DIRECTORATE INCOME-TAX (INVESTIGATION) KOLKATA

P-13, CHOWRINGHEE SQUARE, KOLKATA-700013.

investigation report

IN THE CASE OF

Project Bogus LTCG/STCL Through BSE Listed Penny Stocks.

Prepared by

Dhruva Purari Singh, IRS

DDIT (Inv.), Unit-2 (3)

| CHAPTER | CONTENTS. |

| 1 | Preface. |

| 2 | Detailed Comment of DDIT (Inv.), Kolkata, on modus operandi of Providing Bogus Long Term Capital/ Short Term Capital Loss. |

| 3 | Brief discussion on All Listed Penny Stocks (Scripts) used in Bogus LTCG Scam. |

| 4 | Details of Share Brokers involved in the syndicate and their modus operandi. |

| 5 | Details of Entry Operators involved in the syndicate and their modus operandi. |

| 6 | Details of Jamakharchi companies/ Bogus Clients used for purchasing shares of listed penny stocks for providing Long Term Capital Gain to Beneficiaries. |

| 7 | Sample Cash Trail of 1500 Crore Rupees. |

| 8 | SEBI Action, and details of Beneficiaries searched/ surveyed |

| Annexure- A | Basic Details and Financials of All Listed Penny Stocks (Scripts), showing their price manipulation and financial hollowness. |

| Annexure- B | A DVD Containing Details of Beneficiaries DGIT wise and PDF Format of All the statements Recorded. (Marked as LTCG Database). |

OFFICE OF THE PRINCIPAL DIRECTOR OF INCOME TAX (Inv), KOLKATA

Aayakar Bhawan (Annex), P-13, Chowringhee Square, Kolkata-700069

Phone : 033-22136992, Fax: 033-22136191, Email: dit.inv.kolkata @ incometax.gov.in

F.No 75A /2015-16/257-273

Dated: 27-04-2015

To

The DGIT(Inv)

Mumbai, Delhi, Ahmedabad, Bangaluru, Bhopal, Chandigarh, Chennai, Delhi, Hyderabad, Jaipur, Kochhi, Kolkata, Lucknow, Patna, Pune & DG(Intl. tax), Mumbai.

SUB: Entry of bogus LTCG -reg

Sir,

The Directorate of Investigation, Kolkata this time, has undertaken the accommodation entry of Long Term Capital Gain (LTCG) investigation on a much larger scale than earlier and as a result, we have been able to identify a very large number of beneficiaries who have together taken a huge amount bogus entries of LTCG. The span of investigation can be gauged from the fact that as result of this investigation we have identified 64811 beneficiaries involving bogus LTCG of nearly Rs. 38,000 crores. In order to cast the net wide we adopted a different approach of investigation in this investigation which acquired the character of a project. As you are aware, the illegal business of bogus LTCG involves three different individuals.The promoter of ‘Penny stock’ companies (also known as syndicate member), the share brokers & the entry operator who purchases the shares through paper companies by taking cash. Many a times the three categories of individuals perform overlapping roles. A single individual may, at times, perform all the three functions. In LTCG investigations hitherto being done by Kolkata or other directorates, the approach was to target the individuals and through him identify the penny stocks and beneficiaries. This method yielded results on a limited scale emanating only from individual / individuals targeted. Keeping in mind the rampant nature and exponential growth of this illegal business in recent times and to cast the net wide, we reversed the methodology of investigation. We first identified the ‘Penny Stocks’ and then started targeting the individuals who dealt in them. As a result we have been able to virtually cover almost all Kolkata based operators in one investigation itself. It was an on-going process which acquired the character of a project that continued for quite some time, unlike usual investigation which ends with the statement of the individual involved.

We identified the following BSE listed penny stocks which have been used for generating bogus LTCG

| SL NO |

SCRIPT CODE | SCRIPT NAME | FULL NAME of PENNY STOCK | Amount of Total trade Value |

