“Taka mati, mati taka (Money is mud, mud is money).”

– Ramakrishna Paramahamsa

“Among all forms of mistake, prophecy is the most gratuitous.”

– George Eliot, Middlemarch

Demonetisation has been a radical, unprecedented step with short term costs and long term benefits. The liquidity squeeze was less severe than suggested by the headlines and has been easing since end-December 2016. A number of follow-up actions would minimize the costs and maximise the benefits of demonetisation. These include: fast, demand-driven, remonetisation; further tax reforms, including bringing land and real estate into the GST, reducing tax rates and stamp duties; and acting to allay anxieties about over-zealous tax administration. These actions would allow growth to return to trend in 2017-18, following a temporary decline in 2016-17.

I. IntroductIon

3.1 On November 8, 2016, the government announced a historic measure, with profound implications for the economy. The two largest denomination notes, Rs 500 and Rs 1000, were “demonetized” with immediate effect, ceasing to be legal tender except for a few specified purposes.1 At one fell stroke, 86 percent of the cash in circulation was thereby rendered invalid.2 These notes were to be deposited in the banks by December 30, 2016, while restrictions were placed on cash withdrawals. In other words, restrictions were placed on the convertibility of domestic money and bank deposits.3

3.2 The aim of the action was fourfold: to curb corruption; counterfeiting; the use of high denomination notes for terrorist activities; and especially the accumulation of “black money”, generated by income that has not been declared to the tax authorities.

3.3 It followed a series of earlier efforts to curb such illicit activities, including the creation of the Special Investigative Team (SIT) in the 2014 budget; the Black Money and Imposition of Tax Act 2015; Benami Transactions Act 2016; the information exchange agreement with Switzerland; changes in the tax treaties with Mauritius, Cyprus and Singapore; and the Income Disclosure Scheme. Demonetisation was aimed at signalling a regime change, emphasizing the government’s determination to penalize illicit activities and the associated wealth. In effect, the tax on all illicit activities, as well as legal activities that were not disclosed to the tax authorities, was sought to be permanently and punitively increased.

3.4 India’s demonetisation is unprecedented in international economic history, in that it combined secrecy and suddenness amidst normal economic and political conditions. All other sudden demonetisations have occurred in the context of hyperinflation, wars, political upheavals, or other extreme circumstances. But the Indian economy had been growing at the fastest clip in the world on the back of stable macroeconomics and an impressive set of reforms (Chapter 1). In such normal circumstances, demonetisations—such as the one announced recently in Europe— tend to be phased in gradually (See Appendix 1 for a list of cross-country episodes of both gradual and sudden demonetisations.)

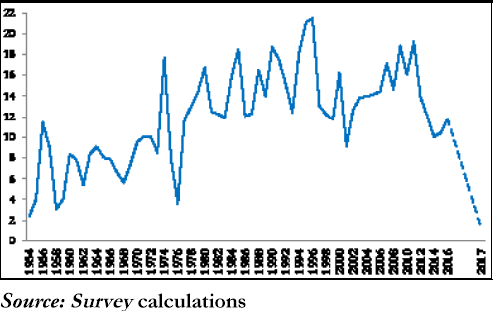

3.5 India’s action is not unprecedented in its own economic history: there were two previous instances of demonetisation, in 1946 and 1978, the latter not having any significant effect on cash as Figure 1 shows.4 But the recent action had large, albeit temporary, currency consequences. Figure 1 shows annual percentage changes in currency since 1953. For 2016-17, this

Figure 1. Growth in average currency with

public (%, yoy)

Note: Years are financial years and only even number years have been labeled

change is expected to be only 1.2 percent year-on-year, more than 2 percentage points lower than four previous troughs, which averaged about 3.3 percent.5

3.6 In the wake of the Global Financial Crisis (GFC), advanced economies have used monetary policy to stimulate growth, stretching its use to domains heretofore considered heretical such as negative interest rate policies and “helicopter drops” of money. In fact, India has given a whole new expression to unconventional monetary policy, with the difference that whereas advanced economies have focused on expanding the money supply, India’s demonetisation has reduced it. This policy could be considered a “reverse helicopter drop”, or perhaps more accurately a “helicopter hoover”.

3.7 The public debate on demonetisation has raised three sets of questions. First, broader aspects of management, as reflected in the design and implementation of the initiative. Second, its economic impact in the short and medium run. And, third, its implications for the broader vision underlying the future conduct of economic policy. This Survey is not the forum to discuss the first question, and the third is discussed in Chapter 1. This chapter focuses on the second question.

3.8 What are the background facts? What are the analytics? What are the long-term benefits and short-term costs? And what policy responses going forward would maximise benefits and minimizes costs? This section attempts to answer these questions. The Survey does not discuss the broader welfare and other non-economic dimensions (Rai, 2016). There have been reports of job losses, declines in farm incomes, and social disruption, especially in the informal, cash-intensive parts of the economy but a systematic analysis cannot be included here due to paucity of macro-economic data.

3.9 A cautionary word is in order. India’s demonetisation is unprecedented, representing a structural break from the past. This means that forecasting its impact is hazardous. The discussion that follows, especially the attempts at quantification, must consequently be seen as tentative and far from definitive. History’s verdict, when it arrives through the “foggy ruins of time,” could surprise today’s prognostications.

