The Reserve Bank of India issued the “Commercial Banks – Capital Charge for Credit Risk (Standardised Approach) Directions, 2026” to implement the Basel III framework for calculating risk-weighted assets in a more consistent and risk-sensitive manner. Applicable from April 1, 2027, the Directions mandate the Standardised Approach for assessing credit risk across banking book exposures, covering sovereigns, banks, corporates, MSMEs, retail, real estate, and off-balance sheet items. The framework prescribes detailed risk weights based on external credit ratings, exposure types, and collateral, while emphasizing due diligence, alignment with internal risk assessment, and prudent valuation norms. It also introduces refined treatment for specialised lending, NPAs, unhedged foreign currency exposures, and credit risk mitigation techniques. Overall, the Directions aim to strengthen capital adequacy, enhance risk management practices, and ensure greater transparency and comparability in banking regulation.

RESERVE BANK OF INDIA

RBI/DOR/2026-27/397

DOR.CRE.REC 5/21.06.201/2026-27 | Dated: April 27, 2026

Reserve Bank of India (Commercial Banks – Capital Charge for Credit Risk – Standardised Approach) Directions, 2026

1. Introduction

The Basel Committee on Banking Supervision had issued the final ‘Basel III framework (Basel III: Finalising post-crisis reforms) in December 2017 with a view to ensuring prudent and credible calculation of risk-weighted assets for arriving at capital ratios for banks in a comparable and risk-sensitive manner. The framework has permitted two broad approaches for calculating risk-based capital requirements for credit risk, viz., the Standardised Approach (SA) and the Internal Ratings Based approach (IRB). The Reserve Bank of India has decided to implement the Standardised Approach (SA) for credit risk for banks under its jurisdiction, as prescribed in these Directions.

2. Powers Exercised and Commencement

1. In exercise of the powers conferred by the Sections 21 and 35A of the Banking Regulation Act, 1949, the Reserve Bank of India (hereinafter called the ‘Reserve Bank’ or RBI) being satisfied that it is necessary and expedient in the public interest and in the interest of depositors so to do, hereby, issues these instructions hereinafter specified.

2. These instructions shall come into effect from April 01, 2027.

3. Scope

1. These instructions shall apply, unless specified otherwise, to the banking book exposures of Commercial Banks (hereinafter collectively referred to as ‘banks’ and individually as a ‘bank’).

2. For the purpose of these Directions, ‘Commercial Banks’ means banking companies (other than Small Finance Banks, Payments Banks, and Local Area Banks), corresponding new banks, and the State Bank of India, as defined respectively under clauses (c), (da), and (nc) of Section 5 of the Banking Regulation Act, 1949.

4. Definitions

(1) In these instructions, unless the context otherwise requires, the terms herein shall bear the meanings assigned to them below:

(i) “Capital market exposure” shall have the same meaning as defined in ‘Reserve Bank of India (Commercial Banks – Concentration Risk Management) Directions, 2025, as amended from time to time.

ii. “Commercial Real Estate exposure” means an exposure secured by real estate and which is not a residential real estate

iii. “Commitment” with reference to a bank’s off-balance sheet exposures shall mean any contractual arrangement that has been offered by the bank and accepted by its counterparty to extend credit, purchase assets or issue credit substitutes. It includes any such arrangement that can be unconditionally cancelled by the bank at any time without prior notice to the obligor. It also includes any such arrangement that can be cancelled by the bank if the obligor fails to meet conditions set out in the facility documentation, including conditions that must be met by the obligor prior to any initial or subsequent drawdown under the arrangement.

iv. “Consumer Credit” shall have the same meaning as defined in Banking Statistics I (Harmonised Definitions) on the RBI’s website.

v. “Counterparty banks” shall mean other Commercial Banks, Small Finance Banks, Payments Banks, Regional Rural Banks, Local Area Banks, Urban Cooperative banks, Rural Co-operative Banks and All India Financial Institutions (AIFIs) on which a bank takes exposures.

Explanation: Rural Co-operative Banks shall mean State Co-operative Banks and Central Co-operative Banks, unless specified otherwise, as defined in the National Bank for Agriculture and Rural Development Act, 1981.

vi. “Equity exposures” shall mean exposures of a commercial bank to equity of an investee counterparty as also any exposure as defined in Appendix 1 to these Directions.

vii. “Issue” for the purpose of Chapter IV of these Directions shall mean a specific liability – either a credit facility or a debt instrument – of the issuer.

viii. “Issuer” for the purpose of Chapter IV of these Directions shall mean a counterparty to whom a bank has an exposure.

ix. “Local Government Bodies” shall mean institutions of the local self-governance, which look after the local planning, development and administration of a specified area or community such as villages, towns, or cities.

x. “Member lending Institutions (MLIs)” shall have the same meaning as defined in relevant credit guarantee schemes of the Government of India.

xi. “Micro, Small and Medium Enterprises (MSMEs)” shall mean the enterprises as defined in the MSMED Act, 2006 as amended from time to time.

xii. “Multilateral Development Bank (MDB)” shall mean an institution, created by a group of countries that provides financing and professional advice for economic and social development projects. MDBs have large sovereign memberships and may include both developed countries and/or developing countries. Each MDB has its own independent legal and operational status, but with a similar mandate and a considerable number of joint owners.

xiii. “Non-performing assets (NPAs)” and “Stage 3 assets” shall be as defined in the Reserve Bank of India (Commercial Banks – Asset Classification, Provisioning and Income Recognition) Directions, 2026, as amended from time to time.

xiv. “Object finance” is a form of Specialised Lending under Corporate Exposures, and shall mean the method of funding the acquisition of an equipment (eg ships, aircraft, satellites, railcars, and fleets) where the repayment of the loan is dependent on the cash flows generated by the specific asset(s) that have been financed and pledged or assigned to the lender.

xv. “Operational phase” shall have the same meaning as defined in the Reserve Bank of India (Commercial Banks – Credit Facilities) Directions, 2025.

xvi. “Other Capital Instruments” shall mean capital instruments issued by the investee entity which are not included in Equity exposures as defined in sl. no. (vi) above.

xvii. “Personal loans” shall be as defined in Banking Statistics I (Harmonised Definitions) on the RBI’s website.

xviii. “Pre-operational phase” of a project shall mean the phase before the operational phase.

xix. “Project finance” is a form of Specialised Lending under Corporate Exposures, and shall have the same meaning as defined in the Reserve Bank of India (Commercial Banks – Credit Facilities) Directions, 2025.. In addition, for the purpose of these Directions, a project finance shall also include refinancing of an existing installation, with or without improvements.

xx. “Real Estate” means an immovable property that is land, including agricultural land 5 and forest, or anything treated as attached to land, in particular buildings, in contrast to being treated as movable property.

(xxi) “Residential Real Estate exposure” means an exposure that is secured by a property that has the nature of a dwelling and satisfies all applicable laws and regulations enabling the property to be occupied for housing purposes. Indicative examples of such exposures are exposures secured by houses, apartments, etc.

(xxii) “Specialised lending exposure” for the purpose of risk weights shall mean a lending which possesses some or all of the following characteristics, either in legal form or economic substance:

a. The exposure is not related to real estate and is either a project finance or an object finance.

b. The exposure is typically to an entity (often a special purpose vehicle (SPV)) that was created specifically to finance and/or operate physical assets;

c. The borrowing entity has few or no other significant assets or activities, and therefore little or no independent capacity to repay the obligation, apart from the income that it receives from the asset(s) being financed. The primary source of repayment of the obligation is the income generated by the asset(s), rather than the independent capacity of the borrowing entity; and

d. The terms of the obligation give the lender a substantial degree of control over the asset(s) and the income that it generates.

(xxiii) “Speculative unlisted equity exposures” shall mean equity investments in unlisted companies that are invested for short-term resale purposes (ie. up to one year) or are considered venture capital or similar investments which are subject to price volatility and are acquired in anticipation of significant future capital gains.

Provided that a bank’s investments in unlisted equities of corporate clients arising from debt-equity swaps for restructuring purpose would not be treated as speculative unlisted equity exposures.

(xxiv) “Subordinate Debt” shall mean debt instruments of the issuer which are subordinate in claim to the senior debt.

(xxv) “Transactors” shall mean obligors in relation to facilities such as credit cards and charge cards where the balance has been repaid in full at each scheduled repayment date (including the grace period of three days) for the previous 12 months.

