Mystic Electronics Ltd. Vs DCIT (ITAT Mumbai)

ITAT Mumbai held that in case of company is involved in providing illicit LTCG/ short term capital loss (accommodation entries), a substantial addition has to be made in the hands of beneficiaries and only a protective assessment can be made in the hands of company providing such accommodation entries.

Facts- The assessee company filed its return of income declaring total income of Rs. 31,51,330/-. Assessee filed a revised return declaring the income at Rs. 35, 48,140/-. Consequently, the case of the assessee was selected for scrutiny and a notice u/s. 143(2) of the Act.

A search and seizure u/s. 132 of the Act was carried out in the case of Raj Kumar Kedia Group. The main allegation was that it is engaged in providing various types of accommodation entries to large number of beneficiaries all over the country.

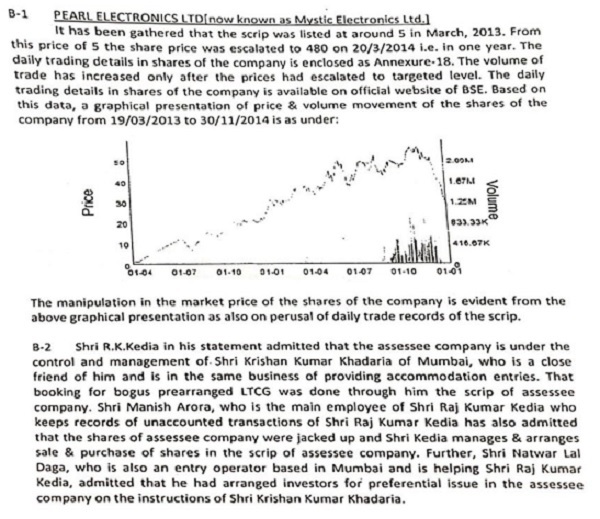

Shri R.K. Kedia in his statement admitted that the assessee company is under the control and management of Shri Krishan Kumar Khadaria of Mumbai, who is a close friend of him and is in the same business of providing accommodation entries. That booking for bogus prearranged LTCG was done through the scrip of Assessee Company.

AO concluded that assessee is a listed company and involved in generating illicit LTCG /short term capital loss. AO added back an amount of Rs. 23,07,50,000/- u/s. 68 received by the company under the head share capital during the year under assessment on the premise that preferential share allotment /warrants is merely a paper transaction and capital is being subscribed by dubious persons. AO further rejected the books of accounts of the assessee u/s. 145 and estimated the income at the rate of 1% i.e. Rs. 23, 44,406/- of total turnover i.e. Rs. 23, 44, 40,568/-. In addition to this, AO further added the income shown under schedule 13 as other income amounting to Rs. 45,44,563/-.

CIT(A) partly allowed the appeal. Being aggrieved, the present appeal is filed.

Conclusion- Held that it is a settled position of law that in such type of transactions unexplained income has to be taxed in the hands of beneficiaries consisting of amount of capital gains and if require the amount of investment made in the shares of assessee company. A substantial addition has to be made in the hands of beneficiaries and only a protective assessment can be made in the hands of company like assessee. In this process, by any reason if the department is not able to tax beneficiary then only a substantial addition can be made in the hands of assessee company. In this case, the only addition which is warranted in the hands of Assessee Company is amount of commission earned on arranging long term capital gains /short term capital losses. If investor in such type of company is able to prove its source of investment, then no addition can be made in the hands of assessee company being genuine transaction as identity, genuineness and creditworthiness is automatically established and in vice-versa position also amount of investment is taxable in the hands of investor, then also not taxable in the hands of assessee company, being double taxation. In view of this, the addition made u/s. 68 amounting to Rs. 23, 07, 50,000/- is unwarranted.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

1. These appeals by assessee and cross appeals by revenue are directed against the order of Ld. CIT (A) – 52. Mumbai dated 27.01.2017 and 27.12.2017 u/s. 250 of the Income Tax Act, 1961 (in short ‘the Act’) for A.Y. 2014-15 and 2015-16 respectively.

