1. Introduction

Recent amendments in section 115BBE emerge from the seesaw battle between the government and the assessees who leaves no stone unturned to evade taxes and between these skirmishes the honest taxpayer is often overripen in this heat of revenge. The provisions of section 115BBE of the Act are draconian at first glance and can give nightmares to assessee. These provisions cannot be applied in a lackadaisical way or perfunctory manner. This section erodes the faith of the taxpayer in Income Tax Law since this section is applied retrospectively from April 2016. This section is tool in the armory of the tax officials which they are using without giving much thought and weight over other issues. The provisions of section 115BBE of the Act cannot be made applicable in routine and light-hearted manner and full zoom view of the facts has to be seen. This section needs to be applied with a lot of circumspection regarding true nature of the income. The facts need to be seen in a very holistic, unbiased and objective manner. The implication of this section has increased in the post demonetization period.

Subsequent to demonetisation announced on 8th November 2016, there were views expressed by professionals that the undisclosed income held in the form of demonetised currency can be deposited in the bank and the said amount can be offered for taxation under specified sections. Consequently, tax on the said income may be paid under section 115BBE @ 30% plus applicable surcharge and cess and in which case, the person may not be subject to penalty. It was with a view to prevent such practice and to overcome the views expressed, the amendments has been made to section 115BBE of the Act. Chapter II of the Taxation Laws (Second Amendment) Act, 2016 amended existing provisions of sections 115BBE and also introduces a new section 271AAC in the Act. But these unhealthy amendments in sec 115BBE have led to an unintentional proliferation of litigation. The amendments made by the Amendment Act are applicable with effect from AY 2017-18 and therefore, for AY 2017-18, though Amendment Act was enacted on 15.12.2016, the amendments apply to– income under Specified Sections from 1st April, 2016 to 8.11.2016; income under Specified Sections during 8th November, 2016 to 30th December, 2016.To start our discussion on this issue, let us understand the provisions of sec 115BBE of the Act.

Section 115BBE as applicable w.e.f. 1-4-2017 [i.e. A.Y. 2017-18]

(1) Where the total income of an assessee,—

(a) includes any income referred to in section 68, section 69, section 69A, section 69B, section 69C or section 69D and reflected in the return of income furnished under section 139; or

(b) determined by the Assessing Officer includes any income referred to in section 68, section 69, section 69A, section 69B, section 69C or section 69D, if such income is not covered under clause (a), the income-tax payable shall be the aggregate of— (i) the amount of income-tax calculated on the income referred to in clause (a) and clause (b), at the rate of sixty per cent; and (ii) the amount of income-tax with which the assessee would have been chargeable had his total income been reduced by the amount of income referred to in clause (i).

(2) Notwithstanding anything contained in this Act, no deduction in respect of any expenditure or allowance or set off of any loss shall be allowed to the assessee under any provision of this Act in computing his income referred to in clause (a) and clause (b) of sub-section (1).

Page Contents

- Salient features of section 115BBE –

- 2. Retrospective Amendment –A Nail in the Coffin

- 3. REGULAR CASH SALE CONVERTED AS UNEXPLAINED CASH CREDIT

- 4. Applicability of Section 115BBE in case of surveys u/s 133A of the Act

- 5. Inordinate delay in deposit of cash from withdrawals ie. 5-6 months from

- 6. Applicability of sec 69C in case where the assessee has adopted presumptive tax system

Salient features of section 115BBE –

a) All assessees-Theamended Section applies to all assessees irrespective of the legal status i.e. it applies to individuals, HUFs, firms, LLP, cooperative society, AOP, BOI, political party. It applies to residents as well as nonresidents. It also covers all assessees adopting presumptive taxation under Sections 44AD / 44ADA / 44AE

b) No Threshold Limit:-The section applies irrespective of the minimum threshold limit i.e. the section applies to even a small amount of Rs. 1,000 if the amount is chargeable as income under the provisions of sections 68, 69, 69A, 69B, 69C and 69D (“specified sections”).

