Industry Standards on Regulation 30 of SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015

SEBI vide Circular dated 25.02.2025 mandate Listed Entities to follow the Industry Standards formulated by Industry Standards Forum in consultation with SEBI comprising of representatives from 3 industry associations, viz. ASSOCHAM, CII and FICCI for effective implementation of the requirement to disclose material events or information under Regulation 30 of SEBI (LODR) Regulations, 2015.

INTRODUCTION

SEBI vide Circular dated 25.02.2025 mandate Listed Entities to follow the Industry Standards formulated by Industry Standards Forum in consultation with SEBI comprising of representatives from 3 industry associations, viz. ASSOCHAM, CII and FICCI for effective implementation of the requirement to disclose material events or information under Regulation 30 of SEBI (LODR) Regulations, 2015.

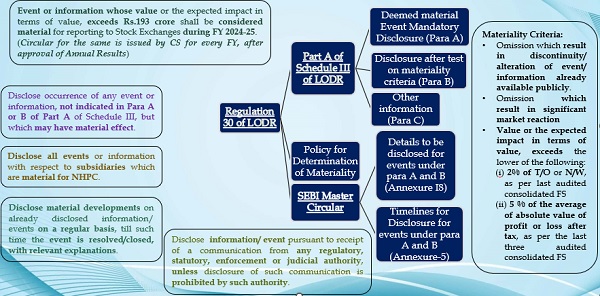

Brief of Regulation 30 and Schedule III

Interpretation of “value or the expected impact in terms of value”

under Regulation 30(4)(i)(c)

- “Expected impact in terms of value” of an event/information

- Shall consider the expected impact in the 4 ensuing quarters (including the quarter in which the event occurs if the event occurs in the first 60 days of the quarter)

| If an event has occurred on 29.05.2023 (which is in the first 60 days of the quarter, then the computation of 4 ensuing quarters shall include the ongoing quarter i.e. 01.04.2023. Accordingly, the period of assessment would be the 4 quarters beginning 01.04.2023 till 31.03.2024. | If an event has occurred on 01.06.2023 (which is not in the first 60 days of the quarter, then the computation of 4 ensuing quarters shall not include the ongoing quarter. Accordingly, the period of assessment would then be from 01.07.2023 till 30.06.2024. |

Interpretation of “value or the expected impact in terms of value”

under Regulation 30(4)(i)(c)

- Disclosure / non-disclosure of events would be in compliance of LODR and applicable accounting standards (Ind AS 37), so as to ensure consistency between the disclosures made to the stock exchanges and the disclosures made in the financial statements.

- Disclosure of an event under Para B if the gross amount exceeds the materiality threshold. However, listed entities may disclose details of indemnity and insurance claims which could mitigate the expected impact, if any, in respect of such event to provide more context while making the disclosure.

- In certain instances, all of the three parameters specified under Regulation 30(4)(i)(c) (viz., profit / net worth / turnover) may not be relevant to an event. As such, while assessing whether an event under Para B exceeds the materiality thresholds, listed entities should refer to Annexure-A for determination of materiality for different types of events.

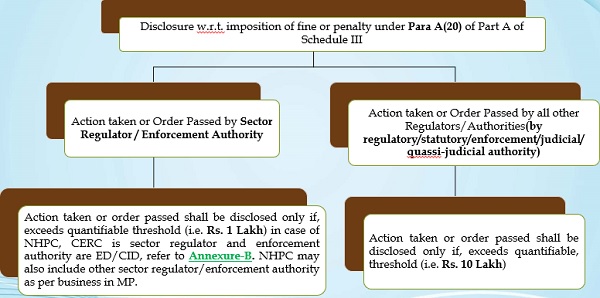

Materiality for disclosure under Para A(20) of Part A of Schedule III

Imposition of fine or penalty below the quantifiable thresholds, should be disclosed by NHPC on a quarterly basis.