|

| 1 | 531517 | ALANG IN GAS | ALANG INDUSTRIAL GASES LTD | 331801921 | |

| 2 | 531720 | ALPHA GRAPHI | ALPHA GRAPHIC INDIA LTD | 936748230 | |

| 3 | 538423 | ALPS MOTOR | Alps Motor Finance Ltd | 1938129485 | |

| 4 | 512355 | ANUKARAN COM | ANUKARAN COMMERCIAL ENTERPRISES LTD |

4232582703 | |

| 5 | 590122 | ASHIKACR | ASHIKA CREDIT CAPITAL LTD | 2502413517 | |

| 6 | 530479 | ATLINFRA | Atlanta Infrastructure and Finance Ltd |

839070437 | |

| 7 | 531570 | BLAZON MARBL | BLAZON MARBLES LIMITED | 2669410119 | |

| 8 | 508939 | BLUE CIRCLE | BLUE CIRCLE SERVICES LTD | 13876582309 | |

| 9 | 531900 | CCLINTER | CCL INTERNATIONAL LTD | 16050220735 | |

| 10 | 535142 | CHANNEL NINE | CHANNEL NINE ENTERTAINMENT LTD | 2732671350 | |

| 11 | 535267 | COM FINCAP | COMFORT FINCAP LTD | 3416275945 | |

| 12 | 526141 | COMP DISC IN | COMPACT DISC INDIA LTD | 3812590165 | |

| 13 | 512361 | CUPID TRADE | CUPID TRADES & FINANCE LTD | 913119045 | |

| 14 | 503637 | DHANLEELA | DHANLEELA INVESTMENTS & TRADING COMPANY LTD |

2849315089 | |

| 15 | 532903 | DHANUSTECH | DHANUS TECHNOLOGIES LTD | 4093178378 | |

| 16 | 534839 | ECO FRIENDLY | ECO FRIENDLY FOOD PROCESSING PARK LTD |

2194295120 | |

| 17 | 512207 | EFFTXT | Effingo Textile & Trading Limited | 1617519917 | |

| 18 | 531502 | ESAAR INDIA | ESAAR (INDIA) LTD | 5413525764 | |

| 19 | 534927 | ESTEEM BIO | ESTEEM BIO ORGANIC FOOD PROCESSING LTD | 3765065680 | |

| 20 | 511369 | FIRST FIN. | FIRST FINANCIAL SERVICES LTD | 3080492684 | |

| 21 | 535431 | GCM SECU | GCM Securities Ltd | 6042144220 | |

| 22 | 531055 | GFLFIN | GFL Financials India Limited | 968152090 | |

| 23 | 531463 | GBLINFRA | Global Infratech & Finance limited |

12462873580 | |

| 24 | 538180 | GOLD LINE | Gold Line International Finvest Ltd | 1887110104 | |

| 25 | 509024 | GOLD.LEG.LEA | GOLDEN LEGAND LEASING & FINANCE LTD |

623686683 | |

| 26 | 531737 | GREENCREST | Greencrest Financial Services Limited |

2468386741 | |

| 27 | 535217 | HPC BIO | HPC BIOSCIENCES LTD | 5011694340 | |

| 28 | 534734 | ICVL CHEM | ICVL CHEMICALS LTD | 254935286 | |

| 29 | 538422 | JACKSON | Jackson Investments Ltd | 3250070747 | |

| 30 | 511092 | JMD TELEFILM | JMD TELEFILMS INDUSTRIES LTD | 12069286646 | |

| 31 | 507968 | JOLLY PLAST. | JOLLY PLASTIC INDUSTRIES LTD | 1646881531 | |

| 32 | 511357 | KAILASH AUTO | KAILASH AUTO FINANCE LTD | 18778385876 | |

| 33 | 506938 | KAPPAC PHARM | KAPPAC PHARMA LTD | 11229853954 | |

| 34 | 530255 | KAY POW PAP | KAY POWER AND PAPER LTD | 2709821817 | |

| 35 | 530701 | KDJHRL | KDJ Holidayscapes and Resorts Limited | 1742412203 | |

| 36 | 506113 | LIFELINE DRU | LIFELINE DRUGS & PHARMA LTD | 7361135725 | |

| 37 | 526045 | LUMINAI TECH | LUMINAIRE TECHNOLOGIES LTD | 13176169651 | |

| 38 | 511082 | MAAJTL | Maa Jagdambe Tradelinks Limited | 2570500032 | |

| 39 | 531689 | MAHAREM | MAHAVIR ADVANCED REMEDIES LTD | 2301565920 | |

| 40 | 512191 | MISHKAFIN | MISHKA FINANCE AND TRADING LTD | 3073341941 | |

| 41 | 513305 | MORYO IND | MORYO INDUSTRIES LTD | 2074435790 | |

| 42 | 530557 | NCL RESEARCH | NCL RESEARCH & FINANCIAL SERVICES LTD |

10473082439 | |

| 43 | 505525 | PARICHAY.INV | PARICHAY INVESTMENTS LTD | 47825882 | |

| 44 | 511421 | PINEANIM | Pine Animation Limited | 6081960691 | |

| 45 | 535514 | PRIMECAPM | PRIME CAPITAL MARKET LTD | 7776927 | |

| 46 | 505502 | PARAG.SHILP. | PS IT Infrastructure & Services Limited | 10521882343 | |

