In India the Income of a person is taxed through the provisions made in Income tax act 1961 read with Income tax rules 1962.The charge of the tax in India is primarily based on the residential Status of the person. A person can be a “Resident and ordinarily resident” or “Resident but not ordinarily resident” or “Non resident” depending upon the no of days of stays in India (In some cases there is also citizenship based taxation). While the global income of the person who is “Resident and ordinarily resident” is taxable in India, the income of a non resident is taxable in India only if such Income belongs to India. Some exemptions are available only to the residents but not to the Non Resident. Therefore in the following article we will read about how an Individual can be resident in Current PY 2021-22. NRI to be Resident in India options available:

“Non-resident Indian” means an individual, being a citizen of India or a person of Indian origin who is not a “resident”.

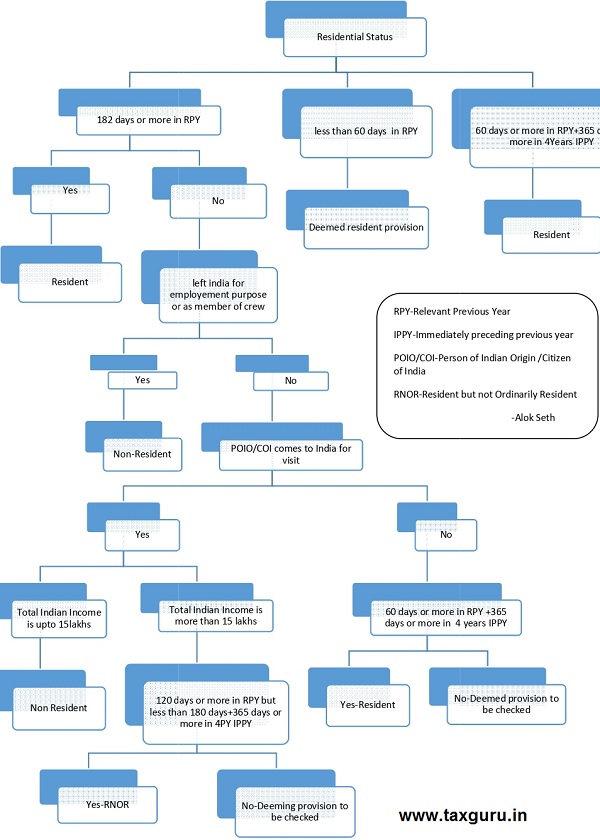

To be resident in India following are the options available to the assessee for the relevant previous year 2021-22:

Option 1-Stay in India 365 days required in 4 previous years preceding the PY2021-22 i.e. PY 2020-21 PY 2019-20, PY 2018-19, PY2017-18, in aggregate there should be stay of 365 or more;

And in the PY 2021-22 there should be stay of 60 or more. The person will be Resident in India Irrespective of the Total Income.

This Option not available to (Exception) –India citizen engaged outside India in an employment or a business or profession or in any other vocation who comes on a visit to India during the relevant previous year irrespective of the total income.

Option 2-In relevant PY i.e. 2021-22 if you stay in India for a total period of 182 days or more you will be Resident in India irrespective of your total income. This option is also applicable to the exception covered in option 1 (mentioned above) irrespective of the total income.

Option 3–Only for Indian citizen engaged outside India in an employment or a business or profession or in any other vocation who comes on a visit to India during the relevant previous year and Total income excluding the income from foreign sources is more than 15 Lakhs, will be Indian Resident if-

He stays in India in PY 2021-22 for a period 120 days or more and his total stay in 4 Previous years preceding the previous year (i.e. PY 2020-21 PY 2019-20, PY 2018-19, PY2017-18) is 365 days or more in aggregate.

Option 4–This option is available to the assesse only if he is not covered by any of the above option i.e. he is not a resident in any of the above mentioned options. There is provision of deemed resident introduced from FY 2020-21 and onward in Income Tax which states to be resident in India the following condition should be satisfied:

1. Assessee should be Individual and Indian citizen.

2. Total Income excluding the Income from foreign sources should be more than 15 Lakhs during the previous year.

3. He should not be liable to pay the tax in any other country by the reason of his domicile or residence or any other criteria of similar nature.

4. There is no need to count no of stays in India in this case.

Conclusion- 1)In case you are an Indian citizen and engaged outside India in an employment or a business or profession or in any other vocation,&;

Come For visit to India during the relevant previous year, In my opinion you, will be covered in either option 2 or option 3 depending on quantum of your Indian income.

In case your Indian income is more than 15 lakhs you need to follow the option 3 i.e. Minimum -120 days in PY 2021-22 & 365 days in 4PY immediately preceding the relevant PY 2021-22 (i.e. PY 2020-21 PY 2019-20, PY 2018-19, PY 2017-18)

In case your Indian Income is upto 15 lakhs you need to follow option 2 i.e. 182 days or more in the PY 2021-22.

Return to India permanently than additional condition of 60 days in relevant Previous Year and 365 in four years immediately preceding the relevant PY would apply (i.e. either option 1 or option 4 will be applicable to check the residential status).

2-In case you are an Indian citizen and engaged outside India other than in an employment or a business or profession or in any other vocation(i.e. for any other purpose) additional condition of 60 days in relevant Previous Year and 365 in four years immediately preceding the relevant PY would apply or 182 or more days during the relevant Previous Year (i.e. either option 1 or Option2 or option 4 will be applicable to check the residential status).

(Further in case of following any of the above option then you need to follow also all the conditions specified in for that option)

*****

(Disclaimer: Also note that the above mentioned provision should not be considered as any professional opinion in any circumstances and the author will not be responsible for any action if taken based on this article, therefore it is requested from the readers to kindly exercise your discretion and take appropriate action.)

Author Bio