This is premium content. Please become a Premium member. If you are already a member, login here to access the full content.

Reopening of assessment quashed as PCIT granted approval without adequate inquiry

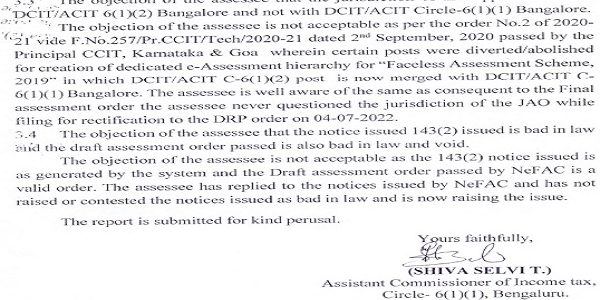

Case Law Details

- Case Name

- Manujendra Shah Vs CIT (Delhi High Court)

- Appeal Number

- Only available for paid members

- Date of Judgement/Order

- Only available for paid members

- Courts

- All High Courts, Delhi High Court

Upgrade to Basic or Premium to download.

Already Upgraded? Log in.

Manujendra Shah Vs CIT (Delhi High Court)

Delhi High Court held that reopening of assessment liable to be quashed as PCIT simply rubber-stamped the attempt of AO to reopen the assessment without inquiring about various basic issues involved in the matter like applicability of section 50C, cost of acquisition and claim of deduction u/s 54EC.

Facts- Vide the present writ petition, the petitioner has mainly contested the reassessment proceedings stating that the same is triggered without due application of mind by the Assessing Officer. Further, it is also contested that the authority granting ap...