Securities and Exchange Board of India

Circular No. SEBI/HO/MIRSD/MIRSD-PoD-1/P/CIR/2023/73 Dated: May 19, 2023

To

All Recognized Stock Exchanges

Depositories

Stock Brokers through Recognized Stock Exchanges

Dear Sir/Madam,

Subject – Risk disclosure with respect to trading by individual traders in Equity Futures & Options Segment

1. Over time there has been increased participation of investors in Indian securities market, including, in the derivatives segment. While investors are expected to make investment decisions based on their own due diligence and risk appetite, it is important to empower them with detailed information about the risks associated with trading in derivatives.

2. With a view to facilitating informed decision making by the investors trading in derivatives segment, it has been decided to introduce ‘Risk disclosures’ with respect to trading in equity Futures & Options (F&O) segment.

3. Accordingly, all stock brokers shall display the ‘Risk disclosures’ given at Annexure-I on their websites and to all their clients in the manner as specified below:

3.1. Upon login into their trading accounts with brokers, the clients may be prompted to read the ‘Risk disclosures’ (which may appear as a pop-up window upon login) and shall be allowed to proceed ahead only after acknowledging the same.

3.2. The ‘Risk disclosures’ shall be displayed prominently, covering at least 50 percent area of the screen.

4. All Qualified Stock Brokers (QSBs) shall maintain the Profit and Loss (P&L) data of their clients on continuous basis as per the format given at Annexure-II. The P&L data of the clients shall be retained for at least 5 years.

5. Stock Exchanges and Depositories are directed to:

5.1. bring the provisions of this circular to the notice of their members / participants and also disseminate the same on their websites;

5.2. display the ‘Risk disclosures’ on their respective websites, with a link to study conducted by SEBI.

6. Applicability: The provisions of this circular shall come into force with effect from July 01, 2023.

7. This circular is issued in exercise of powers conferred under Section 11(1) of the Securities and Exchange Board of India Act, 1992, to protect the interests of investors in securities and to promote the development of, and to regulate, the securities market.

8. This circular is available on SEBI website at www.sebi.gov.in under the category “Circulars”.

Yours faithfully,

Aradhana Verma

General Manager

Market Intermediaries Regulation and Supervision Department

Tel. No.: +91-022 26449633

Email: aradhanad@sebi.gov.in

Annexure-I: Risk disclosures

RISK DISCLOSURES ON DERIVATIVES

- 9 out of 10 individual traders in equity Futures and Options Segment, incurred net losses.

- On an average, loss makers registered net trading loss close to ₹ 50,000.

- Over and above the net trading losses incurred, loss makers expended an additional 28% of net trading losses as transaction costs.

- Those making net trading profits, incurred between 15% to 50% of such profits as transaction cost.

Source:

1. SEBI study dated January 25, 2023 on “Analysis of Profit and Loss of Individual Traders dealing in equity Futures and Options (F&O) Segment”, wherein Aggregate Level findings are based on annual Profit/Loss incurred by individual traders in equity F&O during FY 2021-22.

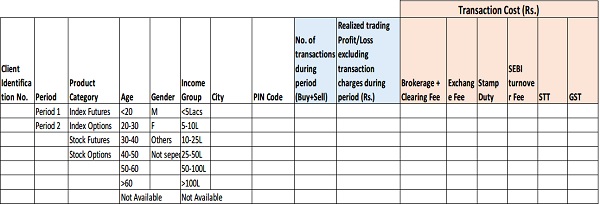

Annexure-II: Data Format

A. Equity F&O Segment

Notes:

1. Client-set: All Individual Clients (which includes HUF and NRIs; excludes Proprietary traders, institutions, partnership firms etc.)

2. Segment: Equity F&O

3. Period: Financial Year

4. Client level realized trading Profit/Loss during the period is considered.

5. With regard to cases where 1 leg of transaction falls under the period, while the other falls outside, explanation is given as under-

- Example 1: Period: April 2018 to March 2019. Consider Contract-A with expiry in April 2018.

Contract- A purchased & sold in March 2018 – will not be considered

Contract- A purchased in March 2018, sold in April 2018/ settled on expiry – will be considered

- Example 2: Period: April 2018 to March 2019. Consider Contract-B with expiry in April 2019.

Contract- B purchased & sold in March 2019 – will be considered

Contract- B purchased in March 2019, sold in April 2019/ settled on expiry – will not be considered

6. Contracts resulting in physical delivery of stocks may be excluded.

7. For PIN Codes – correspondence address may be considered.

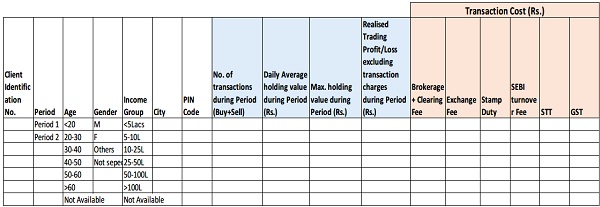

B. Cash Segment

Notes:

1. Client-set: All Individual Clients (which includes HUF and NRIs; excludes Proprietary traders, institutions, partnership firms etc.)

2. Segment: Cash Segment

3. Period: Financial year

4. Client level realized trading Profit/Loss during the period is considered.

5. For computation of Client level realised profit/loss in cash segment during the period, only transactions where both legs (buy and sell side) in a scrip are executed during the period, are considered.