BACKGROUND

Direct Tax Vivad se Vlshwas Act, 2020 offers a win-win dispute resolution package that benefits the taxpayers as well as the Government. Taxpayers All also be better-off due to savings on account of time and resources, certainty with respect to their tax liability and immunity from penalty and prosecution. Government will benefit from timely generation of revenue and savings on account of time and resources that go into appeals process.

AIMS OF THE SCHEME

- Resolution of Pending Income-tax Disputes & Litigation;

- Savings on account of time and resources; Generate timely revenues for the Government

- Help taxpayers end their tax disputes with the Department by paying disputed tax and get waiver from payment of Interest and penalty. Also get immunity from prosecution.

KEY DATES

- The last date for declaration under the scheme is 31st December, 2020. Make the payment without additional amount by 31st March, 2021.

IMPORTANT TERMS

(a) ‘appellant” is a person who fulfils the eligibility criteria (given later in Para) and can file a valid application for declaration under the Scheme.

{b) ‘appellate forum” means the Supreme Court or the High Court or the Income Tax Appellate Tribunal or the Commissioner (Appeals);

The proceedings before Settlement Commission and the Authority for Advance Ruling will not form a part of this Scheme.

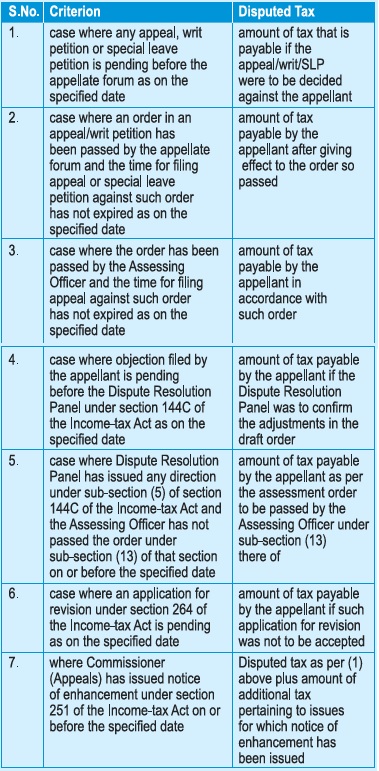

(c) ‘disputed tax”- The determination of disputed tax shall be made as per the table given below:

(d) ‘specified date” means the 31st clay of Jan nary, 2020;

(e) “disputed interest means the interest determined in any case under the provisions of the Income-tax Act, 1961, where—

i. such interest is not charged or chargeable on disputed

ii. an appeal has been filed by the appellant in respect of such interest

(f) ‘disputed penalty” means the penalty determined In any case under the provisions of the Income-tax Act, 1961, where—

i. such penalty Is not levied or leviable In respect of disputed Income or disputed tax, as the case maybe;

ii. an appeal has been filed by the appellant in respect of such penalty;

(g) ‘tax arrear’ means,—

(i) the aggregate amount of disputed tax, interest chargeable or charged on such disputed tax, and penalty leviable or levied on such disputed tax; or

(ii) disputed interest; or

(iii) disputed penalty; Of

(iv) disputed fee,

(v) Disputed TDS or TCS as determined under the provisions of the Income-Tax Act;

SALIENT FEATURES OF THE ACT

ELIGIBILITY

A taxpayer Is eligible to be covered under this scheme If, for an Assessment Year, he/she has a case in which

- Appeals/writs have been filed on or before 31.01.2020.

- Orders for which time for filing appeal has not expired on 31.01.2020.

- Cases pending before Dispute Resolution Panel (DRP) on 31.01.2020.

- Cases where DRP issued direction on or before 31.012020 but no order has been passed.

- Cases where assesses filed revision (Section 264) on or before 31.01.2020 and are pending.

- Search case if the disputed demand is less than Rs. 5 Crore in a year.

- The appeals/writs filed either by taxpayers or the Department.

- Disputes where the payment has already been made are also eligible.

- Cases in Arbitration in India or abroad.

DISPUTES COVERED

All disputes, subject to some exclusion, in relation to the:

- Disputed tax

- Disputed penalty

- Disputed interest

- Disputed Fee

- Disputed IDS or TCS are covered under the Scheme.

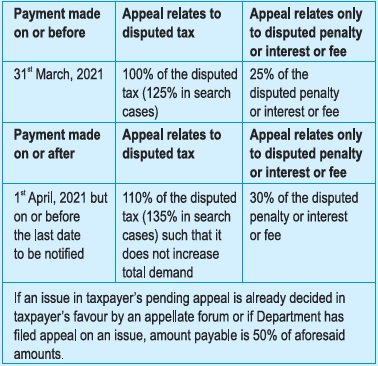

PAYMENT SCHEDULE UNDER THE SCHEME

AMOUNTS PAYABLE

(Appeals by Assessee)

| Nature of tax arrear | If paid till 31.03.2021 | If paid after 01.04.2021 |

| Tex Arrears:

Income Tax + Interest (Charged or chargeable) + Penalty (Charged or chargeable) on |

100 % of Disputed Tax | 110% of Disputed Tax If such 10% of disputed tax exceeds the interest and penalty charged or chargeable then such excess to be ignored. |

| Disputed Interest, Disputed Penalty Disputed Fee | 25 % | 30% |

| Search Cases | 125 % of Disputed Tax | 135% of Disputed Tax |

Appeals by Department

EXCLUSIONS

The taxpayers with cases falling in the categories given below are excluded from the Scheme and cannot file declaration under it:

(i) Search case, where disputed tax is more than Rs.5 crore in a year.