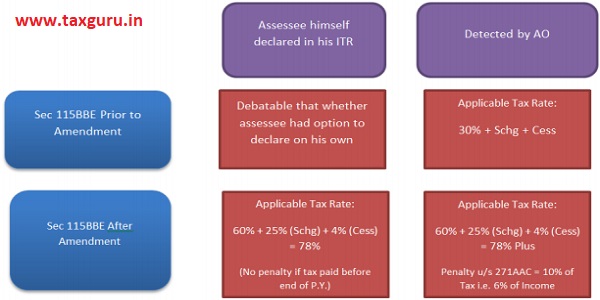

c) Option to show in Return of Income:-Itis now clear that items which could have been taxed by the provisions of specified sections can also be offered for taxation by the assessee in his return of income by paying tax, on or before the end of the previous year, at the rates mentioned in section 115BBE.

d) Tax Rate:-The income referred to in Section 68, 69, 69A, 69B, 69C or 69D is taxable @ 60% u/s. 115BBE of the Act plus a surcharge of 25% and education cess of 4% for the assessment year 2020-21.Thus the effective rate of income tax comes to 78%.

e) Set Off of Loss:-Sub-section (2) of section 115BBE begins with a non-obstante clause and provides that non-deduction in respect of any expenditure or allowance or set off of any loss shall be allowed to the assessee under any provision of this Act in computing his income referred to in clause (a) of sub-section (1). Since the term ‘or set off of loss’ were inserted in sec 115BBE( 2) w.e.f. 01.04.2017. Hence, benefit of set off loss against income declared u/s 115BBE of the Act will not be available from AY 2017-18. This has been made clear by CBDT in Circular No. 11/2019 dated 19th June, 2019 that the amendment is prospective and applies w.e.f. 1.4.2017 i.e. AY 2017-18 onwards. In view of the above, upto AY 2016-17, assessee is entitled to claim set off of losses against income assessed as deemed income under Specified Sections as per provisions of S. 115BBE of the Act.

f) Penalty:- Penalty under section 271AAC is leviable if the following conditions are satisfied.

a) The total income determined includes any income referred to in the specified sections; and

b) the income referred to in the specified sections has not been included in the return of income furnished under section 139; or tax on income referred to in specified sections, in accordance with provisions of section 115BBE(1)(i) has not been paid on or before the end of the relevant previous year.

c) If the above conditions are satisfied then the AO may direct that the assessee shall pay a penalty in addition to tax payable under section 115BBE. The quantum of penalty will be ten percent of the tax payable under clause (i) of sub-section section (1) of section 115BBE.

Now a question arises as to whether the 10% is on tax rate of 60% or on the aggregate of tax rate (of 60%) plus surcharge thereon (25% of 60%) i.e. whether the 10% is to be computed on 60% or 75%. While it is true that the Supreme Court has held that tax in the case of CIT v. K

Srinivasan *83 ITR 346 (SC)+ held that “tax includes surcharge”. But considering the language of the provision which reads as that the assessee shall pay by way of penalty, in addition to tax payable under section 115BBE, a sum computed at the rate of ten per cent of the tax payable under clause (i) of sub-section (1) of section 115BBE of the Act. Hence, the rate of 10% is to be applied to tax of 60%.and not on surcharge of 25%.

g) Restriction on deductions under Chapter VI-A –

The provisions of Sub-section (2) of section 115BBE restricts deduction in respect of any expenditure allowable to the assessee under any provision of the Act. This is not to be confused with deductions admissible in computing ” Total Income” under Chapter VI-A. In the case of an assessee having income referred to in section 115BBE and no other income, while determining the ” Total income”, deduction under Chapter VI-A appears to be admissible. This will result into a lower ‘Total income’ as compared to income determined u/s 115BBE. However it is a debateable issue as the word deduction used in sec 115BBE of the Act does not make the things clear .In our considered opinion, assessee can claim deductions under chapter VI-A of the Act. The word ‘deduction’ used in the section indicates deductions from income from other sources and not deductions from gross total income.

