We know that COVID-19 is one of the major pandemic which has affected each and every person in the world. It has also created a big hole in the pockets of people on account of medical treatment for those affected by COVID.

In this article we will discuss about how to claim refund of TDS deducted on COVID-19 related medical reimbursements made by employer or any other person.

There are two types of individuals based on source of Income:

- Salaried

- Non-salaried (like professionals, businessman, housewife etc)

1) Refund in case of salaried person:

In the case of salaried person many employers use to reimburse them medical expenses incurred for them as well as for their dependent relatives (like spouse, children, dependent parents etc).

Prior to FY 2018-19, medical expenses upto Rs 15,000 was exempt from tax. However the same has been withdrawn from FY 2018-19 onwards. As a result any amount paid by the employer to employee towards medical expenses will be fully taxable under the head “Income from salaries”’.

During this pandemic many employees has incurred expenses under hospitalization / home isolation for COVID treatment and whatever amount has been reimbursed by their employer has been fully taxable under the head salary and their employer has already deducted TDS on that reimbursement and deposited with Govt for FY 2019-20 and 2020-21 respectively.

The above has caused genuine hardship for affected person as if he has been reimbursed Rs 2,00,000 then he has to bear the tax of Rs 60,000 (approx.) (assuming 30% of rate of tax).

In order to address the same Ministry of Finance has issued Press release dated 25.06.2021 with title “Government grants further extension in timelines of compliances. Also announces tax exemption for expenditure on Covid treatment and ex-gratia received on death due to Covid” in which under Clause A (ii) full exemption has been granted for medical reimbursement given by employer for COVID 19 treatment. However where the amount is given by any person (other than employer) then such exemption would be limited to Rs 10 Lacs. The above exemption would be valid for FY 2019-20 and onwards.

The effect of this press release on 25.06.2021 is that since employer has already deducted and deposited TDS with the Govt ex-chequer, so while filing return the employee need to claim refund of extra TDS deducted on COVID related medical reimbursement (if any).

It would be in the interest of employee to take a certificate or some other document to evidence that such amount has been paid by employer on account of COVID-19 treatment to avoid any future litigations.

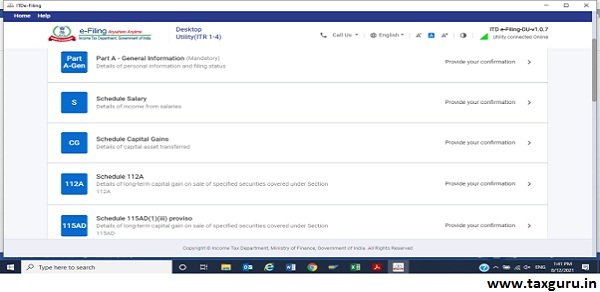

The same should be claimed in applicable ITR forms under the head “schedule salary”→ “Allowances to the extent exempt u/s 10” → Add another → Nature of Exempt Allowance → Any other → Description (COVID-19 Press release dated 25.06.2021) → Amount of exemption claimed.

The relevant screen shots are given below:

___

___

The above method can be followed in case TDS was deducted during FY 2020-21.

However if the TDS was deducted in FY 2019-20, then as on date the return for FY 2019-20 can’t be revised (since return for FY 2019-20 is time barred now and in most of the cases assessment has already been done).

So an employee may also claim the exemption in current FY 2020-21 (for reimbursement made during FY 2019-20). (However the above is subject to litigation in the absence of any clear guidelines from Income Tax department side).

2) In case of non-salaried person:

In case of non-salaried person the impact can be shown with the help of following example.

Say Mr X is a social worker. He got affected due to COVID. His well wishers (including relatives) helped him financially to overcome the disease.

He has received following amount (non-refundable i.e Gift)

| Money Received | Am Rs |

| Mr Y (Relative) | 200,000 |

| Mr Z (friend i.e not relative) | 300,000 |

| 500,000 |

We know as per section 56 of Income Tax Act, any gift received from relative is fully exempt from tax. However if the amount received from a non-relative is within Rs 50,000 then nothing is taxable, but the moment it is Rs 50,001 or more the whole amount of Rs 50,001 or more is fully taxable.