2. The assessee has raised the following grounds of appeal in ITA No. 5867/Mum/2019 for AY 2014-15:-

1. The Ld. CIT (A) erred in upholding the validity of assessment made u/s. 143(3) of the Act.

1. i. In doing so, the ld. CIT(A) did not appreciate that

a. the proceedings u/s 143(2) of the Act which were abated pursuant to proceedings initiated u/s 153C of the Act could have revived only if the proceedings initiated u/s. 153C of the Act have been annulled in appeal or any other legal proceedings and will stand revived with effect from the date of receipt of such annulment by the Pr. CIT or CIT which facts are totally missing in the appellant’s case.

b. the appellant did not challenge the power of the AO to drop the proceedings initiated u/s 153C of the Act but what was challenged was his jurisdiction to revive the abated proceedings initiated u/s 143(2) of the Act, and

c. the assessment year under appeal was an abated assessment and not a non-abated assessment as stated by him.

2. The Ld. CIT(A) erred in holding that the assessment made was in accordance with law even if no opportunity was given to the appellant to cross examine the persons whose statements were relied upon in drawing the adverse inference.

3. The ld. CIT (A) erred in confirming the action of the AO in rejecting the books of account and estimating profit for the year at Rs.23, 44, 406/- being 1% of turnover on the ground that the appellant was a penny stock / paper company and it was not engaged in any real business activity ignoring the past history of the case.

3. i. In doing so, the ld. CIT (A) did not appreciate that

a. the AO rejected the books of account and estimated the profit on a ground other than the ground on which show cause was given, which has rendered action of the AO as bad in law,

b. even if the scrip of the appellant company is used by the operators for providing bogus LTCG as alleged, the same cannot be a ground to consider its business transactions as sham,

c. the AO, in rejecting the book results, has neither made any enquiry worth the name with regard to purchases and sales disclosed in the Statement of Profit & Loss nor has established the transactions to be sham or not bonafide.

d. the AO could not have rejected the books of account without establishing the defects, incompleteness and inaccuracies in the accounts of the appellant as required u/s 145(3) of the Act, and

e. the facts in the decisions relied upon by him were totally distinguishable in as much as the courts have upheld the rejection of books of account on the ground of absence of proper documentation and/or non-maintenance of stock register which are not the facts of the appellant and on the contrary the decisions relied upon by the appellant are directly on the point.

3.ii. In any event, the ld. CIT(A) did not appreciate that the AO in rejecting the book results and estimating profit for the year at Rs. 23,44,406/- being 1% of the turnover could not have separately assessed the other operating income of Rs. 45,44,563/-credited to the Statement of Profit & Loss.

4. The ld. CIT (A) erred in confirming the addition u/s 68 of the Act to the extent of Rs. 4,96,87,500/- subject to verification by the AO.

4.i. In doing so, the ld. CIT (A) erred in

a. not appreciating that no formal show cause was given by the AO prior to making the said addition,

b. not appreciating that the addition has been made by the AO solely on the basis of statement of Shri R. K. Kedia and the conclusion of the search action without any independent enquiry being made by him either in the course of assessment proceedings and / or in the course of remand proceedings as was directed to him,

c. ignoring the decisions of the Guwahati High Court & the MP High Court relied upon by the appellant in support of the proposition that the income returned & capital of the share applicants are not the only criteria to judge creditworthiness,

d. laying down a basis/formula for the above addition which is not supported by any express provision of law,

e. following the principles laid down by the Apex Court in the case of NRA Iron & Steel Pvt. Ltd. [412 ITR 161 (SC)] and by the Delhi High Court in the case of D. K. Garg [84 taxmann.com 257] without appreciating that the facts of the said cases are totally distinguishable with the facts of the appellant and in any event while summarizing the principles that emerged from the decision of the Delhi High Court in the case of D. K. Garg (supra) did not appreciate that as per the said decision, the onus cast u/s. 68 of the Act has to be discharged by the dummy concern only in respect of those credits where identity of the depositors is not available while in the case of the appellant, the identity of each of the shareholders is fully established,

f. not appreciating that identity, genuineness & creditworthiness of the persons from whom the share capital of Rs. 4,96,87,500/- was received stood fully established in as much as notice u / s 133(6) of the Act issued in the course of remand proceedings were served on them and they have not only confirmed the transactions but have also furnished their relevant bank statements, balance sheet and acknowledgement for having filed return of income, not appreciating that the appellant being a widely held public limited company its onus under the provisions of section 68 of the Act was fully discharged having regard to the principles laid down by the Apex Court in the case of Lovely Exports Pvt. Ltd. [216 CTR 195(SC)] and Stellar Investment Ltd. [(2011) 115 Taxman 99 (SC)], and

h. not appreciating that neither any incriminating material was found in the course of search action nor any adverse inferences could be drawn merely on the basis of statements of the persons referred to and relied upon by him without bringing any corroborative material in support of the same.