2. Retrospective Amendment –A Nail in the Coffin

A farmer is engaged in producing 100 kg of wheat of which 50 kgs are sold by him in the market, 20 kgs are kept for his own consumption for the coming six months and 30 kgs in the shape of legitimate tax are handed over by him to the king’s Minister. After six months king’s Minister collecting taxes in the shape of wheat advises to king that some of the farmers have managed to cheat king’s empire so each one of them though honest should be punished that 100 kg of more produce pertaining to that faulty produce should be given to the treasury of the king. The farmer requests before the king that the wheat was his rightful food at the time of consumption so he and his family has consumed it and for the remaining six months they will manage with the profits of produce they sold, so now how he will pay off his debt towards the king treasure. King was sympathetic and orders his ministers to change the law as this is not the correct way of punishing those practicing malpractices. The King explains how we can ask someone to pay that which was his right at the time he consumed it. Now we are asking to give us anyhow just by changing law at a later date. If such things continue, people in my State will never be able to eat due to the retrospective amendment in the law and will not be able to pay off the debts.

The provisions of sec 115BBE have been amended by the the by Taxation Laws (Second Amendment`) Act, 2016 wef 01/04/2017 i.e. AY 2017-18 relevant to PY 2016-17 which received the assent of President of India on 15.12.2016. Now a question as to whether it is retroactive since it covers cases where income of the nature referred to in specified sections pertains to the period from 1st April 2016 to 8th November 2016. In other words, is the section applicable to acts done before its enactment. It is well settled rule of interpretation allowed by time and sanctified by judicial decisions that retrospective operation should not be given to a statute so as to effect, alter or destroy an existing right or create a new liability or obligation. If the enactment is expressed in language which is fairly capable of either interpretation, it ought to be construed as prospective only as per ratio of Hon’ble Supreme Court in the case of Govinddas Vs. ITO, (1976) 103ITR 123 (SC). A statute is retrospective when it takes away or impairs any vested right acquired under the existing laws, or creates a new obligation, or imposes a new duty, or attaches a new liability in respect of transactions or considerations already past. A substantive law determines the rights and liabilities of the parties concerned, whereas procedural laws govern the manner in which such rights or obligations are to be enforced or realized. A law applicable to the assessment is the law as it stands in the year of assessment and not that during the year in which the income was earned.

In Karimtharuvi Tea Estate Ltd. v. State of Kerala*1966+ 60 ITR 262 (SC), it was held: “. Now, it is well-settled that the Income-tax Act, as it stands amended on the first day of April of any financial year must apply to the assessments of that year. Any amendments in the Act which come into, force after the first day of April of a financial year, would not apply to the assessment for that year, even if the assessment is actually made after the amendments come into force.”

In this matter, the reference may be made to the Supreme Court decision in the case of CIT vs. Scindia Steam Navigation Co. Ltd. [1961] 42 ITR 589 wherein it was held that total income has to be computed in accordance with the law existing as on 1st day of the assessment year. The validity of this amendment to section 115BBE by the Taxation Laws (Second Amendment) Act, 2016 has been challenged before the Jodhpur bench of the Rajasthan High Court in Deepak Maratha v. UoI, through the Ministry of Finance & Anr (Civil Writ Petition No. 3625/ 2020).. The Writ Petition is pending for hearing.

3. REGULAR CASH SALE CONVERTED AS UNEXPLAINED CASH CREDIT

In practical life, we see that certain sectors like jewelry, liquor, grocery,sweets, electronics have high cash sales. In most of the cases, the details of customers are not available with the assessee and same is also not required under the Act to keep the records of customers to whom cash sales have been made. But with effect from 01.07.2011, in case of sale of jewelry, seller as to obtain the PAN of all the buyers to whom sales have been made above a specified limit. Now a question arises that in case of an assessee, if these sales have been entered into the books of account. Can the same can be put to tax u/s 68 of the Act.During the course of scrutiny assessments for the assessment year 2016-17, It has been observed that while making assessments, cash deposited by the assessee during demonetization period out of the cash sales made in pre demonetization period, some assessing officers have made addition under various sections of the Income Tax Act, 1961. In many cases, it seems that AO had added cash deposited during the Demonetization period, on the pretext that Assessee has created an artificial scenario in its books of account. Where unaccounted income was introduced by showing them as cash sales or cash in hand which was then deposited into the bank account conveniently and craftily after 08.11.2016.

