The Reserve Bank of India (RBI) can exercised the power under The Reserve Bank of India Act, 1934 to issue or cancel the certificate of Non-Banking Finance Company (NBFC) in India. The Reserve Bank of India plays the key role of the Regulatory body and an authority to supervise and regulate NBFCs in India. RBI grants license to the NBFCs only after satisfaction of the prescribed eligibility criteria.

Eligibility Criteria to Register as NBFC

A company should be registered under the Companies Act, 1956/Companies Act 2013

Company should have a minimum net owned fund of ₹ 200 lakh/ Fixed Deposit of Rs.200

One of the Director should be having exposure into Financial industry for running the Operations of NBFC.

Cibil score of all the Director should be more than 700.

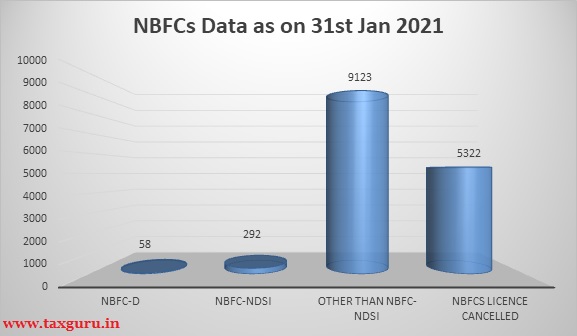

NBFC Statistics (as on 31st Jan 2021)

The Reserve Bank of India issues NBFCs Licence to those who is going to serve to the economy and that should be in the Public Interest.

NBFC-D stands for Deposit Taking NBFC

NBFC-NDSI- Systemically Important non-deposit accepting NBFCs (NBFCs whose asset size is of ₹ 500 cr or more as per last audited balance sheet are considered as systemically important NBFCs)

From the above chart analysis, we can observe that approximate 50% NBFC licence has been cancelled by the Reserve Bank of India.

Reasons for NBFC License Cancellation:

RBI shall provide an opportunity to the concerned NBFC for its clarification, before the Cancellation of its Registration. Only on occasions, when RBI feels a delay shall result against public interest or depositors, is the Registration cancelled instantaneously. At any time if the Non-Banking Financial Company found the following situation can result in cancellation of Certificate of registration granted:

Lets have detailed discussion on the above mentioned reasons.

Non-maintenance of Net Owned Fund

As per section 45-IA (introduce w.e.f 09-01-1997) of the Reserve Bank of India Act 1934, no non-banking financial company shall commence or carry on the business of a non-banking financial institution without having the net owned fund of twenty-five lakh rupees or such other amount, not exceeding two hundred lakh rupees, as the Bank may, by notification in the Official Gazette, specify.

Further, The RBI had issued a notification on 27 March 2015. As per this notification, the NBFCs are required to maintain an enhanced NOF of 2 crore rupees to continue their business. The same notification allowed NBFCs time till 1 April 2016 to raise their NOF to 1 crore and eventually to 2 crores by 1 April 2017.

After the above said notification, The Reserve Bank of India has cancelled many NBFCs CoR which fails to comply with the NOF requirement.

Not Operate in the Public Interest

NBFCs should carry the business in the public interest. NBFC has Board approved Fair Practice code policy, Recovery policy, Grievance Redressal Policy and take care that all the said policy should be uploaded on the Company’s Website and placed at Company’s Premises. The motive behind this is that the customer should get aware about with NBFC practice. The Policies should be in public Interest and in consonance with the notifications, Circulars, Master Directions issued by RBI from time to time.

Failed to re-pay the deposits

When an NBFC fails to repay any deposit or part thereof in accordance with the terms and conditions of such deposit, the depositor can approach Company Law Board or Consumer Forum or file a civil suit in a court of law to recover the deposits. NBFCs are also advised to follow a grievance redress procedure. Even then also if the RBI seems that NBFC is not in condition to re-pay the deposits or failed to re-pay the deposits then RBI shall provide an opportunity to the concerned NBFC for its clarification, before the Cancellation of its Registration.