(2) All other expressions, unless defined herein, shall have the same meaning as have been assigned to them under the Banking Regulation Act,1949 or the Reserve Bank of India Act, 1934 or any statutory modification or re-enactment thereto or as used in commercial parlance, as the case may be.

CHAPTER II – GENERAL INSTRUCTIONS

5. General

1. Under the standardised approach (SA), banking book exposures shall be risk weighted either as per the risk weights prescribed for specific categories of exposures or as per the ratings assigned by eligible credit rating agencies (ECRAs), as stipulated in these Directions.

2. Risk weighted assets (RWAs) shall be calculated as the product of the standardised risk weights and the exposure amount. The exposures shall be risk-weighted net of specific provisions (including partial write-offs).

3. Risk weights prescribed under these Directions shall be without prejudice to any action that the Reserve Bank may take relating to specific exposures on account of macroprudential considerations, if any.

4. Mere prescription of risk weights for any exposure shall not be construed as regulatory approval for a specific type of activity, which is otherwise not permitted.

5. The requirements covering the use of external ratings are set out in Chapter IV of these Directions. The credit risk mitigation techniques that are permitted to be recognised under the standardised approach are set out in Chapter V of these Directions.

6. Due diligence requirements

1. The banks shall put in place a system of due diligence to ensure that, (i) they have an adequate understanding, at origination and thereafter on a regular basis (at least annually), of the risk profile and characteristics of the counterparty; and (ii) the risk weights assigned to counterparty is broadly aligned with the bank’s internal credit assessment.

Provided that the due diligence requirements do not apply to exposures to Sovereigns and Central Banks covered under paragraphs 7 and 8 below.

Provided further that, due diligence analysis must never result in the application of a risk weight lower than the applicable base risk weight as per the external credit rating.

2. The sophistication of the due diligence shall be appropriate to the size and complexity of banks’ activities. Banks may give proper consideration to the climate-related financial risks as part of the counterparty due diligence.

(3) For exposures to entities belonging to consolidated groups, due diligence shall be performed at the solo level to which there is a credit exposure. In evaluating the repayment capacity of the solo entity, banks shall take into account the support of the group and the potential for it to be adversely impacted by problems in the group.

(4) Banks shall demonstrate to the supervisor that due diligence has been performed as per the policy approved by the Board.

CHAPTER III – EXPOSURE CLASSES AND RISK WEIGHTS

7. Exposures to Domestic Sovereigns

1. Both fund based and non-fund-based claims on the Central Government shall attract a zero per cent (0%) risk weight. Central Government guaranteed claims shall also attract a zero per cent (0%) risk weight.

2. Direct loan / credit / overdraft exposure, if any, of banks to the State Governments and investments in State Government securities shall attract zero per cent (0%) risk weight. However, claims guaranteed by the State Governments shall attract 20 per cent risk weight.

3. The risk weight applicable to claims on Central Government exposures shall also apply to the claims on the Reserve Bank of India and DICGC.

4. For credit facilities extended under schemes guaranteed by Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), Credit Risk Guarantee Fund Trust for Low Income Housing (CRGFTLIH) and individual schemes under National Credit Guarantee Trustee Company Ltd. (NCGTC) which are backed by an unconditional and irrevocable guarantee provided by Government of India, a zero percent (0%) risk weight shall be applicable to the extent of guarantee coverage subject to the following conditions:

i. Prudential Aspects: The guarantees provided under the respective schemes should comply with the requirements for credit risk mitigation framework covered under Chapter V of these Directions.

ii. Restrictions on permissible claims: Where the terms of the guarantee schemes restrict the maximum permissible claims through features like specified extent of guarantee coverage, clause on first loss absorption by member lending institutions (MLI), payout cap, etc., the zero per cent (0%) risk weight shall be restricted to the maximum permissible claim and the residual exposure shall be subjected to risk weight as applicable to the counterparty in terms of these Directions.

iii. In case of a portfolio-level guarantee, the extent of exposure subjected to first loss absorption by the MLI, if any, shall be subjected to full capital deduction and the residual exposure shall be subjected to risk weight as applicable to the counterparty, on a pro rata basis. The maximum capital charge shall be capped at a notional level arrived at by treating the entire exposure as unguaranteed.

Provided that, any scheme launched on or after September 7, 2022 under any of the aforementioned Trust Funds shall be eligible for zero percent (0%) risk weight only if, (a) it qualifies all the conditions prescribed in paragraph 7(4) (i) to (iii) above; (b) the scheme provides for settlement of the eligible guaranteed claims within thirty days from the date of lodgment; and, (c) the lodgment of claim under such scheme is permitted within sixty days from the date of default.

Some illustrative examples of risk weights applicable on claims guaranteed under specific existing schemes are as follows:

| Scheme name | Guarantee Cover | Risk Weight |

| 1. Credit Guarantee Fund Scheme for Factoring (CGFSF) | The first loss of 10% of the amount in default to be borne by Factors. The remaining 90% (i.e., second loss) of the amount in default will be borne by NCGTC and Factors in the ratio of 2:1 respectively | First loss of 10% amount in default – Full capital deduction

60% amount in default borne by NCGTC- 0% RW. Balance 30% amount in default Counterparty / Regulatory Retail Portfolio (RRP) RW as Applicable Note – The maximum capital charge shall be capped at a notional level arrived by treating the entire exposure as unguaranteed. |

| 2. Credit Guarantee Fund Scheme for Skill Development (CGFSD) | 75% of the amount in default. 100% of the guaranteed claims shall be paid by the Trust after all avenues for recovery have been exhausted and there is no scope for recovering the default amount | Entire amount in default – Counterparty / Regulatory Retail

Portfolio (RRP) RW as applicable. |

| 3. Credit Guarantee Fund for Micro Units (CGFMU) | Micro Loans

The first loss to the extent of 3% of amount in default. Out of the balance, guarantee will be to a maximum extent of 75% of the amount in default in the crystallized portfolio |

First loss of 3% amount in default – Full capital deduction

72.75% of the amount in default – 0% RW, subject to maximum of ({15%∗CP}−C)∗ SLACP Where- CP = Crystallized Portfolio (sanctioned amount) • C = Claims received in previous years, if any, in the crystallized portfolio • SLA = Sanctioned limit of each account in the crystallized portfolio • 15 per cent represents the payout cap Balance amount in default – Counterparty / RRP RW as applicable. Note – The maximum capital charge shall be capped at a notional level arrived by treating the entire exposure as unguaranteed. |

| 4.CGTMSE guarantee coverage for Micro-Enterprises | Up to ₹5 lakh

85% of the amount in default subject to a maximum of ₹4.25 lakh Above ₹5 lakh & up to ₹50 lakh 75% of the amount in default subject to a maximum of ₹37.50 lakh Above ₹50 lakh & up to ₹200 lakh 75% of the amount in default subject to a maximum of ₹150 lakh |

Guaranteed amount in default – 0% RW*

Balance amount in default – Counterparty / RRP RW asapplicable. |

| *In terms of the payout cap stipulations of CGTMSE, claims of the member lending institutions will be settled to the extent of 2 times of the fee including recovery remitted during the previous financial year. However, since the balance claims will be settled in subsequent year / s as the position is remedied, the entire extent of guaranteed portion may be assigned zero percent risk weight. | ||

Note: The regulatory stipulation in paragraph 7(4) above shall be applicable to a bank to the extent it is recognised as an eligible MLI under the respective schemes.

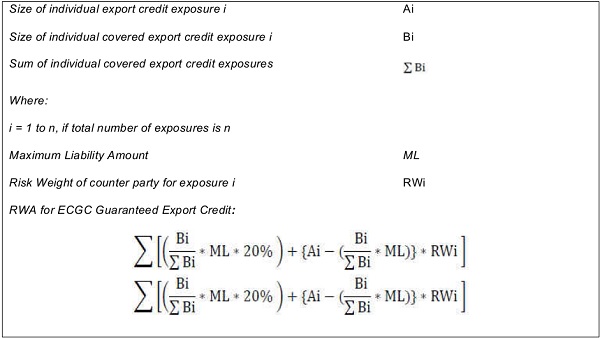

5. The claims on Export Credit Guarantee Corporation of India (ECGC) shall attract a risk weight of 20 per cent.

6. The above risk weights for both direct claims and guaranteed claims shall be applicable as long as they are classified as ‘standard’ / performing assets. Where such Central Government guaranteed exposures are classified as non-performing and / or Stage 3, they shall attract risk weights as prescribed in paragraph 17.