| 47 | 530561 | PSGLOBAL | Radford Global Limited | 5069291489 | |

| 48 | 512319 | RAJLAXMI IND | RAJLAXMI INDUSTRIES LTD | 3843851999 | |

| 49 | 531228 | RANDER CORPO | RANDER CORPORATION LTD | 4386842551 | |

| 50 | 504335 | RUTRON INT. | RUTRON INTERNATIONAL LTD | 3413402665 | |

| 51 | 530657 | GLOBALSECUR | GLOBAL SECURITIES LTD | 820767494 | |

| 52 | 531800 | SHEETAL BIO | SHEETAL BIO-AGRO TECH LTD | 84392997 | |

| 53 | 512105 | SHREENATH | SHREE NATH COMMERCIAL & FINANCE LTD |

9099925673 | |

| 54 | 505513 | SHRSHA TEX | Shree Shaleen Textiles Limited | 5021678429 | |

| 55 | 512048 | SPLASH MEDIA | SPLASH MEDIA & INFRA LTD | 15053775100 | |

| 56 | 531307 | SRK INDUS | S R K INDUSTRIES LTD | 10183466070 | |

| 57 | 512075 | SUCHAKTRAD | SUCHAK TRADING LTD | 779157597 | |

| 58 | 508969 | SULABHA ENGG | SULABH ENGINEERS & SERVICES LTD | 7263897942 | |

| 59 | 506615 | SUN ASIAN | Sunrise Asian Limited | 23039310931 | |

| 60 | 512311 | SURAB.CHE.&I | SURABHI CHEMICALS & INVESTMENTS LTD |

7826819506 | |

| 61 | 531411 | TUNI TEXTILE | TUNI TEXTILE MILLS LTD | 15004762452 | |

| 62 | 504358 | TURBO TECH | TURBOTECH ENGINEERING LTD | 8319513048 | |

| 63 | 537582 | UNISHIRE | Unishire Urban Infra Ltd | 66941000 | |

| 64 | 531831 | UNISYS SOF H | UNISYS SOFTWARES & HOLDING INDUSTRIES LTD | 6242882248 | |

| 65 | 519273 | UNNO INDUSTR | UNNO INDUSTRIES LTD | 10069623779 | |

| 66 | 512067 | VISHJYOTI TR | VISHVJYOTI TRADING LTD | 806226394 | |

| 67 | 526671 | MKEL | Matra Kaushal Enterprise Limited | 3314059825 | |

| 68 | 535204 | PEARL AGRI | PEARL AGRICULTURE LTD | 594169145 | |

| 69 | 512379 | CRESSAN | CRESSANDA SOLUTIONS LTD | 12731895395 | |

| 70 | 501945 | HINGIR RAM C | DHENU BUILDCON INFRA LTD | 1728918198 | |

| 71 | 531465 | NOUVEAU | NOUVEAU GLOBAL VENTURES LTD | 2038723071 | |

| 72 | 511016 | PREMCAP | PREMIER CAPITAL SERVICES LTD | 1931547811 | |

| 73 | 512417 | TRITRADE | TRINITY TRADELINK LIMITED | 3964454359 | |

| 74 | 538295 | KAUSAMBI | GOLDEN BULL RESEARCH & GROWTH LIMITED | 76334491 | |

| 75 | 511064 | EINSEDUTEC | Eins Edutech Limited | 2053636409 | |

| 76 | 504369 | GRANDMA TRAD | GRANDMA TRADING & AGENCIES LTD | 1931947735 | |

| 77 | 535205 | PEARLELEC | Pearl Electronics Ltd | 873557789 | |

| 78 | 532031 | SARCHEM | SARANG CHEMICALS LTD | Data not available | |

| 79 | 531272 | NIKKIGL | NIKKI GLOBAL FINANCE LTD | Data not available | |

| 80 | 531597 | MIDPOLY | MIDLAND POLYMERS LTD | Data not available | |

| 81 | 511690 | WARNER | WARNER MULTIMEDIA LTD | Data not available | |

| 82 | 512585 | KARMA | KARMA INDUSTRIES LTD | Data not available | |

| 83 | 538684 | ENCASH | Encash Entertainment Ltd | Data not available | |

| 84 | 511668 | FACTENT | FACT ENTERPRISE LTD. | Data not available | |

| Total | 38373,61,55,346 | ||||

The above list also includes 18 scripts on which Virendra Singh, DIT(Inv)1, Delhi has also done very good work and the results of the investigation in hard copy has already been circulated.

We have covered the following brokers also in our investigation who were involved in purchase/ sale and price rigging of the penny stocks mentioned above. It is pertinent to note that the list includes some of the big names like Anand Rahthi, Religare & SMC.

| NO | SHARE BROKER | PURCHASE / LOSS BOOKED VALUE | I. T. Action |

| 1 | THE CALCUTTA STOCK EXCHANGE LTD. | 67883672746 | Many sub Brokers cum operators Covered US 133A |

| 2 | GATEWAY FINANCIAL SERVICES LTD. | 15631310914 | Broker cum Operator covered u/s 133A |

| 3 | SMC GLOBAL SECURITIES LTD. | 13621692916 | Regional office and sub broker covered u/s 13 3A |

| 4 | ANAND RATHI SHARE & STOCK BROKERS LTD. | 12094512349 | Regional office and sub broker covered u/s 13 3A |

| 5 | COMFORT SECURITIES LTD. | 9705146605 | Registered office covered U/S 132 by Mumbai Wing |

| 6 | KORP SECURITIES LTD. | 8189291860 | Broker cum Operator covered u/s 133A |

| 7 | RELIGARE SECURITIES LTD. | 6628979582 | Regional office and sub broker covered u/s 13 3A |

| 8 | DESTINY SECURITIES LTD. | 5247986735 | Broker cum Operator covered u/s 132 |

| 9 | EUREKA STOCK & SHARE BROKING | 3692874993 | Registered office and Sub Brokers covered u/s 133A |

| 10 | MADHYA PRADESH STOCK EXCHANGE LTD. | 2804620283 | Sub Brokers covered u/s 133A |

| 11 | DYNAMIC EQUITIES PVT.LTD. | 2143576378 | Sub Brokers covered u/s 131 |

| 12 | MANU STOCK BROKING PVT.LTD. | 2000562872 | Broker covered u/s 133A |

| 13 | NAKAMICHI SECURITIES LTD. | 1814351977 | Sub Broker covered u/s 131 |

| 14 | BABA BHOOTHNATH TRADE & COMMERCE PVT. LTD. |

1536516621 | Broker cum Operator covered u/s 133A |

| 15 | INTELLECT STOCK BROKING LTD. | 1745088266 | Broker cum Operator covered u/s 133A |

| 16 | EAST INDIA SECURITIES LTD. | 1303498586 | Broker cum Operator covered u/s 133A |

| 17 | ABHINANDAN STOCK BROKING PVT. LTD. | 1197078242 | Broker cum Operator covered u/s 133A |

| 18 | FORT SHARE BROKING PVT.LTD | 1020106004 | Broker covered u/s 133A |

| 19 | RNA CAPITAL MARKETS LTD. | 584774994 | Broker covered u/s 133A |

| 20 | SOSHA CREDIT PVT.LTD. | 483067293 | Broker covered u/s 133A |

| 21 | Millennium Stock Broking Private Limited | 376229158 | Sub Broker covered u/s 133A |

| 22 | KAYAN SECURITIES PVT. LTD. | 26457363 | Broker cum Operator covered u/s 133A |

| TOTAL | 159704939372 |

The figure of total transaction of the brokers is only ^ 15,970 crores as against the total trade in the scripts which is more than ^ 38,000 crores. The reason for this is, there are other brokers from other cities including some leading names who have traded in these scripts but they could not be covered in our investigation.

We have also been able to establish full cash trail starting from cash deposit account to the account of the beneficiary for nearly ^ 1575 crores. The broker wise split-up is as under:

| SL | NAME OF JAMAKHARCHI / BOGUS CLIENT COMPANY | AMOUNT OF CASH TRAIL (Rs.) | NAME OF CONCERNED SHARE BROKER |

| 1 | DEBDARU PROMOTERS PVT. LTD | 28 Crores | RELIGARE SECURITIES LTD |

| 2 | DUARI MARKETING PVT LTD | 162 CRORES | THE CALCUTTA STOCK EXCHANGE LTD. |

| 3 | HEADFIRST VINIMAY PVT LTD | 8 CRORES | THE CALCUTTA STOCK EXCHANGE LTD. |

| 4 | CAMELLIA VINIMAY PVT LTD | 24 CRORES | THE CALCUTTA STOCK EXCHANGE LTD. |

| 5 | KapeswarVintrade Pvt Ltd | 157 Crores | THE CALCUTTA STOCK EXCHANGE LTD. |

| 6 | LAVANDER EXIM PVT LTD | 17 CRORES | THE CALCUTTA STOCK EXCHANGE LTD. |

| 7 | LADIOS TRADING PVT LTD | 206 CRORES | THE CALCUTTA STOCK EXCHANGE LTD. |

| 8 | MAHAMANI TRADE LINK PVT LTD | 103 Crores | THE CALCUTTA STOCK EXCHANGE LTD. |

| 9 | AMIT SARAOGI | 663 Crores | THE CALCUTTA STOCK EXCHANGE LTD. |

| 10 | SankalpVincom Pvt Ltd | 95 Crores | THE CALCUTTA STOCK EXCHANGE LTD. |

| 11 | GALLANT COMMOSALES PVT LTD | 46 CRORES | THE CALCUTTA STOCK EXCHANGE LTD. |

| 12 | Ashok Kumar Kayan Kayan Securities pvt ltd |

51 Crores | THE CALCUTTA STOCK EXCHANGE LTD. |

| 13 | PRAN JEEVAN DISTRIBUTORS PVT. LTD. | 6.14 Crores | EUREKA STOCK AND SHARE BROKING SERVICES LTD |

| 14 | Dristi Suppliers Pvt Ltd | 7.40 Crores | EUREKA STOCK AND SHARE BROKING SERVICES LTD |

| 15 | PRAN JEEVAN DISTRIBUTORS PVT. LTD. | 1.16 Crores | Guiness Securities Ltd |

| 16 | PWAN KUMAR KAYAN | Cash Seizure 90 Lakhs | SMC GLOBAL SECURITIES LTD, & EUREKA STOCK .(Sub Broker) |

| TOTAL | 1575 Crores |

Modus operandi

The whole business of providing entries of bogus LTCG over the years have become much more organised and with economy of scale in full operation the stake involved have become huge. Before the actual transaction start taking place there are brokers in different towns who contact prospective clients and take paper booking for entries. The commission to be paid to the operators is decided at this stage however, no money is paid. Once the booking is complete the operators have a reasonably good idea of how much LTCG is to be provided along with the break-up of individual beneficiaries. This data is essential to decide which penny stock or companies to use for the job and which beneficiary to buy how many shares.

Types of Penny stock companies

Broadly speaking there are two types of companies.

i) An old already listed company, the entire shareholding of which is bought by the syndicate to provide LTCG entries. These are generally dormant company with no business and with accumulated losses

ii) A new company which is floated just for the purpose giving LTCG entries. Such new companies are often floated after the initial booking is complete and the capital base is decided keeping in mind the entries to be provided.

The entities involved in the transactions

As mentioned earlier there are three categories of individuals who are involved in the transactions

i) Syndicate Members.

They are the promoters of the Penny Stock companies who own the initial shareholding mostly in the name of paper companies either in a fresh IPO or purchased from the shareholders of a dormant company. They are usually a group of 4-5 individuals who also referred to as Syndicate Members and are sometimes also referred to as Operators. Their nominees are directors of the Penny Stock companies which is indirectly controlled by them through such dummy directors. The whole operation is managed by them. They get the net commission income from the transactions. Their name however, seldom appears in the actual transactions.

ii) The Brokers

They are registered brokers through whom shares are traded both online and off-line. They are fully aware of the nature of transactions and get paid a commission over and above their normal brokerage. Some of the big broking houses are also indulging in such transactions mostly through sub-brokers. Even Calcutta Stock Exchange has registered itself as a broker with BSE and has given a large number of terminals to sub-brokers who are dealing into this type of transactions. In this investigation we have also covered some of the sub-brokers of big broking houses like Anand Rathi, Religare Securities, SMC etc. The brokers often compromise on KMC norms of the clients to help the Syndicate Members.

iii) The Entry Operators.

They are individuals who control a large number of paper/shell companies which are used for routing cash for the transactions as well as buying and selling shares during the process of price rigging. They work for commission to be paid by the Syndicate Members.

To cut cost sometimes in smaller operations, the same group perform more than one function.

The Transaction

The transaction involves three legs.

i) Purchase of share by the beneficiary. In this the beneficiary is sold a fixed number of shares at a nominal rate. The price and the number of shares to be purchased are decided on the basis of the booking taken and the value up to which price would be rigged. This leg of the transaction mostly is off-line. This is done to save on STT using the loophole in Section 10(38) of the IT Act which palaces restriction of trading by payment of STT on sale of shares and not on purchase.

ii) Price rigging. After the shares have been purchased by the beneficiaries, the syndicate members starts rigging the price gradually through the brokers. In these transactions the volume is almost negligible. Two fixed brokers who are in league with the Syndicate buy shares at a fixed time and at a fixed price. These low volume transactions are managed through paper companies of entry operators.

iii) Final sale by the beneficiary. This is done after the beneficiary has already held the share for one year. The period of holding may be a little more to match the amount of booking with the final rate. The beneficiary is contacted either by the Syndicate member or the Broker (Middle man) through whom the initial booking was done. The beneficiary provides the required amount of cash which is routed through some of the paper companies of the entry operator and is finally parked in one company which will buy the share from the beneficiary. The paper company issues cheque to the beneficiary.

The above mentioned methodology is referred to as Conventional Method. Another method which also used quite often is called Merger Method. The methodology adopted in Merger Method is as under:

Merger method :

In this method the operators first form a Private Limited Company and the shares at par are allotted to beneficiary individuals. This private limited company is then amalgamated / merged with a listed penny stock company by a High court order. Depending on the capital of the amalgamating and amalgamated companies, the investors are allotted stock of the listed companies in the same proportion. The capital of the Penny stock listed company and the private limited company are so arranged that the beneficiaries post- merger, get shares of listed company in the ratio 1:1, thus the investor gets equal number stocks of the listed company. The promoters of the listed penny stock companies run the syndicate, the brokers and the entry-operators through whose paper/shell companies cash are routed are merely commission agents. The penny stock listed company is such that though its capital base is small its market capitalisation is many times its capital base. This is managed again through small volume predetermined transaction amongst members of the syndicate. The prices of shares are thus manipulated at 20 to 25 times the face value. For example the quoted price of such a company would be around t 250 with minor fluctuations synchronised with rise and fall in the market to avoid regulatory glare. One such company is Quest Financial Services Ltd. quoted on CSE. The investors hold these shares the penny stock listed company which it got as a result of merger for one year (statutory lock-in period for exemption under IT Act) and then sell it to one of the shell private limited companies of the operator. The investor thus makes a LTCG of 25 times its original investment. The purchase consideration is again provided in cash by the investor which is laundered to the buyers account through a maze of shell companies as mentioned in the previous method.