3. Brief facts of the case are that assessee company filed its return of income on 31.11.2014 declaring total income of Rs. 31,51,330/-. Assessee filed a revised return on 31.03.2015 declaring the income at Rs. 35, 48,140/-; however there was no reason on record for revising the return of income. Consequently, case of the assessee was selected for scrutiny and a notice u/s. 143(2) was issued on 19.09.2015.

4. In addition to the facts above, it is pertinent to mention that a search and seizure u/s. 132 of the Act was carried out in the case of Raj Kumar Kedia Group on 13.06.2014 by the DDIT (lnv.), Unit-3(3), Delhi. The main allegation against the group was that it is engaged in providing various types of accommodation entries to large number of beneficiaries all over the country. One of various types of accommodation entries provided by R.K. Kedia group is that of bogus LTCG by pre-arranged trading in shares of various non-descript listed companies, which are under the control and management of the syndicate of entry operators.

5. In the light of above, the case of assessee was centralized to the charge of DCIT, Central Circle – 4(3) The case of the assessee was assigned to this Circle as per order u/s 127(2) passed by the PCIT-10, Mumbai vide order PCIT-10/u/s.127/53/2/2016-17-/1430 dated 16.09.2016.

6. Shri R.K. Kedia in his statement admitted that the assessee company is under the control and management of Shri Krishan Kumar Khadaria of Mumbai, who is a close friend of him and is in the same business of providing accommodation entries. That booking for bogus prearranged LTCG was done through the scrip of Assessee Company. Shri Manish Arora, who is the main employee of Shri Raj Kumar Kedia who keeps records of unaccounted transactions of Shri Raj Kumar Kedia has also admitted that the shares of assessee company were jacked up and Shri Kedia manages & arranges sale & purchase of shares in the scrip of assessee company. Further, Shri Natwar Lal Daga, who is also an entry operator based in Mumbai and is, helping Shri Raj Kumar Kedia admitted while replying the Q.21 during the course of his statement recorded on oath u/s. 132 of the IT Act, on 13.06.2014 that he had arranged investors for preferential issue in the assessee company on the instructions of Shri Krishan Kumar Khadaria.

7. Relevant findings pertaining to the matter as observed by the AO vide page 14 to 16 of assessment order is reproduced herein below:-

B-3 During the course of search, statement of Sh. Krishan Kumar Khadaria has been recorded. However, it is seen from his statement that he could not give any logical explanation as to why the companies in which he is promoter and director, experienced such a huge rise in price of their shares. No attempt of justification in the form of financial strength and/or any sort of potential future prospects/publicity of the companies was made by Sh Krishan Khadaria. When confronted, Sh Khadaria simply explained away such observations by merely submitting that there was no single share transaction belonging directly or indirectly to him in these scrips. In view of this, as discussed earlier, there is no rationale behind such abnormal price rise in the shares of these companies, except a controlled arrangement of manipulated price rise in order to provide profitable exit to the beneficiaries/preferential allottees by providing them accommodation entries of bogus LTCG.

8.4 During the course of post-search enquiries, vide his statement dated 07.08.2014, Sh Rajesh Om Prakash Aggarwal, employee of Shri Krishan Kumar Khadaria, revealed that certain transaction in the scrip of assessee company were carried out on the instructions of Sh Krishan Khadaria, who had strong linkages with Sh R K Kedia. Further, it was also revealed that this share transaction was not for any preferential allotment, but for sale in secondary market, substantiating thereby the allegation that such share transaction was manipulative in order to realize desired result(s) there from. From the above, it gets substantiated that manipulative trading in the shares of M/s. Pearl Electronics Limited has been done by Sh. Krishan Kumar Khadaria in order to provide various accommodation entries such as those of LTCG, LTCL, STCG, STCL etc to different beneficiaries.