In the case of a cash transaction where delivery of goods is taken against cash payment, it is hardly necessary for the seller to bother about the name and address of the purchaser. In our opinion . the addition made by the assessing officer is not justified at all. In such cases, it appears, that the assessing officers have approached the matter on certain surmises and conjectures.

To resolve this issue firstly let us read Section 68 which is as follow:-

“68. Where any sum is found credited in the books of an assessee maintained for any previous year, and the assessee offers no explanation about the nature and source thereof or the explanation offered by him is not, in the opinion of the Assessing Officer, satisfactory, the sum so credited may be charged to income-tax as the income of the assessee of that previous year :”

The object of Section 68 is to bring items which are not offered for taxation to tax as income and this object is evident from the language of Section 68 which reads “…………………………….the sum so credited may be charged to income-tax as the income of the assessee of that previous year :”

From the reading of the above sec 68 of the Act,it is clear that Section 68 is to tax something clandestine, something which has been hidden by the assessee. Not something which is apparent, not something which has been credited in the books of account of the assessee. In other words,we can say that if cash sales,which have been duly credited in the profit and loss account of the assessee, cannot be taxed u/s 68 of the Act. If it is put to tax,it will lead to double taxation.

From the above discussion ,we conclude:-

(i) sales can be in cash and it is hardly necessary for the seller to bother about the name and address of the purchaser ;

(ii) so long as the availability of stock is there and there is nothing adverse against the cash memos issued by the assessee, such cash sales cannot be doubted;

(iii) It is but natural that if a customer makes cash purchase and lifts the goods there is no duty cast upon the seller to insist for the address of the purchaser;

(iv) the assessee has himself offered the amount of cash sales as his income by duly including it in his total sales – once a particular amount is already offered for taxation, it cannot be again considered u/s 68 of the Act;

(v) thus, any addition cannot be made by treating cash sales as bogus.

The same view is upheld in following judgements:-

Delhi Hight Court in CIT v. Kailash Jewellery House ITA No. 613/2010 decided on 09.04.2010 In the facts of above case cash of Rs.24,58,400/- was deposited in bank account. The Assessing Officer made the addition on the ground that nexus of such deposit was not establish with any source of income. The assessee claimed that it was duly recorded in the books on account of cash sales and was considered in the Profit and Loss Account. The Assessing Officer had verified the stock and cash position as per books and had accepted the same. Complete books of account and cash book were submitted to the Assessing Officer and no discrepancy was pointed out. On this basis CIT(A) deleted the addition. Tribunal also observed that it is not in dispute that sum of Rs.24,58,400/- was credited in the sale account and had been duly included in the profit disclosed by the assessee in its return. Therefore, cash sales could not be treated as undisclosed income and no addition could be made once again in respect of the same. The Hon’ble High Court dismissed the appeal filed by the Department.

M/s Singhal Exim Pvt. Ltd. v. ITO ITA No. 6520/Del/2018 decided by ITAT Delhi on 12.04.2019 Assessee was importing mobile phones from China. Most of the time it was making sales of the goods when in transit by way of high sea sales. During the year total turn-over was Rs.62.91 crores out of which high sea sales were of Rs.59.11 crores. Sale consideration for high sea sales was received in cash. The assessee was having meager finances and was purchasing the goods on credit and was making the payment after the sale. The Assessing Officer with a view to verify the transactions of high sea sales issued notices to the buyers which were returned by postal authorities with remarks “left or not exist”. The Assessing Officer on this basis made addition of Rs.59.11 crores u/s 68. Held by the Tribunal that Section 68 was not applicable. Goods have been duly imported there have been custom clearances for the same. There were agreements for sale of the goods on high sea basis. Once the goods have been sold, the buyer became the debtor and any receipt of money from him is the realization of such debt. Therefore, Section 68 cannot be applied.