II. Background Facts

3.10 To dispel confusion and sharpen understanding of the issues, key distinctions must be made at the outset. Cash can be understood along two dimensions: its function and its nature/origins. In terms of function, cash can be used as a medium of exchange (for transactions) or as a store of value like other forms of wealth such as gold and real estate. In terms of nature, cash can be illicit or not.

3.11 Function and nature are quite distinct (Table 1). For example, cash used as a store of value could be white (the savings that all households keep for an emergency), while cash used for transactions could be black (if it was earned through tax evasion and/or corruption). Moreover, categories are fluid. Cash held as black money can be converted to white through laundering and other means, or by declaring it to the authorities and paying the associated tax/penalty.

3.12 A few facts are relevant to, and have motivated, demonetisation.

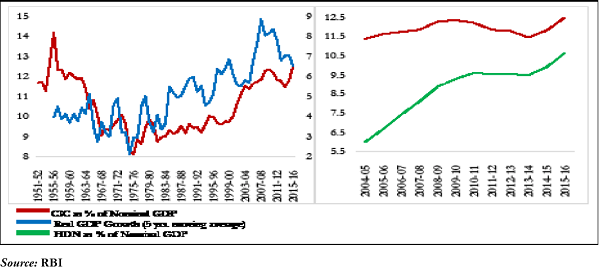

3.13 First, India’s currency to GDP ratio has evolved in two broad phases. It declined fairly steadily for the first decade and a half after Independence, falling from around 12 percent in 1952-53 to about 9 percent in 1967-68. Thereafter, the ratio appears to have responded to the growth of the economy. It began its upward trend in the late 1970s when growth increased, and then accelerated further during the growth boom of the 2000s. This ratio declined during the period of high inflation in the late 2000s and early 2010s but it rebounded after 2014-15 to 12 percent when inflation declined again. The value of high denomination notes (INR

Table 1. Dual Dimensions of Cash

| Origin/nature | ||

| White | Black | |

| Function | ||

| Transactions | Company pays employee salary in cash; payment and receipt are declared to tax authorities | Small enterprise pays for input in cash; neither declares the transaction to tax authorities |

| Store of value | Household keeps savings in cash for emergencies | Businessman hoards undeclared cash, with a view to distributing it to his candidate during elections |

500 and INR 1000) relative to GDP has also increased in line with rising living standards (green line in the second chart of Figure 2).

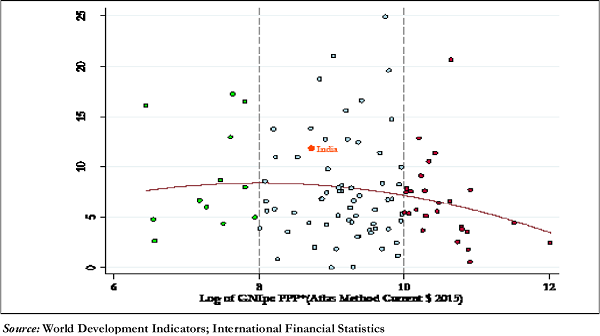

3.14 Second, India’s economy is relatively cash-dependent, even taking account of the fact that it is a relatively poor country. Figure 1 plots the cash to GDP ratio against country per capita GDP, showing that on average the use of cash does indeed decline with development (yellow line). India’s level is somewhat higher than other countries in its income group (central panel).

3.15 This might seem to suggest that some of the cash holdings were not being used

Figure 2. Currency in Circulation, High Denomination Notes and Real GDP Growth

Source: RBI

Note: CIC = Currency in Circulation

HDN = High Denomination Notes (INR 500 and INR 1000)

Figure 3. Cash-to-GDP Ratio Versus Per capita GNI in PPP Terms

for legitimate transactions, but perhaps for other activities such as corruption.6 This presumption is especially strong because across the globe there is a link between cash and nefarious activities: the higher the amount of cash in circulation, the greater the amount of corruption, as measured by Transparency International (Figure 4).

3.16 In this sense, attempts to reduce the cash in an economy could have important long-term benefits in terms of reducing levels of corruption. Yet India is “off the line”, meaning that its cash in circulation is relatively high for its level of corruption. This suggests two possibilities. Perhaps India’s level of corruption (or other related pathologies) is much worse than the index shows, so that the orange dot should really be placed to the right. Or cash is being used for other, presumably legitimate purposes.

3.17 But even if high levels of cash are needed this doesn’t mean high denominations are needed. It is usually the case that high value notes are associated with corruption because they are easier to store and carry, compared to smaller denominations or other stores of value such as gold (Sands, 2016; Henry, 1980; Summers, 2016; Rogoff, 2016).

3.18 How high were India’s high denomination notes in terms of their use for transactions relative to store of value? Figures 5-6 shed some light. In particular, it is useful to look at the size of the notes relative to nominal per capita income. The higher a note is relative to income, the less likely it is to be used purely for transactions purposes. In India’s case, the denomination/ income ratio has fallen sharply over the past quarter century because incomes have been growing rapidly relative to the prevailing