(7) The risk weights prescribed under paragraphs 7(1) to 7(5) shall be applied only if such exposures are denominated in Indian Rupees and also funded in Indian Rupees.

8. Exposures to Foreign Sovereigns and Foreign Central Banks

1. Exposures to foreign sovereigns and foreign central banks shall attract risk weights as per the ratings assigned to those sovereigns / sovereign claims and Central Banks / Central Bank claims by international credit rating agencies as follows:

Table 1: Risk weight table for sovereigns and central banks

| S&P*/ Fitch rating category |

AAA to AA |

A | BBB | BB to B |

Below B |

Unrated |

| Moody’s rating category |

Aaa to Aa3 |

A1 to A3 | Baa1 toBaa3 |

Ba1 to B3 |

Below B3 |

Unrated |

| Risk weight

(%) |

0 | 20 | 50 | 100 | 150 | 100 |

* Standard & Poor’s

Note: The modifiers “+” or “-” have been subsumed with the main rating category.

Illustration: The risk weight assigned to an investment in US Treasury Bills by overseas branch of an Indian bank in Paris, irrespective of the currency of funding, shall be determined by the rating assigned to the Treasury Bills, as indicated in Table 1 above.

2. If a foreign jurisdiction has exercised its national discretion to allow its banks to risk weight their domestic currency exposures to their sovereign and central bank lower than what is accorded as per the external ratings in Table 1, then Indian banks can also use the same risk weight for similar exposures in those jurisdictions, provided that such exposures are funded in the same currency. However, in case a Host Supervisor requires a more conservative treatment to such claims in the books of the Indian banks, they shall adopt the requirements prescribed by the Host Country supervisors for computing capital adequacy.

Provided that in cases where a foreign jurisdiction has exercised its discretion to treat its regional governments as equivalent to sovereign for capital adequacy purposes, the risk weights assigned to exposures of banks to such regional governments shall be subject to a floor as follows:

i. In case such regional governments have revenue raising powers and have specific institutional arrangements the effect of which is to reduce their risk of default, the risk weights shall not be less than the risk weights as per the rating of the foreign sovereign as per Table 1.

ii. In case such regional governments do not have revenue raising powers, the risk weights shall not be less than the risk weights as per the rating of the foreign sovereign as per Table 2:

Table 2: Risk weight floors for foreign regional governments, which do not have revenue raising powers, and treated as sovereign by the foreign jurisdiction

| External | AAA to | A to | BBB to | BB to | Below | Unrated |

| rating category of the sovereign |

AA | A | BBB | B | B | |

| Risk weight (%) | 20 | 50 | 100 | 100 | 150 | 100 |

9. Exposures to Public Sector Entities (PSEs)

Exposures to public sector entities and local government bodies – both domestic and foreign – shall be risk weighted in a manner similar to claims on Corporates as per paragraph 12.

10. Exposures to MDBs, BIS and IMF

(1) Exposures to the Bank for International Settlements (BIS), the International Monetary Fund (IMF) and the following eligible Multilateral Development Banks (MDBs), as updated from time to time, shall be assigned a uniform zero percent (0%) risk weight:

i. World Bank Group: IBRD and IFC, MIGA and IDA,

ii. Asian Development Bank,

iii. African Development Bank,

iv. European Bank for Reconstruction and Development,

v. Inter-American Development Bank,

vi. European Investment Bank,

vii. European Investment Fund,

viii. Nordic Investment Bank,

ix. Caribbean Development Bank,

x. Islamic Development Bank,

xi. Council of Europe Development Bank,

xii. International Finance Facility for Immunization (IFFIm), and

xiii. Asian Infrastructure Investment Bank (AIIB)

(2) Exposures to all other MDBs shall be risk weighted as per the rating assigned by the international credit rating agencies as under:

Table 3: Exposures to other MDBs

| S&P/ Fitch rating category |

AAA to AA |

A | BBB | BB to B | Below B | Unrated |

| Moody’s rating category |

Aaa to Aa3 |

A1 to A3 |

Baa1 to Baa3 |

Ba1 to B3 |

Below B3 | Unrated |

| Risk weight (%) | 20 | 30 | 50 | 100 | 150 | 50 |

11. Exposures to Banks

(1) Exposures covered under this paragraph include all exposures of banks to their counterparty banks, excluding exposures in equity, capital instruments and subordinated debt instruments which are covered in paragraph 13 of these Directions. Banks shall assign to their rated bank exposures, the “base” risk weights based on the external ratings according to Table 4.

Explanation: As specified in paragraph 4(1)(v) above, “Counterparty banks” shall also include All India Financial Institutions (AIFIs).

Table 4: Exposures to Banks (Incorporated in India or outside), Foreign Bank branches in India and WOS of foreign banks in India

| External ratingcategory of counterparty |

AAA to AA |

A | BBB | BB to B | Below B |

Unrated |

| “Base”risk weight (%) | 20 | 30 | 50 | 100 | 150 | 100 |

| Risk weight for short-term exposures (%) | 20 | 20 | 20 | 50 | 150 | 50 |

Explanation: External ratings of the parent bank may be considered as rating of foreign bank operating in branch mode for risk weight purposes.

2. Exposures to banks with an original maturity of three months or less, as well as exposures to banks that arise from the movement of goods across national borders with an original maturity of six months or less, can be assigned a risk weight that correspond to the risk weights for short term exposures in Table 4. Other short-term claims shall be risk weighted as given in Table 23 or 24, as the case may be.

Explanation: The exposures to banks that arise from the movement of goods across national borders may include on-balance sheet exposures such as loans and off-balance sheet exposures such as self-liquidating trade-related contingent items.

3. Such exposures of the Indian branches of foreign banks, which are guaranteed / counter-guaranteed by their overseas Head Offices (HO) or the bank’s branch in another country, shall amount to a claim on the parent foreign bank, and shall also attract the risk weights as per Table 4. However, if the bank branch having such exposure decides to reckon the exposure on the original counterparty instead of on its HO, then the exposure shall attract the risk weight as applicable to the counterparty as per these Directions.

4. To reflect transfer and convertibility risk under unrated exposures, a risk-weight floor based on the risk weight applicable to exposures to the sovereign of the country where the bank counterparty is incorporated shall be applied to the risk weight assigned to bank exposures. The sovereign floor applies when: (i) the exposure is not in the local currency of the jurisdiction of incorporation of the debtor bank; and (ii) for a borrowing booked in a branch of the debtor bank in a foreign jurisdiction, when the exposure is not in the local currency of the jurisdiction in which the branch operates. The sovereign floor shall not apply to short-term (i.e. with a maturity below one year) self-liquidating, trade-related contingent items that arise from the movement of goods.

12. Exposures to Corporates

(1) Scope

i. Exposures to corporates include exposures (loans, bonds, receivables, etc.) to incorporated entities, associations, partnerships, Limited Liability Partnerships (LLPs), proprietorships, trusts, funds and other entities with similar characteristics.

Explanation: Exposures include all fund based and non-fund based exposures other than those which qualify for inclusion under ‘sovereign’, ‘bank/AIFIs’, ‘regulatory retail’, ‘real estate’, ‘non-performing assets / Stage 3 assets’, or any other specified category addressed separately in these Directions.

ii. This exposure class also includes exposures to securities firms, primary dealers, NBFCs, insurance companies and other financial institutions not covered under paragraph 11. The corporate exposure class shall not include exposures to individuals and exposures to micro, small and medium enterprises (MSMEs) meeting the criteria prescribed under paragraphs 14 and 15.

iii. Notwithstanding above, exposures to corporates classified as capital market exposure shall be risk weighted as prescribed in paragraph 19 of these Directions.

iv. Exposures to Subordinate debt, equity and other capital instruments of corporates are covered under paragraph 13 of these Directions.

v. Exposures to Corporates fully secured by real estate, either as primary security or collateral or both, shall be risk weighted as prescribed for real estate exposure class in paragraph 16 of these Directions.

(2) The corporate exposure class differentiates between the following subcategories:

i. General Corporate Exposures

ii. Specialised Lending Exposures

(3) General Corporate Exposures

Exposures to corporates shall be assigned risk weights as per the “base” risk weights in Tables 5 and 6 below, adjusted for the average one-year ODR for each rating category published by the respective ECRAs, as specified in Chapter IV of these Directions.