The ITAT Ahmedabad in the case of Shree Sanand Textiles Industries Ltd. Vs DCIT (ITAT Ahmedabad All ITAT (6725) ITAT Ahmedabad (465) dated 01/01/2020has harped upon the mechanical practices adopted by the Assessing Officers to make addition u/s 68. The moot point is that a sale which already forms part of books of account cannot be added again u/s 68 due to the reasons that Sales are already recorded in the books of accounts and the addition of the same amounts to double taxation.

A prejudiced view on sale cannot be drawn when purchases are accepted without any reservation.

Section 68 connotate amount credits in books of account remained unexplained need to be added. Recorded sales are not unexplained cash credits.

The same view has been held in Agons Global P Ltd V/S Acit (Appeal No 3741 To 3746/Del/2019.”

Dewas Soya Ltd, Ujjain V/S Income Tax (Appeal No 336/Ind/2012 the Ld. Indore Bench “s Delhi High Court in the case of CIT v. Jindal Dyechem Industries Pvt. Ltd.

4. Applicability of Section 115BBE in case of surveys u/s 133A of the Act

In the case of survey conducted by the Income Tax department u/s 133A of the Act, certain assets or incriminating documents are found which are not disclosed in the books of accounts and resultantly the assessee offer the same for taxation under the Income Tax Act as an additional income over and above the normal income of the assessee. The said offer is made with the department in order to buy peace of mind and to avoid litigation with the Income Tax Department. This offer is always subject to no penalty by the assessee. Now a question arises as to whether the amounts surrendered on the basis of incriminating papers / assets found are chargeable to tax by virtue of provisions of Specified Sections and therefore attract the rate of tax mentioned in Sec. 115BBE of the Act or is it that these amounts are taxable under the head `Profits & Gains of Business or Profession’ or `Income from Other Sources’. In this connection, the assessee has to prove that the amounts are earned in the course of business. The onus is on the assessee to establish the source of the surrendered income failing which it is to be categorized as deemed income u/s 69/69A/69B/69C of the Act. It is to be observed that whether or not additional income surrendered during the course of survey is feasible as income from business or not is essentially a question, which has to be decided having regard to the particular facts and circumstances of each case. Ostensibly, there cannot be an absolute proposition that any income surrendered during the survey is a business income or vice versa

From the above discussion, If we closely observe that in invoking provisions of sections 69, 69A, 69B & 69C, two conditions are required to be satisfied. They are (i) investment/expenditure are not recorded in the books of account of assessee & (ii) the nature and source of acquisition of assets or expenditure are not explained or not explained satisfactorily the expression “nature and source” used in this section should be understood to mean requirement of identification of source and its genuineness. To explain “Nature” it would require the assessee to explain what is description of investment or expenditure, period and the manner in which it was done. To explain the source it would require the assessee to explain the corpus or fund from where investment or expenditure has been met and also the head under which the investment or expenditure would fall such as whether investment/expenditure pertains to business or relates to acquisition of capital asset or to other source or to agriculture. In this connection it is further submitted that where source of investment/expenditure is clearly identifiable and alleged undisclosed asset has no independent existence of its own or there is no separate physical identity of such investment/expenditure then first what is to be taxed is the undisclosed business receipt invested in unidentifiable unaccounted asset and only on failure it should be considered to be taxed under section 69 on the premises that such excess investment is not recorded in the books of account and its nature and source is not identifiable . It can be explained with an example that excess stock found during survey operation is not separately and clearly identifiable but is part of mixed lots of stock found at the premises of the assessee which included declared stock as per books and also the excess stock as computed by the Authorized Officers during the survey operations at the premises. Since excess stock is a result of suppression of profit from business over the years and has not been kept identifiable separately but is the part of overall physical stock found, the investment in the excess stock has to be treated as business income.