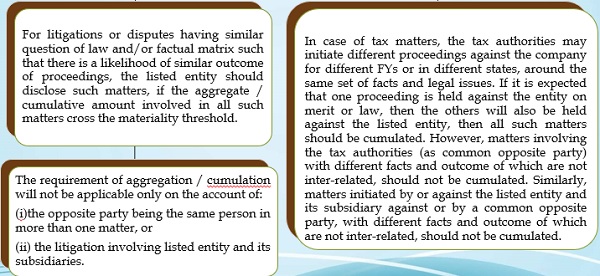

Interpretation of ‘cumulative basis’ for disclosure of pending litigations or disputes under Regulation 30(4) read with Para B(8) of Part A of Schedule III

Compliance of timelines for disclosure under Regulation 30(6)

- Appropriate systems for prompt internal reporting of events and training sessions at regular intervals for awareness

- The timelines would begin once an officer of the listed entity has become aware of the occurrence of an event / information, through credible and verifiable channels of communication.

- Defence for non-compliance with the timelines prescribed if there is any reasonable delay on account of:

1. a force majeure event,

2. time taken for completion of prima facie assessment of materiality for certain relevant events (such as orders, fraud, winding-up petitions, action initiated, claims made against listed entity, etc.), or

3. information / event relating to subsidiary, director, key managerial personnel, senior management or promoter (where listed entity is not directly involved), etc.

In such events, explanation for the delay should be provided along with the disclosure of the event/information.

Disclosure of communication from regulatory, statutory, enforcement or judicial authority under Regulation 30(13)

Regulation 30(13) of SEBI(LODR), 2015 states that:

In case an event or information is required to be disclosed by the listed entity, pursuant to the receipt of a communication from any regulatory, statutory, enforcement or judicial authority, the listed entity shall disclose such communication, along with the event or information, unless disclosure of such communication is prohibited by such authority.

- The listed entities, while disclosing material information (receipt of a communication from any regulatory, statutory, enforcement or judicial authority) such communication, shall not be required to disclose confidential and sensitive information, including proprietary information.

- A summary of key elements of such communication shall be furnished as per Annexure-C, which shall constitute sufficient compliance

- To the extent the listed entities make disclosures of all relevant information as per the prescribed format under this requirement, they shall not be required to provide a copy

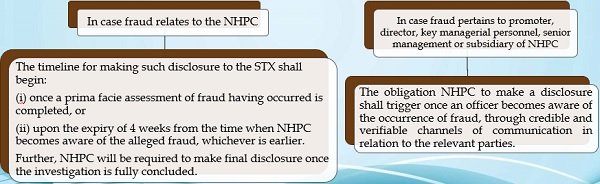

Disclosure of fraud or default under Regulation 30 read with Para A(6) of Part A of Schedule III

Regulation 30 read with Para A(6) of Part A of Schedule III states that:

Fraud or defaults by a listed entity, its promoter, director, key managerial personnel, senior management or subsidiary or arrest of key managerial personnel, senior management, promoter or director of the listed entity, whether occurred within India or abroad shall be disclosed.

Disclosure for resignation of key managerial personnel, senior management, etc. under Para A(7C) of Part A of Schedule III

In case resignation of KMP, SM, CO and non ID of NHPC, the phrase “resignation comes into effect” shall mean the last date of the concerned person in NHPC and the timelines for disclosure shall be calculated accordingly.

| NHPC shall disclose such resignation of concerned person within 24 hours of such resignation c.i.e. | NHPC shall provide the copy of resignation letter of the concerned person within 7 days from the date that such resignation c.i.e. along with detailed reasons for the resignation. |

For example, if Ms. X is a KMP of NHPC, who submits her resignation letter on 01.01.2024 and the management accepts the resignation on 31.01.2024 and her last date in NHPC being 28.02.2024. Then, NHPC shall be required to make the disclosure of her resignation on or prior to 29.02.2024 (i.e. within 24 hours of such resignation coming into effect). Further, NHPC shall also be required to provide the copy of her resignation letter dated 01.01.2024 on or prior to 06.03.2024 (i.e. within 7 days from the date that such resignation comes into effect), along with detailed reasons for the resignation.

When disclosing a copy of the resignation letter to STX, NHPC may redact portions from such resignation letter, other than the detailed reasons for resignation.

Disclosure of guarantees and indemnity under Regulation 30(4) read with Para B(11) of Part A of Schedule III

- NHPC may exclude disclosure w.r.t. indemnity/guarantee/surety, provided to WOS whose accounts are consolidated.