B-5 During the course of search, the investigation wing detected that the activities of the assessee company was not real. Moreover, the parties transacting with Pearl Electronics and Pearl Agriculture are found to have no creditworthiness or are under the control of same group. Such arrangement is done in order to show some genuine business activity in these companies, which is not actually the case. No prudent investor would invest in the shares of such a company unless some prearranged desired capital or loss is ensured to such investor. It is found that there are no substantial business transactions taken place in M/s. Pearl Electronics Ltd. and that trading in its shares has been manipulated for providing profitable exit to various beneficiaries by availing them bogus LTCG. The relevant year wise data is placed as under:

|

F.Y. |

Turnover (in Rs) |

PEST (in Rs) |

|

2007-2008 |

Incorporated in August, 2011

|

|

|

2008-2009 |

||

|

2009-2010 |

||

|

2010-2011 |

||

|

2011-2012 |

0 |

0 |

|

2012-2013 |

68,91,87,129 |

4,94,063 |

From the above tabular statement it is clearly seen that there was no reason to support the sharp rise in the price of the shares of the assessee company other than manipulative trading.

8. Based on above observations, AO concluded that assessee is a listed company and involved in generating illicit LTCG /short term capital loss. Based on above findings, AO added back an amount of Rs. 23,07,50,000/- u/s. 68 received by the company under the head share capital during the year under assessment on the premise that preferential share allotment /warrants is merely a paper transaction and capital is being subscribed by dubious persons. AO further rejected the books of accounts of the assessee u/s. 145 and estimated the income at the rate of 1% i.e. Rs. 23, 44,406/- of total turnover i.e. Rs. 23, 44, 40,568/-. In addition to this, AO further added the income shown under schedule 13 as other income amounting to Rs. 45,44,563/-.

9. Assessee being aggrieved with this order of AO, preferred an appeal before the Ld. CIT(A)-52, Mumbai who in turn partly allowed the appeal by sustaining rejection of books of accounts (addition of Rs. 23, 44,406/-) addition of other income (Rs. 45,44,563/-) and sustaining addition u/s. 68 to the extent of Rs. 4,96,87,500/-. Assessee being further aggrieved with this order of Ld. CIT (A) passed u/s. 250 preferred this appeal before us.

10. We have thoroughly gone through the order of AO, order of Ld. CIT (A) and submissions of the assessee alongwith paper book filed. We observed that Assessee Company is a listed entity on the stock exchange, although based on the facts narrated (supra), it is an established fact that the entity was involved in the rigging/manipulation of share price. In these circumstances, assessee company is a conduit for arranging long term capital gains exempted u/s. 10(38) and short term capital losses for various beneficiaries . In this circumstance as the identity of beneficiary are already there with the department, the question of identity, genuineness and creditworthiness for the purposes of section 68 cannot be raised in the case of Assessee Company.

11. it is a settled position of law that in such type of transactions unexplained income has to be taxed in the hands of beneficiaries consisting of amount of capital gains and if require the amount of investment made in the shares of assessee company. A substantial addition has to be made in the hands of beneficiaries and only a protective assessment can be made in the hands of company like assessee. In this process, by any reason if the department is not able to tax beneficiary then only a substantial addition can be made in the hands of assessee company. In this case, the only addition which is warranted in the hands of Assessee Company is amount of commission earned on arranging long term capital gains /short term capital losses. If investor in such type of company is able to prove its source of investment, then no addition can be made in the hands of assessee company being genuine transaction as identity, genuineness and creditworthiness is automatically established and in vice-versa position also amount of investment is taxable in the hands of investor, then also not taxable in the hands of assessee company, being double taxation. In view of this, the addition made u/s. 68 amounting to Rs. 23, 07, 50,000/- is unwarranted. Hence, this amount of addition is directed to be deleted minus addition already, deleted by Ld. CIT (A) amounting to Rs. 18,10,62,500/-. Resultantly, ground no. 4 with its sub grounds is allowed.

