There is an earnest desire among many members of the public to do charity, welfare and social good. This leads to flow of money without consideration from one individual to another or from one entity to another. Such flow of money is termed as donation in common as well as legal parlance. Unlike in commercial transactions, in case of donations, the decision makers, or person carrying out charitable activities or the beneficiaries of such activities are different from the person who are extending the money (‘Donors’). Such set ups may, at times, be an opportunity for anti-social elements to negate the welfare of the needy or to carry out their malicious activities in disguise.

In order to tackle these nuisances, charitable institutions have to obtain various registrations and comply with multiple statutory filings, reporting and audits. This article looks into these compliances within the ambit of the Income Tax Act, 1961(‘Act’).

Page Contents

Types of Charitable Institutions

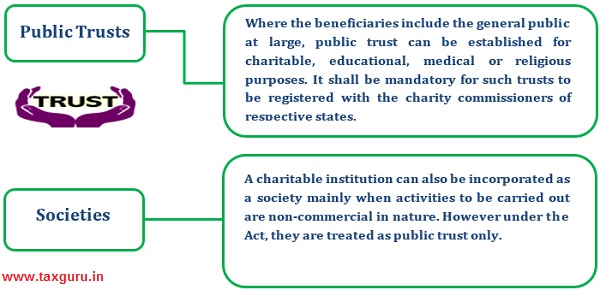

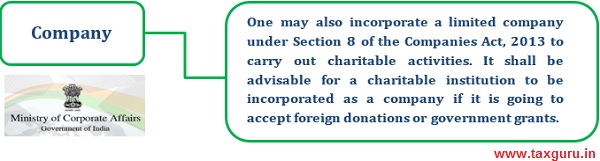

Before jumping to the applicable provisions under the Act for charitable institutions, different types of charitable institutions can be looked at. Most of us know these institutions as Non-Government Organisation (‘NGO’) or Non-Profit Organisation (‘NPO’). However, from legal point of view, these institutions are incorporated as a separate legal entity either as public trusts or societies or companies.

Registrations under the Act:

|

Mandatory Registration under the Act Once the trust/institution is incorporated as any one of the above legal entity, it shall then be required to get itself mandatorily registered either under Section 12A or under Section 10(23C) of the Act, but not both. Without either of these registrations, all the donations and the receipts of the institutions shall be subjected to tax without any set off for expenditure incurred. |

|

|

Normal Registration As per Section 12A/10(23C) and other related provisions, trust or institution is required to apply for fresh, renewal or provisional registration in Form 10A which is to be filled online and shall be furnished electronically. Form shall be verified by the person who is authorized to verify the return of income. Before the Finance Act, 2020, above registrations once granted were valid in perpetual. However, after the above act, the registrations now granted, shall remain valid for 5 years, after which application has to be made in the same form for renewal. |

Provisional Registration Provisional registrations are applied for when the trust or institution has not started its charitable activities. Form 10AB is required to be filed for the purpose of conversion of provisional registration into final registration. In case of provisional registration, it shall be valid for 3 years.

|

|

Registration under Section 80G of the Act Registration under Section 80G is required only when trust or institution wants to pass on tax benefits to its donors in the form of eligible tax deductions. More often than not, trusts or charitable institutions opt for registration under Section 80G as well. However, it is mandatory to have registration under Section 12A/10(23C) before applying for registration under 80G. This registration, which was earlier valid perpetually once granted, now needs to be renewed every 5 years just like the applications under Section 12A/10(23C). |

|

Benefits of above registrations under the Act

On registration under the Act, trusts or institutions get recognized as charitable or religious trust and shall get special benefits and treatment for taxation. The most important ones are:-

| Complete Tax Exemption

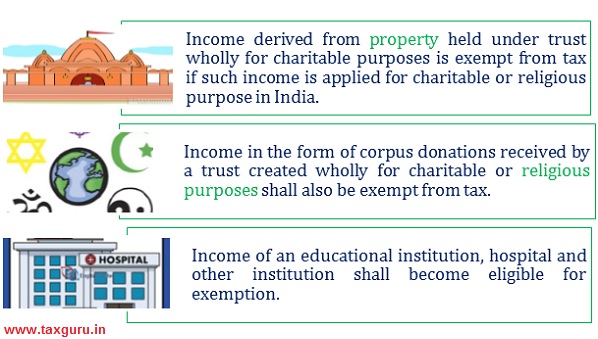

The most important reason for getting the charitable entity registered under the Act is to avail full tax exemptions, subject to fulfillment of certain conditions. No receipts of the trust or institution shall be taxable. Some of the examples are:- |

|

| Tax Deduction to Donor

Registration of trust as per income tax law can be beneficial for donor also. As such the donors do not receive any monetary benefits by making the donations. But as a general encouragement to the members of public to come forward and do the charity, the Act provides such donors to deduct the amount of donations made to the registered trusts and institutions from their total income, subject to certain limits and to pay tax only on the balance income |

Annual filing and statutory compliance:

Over the past few years the charitable trusts and institutions have been subjected to increasing level of statutory obligations in the form of new compliances and reporting requirements.

Other than the compliance of the charity commissioners, the Act also mandates compulsory filing of returns, adherence with the Tax Deducted at Source (‘TDS’) rules, tax audits, prohibition on acceptance of donations in cash exceeding Rs. 2,000/-, no tax exemption for anonymous donations to charitable institutions and renewal in 5 years of its registrations among other things.

To add to the above list, beginning from Financial Year 2021-2022, donations have been categorized as a Specified Financial Transaction (‘SFT’). Accordingly, registered trusts and institutions have to furnish statement of donations received annually, based on which the tax deduction shall be available to the donors. These details of donations have to be furnished in Form No. 10BD annually, on or before 31st May of the subsequent financial year. Details of donation include PAN/Aadhaar of the donor, passport number if PAN/Aadhaar is unavailable, amount of donation, mode of payment and date of donation.

In view of these increasing statutory obligations, it has become imperative for charitable trusts to streamline its activities and accountability. Also, these increased regularizations have led to substantial increase in the overall cost of compliance for charitable trusts. Hence charitable institutions should be incorporated only in case one is sure of continuous and consistent charitable activities year after year.

*****

(This article represents the views of the authors only and does not intent to give any kind of legal opinion on any matter)

Authors:

Chetan Mody | Consultant | Email: chetan.mody@masd.co.in

Soham Dongre | Associate Consultant | Email: soham.dongre@masd.co.in

Author Bio