ITR filling has become an activity which needs NUMEROUS STEPS and we require to ensure multiple checkpoints. These are general steps for ITR 1 TO 5 which are applicable generally to all. Any special/specific income must be treated with own experience & wisdom. Sequencing of these steps may be different from person to person. I am not claiming that this is an Exhaustive list. Hope you all find it Useful. Please Let me know any important steps left in these.

CHECK 33 STEPS BELOW

|

DOCUMENTS |

|

| 1

|

Make sure to have all COPIES OF FOLLOWINGS DOCUMENTS & CHECK EVERYTHING IN ONE GO to decide the SCOPE OF WORK

1. Balance sheet , Profit Loss A/c , Capital A/c , Fixed Asset Ledgers , Indirect Incomes ledgers , If Partner in any Firm then Partner’s Capital A/c 2. 26AS + TIS +AIS 3. Salary Certificate, Agriculture Income Proofs , Bank statements , Interest certificate from SB Bank / FD/ Bonds / MIS / Post etc. 4. If there is sale of shares/ MF, then ask Profit/loss report from Broker. Decide what is LT / ST & INTRA DAY 5. Details of Capital Gain from sale of any property/Gold/capital assets 6. For Audit case , Do check Capital Account from BOOKS because Audit report does not have all Information 7. All Investment proofs – ,L.I.C. & U.L.I.P. Premium paid receipts ,Mediclaim Receipt , Housing Loan Repayment Certificate ,Donation receipts, ,School / College Tuition Fees receipts . (Only tuition fee & Not for any other activity) ,PPF Pass book duly filled up up to MARCH including Interest entry ,N.S.C, KVP . Purchased Proof ,contri to NPS proof |

| PRE-CHECKING | |

| 2 | FOR NON PRESUMTIVE & NO AUDIT CASE , Check MIN 6% / 8% – Income from B&P after reducing IFOS /CG / HP income – For any Business Assessee – |

| 3 | IF PRESUMTIVE U/S 44AD/44ADA/44AE THEN – For eligibility of Presumptive check last year return. Also check 5 year continuity Rule |

| 4 | If last year ITR filed having Business Losses , Then do check 143.1 of last year to confirm Loss Amount |

| 5 | In case of partnership firm , Do add All partners details PAN +AADHAR + PERCANTAGE in Partners details IN PARTNER MASTER |

| 6 | MASTER update in SOFTWARE –> ADDRSS , PIN CODE , PHONE NUMBER , MOBILE NUMBER , WARD , EMAIL ID , AADHAAR NUMBER |

| ONLINE ACTIVITY | |

| 7 | LOGIN & IMPORT 26AS txt file in software. ( We still yet to make all entries but I PREFER doing this first) |

| 8 | Open AIS TIS Remain Logged in , We will come back to AIS TIS in later steps |

| COMPUTATION in Business & Profession | |

| 9 | start with Net profit in BP head – Add back all Disallowed expenses |

| 10 |  |

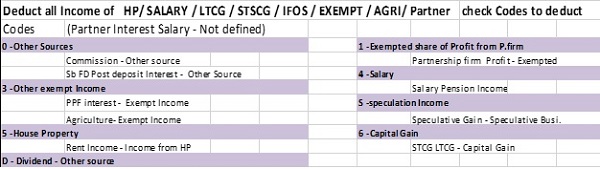

| 11 | Now , Add back same Income in other heads – HP/ SALARY / LTCG / STCG / IFOS / EXEMPT / AGRI/ Partner . whichever heads applicable ( Property sale , Sale of share transactions etc may not be in BOOKS OF ACCOUNTS so identify and make entries in SOFTWARE) |

| OTHER HEADS AND IMPORTANT ENTRIES IN SOFTWARE – THESE ARE REALLY IMPORTANT | |

| 12 | DEDUCTIONS – 80C/80G/80D/80CCD/80U/80DD ETC |

| 13 | Audit special– Check Whole report thoroughly – Make sure check all clauses of 3CD FOR KNOWING ALL DISALLOWANCE / REPORING AND DEDUCTIONS IN CASE OF Individuals |