- However, NHPC required to disclose above for WOS, if the concerned entity ceases to be a WOS.

- All material indemnity/ guarantee/ surety pertaining to their WOS would be required to be disclosed by the NHPC in case the same is invoked.

- The disclosure requirement shall not extend to contractual performance guarantees given by NHPC in the normal course of business. However, disclosure upon invocation of such performance guarantees.

OTHER MISCELLANEOUS ASPECTS COVERED

| Disclosure relating to other persons under Para A (19) and (20) of Part A of Schedule III | Company while considering a matter involving directors, key managerial personnel, senior management, promoter or subsidiary requires disclosure can restrict themselves to disclosing such matters which are “in relation to the listed entity” and have an impact on operations, financial position or reputation of the listed entity. |

| Disclosure of show cause notices under: (i) Para A(20) of Part A of the Schedule III and (ii) Para B(8) of Part A of Schedule III | Receipt of a show cause notice would not trigger a disclosure requirement under Para A(20) of Part A of the Schedule III. However, receipt of a show cause notice from any regulatory, statutory, enforcement authority would come under Para B(8) of Part A of the Schedule III, and require disclosure upon application of the guidelines for materiality. |

| Disclosure of confidential litigation / dispute / order / action initiated or taken under (i) Para A(19) and (20) of Part A of the Schedule III, and (ii) Para B(8) of Part A of Schedule III | Listed entities while evaluating the expected impact (and subsequently, the disclosure requirement) of pending litigation / dispute / order / action initiated or taken may also consider whether the same is confidential in nature under any applicable law and/or requirement / direction of any regulatory, statutory, judicial or quasi-judicial authority, or any tribunal. |

| Disclosure of events/ information which emanate from a decision taken in a meeting of BOD under Regulation 30(6) | The timelines specified for disclosure of events or information which emanate from a decision taken in a meeting of BOD, shall be applicable for making the disclosure in PDF and XBRL format within 24 hours from the conclusion of the meeting of BOD. |

| Disclosure of announcement/ communication through social media intermediaries or mainstream media under Regulation 30(4) read with Para A(18) of Part A of Schedule III | In case of any premature announcement/ communication through social media intermediaries/ mainstream media by directors, promoters, KMP or SM of NHPC, while making the requisite disclosure under this provision, NHPC shall be required to issue necessary clarification in respect to such announcement/ communication. |

OTHER MISCELLANEOUS ASPECTS COVERED

| Disclosure of schedule of analysts or institutional investors meet at least 2 working days in advance under Para A(15(a)) of Part A of Schedule III | For analysts or institutional investors meet which are scheduled by NHPC at short notice, the requirement of providing at least 2 working days notice in advance may be dispensed. In such a case, the schedule of meetings should simultaneously be submitted to STX along with the explanation for the short notice. Further, the meeting shall not be preceded or succeeded by any one-to-one meetings. |

| Disclosure of winding up petition under Regulation 30 read with Para A(11) of Part A of Schedule III | Listed entities while considering whether a winding up petition requires disclosure can restrict themselves to disclosing those winding up petitions validly filed by eligible parties under Sections 271 and 272 of the Companies Act, 2013 (once such matter is admitted by NCLT). |

| Disclosure of proceedings of AGMs and EGMs of the listed entity under Para A(13) of Part A of Schedule III | A listed entity shall disclose voting results of annual and extraordinary general meetings as per the timelines provided in Regulation 44(3) of the LODR Regulations. However, certain specific details, such as, date of meeting and brief details of items deliberated, should be disclosed within 12 hours as per Regulation 30(6)(ii) of the LODR Regulations. |

| Intimation of forfeiture/restriction on transferability under Para A(2) of Part A of Schedule III | The listed entity shall not be required to make disclosures where the restriction on transferability was a result of operation of any of the statutes or regulations applicable to the listed entity. For instance, the RBI imposes restrictions on change in shareholding of NBFCs beyond 26% without approval of the RBI. Similarly, the Insurance and Regulatory Development Authority of India (IRDAI) has prescribed approval requirements if the holding crosses a certain limit. In such cases, the listed entity would not be required to make disclosures on the restriction on transferability. |