Table 5: Long Term Claims on Corporates – Base Risk Weights

| External rating category of counterparty |

AAA and AA | A | BBB | BB | Below BB |

Unrated |

| Base risk weight (%) | 20 | 50 | 75 | 100 | 150 | 100 |

Table 6: Short Term Claims on Corporates – Risk Weights

| External rating category of counterparty |

A1+ | A1 | A2 | A3 | A4 & D | Unrated |

| Base risk weight (%) | 20 | 20 | 50 | 100 | 150 | 100 |

Note:

a. No claim on an unrated corporate may be given a risk weight preferential to that assigned to its sovereign of incorporation.

b. All unrated claims on corporates (including those categorized as MSMEs) and NBFCs, except specialized lending exposures in terms of paragraph 12 (4) below, having aggregate exposure from banking system of more than ₹500 crore, will attract a risk weight of 150 per cent.

c. Notwithstanding (b) above, banks may assign risk weights to such unrated exposures based on the issuer rating or another issue-specific rating of the same counterparty (excluding NBFC-CIC), in terms of Chapter IV of these Directions.

d. NBFC-CICs shall always be risk weighted at 100 per cent.

(4) Specialised Lending Exposures

(i) Corporate exposures in the form of Specialised Lending, i.e., either a Project Finance or an Object Finance, and where issue-specific ratings are not available, shall be risk-weighted according to this sub-paragraph.

ii. For the purpose of risk-weighting, projects shall be classified under: (a) Preoperational phase, or (b) Operational phase.

iii. Specialised lending exposures, where issue-specific external ratings are available, shall be assigned risk weights according to paragraph 12(3), i.e., as per the “base” risk weights in Tables 5-6, adjusted for the one-year ODR for each rating category published by the respective ECRAs, as specified in Chapter IV of these Directions.

iv. Specialised lending exposures where the activity is related to real estate shall be treated like a real estate exposure class for the purpose of risk weights.

v. Issuer ratings or rating of an issue of a counterparty in which the bank does not have an exposure shall not be used in the case of specialised lending exposures. Specialised lending exposures for which an issue-specific external rating is not available shall be risk weighted as per the Table 7 below:

Table 7: Corporate exposures classified as Specialised Lending (not related to real estate) – Risk Weights

| Specialised lending subcategory → |

Object finance | Project Finance | ||

| Pre- operational phase |

Operational phase | |||

| Non-High Quality Projects |

High Quality Projects |

|||

| Risk weight (%) | 100 | 130 | 100 | 80 |

vi. Operational Phase of Project Finance: The risk weights of 100 per cent or 80 per cent, as the case may be, as per Table 7 shall be applicable for operational phase only if the borrower entity has (a) a positive net cash flow that is sufficient to cover any remaining contractual obligation, and (b) started repayment of interest and principal dues. Till both the conditions are achieved, the risk weight shall continue at 130 per cent even under operational phase.

vii. During the operational phase, a project that is able to meet its financial commitments in a timely manner and its ability to do so is assessed to be robust against adverse changes in the economic cycle and business conditions will be classified as High Quality Projects. Such projects, on meeting the following criteria

in addition to the conditions specified in the paragraph 12(4)(vi), shall attract a favourable risk weight of 80 per cent as per Table 7:

a. The infrastructure project has completed at least one year of operations post achievement of the date of completion of commercial operations, without breach of any material covenants stipulated by the lenders;

b. The borrower entity is restricted from acting to the detriment of the creditors through suitable covenants, e.g., being restricted from issuing additional debt without the consent of existing creditors;

c. The borrower entity has sufficient reserve funds or other financial arrangements to cover the contingency funding and working capital requirements of the project;

d. The revenues are availability-based or subject to a rate-of-return regulation or take-or-pay contract. For instance, annuities under build-operate-transfer (BOT) model in respect of road/ highway projects and toll collection rights, where there are provisions to compensate the project sponsor if a certain level of traffic is not achieved, and banks’ right to receive annuities and toll collection rights is legally enforceable and irrevocable;

e. The borrower’s revenue depends on rights granted under concession / contract by the Central Government, a State Government, a public sector entity, or a statutory or regulatory body, or a corporate entity with a risk weight of 80 per cent or lower and the contractual provisions provide for protection of these rights for the entire period of concession/ contract as long as the borrower fulfils its obligations under the contract;

f. The concession / contractual provisions provide for a high degree of protection for a lender, which shall, at a minimum, include: (i) provisions of an escrow / Trust and Retention Account mechanism for ringfencing the cash flows; (ii) pari-passu charge in favour of the lender over all movable and immovable assets; and (iii) mitigation of risk for lenders in case of early termination (eg. step-in rights for the lenders, minimum termination payments etc).

Explanation:

I. Availability-based revenues mean that once construction is completed, the project finance entity is entitled to payments from its contractual counterparties (eg the government), as long as contract conditions are fulfilled.

II. Rate of return regulation is a form of price setting regulation where government

or an authority determines the fair price allowed to be charged by a public utility.

III. Take or pay contracts between a buyer and a seller of good and/or services mandate buyers to either accept the pre-determined quantity of goods/services at a pre-determined price or pay a penalty, ensuring risk-sharing between suppliers and buyers.

13. Exposures to Subordinated Debt, Equity and Other Capital Instruments

(1) Scope

i. Exposures for which this paragraph would apply shall include subordinate debt, equity and other regulatory capital instrument issued by counterparty banks and corporates. Corporates for this purpose are as defined in paragraph 12.

ii. Exposures shall exclude instruments deducted from the regulatory capital of the investing bank or investments which are required to be risk weighted at 250 per cent as per Chapter III of the Reserve Bank of India (Commercial Banks – Prudential Norms on Capital Adequacy) Directions, 2025, as amended from time to time, and banks’ equity investment in funds as prescribed in paragraph 18 of these Directions.

(2) The following risk weights shall be applicable for such exposures:

Table 8 – Exposures to Subordinated debt, equity and other capital instruments – Risk Wights

| Exposure Type → | Equity Exposures | Speculative Unlisted Equity |

Subordinate debt and other Capital Instruments |

| Risk Weight (%) | 250 | 400 | 150 |

(3) All investments in the paid-up equity of non-financial entities (other than subsidiaries) which exceed 10 per cent of the issued common share capital of the issuing entity or where the entity is an unconsolidated affiliate as defined in paragraph 28(8)(ii)(c)(i) of the Reserve Bank of India (Commercial Banks – Prudential Norms on Capital Adequacy) Directions, 2025shall receive a risk weight of 1250 per cent. Equity investments equal to or below 10 per cent paid-up equity of such investee companies shall be assigned a risk weight as per Table 8 above.

14. Retail Exposures

1. Claims (including both fund-based and non-fund based) that meet all the four criteria listed below in paragraph 14(3) shall be considered as retail claims for regulatory capital purposes and included in a regulatory retail portfolio.

2. Claims included in regulatory retail portfolio shall be assigned a risk weight of 75 per cent.

3. Qualifying Criteria for regulatory retail portfolio:

i. Orientation Criterion: The exposure (both fund based and non-fund based) is to an individual person or persons or to small business. A person under this clause shall mean any non-commercial entity capable of entering into contracts and shall include but not be restricted to individual and HUF.

Explanation: Small business for this purpose would include an MSME or any other business entity having a turnover equal to or less than ₹500 crore. If such MSME or business entity is affiliated to another business entity, then the turnover criteria of equal to or less than ₹500 crore shall be qualified at the Group level.

ii. Product criterion: The exposure (both fund and non-fund based) takes the form of any of the following: revolving credits and lines of credit (including credit cards which qualify as transactors), term loans and leases (e.g. instalment loans and leases), commitments and facilities for small businesses and student and educational loans.

iii. Low value of individual exposures: The maximum aggregated exposure to one counterparty cannot exceed an absolute threshold of ₹10 crore.

iv. Granularity criterion: Banks must ensure that the regulatory retail portfolio is sufficiently diversified to a degree that reduces the risks in the portfolio, warranting the 75 per cent risk weight. No aggregated exposure to one counterparty can exceed 0.2 per cent of the overall regulatory retail portfolio. While banks may appropriately use the group exposure concept for computing aggregated exposures, they should evolve adequate systems to ensure strict adherence with this criterion. NPAs under retail loans are to be excluded from the overall regulatory retail portfolio when assessing the granularity criterion for risk weighting purposes.

Explanation:

I. ‘Aggregated exposure’ in this context means gross amount (i.e. not taking any benefit for credit risk mitigation into account) of all forms of retail exposures excluding residential real estate exposures.