| 14 | 26AS + TIS + AIS SPECIAL – to check them thoroughly-Identify incomes which need to show over And above what client has given – make sure All incomes are covered – |

| 15 | Code selection For TDS / TCS credit – We have to select proper code , If Income of 94A/94I/94J/94H is for business then Select Business otherwise Other source |

| 16 | LT ST Gains (if any ) of shares if any – Check AIS TIS on Portal .. Download CSV file … if there sale of Shares then ask client about l LT ST sale of shares /MF and intraday trading profit.. For LT, import CSV file in software.. If client does not provide THEN u have to use figures of AIS TIS |

| 17 | BALANCE SHEET & PROFIT LOSS ( DO match Depreciation and Other incomes in PL must be in specific head only ) |

| 18 | ITR 4 SPECIAL (PRESUMTIVE WHEN NO BOOKS) -Four financial parameters – CASH + DRS + CRS + CASH BALANCE. Compulsory need to write.. In case of Profession , Do enter , Receipts details |

| 19 | GST NO & GST Turnover |

| 20 | NATURE OF BUSINESS

CODE SELECT DESCRIPTION – TRADING IN THIS ITEMS NAME OF BUSINESS |

| 21 | BUISNESS & AUDIT INFO-

Nature of Activity METHOD OF ACCOUNTING RM/FG STOCK METHOD BOOKS 44AA YES |

| 22 | Audit special – BUSI. & AUDIT INFO – WRITE AUDITORS DETAILS & DATE OF TAR & FURNISH OF TAR DATE |

| 23 | Audit special – OTHER INFORMATION OF 3CD. IN CASE OF AUDIT IF ANYTHING DISALLOWED IN REPORT |

| 24 | If Shareholder / director in any Company then Write opening + closing of Unlisted shares details. Compulsory |

| 25 | IMPORTANT POINTS |

| 1. for Speculative Business , You have to Show in Normal then deduct from Normal and Then show in Speculative Business | |

| 2. for STCG – LTCG , Do not show straight way Profit Loss , Make sure to write Sale Purchase amount and then derive Profit Loss | |

| 3. Carried Forward Loss must be bifurcated between Business loss & Unabsorbed Deprecation | |

| 4. If 26AS is showing LIC maturity then write amount in Exempt Income if it is exempted, Otherwise in Other source ( Chek whether TDS deducted) | |

| COMPUTATION & TAX PAYABLE | |

| 26 | Check Computation and make sure all incomes are Properly Shown head wise. From AIS/TIS & books. For all other incomes which is also reflected in AIS TIS , Makes sure Incomes in final Computation must be EQUAL TO OR higher than AIS TIS figure |

| NOTE- Generate computation AS ON DATE , This is useful when Return prepared in last month and upload in Next month due to challan payable .(If challan , then It will change Interest and if Refund , It will reduce Refund) | |

| 27 | Option for new Scheme – If there is any tax payable then do check OPTION as per NEW SCHEME |

| 28 | If Tax payable, Print challan. After payment of tax, enter challan details. |

| AT TIME OF UPLOADING | |

| 29 | Now NAME should match at all places – 1. Master 2. Online Profile 3. Verification screen when uploading |

| 30 | If Refund, please write correct Bank account – SB. If last year refund failed then , make correction in bank details |

| 31 | FOR 3 QUESTIONS – if TO 1 CR TO 10 CR =YES/NO + cash< 5%= NO + cash <5%= NO |

| 32 | after upload save COMPUTATION & ITR V AND make BILLS & RECEIPTS ENTRY |

| 33 | E-VERIFY |

In case of Refund Dont forget to Bank account be Validated and EVC Enabled. I prefer E-verification through EVC.