12. Ground No. 3 with its sub-grounds pertains to rejection of books of accounts applying provisions of section 145(3) of the Act. We have gone through the order of AO, order of the Ld. CIT(A) and submissions of the assessee. It is observed that to reject books result, AO is duty bound to specify the defects in the books of accounts maintained by the assessee. We have gone through para C2 vide page no. 18 of the assessment order wherein the AO has applied section 145(3) of the Act. For sake of ready reference, we are reproducing the relevant para of assessment order mentioned (supra) as under:-

Addition on account of bogus turnover on estimate basis @ 1%

C-2.1 As discussed in the modus operandi, the penny stock scrips are shown to carry out some form of trading in shares or other commodities so as to create some credentials in its books. The assessee company following this the same modus, has shown fictitious sales at Rs. 23.44 Crore out of bogus purchases booked at Rs. 23.42 crore. All these transactions and figures are fictitious, non genuine and manipulated with sole intention to record desired turnover so as to support the artificial spurt shown in the price of the penny stock at various timelines.

C-2.2 In view of the above discussion, the books of account of the assessee company for the year under consideration are hereby rejected u/s. 145 of the IT Act, since the same do not reflect true and correct trade results. Accordingly, the profit for the is estimated at Rs.23,44,406/- being 1% of total turnover of company shown under the head income from operation’ at Rs. 23,44,40,568/- during the year under assessment Since the assessee has furnished inaccurate particulars and concealed its income, penalty u/s. 271(1)(c) is hereby initiated for the same.

13. With reference to the above findings of AO in the assessment order, it is clearly established that AO was not able to make out the case as required to apply the provisions of section 145(3) of the Act. The findings of AO are cursory in nature may be relevant for other purposes, but to apply section 145, a detail reasoning with specific defects pointed out during the assessment proceedings has to be mentioned and then only provisions of section 145(3) can be applied and the same are missing in the present case.

14. In his order, Ld. CIT (A) confirmed the action of AO and held as under vide para 7.6 page 44 of the appeal order:-

7.6 The assessee has objected to the rejection of the books and estimation of an income on the ground that the reasons recorded in the show cause notice were different from the ones in the assessment order. It is observed that in the show cause notice the AO had pointed out that are no agricultural activities being carried out at Rajasthan and there is also no warehouse existing as was being claimed. It was also pointed out that the purchase/sale parties do not have any creditworthiness. Accordingly, the assessee was asked to show cause as to why it should not be treated as a paper concern with hardly any business activity. It is observed that in the assessment order, while rejecting the books, it has been mentioned that the purchases and sales shown are fictitious. Thus, it is noted that both in the show cause notice as well as the assessment order, the primary ground for rejection of books is that the sales/purchases of the assessee are fictitious and it is not carrying out any actual business activity. As noted earlier, the search action revealed that with certain parties, the assesses has entered into purchase transactions as well as sale transactions which made it obvious that the assessee had undertaken circular transactions to show fictitious turnover. It is also a fact that the assessee did not maintain any warehouse for storing the agricultural produce at Rajasthan which was being claimed by it. In view of such a factual position, the contention of the assessee of rejection of its books and estimation of its income in the assessment order on a ground which was different from the one mentioned in the show cause notice, is found to be erroneous and is therefore, rejected. Accordingly, all the additional grounds of appeal raised by the assessee are dismissed.

15. The findings of the authorities below mentioned (supra) to justify rejection of books of accounts u/s. 145(3) clearly reflects that whatever may be the show cause issued or enquiry conducted leads to specific additions /disallowance u/s 37/69C, etc. Legal position with reference to rejection of books of accounts is altogether different whereas the case made by AO and further confirmed by the Ld. CIT (A) leads the matter towards specific disallowance /addition. We found that revenue is failed to bring material on record which justify rejection of books of accounts leading to application of GP rate @ 1% on total revenue. In view of the above, we direct to delete the addition of Rs. 23,44,406/- being 1% of turnover and other operating income of Rs. 45,44,563/- (as the same is already part of revenue declared by the assessee) and returned income of Rs. 35,48,140/- declared by assessee is directed to be final figure. In the result, ground no. 3 with its sub grounds is allowed.

16. As the matter has been discussed and adjudicated in detail on merits vide ground no. 3 & 4 (supra), now there is no need to adjudicate ground no. 1 and 2 on technicalities of the matter raised by the assessee. Hence, ground no. 1 and 2 left undecided being academic in nature now as ground no. 3 & 4 on the merits of the case has already been decided in favour of assessee and no substantial grievance left. In the result, ground no. 1 and 2 are dismissed.

