Foreign Direct Investment (FDI) in India is undertaken in accordance with the FDI Policy which is formulated and announced by the Government of India. The Department of Industrial Policy and Promotion, Ministry of Commerce and Industry, Government of India issues a “Consolidated FDI Policy Circular ” on an half yearly basis on March 31 and September 30 of each year (since 2010) elaborating the policy and the process in respect of FDI in India. FEMA Regulations which prescribe amongst other things the mode of investments i.e. issue or acquisition of shares / convertible debentures and preference shares, manner of receipt of funds, pricing guidelines and reporting of the investments to the Reserve Bank. The Reserve Bank has issued Notification No. FEMA 20/2000-RB dated May 3, 2000 which contains the Regulations in this regard. This Notification has been amended from time to time.

1) Entry routes for investments in India:-

Under the Foreign Direct Investments (FDI) Scheme, investments can be made in shares, mandatorily and fully convertible debentures and mandatorily and fully preference shares of an Indian company by non-residents through two routes:

- Automatic Route: Under the Automatic Route, the foreign investor or the Indian company does not require any approval from the Reserve Bank or Government of India for the investment.

- RBI Approval Route: Under the Government Route, the foreign investor or the Indian company should obtain prior approval of the Government of India, Ministry of Finance, Foreign Investment Promotion Board (FIPB) for the investment.

2) Description:-

Foreign investment comes into India in various forms. Following the reforms path, the Reserve Bank has liberalized the provisions relating to such investments.

- The Reserve Bank has permitted foreign investment in almost all sectors, with a few exceptions. Foreign companies are permitted to set up 100 per cent subsidiaries in India.

- In many sectors, no prior approval from the Government or the Reserve Bank is required for non-residents investing in India.

- Foreign institutional investors are allowed to invest in all equity securities traded in the primary and secondary markets.

- Foreign institutional investors have also been permitted to invest in Government of India treasury bills and dated securities, corporate debt instruments and mutual funds. The NRIs have the flexibility of investing under the options of repatriation and non-repatriation.

- The Government allows Indian companies to issue Global Depository Receipts (GDRs) and American Depository Receipts (ADRs) to foreign investors The GDRs/ADRs issued by Indian companies to non-residents have free convertibility outside India.

All foreign investment through any of the channels mentioned above are required to be reported to RBI under FEMA, 1999.

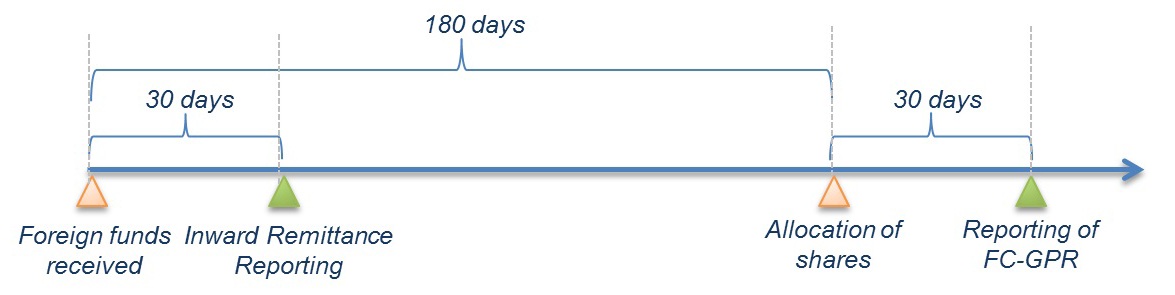

Any company or organization receiving foreign investment must report the transaction to the Reserve Bank of India in stipulated timeline. The reporting of the transaction must be done as illustrated in the figure below.

- Allocation of Shares against the investment should be completed within 180 days of receipt of fund.

- The company should file the FC-GPR form within 30 days of allotment of shares.

3) The sectors where FDI is not allowed in India, both under the Automatic Route as well as under the Government Route:-

1. Atomic Energy

2. Lottery Business

3. Gambling and Betting

4. Business of Chit Fund

5. Nidhi Company

6. Agricultural (excluding Floriculture, Horticulture, Development of seeds, Animal Husbandry, Pisciculture and cultivation of vegetables, mushrooms, etc. under controlled conditions and services related to agro and allied sectors) and Plantations activities (other than Tea Plantations) (c.f. Notification No. FEMA 94/2003-RB dated June 18, 2003).

7. Real Estate Business (other than construction development) or Construction of Farm Houses.

8. Trading in Transferable Development Rights (TDRs).

9. Manufacture of cigars, cheroots, cigarillos and cigarettes, of tobacco or of tobacco substitutes.

10. Services like legal, book keeping, accounting & auditing.

4) FDI Inflow into the Company:-

An Indian company that is issuing shares or convertible debentures under FDI, can receive the money for such shares or debentures through one of the following modes:

1. Remittance through normal banking channels.

2. Debit to NRE/FCNR account of a person concerned maintained with a Bank.

3. Conversion of royalty/lump sum/ technical knowhow fee due for payment or conversion of ECB, shall be treated as consideration for issue of shares.