The list of companies merged and the beneficiaries emanating therefrom is mentioned in the DDIT’s report. The High Courts do sometimes refer the case to the jurisdictional CIT before passing amalgamation order. The CIT however, neither has the time nor the wherewithal / jurisdiction to investigate. The result, the blatant tax evasion is getting stamped by the Hon’ble High Courts.

A typical chart of share price verses date and the volume of a ‘Penny stock’ included in the above mentioned list is illustrated below. Mark the heavy volume in 2014 when the price is negligible. One year later this chart will again see the bell curve peak as one shown on the left.

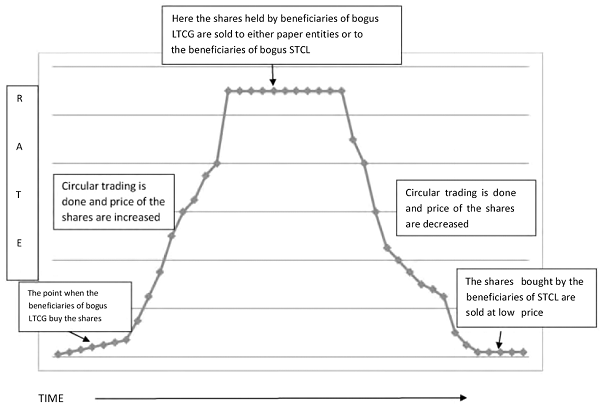

In the curve above while LTCG is booked while the share price is going up, the downward journey is used by the operators for booking bogus losses. People who have huge profit take the Short Term Capital loss (STCL) to set-off their profit. The methodology used is the same. The beneficiary who wants loss buys the share at a high rate from the beneficiary who is taking LTCG. The loss taking beneficiary pays cheque to the LTCG taking beneficiary and the cash provided by the LTCG beneficiary is returned to the Loss taking beneficiary. The operator deducts his commission before payment by cash. As prices crash the loss taking beneficiary sells these shares bought at high value for small value resulting in artificial loss.

A DGIT(Inv) wise list of beneficiaries along with all statements is enclosed on a DVD. You are requested to kindly disseminate the same to the A.Os through the CCITs concerned. The list has been segregated on the basis of the address given by the beneficiaries to the broker. It is possible that some of the beneficiaries are assessed somewhere else. In such cases the information may kindly be passed on to the DGIT concerned. We were not able to cover some individuals who are presently operating in other jurisdictions. The DGIT(Inv) concerned may supplement the effort by covering some more individual or individuals who despite our best efforts could not be covered. However, the entire list of beneficiaries given in the report is backed by some statement which is on the enclosed DVD . Some of the big beneficiaries may also be targeted for focused further probe. Acceptance by them would be the final nail on the coffin. In one of the investigation in Kolkata Sri Deepak Kumar Agarwal in course of search accepted taking entries of LTCG amounting to ^ 25 crores. Some other beneficiaries have also accepted as mentioned in the report of Virendra Singh DIT(Inv) 1 Delhi.

The issue is not that on the basis of this investigation we may have built a water tight case of concealment where each and every beneficiary can be prosecuted. Even if our effort results in raising the cost of evasion, I will personally consider it successful.

If any other directorate has done some work on this and wishes to supplement the effort undertaken by us, kindly get in touch with us.

A copy of this letter is also being marked to Chairman SEBI as SEBI is the regulatory authority vested with the mandate to stop such illegal trade. What we have undertaken is actually a post-mortem of the trade, a better course would be to nip the trade in the bud, which can be done only by SEBI.

At end I would like to explain the arrangement of the data in the DVD which is enclosed. When you open the DVD there would be five folders as under;

i) INVESTIGATION REPORT

ii) LTCG DATABASE

iii) LTCG summary

iv) LTCG TRADE LEDGER

v) STCL Summary

vi) STCL TRADE LEDGER

vii) SEBI ORDERS

Investigation Report contains in soft form what has been sent as hard copy which includes my report, the report of the DDIT(Inv) and some data.

LTCG Database contains all statements of brokers, promoters and entry operators.

LTCG summary gives the total amount of sale by individual beneficiaries along with their PAN and address as given to the broker under KYC.

LTCG trade Ledger gives the details of transaction script wise and date wise. In other words it is the details of LTCG summary.

STCL stands for Short Term Capital Loss. TP+’he STCL summary and ledger is exactly similar to LTCG except that it contains list of beneficiaries who have taken entries of bogus loss.

SEBI Orders contain some of the orders passed by SEBI wherein some such penny stock company’s trading has been suspended. These orders are available in public domain, however, we thought to put it here also for ready reference.

The data of DGIT(International tax) needs a special mention here. To our surprise we found that a large number of NRIs and many well-known FIIs are buying or selling these stocks. This appears like a case of black money stashed abroad coming back to India(purchase) or money being sent out of the country (Sale). It is found that while only ^ 27.57 crores have gone out of the country; the amount coming in is ^ 114.97 crores. For details of this modus operandi please click on the link after pressing Ctrl on your computer to see the video. https://www.youtube.com/watch?1ist=UUSrS7iCispbQYTG1-NSLNyw&t=25&v=CI2gIwBg35c. Or copy this link and paste it in Google search for the video. The matter may be examined from this angle.

A detailed report prepared by the DDIT(Inv), Dhruv Purari Singh who painstakingly investigated this case is also enclosed along with the DVD.