II. ‘One counterpart’ means one or several entities that may be considered as a single beneficiary (e.g. in the case of a MSME that is affiliated to another MSME, the limit shall apply to the bank’s aggregated exposure on both businesses).

III. To apply the 0.2 per cent threshold of the granularity criterion, banks must: first, identify the full set of exposures in the retail exposure class (as defined by the orientation criterion in paragraph 14(3)(i)); second, identify the subset of exposure that meet product criterion and do not exceed the threshold for the value of aggregated exposures to one counterparty; and third, exclude any exposures that have a value greater than 0.2 per cent of the subset before exclusions.

(4) The following claims, both fund-based and non-fund-based, shall be excluded from the regulatory retail portfolio:

i. Personal Loans (excluding education loans meeting regulatory retail criteria);

ii. Credit card receivables other than those which qualify as transactors;

iii. Capital Market Exposures;

iv. Derivative exposures;

v. Real Estate Exposures as per paragraph 16 of these Directions;

vi. Loans and Advances to bank’s own staff which are fully covered by superannuation benefits and / or mortgage of flat/ house.

(5) For the purpose of ascertaining compliance with the absolute threshold, exposure shall mean sanctioned limit or the actual outstanding, whichever is higher, for all fund based and non-fund based facilities, including all forms of off-balance sheet exposures. In the case of term loans and EMI based facilities, where there is no scope for redrawing any portion of the repaid amount, exposure shall mean the actual outstanding.

6. The risk weight assigned to the retail portfolio would be evaluated with reference to the default experience for these exposures. As part of the supervisory review process, an assessment would be made on whether the credit quality of regulatory retail claims held by individual banks should warrant a standard risk weight higher than 75 per cent.

7. “Other retail” exposures to individuals not meeting the criteria of regulatory retail portfolio in paragraph 14(3) shall be risk-weighted as follows:

i. Personal loans (other than education loans meeting the regulatory retail criteria and transactor credit card receivables, loans fully secured by real estate, vehicle loans, and microfinance loans), shall attract a risk weight of 125 per cent;

ii. Loans to individuals that are fully secured by real estate, either as primary security or collateral or both, shall be risk weighted as prescribed in real estate asset class under paragraph 16.

iii. Credit card receivables other than those which qualify as transactors under regulatory retail portfolio asset class shall attract a risk weight of 125 per cent;

iv. Exposures to individuals that are classified as ‘capital market exposures’ shall attract a 125 per cent risk weight;

v. Exposures in respect of personal loans secured by gold and gold jewellery shall be worked out under the comprehensive approach as per Chapter V. The ‘exposure value after risk mitigation’ shall attract the risk weight of 125 per cent.

vi. Microfinance loans that are in the nature of consumer credit and are not eligible for classification under ‘regulatory retail’ shall attract a risk weight of 100 per cent.

vii. All other credit exposure to individuals shall attract a risk weight of 100 per cent, unless specified otherwise.

15. Exposure to Micro, Small and Medium Enterprises (MSMEs)

(1) Exposures to MSMEs shall be risk weighted as follows:

(i) Exposures to MSMEs fully secured by real estate, either as primary security or collateral or both, shall be risk weighted as prescribed in real estate asset class under paragraph 16.

ii. Exposures to MSMEs that are classified as capital market exposure shall be risk weighted as per paragraph 19(1).

iii. Rated exposures to MSMEs shall be risk weighted as per paragraph 12(3) of these Directions.

iv. Unrated exposures to MSMEs shall be risk weighted as follows:

v. Unrated exposure to MSMEs that meet the criteria of regulatory retail portfolio given in paragraph 14(3) shall be risk weighted at 75 per cent.

vi. Other unrated exposures to MSMEs not meeting the regulatory retail criteria exposures shall be risk weighted at 85 per cent.

Provided that unrated capital market exposures and specialised lending exposures to MSMEs shall be risk weighted as per paragraphs 19(1) and 12(4), respectively.

Provided further that unrated exposures to MSMEs (excluding specialised lending exposures under Corporate Exposures) having aggregate exposure from banking system of more than ₹500 crore shall attract a risk weight of 150 per cent.

(2) The Reserve Bank may increase the standard risk weight for unrated MSME claims where a higher risk weight is warranted by the overall default experience. As part of the supervisory review process, the Reserve Bank would also consider whether the credit quality of unrated MSME claims held by individual banks should warrant a standard risk weight higher than 85 per cent.

16. Real Estate Exposures

(1) General Conditions: Real estate exposures of a bank shall be subject to the following general conditions:

(i) Underwriting Policies: For exposures that qualify for real estate exposure asset class, banks shall put in place underwriting policies with respect to the granting of mortgage loans that include the assessment of the ability of the borrower to repay. Underwriting policies must define metric(s) (such as the loan’s debt service coverage ratio, debt service-to-income ratio) and specify its (their) corresponding relevant level(s) to conduct such assessment. Underwriting policies must also be appropriate when the repayment of the mortgage loan depends materially on the cash flows generated by the property, including relevant metrics (such as an occupancy rate of the property and likely income).

(ii) Value of the property: Banks shall put in place a policy for valuation of properties accepted as security for their exposures. The valuation shall be appraised independently using prudently conservative valuation criteria. To ensure that the value of the property is appraised in a prudently conservative manner, the valuation must exclude expectations on price increases and must be adjusted to take into account the potential for the current market price to be significantly above the value that shall be sustainable over the life of the loan. Valuations shall be made as specified in the Reserve Bank of India (Commercial Banks – Credit Risk Management) Directions, 2025, taking into account inter alia the valuation standards notified by Central Government (viz. Companies (Registered Valuers and Valuation) Rules, 2017). If a market value can be determined, the valuation should not be higher than the market value.

Explanation:

a. The valuation must be done independently from the bank’s mortgage acquisition, loan processing and loan decision process. The valuation done by a bank’s empanelled independent valuer in terms of the Reserve Bank of India (Commercial Banks – Credit Risk Management) Directions, 2025 shall deem to comply with this requirement.

b. In the case where the mortgage loan is financing the purchase of the property, the value of the property for LTV purposes shall not be higher than the effective purchase price. The effective purchase price for this purpose shall be the cost of housing property as per the Chapter VIII of the Reserve Bank of India (Commercial Banks – Credit Facilities) Directions, 2025.

(iii) The bank is expected to monitor the value of the collateral at least once in three years. More frequent monitoring is suggested where the market is subject to significant changes in conditions. Statistical methods of evaluation may be used to update estimates or to identify collateral that may have declined in value and that may need re-appraisal. A qualified professional valuer must evaluate the property when information indicates that the value of the collateral may have declined materially relative to general market prices or when exposures are classified as NPA and / or Stage 3.

(iv) LTV ratio: LTV ratio shall be computed as a percentage of ‘total loan outstanding’ in the numerator and the ‘realisable value’ of the residential property mortgaged to the bank in the denominator. For this purpose:

a. ‘total loan outstanding’ shall include the funded outstanding and any undrawn committed amount in the account (viz. “principal + accrued interest + other charges pertaining to the loan”) gross of any provisions and other risk mitigants, except for pledged deposit accounts with the lending bank that meet all requirements for on-balance sheet netting and have been unconditionally and irrevocably lien-marked for the sole purposes of redemption of the mortgage loan.

Explanation: If a bank grants multiple loans secured by the same property and they are sequential in ranking order (i.e. there is no intermediate lien from another bank), the multiple loans should be considered as a single exposure for risk-weighting purposes, and the amount of the loans should be added to calculate the LTV.

b. Value of the property shall be reckoned at the value measured at origination unless the value of the property has been revised downwards (as per the bank’s policy on periodic valuation of the property). These downward valuations need to be considered for LTV computation. If the value has been adjusted downwards, a subsequent upwards adjustment can be made but not to a higher value than the value at origination. The value of the property should be adjusted if an extraordinary event occurs resulting in permanent reduction of the property value. Modifications made to the property that unequivocally increase its value could also be considered in the LTV. Moreover, the value of the property must not depend materially on the performance of the borrower.

c. Notwithstanding the requirements in Sl. No. iv(b) above, upward revision in the value of property shall be permitted for the purpose of LTV after at least five years from the date of start of the loan repayment or the date of possession of the finished property by the borrower, whichever is later, based on a fresh valuation obtained by the bank for the purpose of extending a new or additional loan secured by the same property. Subsequent upward re- valuation of the property as a part of additional loan applications shall be after at least five years from the date of any previous revaluation.