It is to be noted that once such excess investment is taxed as undeclared business receipt then taxing it further as deemed income under section 69 would not be find out link of undeclared investment/expenditure with the known head, give opportunity to the assessee to establish nexus and if it is satisfactorily established then it should be considered as deemed income under section 69,69A,69B, & 69C as the case may be. It should not be done at the first instance without giving opportunity to the assessee to establish nexus. In case of survey u/s 133A it is to be noted that once a specific surrender made by the assessee has been accepted by the Income Tax department as business income and tax on the same has been realized, the department cannot take a U turn while framing the assessment of the assessee by taxing the same under the head Income from other sources under Section 69, 69A and 69B. It has to be assessed under the Head Income from Business.

In the following cases income surrendered / detected the course of survey was held to be taxable as Business Income –

Construction Portal Pvt. Ltd. v. ITO [ITA Nos. 1607 & 1608/Pun/2014; Assessment Years: 2005-06 & 2006-07; Order dated 6.6.2018]

SAB Industries Limited v. DCIT [ITA No. 848/Chd./2017; Assessment Year: 2013-14; Order dated 28.3.2018]

Gaurish Steels (P.) Ltd. v. ACIT [(2017) 82 taxmann.com 337 (Chandigarh – Trib.)]

Shri Ram Swaroop Singhal, … vs Acit, Circle, Sriganganagar

Shri Lovish Singhal Vs Income Tax Officer (ITAT Jodhpur) ITA No. 143/Jodh/2018

Dcit, Ludhiana vs M/S C.L. Engineering Limited, … ITA NO. 204/Chd/2017

Dcit, Ludhiana vs M/S Marshal Machines Pvt. Ltd., ..ITA No.57/Chd/2017

Rajasthan high court in the case of Bajrang Traders in Income Tax Appeal No. 258/2017 dated 12/09/2017 has held that excess stock found during the course of survey and surrender made thereof is taxable under the head ‘business and profession.

In the following cases it has been held that income detected / surrendered in the course of search / survey is taxable under Specified Sections –

Radheshyam Totaram Narayani v. ACIT [ITA No. 1491/Pun/2015; AY 2010-11; Order dated 21.3.2018]

Kim Pharma Pvt. Ltd. v. CIT [35 taxmann.com 456 (P & H. HC)] Satish Kumar Goyal v. JCIT [70 taxmann.com 382 (Agra-Trib.)]

In each of the above mentioned cases, the assessee was not in a position to explain the source of cash found.

5. Inordinate delay in deposit of cash from withdrawals ie. 5-6 months from

It has been noticed that some assessing officers have made additions u/s 68 of the Act in cases where the assessee has withdrawn the sum in pre demonetization period and redeposited the same in post demonetization period. In some of the cases,the assessing officers have made additions that the time gap between withdrawal or deposit is longer.In this connection,it is submitted that no addition can be made u/s 68 on the sole reason that there is a time gap of 5 months between the date of withdrawals from bank account and redeposit the same in the bank account , Unless the AO demonstrate that the amount in question has been used by the assessee for any other purpose. On this issue following case laws can be considered.

CIT v. Kulwant Rai (2007)291 ITR 36 (DEL)

DCIT v. Smt. Veena Awasthi ITA No. 215/ LKW/2016 decided by ITAT Lucknow Bench on 30.11.2018

Neeta Breja v. ITO ITA No. 524/Del/2017 decided by ITAT Delhi on 25.11.2019

Moongipa Investment Ltd. vs. ITO (2016) (Tax Appeal No. 1106 of 2006 dated 07/06/2016) (Guj)

6. Applicability of sec 69C in case where the assessee has adopted presumptive tax system

The basic edifice of presumptive scheme u/s 44AD is assessee would not be called to maintain books under the Act and get them audited if profit shown by assessee is otherwise in accordance with prescription of section 44AD of the Act. Now a question arises whether these deposits in bank can be transformed as unexplained cash credit u/s 68 of the Act.