Yours faithfully

(BISHWANATH JHA)

Principal Director of Income tax (Inv)

Kolkata

Dated: 27-04-2015

Memo F. No. 75A/2015-16/274-75

i) Chairman SEBI

ii) Member(Inv), CBDT

(BISHWANATH JHA)

Principal Director of Income tax (Inv)

Kolkata

Chapter-1: Preface.

For quite some time information about bogus Long Term Capital Gain and Short Term Capital Loss was coming from various sources. Even Directorate of Investigation Kolkata, conducted some inquiries in the past which unearthed some big syndicates involved in providing accommodation entry of Long Term Capital Gain. However, these were cases of individual brokers. In order to cast the net wide, it was decided that in this investigation, which acquired the character of a project, the focus would be on the penny stocks, instead of the operator.

In the whole project total 84 BSE listed penny stocks have been identified and worked upon. After that, number of search and surveys were conducted in the office premises of more than 32 Share broking entities, which accepted that they were actively involved in the bogus LTCS/STCL Scam. Surveys were also conducted in the office premises of many accommodation entry providers and their statements recorded. All have accepted their role in the scam.

Beneficiaries of more than Rs. 38 thousand Crore Have been identified and segregated DGIT(Inv.) wise. Total number of more than 60 thousand PAN numbers of the beneficiaries have been identified, which is being reported to assessment wings through the DGIT,s.

This report covers more than 5000 paper/shell companies, also known as Jamakharchi companies, which are involved in providing bogus accommodation of various kinds. Statements for most of the directors of companies have been recorded under oath and are given in the LTCG Database, which is in the DVD enclosed.

We have also prepared cash trail of Rs. 1570 Crores. This massive cash trail of Rs. 1570 Crores shows, how unaccounted/undisclosed cash of beneficiaries is being routed through this modus to convert black money into LTCG. We have followed the money trail from the point it is being deposited to the undisclosed proprietorship bank accounts, to the accounts of share brokers. Then we have recorded statements of share brokers where they have accepted that this cash has been used for providing accommodation entry of bogus LTCG.

This report contains a Database in soft form (in DVD), which comprised statements of 25 entry operators their dummy directors and list of their 5000 shell companies. This database also contains statements of more than 34 Share broking entities recorded under oath. In short, this report can claim to be a database of bogus LTCG/STCL syndicate. This report is not full and final; we intend to update our database on regular basis with new actions against entry operators and assures that the same will be communicated to all stakeholders, at the earliest. It is also requested that other directorates, who have carried out similar investigation may like to share the data with us in soft form so that a comprehensive database of LTCG operators can be made.

Capital Gain Side or Sale Side Beneficiaries

| DGIT Wise | NO OF PAN | AMOUNT |

| MUMBAI | 17344 | ^ 1223392,20,545 |

| KOLKATA | 12236 | ^ 671804,06,328 |

| DELHI | 6632 | ^ 609972,97,795 |

| AHEMDABAD | 6962 | ^ 241851,44,408 |

| LUCKNOW | 3996 | ^ 221427,35,005 |

| CHANDIGARH | 2519 | ^ 165985,63,664 |

| BHOPAL | 3118 | ^ 151807,09,899 |

| JAIPUR | 3471 | ^ 150909,93,477 |

| BENGALURU | 1619 | ^ 107038,20,659 |

| HYDERABAD | 2604 | ^ 105012,00,292 |

| CHENNAI | 1790 | ^ 90944,04,614 |

| PATNA | 1133 | ^ 42251,14,570 |

| PUNE | 399 | ? 514,21,00,307 |

| INTERNATIONAL TAXATION | 136 | ^ 2757,35,307 |

| KOCHI | 187 | ^ 2172,38,411 |

| TOTAL | 64811 | ^ 3838746,85,281 |

Short Term Capital Loss or Purchase Side Beneficiaries/Jamakharchi

Providers.

| DGIT Wise | NO. OF PAN | AMOUNT |

| KOLKATA | 12240 | R 2246797,65,038 |

| MUMBAI | 11854 | R 797756,89,393 |

| DELHI | 2920 | R 311585,30,784 |

| AHEMDABAD | 4742 | R 117224,30,395 |

| BHOPAL | 1514 | R 87343,71,717 |

| CHANDIGARH | 1241 | R 59263,52,548 |

| JAIPUR | 2098 | R 57041,28,394 |

| LUCKNOW | 2062 | R 56115,31,092 |

| BENGALURU | 914 | R 24008,04,555 |

| CHENNAI | 899 | R 16965,42,285 |

| HYDERABAD | 1187 | R 16060,99,482 |

| INTERNATIONAL TAXATION | 248 | R 11497,68,948 |

| PATNA | 437 | R 4635,75,503 |

| PUNE | 300 | ?7950,47,517 |

| KOCHI | 216 | R 734,28,064 |

| TOTAL | 43154 | R 3814980,65,714 |

Chapter-2

Detailed Comment on Modus Qperandi of the syndicates providing Bogus Accommodation Entry of LTCG/STCL.

1. Accommodation entry is a financial transaction between the two parties where one party enters the financial transaction in its books to accommodate the other party. These transactions are accommodated mostly in lieu of cash of equal amount and commission charged over and above at certain fixed percentage for providing such accommodation entry. These accommodation entries are taken by various beneficiaries for introducing their unaccounted cash into their books of accounts without paying the due taxes.

An entry operator is the person who is in the business of giving accommodation entries in lieu of cash/ cheque of equal amount after charging certain percentage of commission in cash.

Long Term Capital Gain in shares, is defined by the value of such shares, which are shares of a stock exchange listed company, held by assesse for more than a year. Needless to add, it is exempt from tax under section 10(38), of the I. T. Act.

2. BOGUS LONG TERM CAPITAL GAIN

Let us suppose that there is a person “B” (Beneficiary) who is in possession of unaccounted money and who wants to bring this unaccounted money into his books. At the same time this person also desires to avoid paying any tax whatsoever when this money is brought into the books.