(2) Qualifying conditions: Real estate exposure shall also meet the following criteria:

i. Legal enforceability: Bank’s claim on the mortgaged property must be legally enforceable. The loan agreement and the legal process underpinning it must be such that they provide for the bank to realise the value of the property within a reasonable time frame.

ii. Claims over the property: A single bank has an absolute claim or multiple banks have first pari-passu claims over the property, subject to the condition that: (a) there is an inter-creditor agreement or any other arrangements among the banks detailing the sequence of claims of individual banks over the property, (b) each bank’s loan should be fully secured by the current value of the property, either as primary security or as collateral or both, and is within the permissible LTV limit, failing which risk weights under Table 16 or 17, as applicable, shall apply.

iii. Ability of the borrower to repay: Repayment capacity of the borrower shall invariably be assessed irrespective of the value of the property and the borrower must meet the requirements set according to paragraph 16(1)(i).

iv. Prudent value of property: The property must be valued according to the criteria in paragraphs 16(1)(ii) and 16(1)(iii) for determining the value in the LTV ratio. Moreover, the valuation of the property must not depend on the credit worthiness of the borrower.

v. Required documentation: All the information required at loan origination and for monitoring purposes must be properly documented, including information on the ability of the borrower to repay and on the valuation of the property.

(3) Application of credit risk mitigation: A guarantee or financial collateral may be recognised as a credit risk mitigant in relation to exposures secured by real estate if it qualifies as eligible collateral under the credit risk mitigation framework as detailed in Chapter V of these Directions. This may include mortgage guarantee if it meets the operational requirements of the credit risk mitigation framework for a guarantee. Banks may recognise these risk mitigants in calculating the exposure amount; however, the LTV bucket and risk weight to be applied to the exposure amount must be determined before the application of the appropriate credit risk mitigation technique.

Explanation: A bank’s use of mortgage guarantee should mirror the FSB Principles for sound residential mortgage underwriting (April 2012).

(4) Categories of Real Estate Exposures

The real estate exposure asset class shall consist of:

i. Housing Loans to Individuals

ii. Commercial Real Estate – Acquisition, Development and Construction Exposures – CRE(ADC)

iii. Other Claims secured by Real Estate

(5) Housing Loans to Individuals

(i) Housing loans to individuals shall be for construction or acquisition of housing units and shall consist of the following exposures:

a. loans to individuals for purchase of a plot of land for construction of residential property;

b. loans to individuals secured by under-construction residential property on their existing plot of land for completion of construction;

c. loans to the individual members of registered associations or co-operative housing societies for construction of residential houses for the members as per the bye-laws of the society under the relevant Act;

d. loans to individuals for purchase of under-construction dwelling units in: projects registered with a relevant Real Estate Regulatory Authority (RERA) under the Real Estate (Regulation and Development) Act 2016, or other projects where registration with a RERA is not mandatory under the Act.

e. loans to individuals for acquisition of ready-built dwelling units.

Provided that:

i. in above cases (a) to (c), the construction shall start within a year and shall finish in maximum five years from the date of first disbursement as per the loan agreement with the bank, and wherever applicable, bye-laws of the Society.

ii. In case of (d), the construction shall be completed as per the terms and conditions of registration granted by the RERA in projects having mandatory registration with RERA. In cases of projects not requiring mandatory registration with RERA, the construction shall start within a year and shall finish in maximum five years from the date of first disbursement as per the loan agreement with the bank.

iii. In all the above cases, the property shall satisfy all the applicable laws and regulations enabling the property to be occupied for housing purposes upon completion

Explanation: Housing loans to individuals shall also include loans for carrying out alterations, additions, or repairs to a residential unit. Such loans must be supported by an estimate of the proposed work, stage wise disbursement based on the progress of construction, and periodic review of the construction progress by the bank.

(ii) Risk weights for housing loans to individuals:

a. Housing loans to individuals for up to two housing loans (shall include all existing as well as fresh loans, but shall exclude fully repaid loans), which shall be treated as their primary residences, shall attract the following risk weights as per the ceilings of LTV ratio prescribed subject to compliance of qualifying conditions mentioned at paragraph 16(2):

Table 9 – Housing Loans to Individuals – Up to two loans

| LTV | ≤ 50% | >50% to ≤ 60% | > 60% to ≤ 80% | > 80% to ≤ 90% |

| Risk weight (%) | 20 | 25 | 30 | 40 |

b. Risk weights on the third housing loan onward to individuals (excluding fully repaid loans) shall be as per the ceilings of LTV ratios given in the following Table subject to compliance of qualifying conditions mentioned at paragraph 16(2):

Table 10 – Housing Loans to Individuals – Third loan onward

| LTV | ≤ 50% | >50% to ≤ 60% | > 60% to ≤ 80% | > 80% to ≤ 90% |

| Risk weight (%) | 30 | 35 | 45 | 60 |

Explanation:

1. Co-applicant(s) shall also be included while counting the number of housing loans.

2. Number of housing loans shall be computed at the banking system level.

c. In both the above cases, an additional five percentage points of risk weight would be applicable if ‘total loan outstanding’ computed in terms of paragraph 16(1)(iv)(a) is ₹3 crore or above.

d. If the timelines specified in proviso i. to paragraph 16(5)(i) are not met, a risk weight of 150 per cent shall apply till the exposure remains in breach of the prescribed covenants.

(6) Commercial Real Estate Exposures – Acquisition, Development and Construction – CRE (ADC)

i. Loans to commercial entities (including proprietorship firms and HUFs) for acquisition (wherever permitted) and development of land, and / or construction of commercial or residential real estate projects where the repayment is dependent on the underlying property such as renting, leasing the units or; selling the units of the project; selling the complete, or part of, the project, etc. shall be classified as CRE(ADC) exposures.

ii. Such loans for construction of residential complexes or integrated projects (residential plus commercial) having at least 90 per cent Floor Space Index for residential real estate, and which meet all the following criteria, shall be sub-classified as CRE-RH (ADC) (Commercial Real Estate – Residential Housing (ADC)):

a. All conditions stipulated in paragraph 16(2);

b. The project should be registered with the relevant RERA, wherever the registration is mandatory under the Real Estate (Regulation and Development) Act;

c. The upfront contribution by the borrower, excluding any payment received from prospective homebuyers, shall be not less than 25 per cent of the total cost of the project. Without prejudice to the restrictions contained in Chapter VIII of the Reserve Bank of India (Commercial Banks – Credit Facilities) Directions, 2025, it is clarified that the cost of project shall be inclusive of the cost of the land, which shall be reckoned at higher of Purchase price or Circle rate.

d. Risk Weights: The following RWs shall be applicable on CRE(ADC) exposures: 31

Table 11 – Commercial Real Estate Exposures (ADC)

| Category | CRE-RH (ADC) | Other CRE (ADC) |

| Risk weight (%) | 100 | 150 |

(7) Other Claims secured by Real Estate

i. All other loans not categorised as either housing loans to individuals or CRE-ADC shall be classified under this category, including loans to commercial entities (including proprietorship firms and HUFs) against the security of existing real estate assets or for acquisition of real estate properties for business and other permissible purposes; loans against semi-finished or unfinished properties; and personal loans to individuals against their existing properties. Further, exposures classified under Capital Market Exposure but secured by existing real estate assets shall attract a risk weight treatment provided under paragraph 19(1).

ii. An exposure with multiple items of collateral can be split, according to the ratio of the values of the residential property and the commercial property, into separate exposures secured by residential real estate and commercial real estate, with the applicable risk weights as per the source of repayment. Both on- and off-balance sheet elements of such exposure should be split according to the same ratio.

iii. Apart from qualifying the General Conditions for real estate exposures as in paragraph 16(1), such loans shall also be underwritten for the purposes for which they are granted.

iv. Risk weights: The following RWs shall be applicable on such loans:

(a) Loans against, and for acquisition of, finished residential properties which qualify the conditions given in paragraph 16(2), and where the repayment is envisaged from the cash flow generated from the economic activity for which loan is taken, shall qualify for the following RWs:

Table 12 – Claims secured by residential properties – Repayment from economic activity

| LTV | ≤ 50% | >50% to ≤ 60% | > 60% to ≤ 80% | > 80% to ≤ 90% |

| Risk Weight

(%) |

20

|

25

|

30

|

40

|

b. Loans against, and for acquisition of, finished residential properties which qualify the conditions given in paragraph 16(2), and where the repayment is primarily envisaged from the rent / lease / prospective sale of the underlying property and not from cash flow generated from the economic activity for which the loan is taken, shall qualify for the following RWs:

Table 13 – Claims secured by residential properties – Repayment primarily from underlying property

| LTV | ≤ 50% | >50% to ≤ 60% | > 60% to ≤ 80% | > 80% to ≤ 90% | > 90% to ≤ 100% |

| Risk Weight (%) | 30 | 35 | 45 | 60 | 75 |

Explanation: The condition that repayment is primarily from the rent / lease / prospective sale of the underlying property shall mean that such cash flows from the property securing the loan is more than 50 per cent of the periodic loan servicing amount.

c. Loans against, and for acquisition of, finished commercial properties which qualify the conditions given in paragraph 16(2), and where the repayment is envisaged from the cash flow generated from the economic activity for which the loan is taken, shall qualify for the following RWs:

Table 14 – Claims secured by commercial properties – Repayment from economic activity

| LTV | ≤ 60% | > 60% |

| Risk Weight (%) | Lower of 60% or RW for the Counterparty |

RW for the Counterparty |

d. Loans against, and for acquisition of, finished commercial properties which qualify the conditions given in paragraph 16(2), and where the repayment is primarily envisaged from the rent / lease / prospective sale of the underlying property and not from the cash flow generated from the economic activity for which the loan is taken, shall qualify for the following RWs:

Table 15 – Claims secured by commercial properties – Repayment primarily from underlying property

| LTV | ≤ 60% | > 60% to ≤ 80% | > 80% to ≤ 100% |

| Risk Weight (%) | 70

|

90

|

110

|

e. Loans against semi-finished/unfinished residential or commercial properties, plots of land, and/or which do not qualify all the conditions given in paragraph 16(2), which are already owned by the borrower, and where the repayment is envisaged from the cash flow generated from the economic activity for which loan is taken, shall qualify for the following RWs:

Table 16 –Claims secured by Other Real Estate – Repayment from economic activity

| Counterparty Type → | Individuals | MSME | Others |

| Risk Weight (%)

|

75 (for loans meeting qualifying criteria for regulatory retail as per paragraph 14(3)) or 125 (for other loans) | Lower of 85 or Risk Weight applicable to counterparty |

Risk Weight applicable to the counterparty |

f. Loans against semi-finished residential or commercial properties, plots of land, and/or properties which do not qualify all the conditions given in paragraph 16(2), which are already owned by the borrower, and where the repayment is primarily envisaged from the rent / lease / prospective sale of the underlying property and not from cash flow generated from the economic activity for which the loan is taken, shall qualify for the following RWs:

Table 17 – Claims secured by Other Real Estate – Repayment primarily from underlying property

| Risk Weight (%) | 150 |

(g) Loans for construction on existing land for business purposes, where the repayment arises from cash flows of the business, shall attract risk weights as per Table 16.

Explanation: The above categories (a) to (f) above will also include personal loans to individuals against their existing properties. In cases of personal loans where repayment is not envisaged from the rent / lease / prospective sale of the underlying property but from other sources, shall attract the RWs as per Tables 12, 14 or 16, as the case may be. In cases where repayment of such personal loans would depend on rent / lease / prospective sale of the underlying property, RWs would be as per Tables 13, 15 or 17, as the case may be.

(8) Investments in mortgage backed securities (MBS) backed by exposures secured by residential property or commercial real estate shall be governed by the Reserve Bank of India (Commercial Banks – Securitisation Transactions) Directions, 2025.

17. Non-Performing Assets (NPAs)

(1) The unsecured portion of NPA / Stage 3 assets (other than qualifying residential real estate exposure which is addressed in paragraph 17 (2)), net of specific provisions (including partial write-offs), shall be risk-weighted as follows:

i. 150 per cent risk weight when specific provisions are less than 20 per cent of the outstanding amount of the NPA / Stage 3 asset

ii. 100 per cent risk weight when specific provisions are at least 20 per cent of the outstanding amount of the NPA / Stage 3 asset

iii. 50 per cent risk weight when specific provisions are at least 50 per cent of the outstanding amount of the NPA / Stage 3 asset

Explanation: Outstanding amount for this purpose includes any outstanding exposure as well as credit-equivalent amount of undrawn/non-funded exposures.

(2) The residential real estate exposures meeting the qualifying conditions specified in paragraph 16(2) and where repayments do not materially depend on cash flows generated by the property securing the loan which are NPA / Stage 3 assets, shall be risk weighted at 100 per cent net of specific provisions and partial write-offs.

(3) For the purpose of defining the secured portion of the NPA / Stage 3 assets, eligible collateral shall be the same as recognised for credit risk mitigation purposes (paragraph 37(6)). Hence, other forms of collateral like land, buildings, plant, machinery, current assets, etc. shall not be reckoned while computing the secured portion of NPAs / Stage 3 assets for calculating RWAs.

18. Equity Investments in Funds

1. This paragraph prescribes computation of RWAs for a bank’s investments in pooled funds such as Mutual Funds, Alternative Investment Fund (AIF), Hedge Fund, Fund of Funds, Real Estate Investment Trusts (REITs), Infrastructure Investment Trusts (InvITs), etc., where such investments are allowed to be held in the banking book of the investing bank. RWAs for such exposures shall be computed under one or more of the following three approaches, which vary in their risk sensitivity and conservatism: the “look-through approach” (LTA), the “mandate-based approach” (MBA), and the “fall-back approach” (FBA).

2. The requirements set out in this paragraph shall also apply to banks’ off-balance sheet exposures (e.g., unfunded commitments to subscribe to a fund’s future capital calls) in such funds. However, such exposures of banks, including underlying exposures held by the investee funds, that are required to be deducted from capital of investing banks are excluded from provisions contained in paragraphs 18(3) to 18(8).

3. The look-through approach (LTA)

(i) This is the most granular and risk-sensitive approach. It requires a bank to identify the underlying exposures of the investee fund and risk weight those exposures by notionally treating them in its own books. This approach must be used when the following conditions are met:

a. The investee fund is registered with and regulated by a financial sector regulator.

b. The investee fund makes adequate and frequent disclosures about its underlying exposures at equal or higher periodicity than that of the investing bank, and such disclosures must be granular enough to enable the investing bank to identify each distinct underlying exposure and calculate the corresponding risk weights; and

c. Such disclosures are verified and certified by an independent third party, which may include a depository, a custodian bank, or an external auditor.

ii. Under the LTA, investing banks must risk weight all underlying exposures of the investee fund as if those exposures were directly held by it in its own books. This prescription shall be applicable, inter alia, on any underlying exposure of the investee fund, such as its derivative activities, which require risk weighting treatment for the underlying asset of the derivative under minimum risk-based capital requirements as well as the associated counterparty credit risk (CCR) exposure. In such cases, instead of determining a credit valuation adjustment (CVA) charge associated with the fund’s derivatives exposures in accordance with the CVA framework (as per paragraph 85 of the Reserve Bank of India (Commercial Banks – Prudential Norms on Capital Adequacy) Directions, 2025, as amended from time to time), banks shall multiply the CCR exposure by a factor of 1.5 before applying the risk weight associated with the counterparty.

Explanation: A bank is required to apply the 1.5 factor only for transactions that are within the scope of the CVA framework.

iii. Banks may rely on third-party calculations for determining the risk weights associated with their equity investments in funds (i.e., the underlying risk weights of the exposures of the fund) if they do not have adequate data or information to perform the calculations themselves. In such cases, the applicable risk weight shall be 1.2 times higher than the one that would be applicable if the exposure were held directly by the bank.

Illustration: For instance, any exposure that is subject to a 20 per cent risk weight under the standardized approach would be weighted at 24 per cent (1.2 * 20%) when the look through is performed by a third party.

(4) The mandate-based approach (MBA)

i. The second approach, the MBA, provides a method for calculating regulatory capital that can be used when the conditions (b) and (c) of paragraph 18(3)(i) for applying the LTA are not met.

ii. Under the MBA, investing banks may use the information contained in an investee fund’s mandate or in the regulations issued by the concerned financial sector regulator governing such investment funds.

Explanation: Information used for this purpose is not strictly limited to a fund’s mandate or national regulations governing like funds. It may also be drawn from other disclosures of the fund.