Firstly section 68 is a deeming fiction and same needs to interpreted in felicitous words from a ITAT verdict that deeming fiction relates to that branch of jurisprudence which needs to be narrowly watched , zealously regarded and never to be pressed beyond its true limits.

Secondly section 68 requires existence of books and actual credit therein which are jurisdictional fact and without any books and without any credit therein, section 68 can’t be pressed dearer to revenue due to its castigating In other words when a deeming fiction like section 68 is applied it is not allowable to deem that books are there or credit is there when same is otherwise lacking ex-facie. If deeming within deeming provision is allowed then it may lead to absurdity.

To resolve this issue,firstly we have read the provisions of Sec 44AD of the Act.Sec 44AD reads as

“44AD (1) Notwithstanding anything to the contrary contained in sections 28 to 43C, in the case of an eligible assessee engaged in an eligible business, a sum equal to eight per cent of the total turnover or gross receipts of the assessee in the previous year on account of such business or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the eligible assessee, shall be deemed to be the profits and gains of such business chargeable to tax under the head “Profits and gains of business or profession”.

(2) Any deduction allowable under the provisions of sections 30 to 38 shall, for the purposes of sub-section (1), be deemed to have been already given full effect to and no further deduction under those sections shall be allowed :”

The provisions of the above section are quite unambiguous to the effect that in case of an eligible business based on the gross receipts/total turnover, the income under the head ‘profits & gains of business’ shall be deemed to be @ 8% or any higher amount. The first important term here is ‘deemed to be’, which proves that in such cases there is no income to the extent of such percentage, however, to that extent, income is deemed. It is undisputed that ‘deemed’ means presuming the existence of something which actually is not. Therefore, it is quite clear that though for the purpose of levy of income tax 8% or more may be considered as income, but actually this is not the actual income of the assessee. This is also the purport of all provisions relating to presumptive taxation.

Putting the above analysis, in converse, it can be easily inferred that the same is also true for the expenditure of the assessee. If 8% of gross receipts are ‘deemed’ income of the assessee, the remaining 92% are also ‘deemed’ expenditure of the assessee. If the income component is estimated, how the expenditure component on the basis of said income can be considered to have been ‘actually incurred’ and it is only presumption that an amount of 92% of gross receipts was incurred by the assessee as expenditure.It means that actual expenditure may not be 92% of gross receipts, only for the purposes of taxation, it is considered to be so. To take it further, it can be said that the expenditure may be less than 92% or it may also be more than 92% of gross receipts.The crucial words in the said section are ‘any financial year an assessee has incurred any expenditure’. But can we say on the facts and circumstances of the case that the assessee has ‘incurred’ any expenses.

From an analysis of section 44AD of the Act contained hereinabove, we have noted that the assessee had not incurred the expenses to the extent of 92 % of the gross receipts. Therefore, the provisions of section 69C of the Act cannot be applied. Asking the assessee to prove to the satisfaction of the Assessing Officer, the expenditure to the extent of 92% of gross receipts, would also defeat the purpose of presumptive taxation as provided under section 44AD of the Act or other such provision. Since the scheme of presumptive taxation has been formed in order to avoid the long drawn process of assessment in cases of small traders or in cases of those businesses where the incomes are almost of static quantum of all the businesses, the Assessing Officer could have made the addition under section 69C of the Act, once he had carved out the case out of the glitches of the provisions of section 44AD of the Act. This view has been taken by CHANDIGARH BENCH Of ITAT in Nand Lal Popli v.Deputy Commissioner of Income-tax Central Circle-II, ChandigarhIT APPEAL NOS. 1161 & 1162 (CHD) OF 2013[ASSESSMENT YEARS 2007-08 AND 2009-10]

CA R.S. Kalra (98889-27000, ca.rskalra@yahoo.com)

CA Jasmeet Singh (86997-01271, jasmeetsingh1699@gmail.com)

Author Bio