Securities and Exchange Board of India

Discussion Paper on ‘Usage of pool accounts in Mutual Fund Transactions’

Dec 23, 2019- Reports : Reports for Public Comments

A. Background

i. SEBI, vide circular dated November 13, 2009, permitted units of Mutual Fund (MF) schemes to be transacted through registered stock brokers on recognized stock exchanges.

ii. In order to provide more avenues for transacting in Mutual Fund units, vide circular dated November 09, 2010, it was permitted that units of MF schemes may be transacted through clearing members of the registered Stock Exchanges and redemption requests for units in demat form may be processed by Depository Participants, in addition to transactions directly with the mutual funds and through stock brokers. For this purpose, units on purchase and redemption amount were allowed to be routed through broker’s/ clearing member’s pool account.

iii. Vide circular dated October 04, 2013, MF Distributors (MFDs) were also allowed to use the infrastructure of the recognized stock exchanges to purchase and redeem MF units directly from MFs/Asset Management Companies (AMCs) on behalf of their clients. However, MFDs were not allowed to handle pay-in and pay-out of funds and units. The recognized stock exchanges were directed to put in necessary system in place to ensure that pay-in is directly received by recognized Clearing Corporation and pay-out is directly made to the investor account. Similarly, the units would be credited and debited directly from the demat account of the investors. Exchange platforms also facilitate MF transactions in non-demat mode.

iv. Vide circular dated October 19, 2016, SEBI registered Investment Advisers (IAs) were also allowed to use stock exchanges infrastructure to purchase and redeem MF units directly from MF/AMCs on behalf of their clients under the provisions laid down in Circular dated October 04, 2013 with respect to MFDs.

Page Contents

B. Current Structure for Mutual Fund Transactions:

i. At present, an investor can use any of the following methods to invest in mutual funds:

a. Investment directly with the AMCs – Both offline and online

b. Investment through Stock Broker(s) /MFD(s) /IA(s) using Exchange Platform

c. Investment through MFD(s) /IA(s) outside exchange platforms– Both offline and online

d. Platforms for MF transactions provided by other entities not covered above, including those registered as RTAs and are functioning in a manner similar to clearing corporations – Both offline and online

ii. As on October 31, 2019, there are 857 brokers, 62,460 distributors and 356 Investment Advisers registered with Stock exchanges for Mutual Fund transactions.

iii. Value of MF transactions on NSE and BSE on a combined basis during 2018-19 amounted to Rs. 1,04,273 crores. Details of such transactions executed on these exchanges through pool route (i.e. through brokers) and through non-pool route (i.e. through MFDs and IAs) are as under:

Pool (Rs.

|

Non-Pool (Rs. Cr) |

Share of Pool (%) |

Share of

|

Pool (Rs. Cr) |

Non-Pool (Rs. Cr) |

Share of Pool (%) |

Share

|

Share of Pool (%) |

Share

|

|

BSE |

NSE |

Both Exchanges Combined |

||||||||

FY 2016-17 |

31,704.20 |

4,293.66 |

88% |

12% |

3524.38 |

6198.32 |

36.2% |

63.8% |

77.1% |

22.9% |

FY 2017-18 |

47,683.77 |

8,021.51 |

86% |

14% |

4855.76 |

23569.62 |

17.1% |

82.9% |

62.4% |

37.6% |

FY 2018-19 |

46,191.55 |

20,784.35 |

69% |

31% |

7488.28 |

29808.77 |

20.1% |

79.9% |

51.5% |

48.5% |

Source: BSE & NSE

C. Transactions in Pool Account

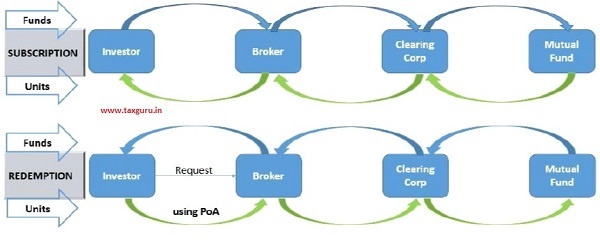

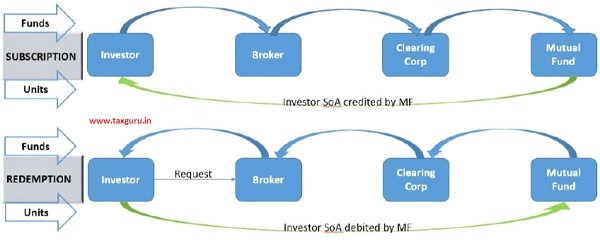

i. Transactions through stock brokers on Exchange Platform

For transactions on stock exchanges (Equity and Derivatives), funds and securities are routed through broker’s pool account. The industry has also evolved to utilize the pool account to give greater ease of transactions, convenience and flexibility to the investors in making Mutual Fund transactions.

