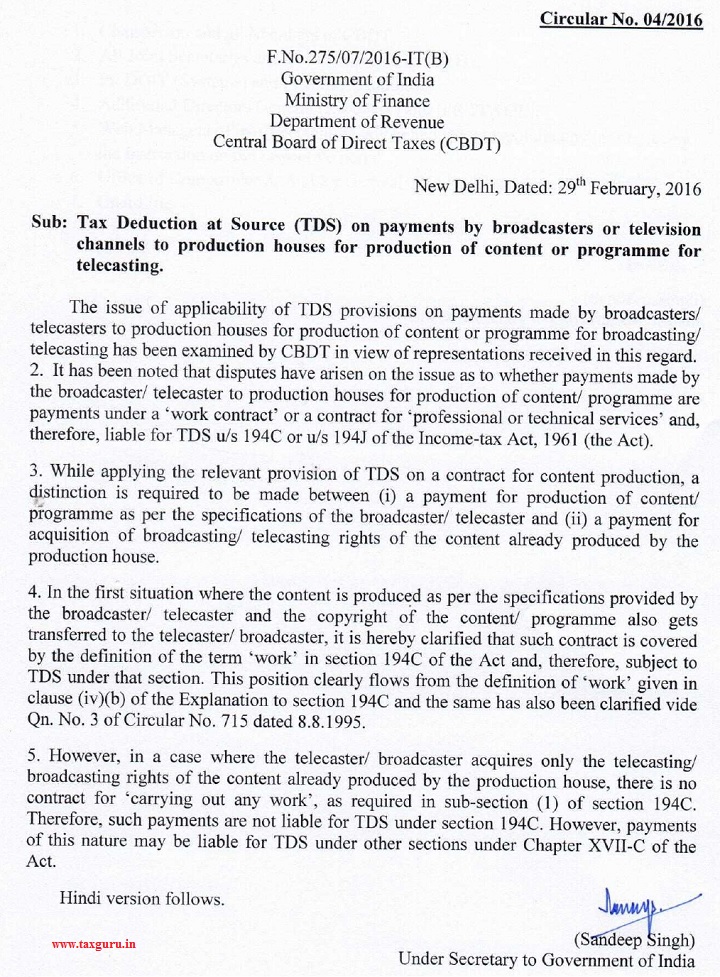

Circular No. 4/2016 dated 29.02.2016 deals with TDS on payments by broadcasters or television channels to production houses for production of content or programme for telecasting. It has been clarified in the Circular that in a situation where the content/programme is produced as per the specifications provided by the broadcaster/telecaster and the copyright of the content/ programme also gets transferred to the telecaster/broadcaster, such contract is covered by the definition of the term ‘work’ in section 194C of the Income-tax Act and, therefore, subject to TDS under section 194C at 2%, rather than at a rate of 10% under section 194J as payment for ‘professional or technical services’.

Circular No. 04/2016

F. No. 275/07/2016-IT(B)

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes (CBDT)

New Delhi, Dated: 29th February, 2016

Sub: Tax Deduction at Source (TDS) on payments by broadcasters or television channels to production houses for production of content or programme for telecasting.

The issue of applicability of TDS provisions on payments made by broadcasters/ telecasters to production houses for production of content or programme for broadcasting/ telecasting has been examined by CBDT in view of representations received in this regard.

2. It has been noted that disputes have arisen on the issue as to whether payments made by the broadcaster/ telecaster to production houses for production of content/ programme are payments under a ‘work contract’ or a contract for `professional or technical services’ and, therefore, liable for TDS u/s 194C or u/s 194J of the Income-tax Act, 1961 (the Act).

3. While applying the relevant provision of TDS on a contract for content production, a distinction is required to be made between (i) a payment for production of content/ programme as per the specifications of the broadcaster/ telecaster and (ii) a payment for acquisition of broadcasting/ telecasting rights of the content already produced by the production house.

4. In the first situation where the content is produced as per the specifications provided by the broadcaster/ telecaster and the copyright of the content/ programme also gets transferred to the telecaster/ broadcaster, it is hereby clarified that such contract is covered by the definition of the term `work’ in section 194C of the Act and, therefore, subject to TDS under that section. This position clearly flows from the definition of `work’ given in clause (iv)(b) of the Explanation to section 194C and the same has also been clarified vide Qn. No. 3 of Circular No. 715 dated 8.8.1995.

5. However, in a case where the telecaster/ broadcaster acquires only the telecasting/ broadcasting rights of the content already produced by the production house, there is no contract for `carrying out any work, as required in sub-section (1) of section 194C. Therefore, such payments are not liable for TDS under section 194C. However, payments of this nature may be liable for TDS under other sections under Chapter XVII-C of the Act.

Hindi version follows.

(Sandeep Singh)

Under Secretary to Government of India

Download Full Circular