⇓

Now this person “B” approaches the Entry operators “O”. Operator is a person who manages the overall scheme of the scam. An operator maintains a complex nexus of various paper/bogus entities and is also in control of some companies whose shares are listed on one or the other Stock Exchanges. He maintains a close nexus with share brokers.

⇓

When approached by “B”, operator asks the “B” to buy some specific number of shares of a specific listed company. These shares can be bought by the Beneficiary either on the exchange itself or the operator may arrange for the issue of these shares to the beneficiary through preferential allotment i.e. through private placement (this is an off-market transaction). These shares are allotted to the beneficiaries at very low price.

⇓

Thereafter, the Operator starts rigging the price of the shares through circular trading and increases the price of the shares, with the help of share brokers and bogus clients. The prices are rigged to an optimum amount over a period of time.

⇓

Once a period of 1 year (for claim of exemption on LTCG u/s 10 (38)) is over, the operator asks the beneficiary to deliver the unaccounted cash. Once the unaccounted cash has been delivered by the beneficiary, the same is then routed by the operator to the books of various Paper/Bogus Companies which ultimately buy the shares belonging to the beneficiary at high prices. The cash is routed to the books of bogus companies through a maze of various other paper companies so as to avoid the direct cash trail.

⇓

Once the cash has been routed to the books of paper/bogus companies, which are registered as clients to the brokers, the operator instructs the Beneficiary to place a sell option for the shares belonging to the beneficiary, in a particular lot size on a particular date and time.

⇓

At the same time the operator instructs the paper/bogus companies maintained by him to buy the shares of the beneficiary on the exchange at the predetermined particular date and time.

⇓

In this way the shares of the beneficiaries are bought by the paper/bogus companies and the unaccounted money of the beneficiary is routed to the books of the beneficiary as a bogus entry of LTCG.

3. BOGUS SHORT TERM CAPITAL LOSS

Sometimes, the operator also has request from some companies which foresee that they are going to have huge profits in their books of accounts. The Company wishes to reduce its taxable income by taking entry of bogus loss in its books of account so as to set-off the profit that it is going to earn. These companies are given entry of bogus Short term Capital Loss in the following manner:

Let us suppose that there is a Company “B” (Beneficiary) which foresees that it is going to have huge profits in its books of accounts. The Company wishes to reduce its taxable income by taking entry of bogus loss in its books of account so as to set-off the profit that it is going to earn.

⇓

Now this Company “B” then approaches the Entry operator “O”. Operator is a person who manages the overall scheme of the scam. An operator maintains a complex nexus of various paper/bogus entities and is also in control of some companies whose shares are listed on one or the other Stock Exchanges.

⇓

When approached by “B”, the operator asks the “B” to buy some specific number of shares of a specific listed company. These shares are bought by the beneficiary company at very high price on the stock exchange.

The shares which are bought by the beneficiary company are held by either the paper/ bogus entities maintained by the operator or by the beneficiaries who wish to take an entry of bogus LTCG in their books.

⇓

Thereafter, the Operator riggs the price of the shares through circular trading and decreases the price of the scrip. The prices are rigged to an optimum amount over a period of time.

⇓

Once the price of the shares has been decreased by circular trading, the operator asks the beneficiary company to place a sell option for the shares belonging to the beneficiary in a particular lot size on a particular date and time.

⇓

The loss that is incurred by the Beneficiary company is returned back to the company in cash.

⇓

In this way the beneficiary companies desirous of booking a loss in their books of account get an entry of bogus STCL which is set-off against the regular profit of the company.

A pictorial depiction of the whole scheme is as follows:

The entities involved in this scheme of price manipulation of shares and entry of bogus LTCG and bogus STCL are as follows:

- The operator of the Scrip

- Directors/promoters of the listed stock (Penny Stock Companies) whose price are manipulated

- The beneficiaries…………………………………… of LTCG

- The beneficiaries of STCL

- Bogus/paper entities maintained by the operator which are involved in price manipulation and in providing exit to the beneficiaries from the exchange.

- The share brokers who provide the access of stock market to these bogus/paper entities, in lieu of high brokerage and cash commissions.

Role of Operator

The operator is a person who manages the overall scheme of the scam. He is in control of numerous paper/bogus companies which are utilized for routing of cash. The beneficiaries desiring bogus LTCG/STCL approach the operator. The operator is also in control of some penny stock companies whose shares are listed on a recognized stock exchange.

Penny Stock is a stock that trades at a relatively low price and market capitalization. These types of stocks are generally considered to be highly speculative and high risk because of their lack of liquidity, large bid-ask spreads, small capitalization and limited following and disclosure.

Sometimes there are a number of intermediaries who work for the operator. These intermediaries introduce the beneficiaries to the operator or in many cases these intermediaries become sub agents of the operator and deal with the beneficiaries on their own.

Role of Promoters of Penny Stock Companies

A penny stock is a stock which is usually traded at very low price and has very low market capitalization. The shares of the penny stock are closely held as the general public is not interested in these stocks due to the poor financials of the listed companies. The operator chooses one of such penny stocks for the implementation of the scheme. The promoters/ directors of the penny stock company are paid some cash commission and in return they allow the operator to manage the affairs of the company. The operator then issues shares of these penny stock companies to the beneficiaries through the route of preferential allotment (Private Placement).

As per the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, the shares that are allotted through private placement, have a lock-in period of 1 year. Therefore, these shares can be sold by the allottees only after a period of one year from the date of allotment. This qualifies them for the benefit of claim of exempt LTCG.

As already mentioned these penny stock companies have no actual business or establishment. They have no financial credentials also. Thus, the fact that beneficiaries subscribe for their shares through private placement is in itself a suspicious thing. No genuine person in the right state of mind would invest in these penny stock companies. The shares are subscribed only for the purpose of claiming LTCG at a later stage. The promoters/directors of the companies work hand in glove with the operator to implement this scheme of availing bogus LTCG.