Not Complied prohibitory orders of RBI

The RBI may after the Inspection of the NBFCs issues any prohibitory order to the company or any other NBFC/RNBC with which the directors/promoters etc. were associated. NBFCs should comply the prohibitory order issued by the RBI. Avoidance/Ignorance of Prohibitory order may lead to cancellation of NBFCs Licence.

Not Carrying NBFC Activity

To Continue as a NBFCs It has to do Financial activity as principal business. Here Financial activity as principal business is when a company’s financial assets constitute more than 50 per cent of the total assets and income from financial assets constitute more than 50 per cent of the gross income. A company which fulfils both these criteria will be continue as NBFC by RBI. This test is popularly known as 50-50 test. Every NBFC has to take care about 50-50 Test to continue as a NBFC Company.

Non-Complied NBFC:-

Apart from the Companies Act 2013, Income Tax Act and Other Statutory Act compliances, the following RBI Compliances has to done by the NBFC Company to remain as Complained NBFC.

A. Returns to be submitted by deposit taking NBFCs

1. NBS-1Quarterly Returns on deposits in First Schedule.

2. NBS-2Quarterly return on Prudential Norms is required to be submitted by NBFC accepting public deposits.

3. NBS-3Quarterly return on Liquid Assets by deposit taking NBFC.

4. NBS-4Annual return of critical parameters by a rejected company holding public deposits. (NBS-5 stands withdrawn as submission of NBS 1 has been made quarterly.)

5. NBS-6Monthly return on exposure to capital market by deposit taking NBFC with total assets of ₹ 100 crore and above.

6. Half-yearly ALM returnby NBFC holding public deposits of more than ₹ 20 crore or asset size of more than ₹ 100 crore

7. Audited Balance sheet and Auditor’s Report by NBFC accepting public deposits.

8. Branch Info Return.

B. Returns to be submitted by NBFCs-ND-SI

1. NBS-7A Quarterly statement of capital funds, risk weighted assets, risk asset ratio etc., for NBFC-ND-SI.

2. Monthly Return on Important Financial Parameters of NBFCs-ND-SI.

3. ALM returns:

(i) Statement of short term dynamic liquidity in format ALM [NBS-ALM1] -Monthly,

(ii) Statement of structural liquidity in format ALM [NBS-ALM2] Half yearly,

(iii) Statement of Interest Rate Sensitivity in format ALM -[NBS-ALM3], Half yearly

4. Branch Info return

C. Quarterly return on important financial parameters of non deposit taking NBFCs having assets of more than ₹50 crore and above but less than ₹100 crore

Basic information like name of the company, address, NOF, profit / loss during the last three years has to be submitted quarterly by non-deposit taking NBFCs with asset size between ₹ 50 crore and ₹ 100 crore

Directors are not fit and proper

To run a NBFC, the Directors of the NBFC should be fit and proper. Here Fit and proper means:-

- Directors should have Finance background for running the operations of NBFC.

- No any prosecution, either civil or criminal, been initiated or pending or commenced or has resulted in conviction, if any, in the past, against the Director and/or against any of the entities he is associated with for violation of economic laws and regulations.

- No any disciplinary action, pending or commenced or resulting in conviction in the past against him/her or has not been banned from entry of any professional occupation at any time. Director should not be disqualified as per sec 164 of the Companies Act 2013.

- Director has not been found guilty of violations of rules/ regulations/legislative requirements by Customs/ Excise/ Income Tax/ Foreign Exchange/ Other Revenue Authorities.

- Directorships held by the Director does not exceed the limits prescribed under Section Section 165 of the Companies Act, 2013.

- Directors is not involved in any criminal case, including under section 138(1) of the Negotiable Instruments Act.

*****

Disclaimer: The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

THE AUTHOR – CS MONIKA MALHOTRA (PRACTICING COMPANY SECRETARY) CAN BE REACHED AT csmonikamalhotra26@gmail.com or +91-9599561517

Author Bio