(ii) Prosecution case, under the Income-tax Act or IPC filed by the Department

(iii) Cases relating to undisclosed foreign income and assets

(iv) Cases completed on the basis of information from foreign countries

(v) Cases covered under Narcotic Drugs and Psychotropic Substances Act, Special Courts Act, the Unlawful Activities (Prevention) Act 1967, the Prevention of Corruption Act, the Conservation of Foreign Exchange and Prevention of Smuggling Activities Act 1974, the Prevention of Money Laundering Act 2002, the Prohibition of Benami Property Transactions Act, 2016.

BENEFITS

The Scheme endows a number of benefits on the people who avail It, some of which areas follows:

- Waiver of interest

- Immunity. from penalty.

- Immunity from prosecution.

FILING OF DECLARATION

- The declarant will file the declaration before the designated authority in such form and in such manner verified as prescribed.

- Upon filing of the declaration, the appeal filed by the declarant shall be deemed to have been withdrawn from the date, certificate is issued by the designated authority.

- The declarant shall withdraw such appeal or writ petition with leave of the court.

- The declarant shall withdraw any proceeding or arbitration or conciliation and furnish its proof along with the declaration.

- The declarant shall furnish an undertaking waiving his right to seek or pursue any remedy or claim in relation to the tax arrear covered under the Scheme.

ROLE OF DESIGNATED AUTHORITY

- The scheme defines the ‘designated authority to bean officer not below the rank of a Commissioner of Income Tax notified by the principal Chief Commissioner for the purposes of this Act”

- ‘The designated authority shall within a period of 15 days from the date of receipt of the declaration, by order determine the amount payable byte declarant.

- He will grant a certificate to the declarant giving details of the tax arrear and amount payable after such determination.

- Once the amount has been paid by the declarant, the designated authority shall pass an order stating that the amount has been paid.

- M such orders shall be conclusive bathe matters stated therein.

PAYMENT BY DECLARANT

- The declarant shell pantie amount determined by the designated authority within 15 days of the receipt of the certificate.

- He shall intimate the details of such payment to the designated authority.

WITHDRAWAL OF APPEAL

- Consequent to such declaration and fulfilment of conditions, appeals/writs/objections of taxpayers & department in respect of the disputed Income, disputed Interest or disputed penalty or disputed fee pending before the Commissioner (Appeals), DRP, ITAT, High Court or Supreme Court shall be withdrawn.

- In the case of taxpayer’s appeals a certificate to the effect shall be furnished by the taxpayer.

REFUND OF EXCESS AMOUNT

- If the amount paid by taxpayer before filing declaration exceeds the amount payable under the Scheme, the taxpayer would be granted the refund far such excess amount.

- No interest shall be payable to the taxpayer on such refund.

OTHER POINTS

- Filing of declaration will not set any precedence and neither the Department nor the taxpayer can claim In any other proceedings that the taxpayer or the Department has conceded Its tax position by settling the dispute.

- The limit of disputed tax of Rs. 5 crore for filing declaration in a search case shall be computed year wise. Hence, in a search case where the aggregate disputed tax for two or more years exceeds Rs 5 crore, a person can file declaration for those years in which the disputed tax does not exceed Rs. 5 Core.

- If there are more than one issues involved in the appeal, the taxpayer would be required to file declaration for all issues, he cannot file declaration for some issues and litigate the balance issues.

- In a case where the taxpayer has got a favourable decision on an issue at higher forum, he would be required to pay only 50% of disputed tax on that issue even in the cases in which he has filed appeal.

- In case where the Assessing Officer has reduced the returned loss by making addition of income/disallowing expenditure, the taxpayer shall have an option to either pay the notional tax on amount by which the loss has been reduced and carry formed the claimed loss without reduction or by accepting the reduced carry forward of loss without making any payment under the Scheme. Same mechanism would apply for reduction in MAT credit_

- The settling of dispute regarding transfer pricing adjustment would not have any effect on the secondary adjustment, both being independent provisions, and the taxpayer would be required to repatriate fund to India in respect of settled transfer pricing adjustment.

- Once declaration is filed by assessee under Vivad Se Vishwas it can be revised, any number of limes before the DA issues a certificate of final tax amount payable under the scheme.

- Please visit the Departmental website

- wmv.incametaxindiaefiling.gov.in for more details.