(iii) To ensure that all underlying risks are taken into account (including CCR) and that the MBA renders capital requirements no less than the LTA, the risk-weighted assets for the fund’s exposures are calculated as the sum of the following three items:

a. Balance sheet exposures (i.e., the funds’ assets) shall be risk weighted assuming the underlying portfolios are invested to the maximum extent allowed under the fund’s mandate in those assets attracting the highest capital requirements, and then progressively in those other assets implying lower capital requirements. If more than one risk weight can be applied to a given exposure, the maximum risk weight applicable must be used.

Illustration: For instance, for investments in corporate bonds with no ratings restrictions, a risk weight of 150 per cent must be applied

b. Whenever the underlying risk of a derivative exposure or an off-balance-sheet item receives a risk weighting treatment under the risk based capital requirements standard, the notional amount of the derivative position or of the off-balance sheet exposure is risk weighted accordingly.

Explanation: If the underlying is unknown, the full notional amount of derivative positions must be used for the calculation. If the notional amount of derivatives is unknown, it shall be estimated conservatively using the maximum notional amount of derivatives allowed under the mandate.

c. CCR associated with the fund’s derivative exposures. Till SA-CCR is implemented, the CCR associated with the fund’s derivative exposures shall be computed in terms of paragraph (18)(3)(iv) above.

5. The fall-back approach (FBA)

Where neither the LTA nor the MBA is feasible, banks shall apply the FBA. Under FBA the bank’s equity investment in the investee fund shall be subject to full capital deduction from CET1 capital.

6. Equity exposure to funds that invest in other funds (Fund of Funds) 38

When a bank has equity exposure to Fund of Funds (FoF), then it shall first identify the underlying exposures of its own investee fund to different other funds, either using the LTA or the MBA. In the second step, it can determine the risk weights for the investee fund’s exposures by using any of the three approaches prescribed above. However, if the investee fund’s investee(s) have further investments in other funds, i.e., the investee fund has also invested in a FoF, then it shall apply only the LTA for determining the RWAs. If the necessary conditions for applying LTA are not met, then the bank must apply FBA.

(7) Computation of RWA for Equity Exposures in Fund

i. For determining the capital requirement for its equity exposures in funds under the LTA and MBA, a bank shall apply a leverage adjustment to the average risk weight of the fund (Avg RWfund). In this context, Leverage (Lvg) is defined as the ratio of total assets of the investee fund to its total equity, and Avg RWfund is obtained by dividing the total risk-weighted assets of the fund as calculated under either LTA or MBA by the total assets of the fund. In cases where the bank uses MBA, Leverage shall be the maximum financial leverage permitted in the fund’s mandate or in the SEBI regulations or regulations of the relevant financial sector regulator governing the fund.

ii. The leverage adjustment, i.e., the product of Lvg and Avg RWfund, is subject to a cap of risk weight equivalent to full capital deduction.

iii. Using Avg RWfund and taking into account the leverage of a fund (Lvg), the risk-weighted assets for a bank’s equity investment in a fund can be represented as follows:

RWAinvestment = Avg RWfd * Lvg * equity investment of the bank in the investee fund

(8) Partial use of an approach

A bank may use a combination of the three approaches when determining the capital requirements for an equity investment in an individual fund, provided that the conditions set out in paragraphs 18(1) to 18(7) are met.

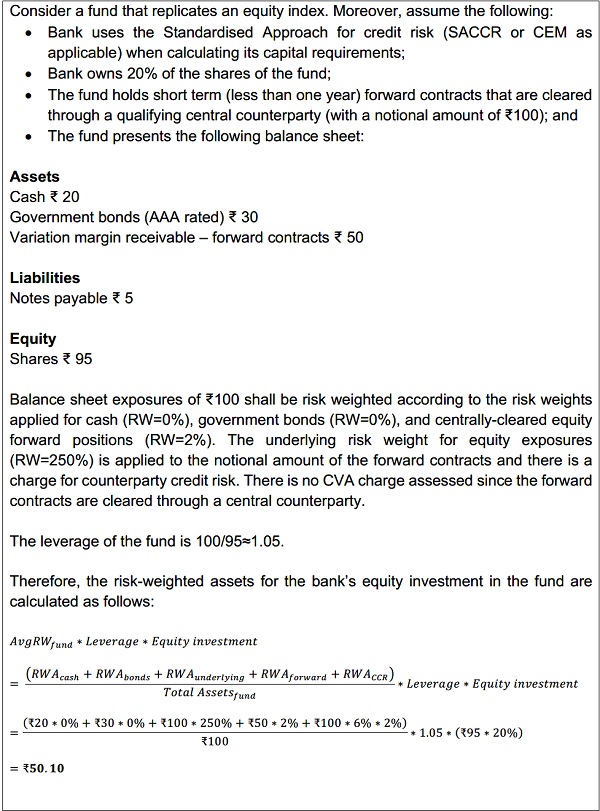

(9) An illustration of the calculation of RWAs using the LTA and MBA as well as the calculation of the leverage adjustment are provided in Appendix 2.

19. Specified Categories

1. Advances classified as ‘Capital market exposures’ other than direct equity exposures as specified under paragraph 13 above, shall attract a 125 per cent risk weight or risk weight as applicable to the counterparty, whichever is higher.

2. A bank’s investment in security receipts shall be risk weighted at 150 per cent.

20. Unhedged Foreign Currency Exposure

1. Bank exposures to entities with unhedged foreign currency exposures shall attract incremental capital requirements, i.e. over and above the present capital requirements as per the instructions contained in Chapter VII of the Reserve Bank of India (Commercial Banks – Credit Risk Management) Directions, 2025, as under:

Table 18: Incremental capital for unhedged exposure

| Potential Loss/EBID (%) | Incremental Capital Requirement |

| Upto to 75 per cent | 0 |

| More than 75 per cent | 25 per cent increase in the risk weight |

2. For unhedged ‘retail and residential real estate exposures’ to individuals where the lending currency differs from the currency of the borrower’s source of income, banks shall apply a 1.5 times multiplier to the applicable risk weight, subject to a maximum risk weight of 150 per cent. Natural and financial hedges are considered sufficient only if they cover at least 90 per cent of the loan instalment.

Explanation:

i. The risk weight treatment at paragraph 20(2) above shall be applicable for exposures to individuals in cases where a bank, in terms of paragraph 61(1) of the Reserve Bank of India (Commercial Banks – Credit Risk Management) Directions, 2025, has exercised the option of exempting exposures to individuals from calculation of UFCE.

ii. For the purpose of risk weight treatment at paragraph 20(2) above, ‘retail and residential real estate exposures’ shall include exposures to individuals that are classified under paragraph 14 or 16.

iii. Natural Hedge: An exposure shall be considered as naturally hedged only if the offsetting exposure has the maturity / cash flow within the same accounting year. For instance, export revenues (booked as receivable) may offset the exchange risk arising out of repayment obligations of an external commercial borrowing if both the exposures have cash flows / maturity within the same accounting year.

(iv) Financial Hedge: Financial hedge shall be considered only where the entity/individual has documented the purpose and the strategy for hedging at inception of the derivative contract and assessed its effectiveness as a hedging instrument at periodic intervals. For the purpose of assessing the effectiveness of hedge, guidance may be taken from the applicable accounting standards and the relevant guidance notes of the Institute of Chartered Accountants of India on the matter.

21. Other Assets

(1) Loans and advances to bank’s own staff which are fully covered by superannuation benefits and/or mortgage of flat/ house shall attract a 20 per cent risk weight. Since flat / house is not an eligible collateral and since banks normally recover the dues by adjusting the superannuation benefits only at the time of cessation from service, the concessional risk weight shall be applied without any adjustment of the outstanding amount. In case a bank is holding eligible collateral in respect of amounts due from a staff member, the outstanding amount in respect of that staff member may be adjusted to the extent permissible under CRM mechanism.

(2) Other loans and advances to bank’s own staff shall be eligible for inclusion under regulatory retail portfolio and shall therefore attract a 75 per cent risk weight.

(3) A 20 per cent risk weight shall apply to cash items in the process of collection.

(4) A zero per cent risk weight shall apply to:

i. Cash owned and held at the bank or in transit; and

ii. Gold bullion, held if any, at the bank or held in another bank on an allocated basis, to the extent the gold bullion assets are backed by the gold bullion liabilities.

(5) All other assets shall attract a uniform risk weight of 100 per cent.

22. Off-Balance Sheet Items

(1) General

(i) The risk-weighted amount of an off-balance sheet item that gives rise to credit exposure is generally calculated by means of a two-step process:

a. the notional amount of the transaction is converted into a credit equivalent amount (CEA), by multiplying the amount with the specified credit conversion factor (CCF); and