4. Conversion of import payables/pre incorporation expenses/share swap can be treated as consideration for issue of shares with the approval of FIPB.

5. Debit to non-interest bearing Escrow account in Indian Rupees in India which is opened with the approval from AD Category – I bank and is maintained with the AD Category I bank on behalf of residents and non-residents towards payment of share purchase consideration.

5) Reporting FDI Inflow into the Company in form Foreign Inward Remittance Certificate (FIRC) :-

When a beneficiary receives fund from outside India, it will be credited to his account only through an Authorized Dealer (normally a Bank). (Authorized dealer means an authorized person by the Reserve Bank of India to deal in foreign exchange or in foreign securities under the FEMA). If the bank, in which the beneficiary has an account, is not an Authorized Dealer, then the remittance needs to be received by the beneficiary through an Authorized Dealer. Based on the information provided by the beneficiary upon receipt of foreign remittance, the banker issues FIRC stating the purpose of receipt i.e. towards equity investment, advance against export of services / goods, capital expenditure etc. (If the amount of inward remittance exceeds Rs.1,00,000 or its equivalent in foreign exchange, then the purpose of remittance should be ascertained by the authorized dealer.

Within 30 days of receipt of share application money/amount of consideration from the foreign investor, the Indian company must report details of the FDI inflow to the Foreign Exchange Department, Reserve Bank of India. The report must be submitted to the Regional Office of the Reserve Bank of India under whose jurisdiction its Registered Office is located. The form to be filed at this stage is the FIRC Form, containing the following details:

6) FIRC normally contains the following details:

1. Name and address of the foreign investor(s);

2. Date of receipt of funds and the Rupee equivalent;

3. Name and address of the authorized dealer through whom the funds have been received;

4. Details of the Government approval, if any; and

5. KYC report (Identify and Address proof) on the non-resident investor from the overseas bank remitting the amount of consideration.

7) Issuing Shares of Indian Company to the Foreign Investor:-

The money received from the foreign investor for purchase of shares in the Indian Company will be accounted under share application money. The Indian Company is required to issue shares within 180 days from the date of inward remittance to the foreign investor, to avoid violation of the FEMA regulations.

8) FDI Reporting to RBI through Form FC-GPR:-

Within 30 days from the date of issue of shares, form FC-GPR must be filed with the RBI along with the following documents.

Certificate from the Company Secretary of the company accepting investment from persons resident outside India certifying that:

1. “The company has complied with the procedure for issue of shares as laid down under the FDI scheme as indicated in the Notification No. FEMA 20/2000-RB dated 3rd May 2000, as amended from time to time.”; AND

2. The investment by the Foreign Investor in the Company is within the sectoral cap/statutory ceiling permissible under the Automatic Route of the Reserve Bank and it fulfills all the conditions laid down for investments under the Automatic Route; OR

3. Shares in the company have been issued to the Foreign Investor in terms of SIA/FIPB approval number and date. A copy of the Foreign Investment Promotion Board (FIPB) must be attached.

Certificate from Statutory Auditors/ SEBI registered Merchant Banker / Chartered Accountant indicating the manner of arriving at the price of the shares issued to the persons resident outside India.

Form FC-GPR and the Company Secretary / Chartered Accountant certificates must be submitted by the company to the Foreign Exchange Department, Reserve Bank of India.

9) Pre-requisites:-

Before reporting the transaction, applicant needs to obtain following:

1. Unique Identification Number from RBI by reporting of Advanced Foreign Remittance;

2. KYC report for the beneficiary if the beneficiary and remitter are different entities;

3. CS certificate;

4. Certificate from SEBI registered Merchant Banker / Chartered Accountant indicating the manner of arriving at the price of the shares issued to the persons resident outside India;

5. Disclaimer Certificate;

6. Statutory Auditor Certificate;

7. Board resolution;

8. LRN (Loan Registration Number) allotted;

9. copy of FIPB approval (if required);

10. Details of Transfer of shares if any;

11. No objection certificate from the remitter for the shares being allotted to the third party mentioning their relationship;

12. Letter from the foreign investor explaining the reason for making subscription to shares by the remitter on his behalf;

13. Copy of agreement/Board resolution from the investee company for issue and allotment of shares to the foreign investor, other than the remitter;

14. Reason for delay in submission (if required).

10) Components of File FC-GPR Form:-

This FC-GPR Form consists of Two Parts:

I. FC-GPR Part A

II. FC-GPR Part B

I] FC-GPR Part A:-

1. Part A of Form FC-GPR has to be duly filled up and signed by the Authorised Signatory and submitted to the Authorised Dealer of the company, who will forward it to the Reserve Bank.

2. While forwarding the Form, the Authorised Dealer will enclose a KYC Report on the foreign investor. Along with Part A of FC-GPR, the following documents has to be attached by the company:

A) A certificate from the Company Secretary of the company certifying that

(a) All the requirements of the Companies Act, 2013 have been complied with;

(b) Terms and conditions of the Government approval, if any, have been complied with;

(c) The company is eligible to issue shares under these Regulations; and

(d) The company has all original certificates issued by authorised dealers in India evidencing receipt of amount of consideration;

B) A certificate from Statutory Auditors or Chartered Accountant indicating the manner of arriving at the price of the shares issued to the persons resident outside India.