Simplified versions of process flows for subscription and redemption transactions through stock brokers on stock exchange platforms are provided below:

Transactions in Demat Mode via Stock Brokers – Present Flow of Funds & Units

Transactions in Non-Demat/Statement of Account (SoA) Mode via Stock Brokers – Present Flow of Funds & Units

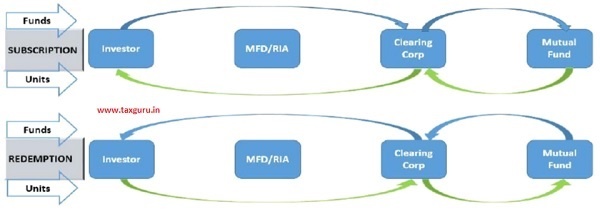

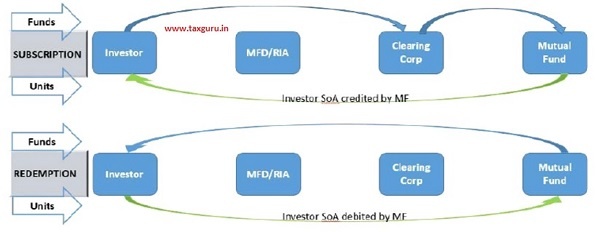

ii. Transactions through MFD(s) or registered IAs on Exchange Platform

As stated above in paragraphs A(iii) and A(iv), MFD(s) and registered IAs were allowed to use stock exchanges’ infrastructure to purchase and redeem MF units directly from MF/AMCs on behalf of their clients.

It was further stated in the circular dated October 04, 2013 that the MF distributors would not handle pay-in and pay-out of funds and units on behalf of the investors and Stock exchanges were advised to put necessary system in place to ensure that pay in will be directly received by recognized clearing corporation and payout will be directly made to investors’ bank account and units would be credited and debited directly from the account of the investors. Similar provisions were also made applicable for IAs vide circular dated October 19, 2016.

Simplified versions of process flows for subscription and redemption transactions through MFD(s) / IAs on stock exchange platforms are provided below:

Transactions in Demat Mode* via MFD(s) / IAs – Present Flow of Funds & Units

*NSE does not allow MFDs and IAs to place orders for units in dematerialized form

Transactions in Non-Demat Mode/SoA via MFD(s)/ IAs – Present Flow of Funds & Units

iii. Transactions through MFD(s) / IAs outside Exchange Platform and through platforms mentioned in paragraph B(i)(d)

Many MFD(s) registered with AMFI and SEBI registered IAs commonly referred as “Channel Partners” and other online platforms covered under paragraph B(i)(d) are also providing digitalized services to investors to transact in mutual fund units. Through these platforms, investors can place single or multiple orders to transact in mutual funds units. These platforms are often pooling the client’s funds in an escrow account / nodal account and subsequently transfer to AMCs either on per transaction basis or lump sum basis. It is understood that, at times, MFDs/ IAs/ other online platforms have been enabled to operate through the pool account mechanism based on bilateral understanding with AMCs.

Transaction details are sent by MFDs/ IAs/ other online platforms to AMCs/ RTAs, based on which units are issued/ redemption is made.

Simplified version of process flow for such MFDs/ IAs/ other platforms, involving pooling of fund, is provided below:

D. Conveniences available to investors in current structure

i. Asset Allocation/Cross Investment in Multiple Products – Stock Broker’s Pool Account allows investors to seamlessly invest across multiple products such as equity, derivatives, NCDs, G-Sec, Mutual Funds, ETFs, etc. using the same broking account, without the need for investors to make frequent fund transfers. Triggers for investments across products/ sectors etc. can be easily monitored and maintained.

ii. Inter scheme or inter AMC Switch – In case of investments in Mutual funds through stock broker’s pool account, inter scheme or inter AMC switch can be easily implemented, without the need of investor to make frequent fund transfers.

iii. Investment in SIP– Through pool account, client can start/stop SIP very easily without reaching out to the bank or MF.

iv. Efficient and cost effective Fund Transfers – Usage of stock broker’s pool account reduces the frequency of fund transfers among investors/ stock brokers/ clearing corporation etc. therefore becomes cost effective.

v. Facilitates Innovation and Better Service – A pool account enables innovation as technology can be used to create tools/ products that provide better understanding about their investment to the investors. For example – portfolio visualization tools that highlight cross-asset exposure to particular security/ sector help investors to re-balance their portfolio.