17. In the result, appeal of the assessee is partly allowed.

ITA No. 929/Mum/2020 (AY 2015-16)

18. Ground no. 2 raised by the assessee has already been discussed and adjudicated in detail vide ITA No. 5867/Mum/2019 for AY 2014-15 in para no. 11. Findings will apply mutatis mutandis here also as the facts of the case and applicable law is similar. In the result, ground no. 2 with its sub grounds raised by the assessee is allowed.

19. Ground no. 3 in this appeal is also identical to ITA No. 5867/Mum/2019 for AY 2014-15. As the same has been discussed in detail and adjudicated. The ratio will apply mutatis mutandis here also. In view of the above, we direct to delete the addition of Rs. 41,264/- being 1% of turnover and other operating income of Rs. 1,28,17,312/- (as the same is already part of revenue declared by the assessee) and returned income of Rs. 83,67,700/- declared by assessee is directed to be final figure. In the result, ground no. 3 with its sub grounds is allowed.

20. As the matter has been discussed and adjudicated in detail on merits vide ground no. 2 & 3 (supra), now there is no need to adjudicate ground no. 1 on technicalities of the matter raised by the assessee. Hence, ground no. 1 left undecided being academic in nature now as ground no. 2 & 3 on the merits of the case has already been decided in favour of assessee and no substantial grievance left. In the result, ground no. 1 is dismissed.

21. In the result, the appeal of the assessee is partly allowed.

ITA No. 6568/Mum/2019 for AY 2014-15

&

ITA No. 1007/Mum/2020 for AY 2015-16

22. The revenue has raised the following grounds in AY 2014-15:-

1. “On the facts and circumstances of the case and in law, whether the Ld. CIT(A) was justified in deleting the addition of unexplained cash credit u/s. 68 to the extent of Rs. 18,10,62,500/- out of Rs. 23,07,50,000/- added by the Assessing Officer in computing the total income.

2. On the facts and circumstances of the case and in law, whether the Ld. CIT (A) was justified in giving relief solely on consideration of identity and creditworthiness of the investor to preferential share capital whereas the addition u/s. 68 was made by the Assessing Officer by holding that the transaction of issuing and allotment of preferential share capital was not genuine.”

The appellant craves to leave, to add, to amend and /or to alter any of the ground of appeal, if need be.

The appellant, therefore, prays that on the ground stated above, the order of the Ld. CIT (A)-52 Mumbai, may be set aside and that of the Assessing Officer restored.

23. The revenue has raised the following grounds in AY 2015-16:-

1. “Whether on the facts and circumstances of the case and in law, the Ld. CIT(A) was justified in deleting the addition of unexplained cash credit u/s. 68 to the extent of Rs. 10,60,58,450/- out of Rs. 14,01,00,800/- added by the Assessing Officer in computing the total income.

2. “Whether on the facts and circumstances of the case and in law, the Ld. CIT (A) was justified in giving relief solely on consideration of creditworthiness of the investor to preferential share capital whereas the addition u/s 68 was made by the Assessing Officer by holding that the transaction of issuing and allotment of preferential share capital was not genuine.”

The appellant craves to leave, to add, to amend and /or to alter any of the ground of appeal, if need be.

The appellant, therefore, prays that on the ground stated above, the order of the Ld. CIT (A)-52 Mumbai, may be set aside and that of the Assessing Officer restored.

24. In both the years vide ITA No. 6568/Mum/2019 for AY 2014-15 and ITA No. 1007/Mum/2020 for AY 2015-16, similar ground were raised by the revenue. As the matter has already been decided in assessee’s appeal vide ITA No. 5867/Mum/2019 and ITA No. 929/Mum/2020, no separate adjudication is required on the grounds raised by the revenue. Matter has been adjudicated in favour of assessee, hence both the appeal of revenue are dismissed.

25. In the result, both the appeals filed by the assessee are partly allowed and both the appeals filed by the revenue are dismissed.

Order pronounced in the open court on 24th day of July, 2023.

but both got monetary benifit . how can you leave main culprit