in market with relatively high volume in cash bond transactions, having necessary experience and capability, risk control mechanism, bond market research capabilities, employing at least 5 qualified bond market practitioners, legal compliance record, etc.

Other major requirements:

a. Each market maker shall designate no less than six bonds in market making, and the final designated ones shall include the following three categories, i.e. a government bond, a governmental development financial institution bond and a non-government credit bond.

b. The maturity of market making bonds shall cover at least four out of the following five types of years to maturity, i.e. 0-1 year, 1-3 years, 3-5 years, 5-7 years and over 7 years.

c. A market maker must not alter market making bonds during a business day once it has designated them, and it shall offer continuous bilateral price quotes on designated bonds with an interval no longer than 30 minutes.

d. Minimum amount for a single price quote shall be 1 million yuan in face value.

e. A market maker shall offer real prices in bilateral price quotes, and bid-ask spread shall be within a reasonable range.

Notes:-

1 As per outstanding Bonds/ Debentures held in NSDL and CDSL depository system as on August 31, 2021.

2 During September 2021, as per Exchanges data, approx. 24.17% of the trades on OTC and RFQ platform were undertaken by Mutual Funds.

3 https://www.londonstockexchange.com/trade/market-making

4 https://www.nasdaq.com/docs/Overview_of_Liquidity_Provider%20Program_V2_Sep_1_2019.pdf

5 http://www.chinamoney.com.cn/english/svcfopgudrmkRgls/20170225/2110.html