E. Extant Practices, Issues and Challenges

Stock Brokers, MFDs and IAs including Channel Partners and other platforms covered under paragraph B(i)(d) are providing valuable services to investors and have helped the Mutual Fund Industry to grow at a substantial pace. However, certain challenges have been envisaged in the current process of using pool accounts. The details are given as under:

In case of Stock Brokers:

i. Loss of traceability of transaction and funds –

As stated above, with respect to investors who purchase and redeem MF units through stock brokers and clearing members, the units and funds flow through brokers’ or clearing members’ pool account. Units and funds move in an aggregate manner from broker’s account to RTA’s/AMC’s account. In such case once pooling happens at an intermediary level the traceability of funds/ investor details is lost to AMCs/ RTAs.

RTAs are not able to identify the exact order details of the investors against which units have been moved / not moved which in turn leads to difference in balances between RTA and depository books.

Further, with respect to investors who purchase and redeem MF units in demat form through stock brokers and clearing members, MF/AMC is discharged of its obligation of payment / credit of units, if such payment or the units have been credited to the broker/clearing members.

Therefore, the actual payment of funds to investors or credit of units in investors’ account is beyond the purview of MF/AMC. Hence, any dispute regarding non-payment of funds or non-credit of units is taken up by the investors under the exchange’s grievance redressal and arbitration mechanism.

iii. Potential misuse of pooled funds/ securities

In the recent past, instances have come to light where client’s funds/securities were diverted or mis-utilized by trading member/ clearing member toward margin obligations or settlement obligations of itself or for some third party or for raising loan against shares on its own account, etc.

As may be observed from data provided in paragraph B(iii) above, the value of MF transaction via pool account has remained significant in the last three years. However, the share of transactions (value) through non-pool has continuously been on rise in the last three years.

In case of Digital Platforms provided by MFDs and IAs (including Channel Partners) / Platforms covered under paragraph B(i)(d):

The practice of acceptance of funds by above platforms poses several risks as given under:

i. AMCs lose the sight of the source of funds as they receive the funds from pool/escrow accounts (instead of investors’ bank accounts).

ii. MFDs are not expected to handle clients’ funds and/or securities. In physical applications, MFDs are not allowed to take cheques/payment instruments from clients in their names. Instead, clients are required to give cheques/payment instruments which are in favour of Mutual Funds/AMCs. IAs are also envisaged to provide non-binding advisory services to their clients. Routing of funds/units through them may lead to potential misuse of funds/units.

iii. Similar risks mentioned above in points (i) and (ii) also arise when funds/units are being pooled using escrow account or in any other form by platforms covered under paragraph B(i)(d).

F. Proposals

In order to address the above mentioned challenges and to promote a secure investing environment in Mutual Funds, the following is proposed:

i. Pooling of funds/units by Stock Brokers, MFDs, IAs and other platforms may be discontinued for Mutual Fund Transactions. For implementation of the same, following may be ensured:

a. For transactions on Exchange platforms through stock broker(s), Exchanges shall put necessary system in place to ensure that pay-in is directly received by recognized Clearing Corporation from investor’s bank account and pay-out is directly made to investor’s bank account from recognized Clearing Corporation’s account. In the same manner, for subscription and redemption, units are directly credited into and debited from the investor account (Demat or Statement of Account) respectively.

b. For transactions outside Exchange platforms, as mentioned in paragraph B (i) (c) and B (i) (d) above, AMC at its end shall put necessary system in place to ensure both subscription and redemption (funds transferred and units transacted between investor and AMC) take place without use of pooling through escrow / nodal account etc.

ii. Suggestions are also requested for improving ease of transaction in MF units through non-pool accounts, as is presently available through pool accounts.

Comments/Suggestions on the above proposals may be sent by email at mfcomments@sebi.gov.in , on or before January 13, 2020 in the following format :

| Name of Entity / Person / Intermediary/ Organization: | |||

| Sr. No. | Issues | Suggestions | Rationale |