II] FC-GPR Part B:-

1. Part-B of FC-GPR should be filed on an annual basis with the Reserve Bank.

2. This filing has to be done in the month of June every year, for all outstanding investment by way of FDI as well as Portfolio / other investments and by way of re-invested earnings for the previous April to March period.

3. For example, all Indian companies who have received FDI, Portfolio investments, other investments (such as bonds, debentures etc.) from foreign investors during the period April 2015 to March 2016, have to report in Part B of Form FC-GPR in the month of June 2016, along with their retained earnings during the period.

Flow Chart showing the Process of Reporting the Foreign Direct Investment to RBI as per regulations under FEMA Act:

11) Failure to report FDI inward remittance or filing of FC-GPR:-

The Reserve Bank is empowered to compound any contraventions as defined under section 13of FEMA, 1999:

1. If any person contravenes any provision of this Act, or contravenes any rule, regulation, notification, direction or order issued in exercise of the powers under this Act, or contravenes any condition subject to which an authorization s issued by the Reserve Bank, he shall, upon adjudication, be liable to a penalty up to thrice the sum involved in such contravention where such amount is quantifiable, or up to two lakh rupees where the amount is not quantifiable, and where such contravention is a continuing one, further penalty which may extend to five thousand rupees for every day after the first day during which the contravention continues.

2. Any Adjudicating Authority adjudging any contravention under sub-section (1), may, if he thinks fit in addition to any penalty which he may impose for such contravention direct that any currency, security or any other money or property in respect of which the contravention has taken place shall be confiscated to the Central Government and further direct that the foreign exchange holdings, if any, of the persons committing the contraventions or any part thereof, shall be brought back into India or she l be retained outside India in accordance with the directions made in this behalf.

Explanation.-

For the purposes of this sub-section, “property” in respect of which contravention has taken place, shall include-

1. Deposits in a bank, where the said property is converted into such deposits;

2. Indian currency, where the said property is converted into that currency; and

3. Any other property which has resulted out of the conversion of that property

12) International law related to Foreign Direct Investment in other countries:-

Foreign Direct Investment (FDI) in Australia:

The Australian Government welcomes foreign investment. It has helped build Australia’s economy and will continue to enhance the wellbeing of Australians by supporting economic growth and prosperity. It supports existing jobs and creates new jobs, it encourages innovation, it introduces new technologies and skills, it brings access to overseas markets and it promotes competition amongst our industries.

The Government’s foreign investment framework is implemented through the Foreign Acquisitions and Takeovers Act 1975 (the Act) and the Government’s foreign investment policy. The Deputy Prime Minister and Treasurer is responsible for the foreign investment framework. Under the Act, the Treasurer reviews investment proposals on a case-by-case basis to decide if they are contrary to Australia’s national interest. This maximizes investment flows, while protecting Australia’s interests. When making such decisions, the Treasurer relies on advice from the Foreign Investment Review Board (FIRB). FIRB will work with an applicant to ensure the national interest is protected. But, if ultimately it is determined that a proposal is contrary to the national interest, it will not be approved. Proposals may also be approved subject to conditions or undertakings.

The policy applies to foreign persons. This includes a natural person not ordinarily resident in Australia, a corporation in which a natural person not ordinarily resident in Australia or a foreign corporation has a controlling (substantial) interest, and the trustee of a trust estate in which a natural person not ordinarily resident in Australia or a foreign corporation has a substantial interest.

A ‘substantial interest’ occurs when a single foreign person (and any associates) has 15 per cent or more of the ownership, or several foreigners (and any associates) have 40 per cent or more in aggregate of the ownership of any corporation, business or trust.

In addition, all foreign governments and their related entities should notify the Government and get prior approval before making an investment in Australia, regardless of the value of the investment.

Contributed by:

Mrs. Hetal Chitroda

Mrs. Jaya Sharma- Sin ghania

M/s. Jaya Sharma & Associates – Practicing Company Secretary Firm, Mumbai

Bibliography:-

- Companies Act, 2013- Impact on Foreign Companies in India by Arun Gupta.

- Foreign Exchange Management (Transfer or Issue of Security by a Person Resident outside India) Regulations, 2000 notified vide Notification No. FEMA.20/2000-RB dated May 3, 2000

- http://dipp.nic.in/Fdi_Circular/FDI_Circular_012011_31March2011.pdf.

- https://www.ebiz.gov.in/fc-gpr-central

- http://www.indiafilings.com/learn/fdi-reporting-to-rbi-using-form-fc-gpr

- http://www.dipp.gov.in

- https://taxguru.in/rbi/compounding-offences-fema-1999.html

- http://finmin.nic.in/the_ministry/dept_eco_affairs/capital_market_div/FEMA_act_1999.pdf