So in the above case in the hands of Mr X Rs 2,00,000 is not taxable (since received from relative). However whole amount of Rs 3,00,000 is fully taxable.

After this press release dated 25.06.2021, now gift received from non-relative upto Rs 10 lacs for COVID-19 treatment is exempt from tax from FY 2019-20 onwards.

So in case of non-salaried person (or even a salaried person receiving amount from any person other than employer) the amount received from any well wisher (like friend, students etc) upto Rs 10 lacs is exempt from tax.

There is no statutory provisions of deducting TDS on amount of Gift. However in case TDS has been deducted by giver then the same can be claimed as refund by receiver of such Gift (provided such gift is on account of covid 19 treatment).

At this juncture it would be of benefit to reiterate that any amount received from medical Insurance Company against medical Insurance policy taken is not treated as Income in the hands of receiver since the receiver is not making any profit or earning Income out of it.

*****

Hope users will find the above article useful. The author ‘CA Srikant Agarwal, CA, CS, CWA, FRM (US’) can be contacted at srikant.agarwal@ gmail.com

Author Bio

can we still claim this exemption

can we still claim covid exemption under salary in section 10(14)(i)?

I am Salaries employee and have incurred Rs.45000/- on corona treatment by Domiciliary Hospitalisation in May2021 and the amount has been reimbursed to me by my Mediclaim Policy TPA. Can I get any exemption of Rs.45,000/- in my I.Tax return of FY 2021-22 and under which section I get the rebate of Rs.45,000/-. I am in 30% Tax bracket

I forgot to mention in my earlier comment that I am 76years of age and am a retired person.

I had Covid19 in November 21 and incurred an expenditure of Rs140,000/- . My wife paid for the same by debit card . Can i get some exemption on this amount under covid related expenses in my return this year FY2021-22

Sir,I am working as stategovernment employee,

I have spent money from relative for covid19 treatment my self and family due to not covered NHIS,

Shall I able to deduct under section 80DDB

Thanks sir

I had spent RS 6 Lakhs for covid 19 treatment to my father in law and mother in law will it be deducted on my income tax for a salaried. if yes under what section it will be deducted

covid treatement expenses comes under which section for pensioners.

if person had did reimbursment og RS 110872 how much rebate he will get or exmpte from tax Ass. 2022-23

Sir ,

Dont see any provision for deduction u/s 10 for other deduction wherein i can claim exemption for covid 19 . Is it available only in the utility and not direct online filing mode?

Does Expenses incurred for covid treatment qualify for sec 80DDB deduction? Any notification for that purpose ?

sir

the son is salaried and spend rs. 1.25 lakhs on the senior citizen fathers treatment can he claim deduction u/s 80dd for the same for covid 19. Unfortunately he lost his father. he has not been reimbursed.

I have received amount from my employer for covid related expenses which increased my taxable income. Also I received help from relatives via funds transfer to my bank account. So where can I claim deductions as I do not see any option in ITR 1. Do I need to use ITR 2 for the same and how to show transfers/gift from my relative/friend to claim exemption?

senior citizen self exp. in carona medical exp at home so how to rebit in income tax return which secation

Sir, what if I have incurred 5lacs and got reimbursement from the employer in fy 2021 to 2022 will I get tax rebate as the amount is for COVID treatment and below 10lacs

Yes. For reimbursement from employer the limit of Rs 10 lacs doesn’t apply. So full amount paid by employer would be tax free for FY 21-22 as well

An employee ends up spending from hand as employer doesn’t reimburse covid treatment expenses. In that case, can the employee get income tax exemption as he has used the money received as salary?

The only section which provides medical related deduction is 80D. In that section all the deduction are given for medical insurance except actual expenditure incurred on senior citizens medical treatment. So no deduction or exemption on self or dependent medical expenses unless they are senior citizens.

Sir if I am a self employed professional and I have incurred an expenditure of Rs 1 lakh during home quarantine, whether I can claim this expenditure as business expenditure

No. For reason refer my another article https://taxguru.in/income-tax/deduction-medical-expenses-computing-business-income.html