As per section 194IA of the Income Tax Act, buyer is required to deduct tax at source @1% of the amount paid/credited to the seller. Therefore, after processing of 26QB statements, the information will appear in 26AS of buyer & Seller. As we all are aware that now the format of Form 26AS has been amended so many people has this doubt as now how the details related to section 194IA will be visible in Form 26AS. Hence, today I will cover this topic through my article.

After processing of 26QB statements, the information will appear in 26AS of buyer & Seller in the following manner:-

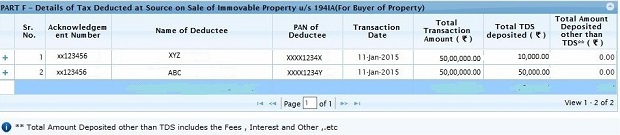

Scenario 1

If Buyer has deducted & deposited Rs.50,000/- on payment of Rs.50,00,000/-.

Seller: TDS Credit is reflected in Part A2 of the seller to the extent of 1% of amount paid/credited. This credit is available for claim in ITR by the seller .

Buyer: Total tax deposited by buyer is shown in Part F of 26AS of Buyer for information. Part F information is not available for Claim in ITR of buyer.

Scenario 2: If Buyer has deducted & deposited Rs.60,000/- on payment of Rs.50,00,000/-.

Seller: TDS Credit is reflected in Part A2 of the seller to the extent of 1% of amount paid/credited. This credit is available for claim in ITR by the seller.

Buyer: (i) Excess Tax Deposited by buyer i.e. Rs.10,000.00(Rs.60000-Rs.50000) is shown in Part A2 of 26AS of Buyer. This credit is available for claim in ITR of Buyer.

Buyer: (ii)Total tax deposited by buyer is shown in Part F of 26AS of Buyer for information. Part F information is not available for Claim in ITR of buyer.

Note: This is only for Information Purpose.

Disclaimer: The contents of this article are for information purposes only and does not constitute advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer to relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that Author / TaxGuru is not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. This is not any kind of advertisement or solicitation of work by a professional.

(Republished with Amendments by Team Taxguru)

Would like to join coure for Incometax + GST

Please advise me, is there any respect for Senior Citizen in fee

Please advice

In case of excess TDS deposited against pur hase of property, how can the same be claimed in ITR. Could you please elaborate a little bit?

SKMittra

What if buyer does not deposit TDS to income tax department and it is not reflected in sellers 26AS? Seller can still ask for if so how and where to approach?

Very useful information.