Role of Share brokers

As per the guidelines of SEBI and the stock exchanges, the brokers are supposed to comply with stringent KYC norms before registering any entity as their client. They are supposed to perform detailed background checks on their clients. However, it is seen that these share brokers have done trading for various paper/bogus companies. These paper/bogus entities have no business or establishment. This clearly implies that the share brokers are hands in glove with the paper/bogus companies in the whole scheme. The share brokers receive cash commission for allowing these paper entities to trade through their terminal. In fact it has been learnt that these brokers perform the trading themselves on behalf of the paper/bogus entities. Many brokers have accepted this fact in their statements recorded by the directorate.

4. Project Basis Enquiry of the scam.

Various inquiries have been conducted by the Directorate of Investigation, Kolkata, on a project basis, which has resulted into the unearthing of a huge syndicate of Entry Operators, share brokers and money launderers, involved in providing bogus accommodation of Long Term Capital Gain, Short term capital loss. It has come to light that large scale manipulation has been/ is being done in market price of shares of certain companies listed on the Bombay Stock Exchange by certain persons working as a syndicate in order to provide entries of tax exempt bogus Long Term Capital Gains to large number of persons in lieu of unaccounted cash. The basic objective of this racket is to convert black money into white without payment of Income Tax. The unaccounted cash of such persons [beneficiaries] is utilized to purchase shares of such companies at a very high artificially inflated market price. This practice is generally called Accommodation Entry Scam, as the activities of such persons are carried out with prime objective of accommodating unaccounted cash of beneficiaries into their regular books of accounts without paying any tax on the same. Some of the listed companies, directly or indirectly owned by operators and whose share prices have been apparently manipulated by the syndicate of operators, which have come to adverse notice of the Income Tax Department, are as under:

(Detailed names, PAN, Entry operators and promoters of these scripts can be found in the LTCG Database, given in DVD separately.)

The above list is not comprehensive as similar racket is being carried out in many other listed companies

5. Background:

Kolkata has a very distinctive place among the cities of India, so for as accommodation entry is concerned. It is the hub of Jamakharchi/accommodation entry providers. This city runs a very organized and systematic money laundering syndicate. Directorate of Investigation Kolkata has successfully handled this syndicate and unearthed huge accommodation entry rackets , from time to time.

A Search & Seizure action was conducted by the Directorate of Income Tax [Investigation], Kolkata in 02/07/ 2013 on Anand Sharma and Janardan Chokhani Group, and subsequently on the Deepak Patwari,s Destiny Security Ltd Group. As a result of the said search & seizure action, it was gathered that certain persons had been involved in manipulation of the market price of shares of some companies listed on the BSE namely M/s Pearl Electronics ltd, Shree Shaleen Textiles Limited, Cressanda Solutions Ltd, etc., in order to provide entries of bogus Long Term Capital Gains to the interested persons hereinafter referred to as ‘beneficiaries’. On the basis of statements recorded and findings of the investigations huge amount of beneficiaries were detected and reported to Assessment wings.

Another Survey U/S 133A of the Income Tax Act, was conducted on 08/05/2014, in the case of Sikaria Share & Stock Broking Services Pvt. Ltd. Where not only a money trail from cash deposit to Beneficiary, via Share Broker, was established but various entry operators were made to confesses their role in the Bogus LTCG Scam.

Another Survey U/S 133A of the Income Tax Act, was conducted on 07/08/2014, in the case of Quest Financial Services Ltd and Prakash Jajodia. Here also, not only a money trail from cash deposit to Beneficiary, via Share Broker, was established but key entry operator/ promoter of Listed Company was made to confess his role in the Bogus LTCG Scam.

Another invaluable investigation report about LTCG Scam was received from DIT (Inv.)Delhi, which provided deep inputs about the modus operandi and length and breadth of the LTCG Syndicate.

In the background of above information Directorate of Income Tax (Investigation) Kolkata, planned to unearth the huge racket of accommodation entry provides and share brokers involved in the racket. So, as per the direction Principal DIT (Inv.) Kolkata, I initiated various actions covering number of entry operators, share brokers, which ultimately resulted in unearthing of LTCG entry scam of a very large magnitude involving a syndicate of operators based in Delhi, Kolkata & Mumbai acting in tandem to manipulate the market price of shares of certain companies in an organized manner and then to provide entries of bogus Long Term Capital Gain to interested person through a complex web of prearranged transactions. This note provides insights into the accommodation entry scam involving the syndicate of operators and the complex web of prearranged or artificial web of transactions created by them in order to carry out their unethical and illegal objective of providing entries of Long Term Capital Gain or, at times, Short Term Capital Loss to the interested persons [beneficiaries].

6. Further elaboration of Modus Operandi of the Syndicate:-

In view of the background discussed in foregone paras, we conducted action on more than 30 Share broking entities and more than 20 entry operators working in Kolkata. Almost everyone has accepted its active participation in providing accommodation entry of Long Term Capital Gain.

The enquiries have revealed that the entire entry providing scam comprises of various levels of operators who either introduce the unaccounted cash of beneficiaries in their accounts through a layer of transactions and utilize the said cash for purchase of shares at manipulated high prices which ultimately results in payment of the amount back to the beneficiary in the guise of sale proceeds of shares ostensibly resulting in Long Term Capital Gain to the beneficiary. Reverse modus operandi is adopted in order to provide entry of bogus Short Term Capital Loss.

The associate operator on his own or with the financial support of intermediary agent purchases a company listed on BSE and having a small capital base. The basic criterion for purchase of a company is a small capital base with majority of shareholding with the promoters who are also mostly persons of dubious reputation. The shareholders are then replaced by the persons who wish to procure entry of Long Term Capital Gain (LTCG) to convert their unaccounted cash/income into tax exempt LTCG and, thus, introduce their unaccounted income in their accounts/ books without payment of income tax which is otherwise due on such income and, thereby, causing loss to the revenue. Such persons are promised tax exempt LTCG 10 to 20 times of the amount initially shown to have been invested. Though the purported initial investment of such persons [beneficiaries] is shown through payment by cheque, the entire amount shown to have been initially invested is either returned to them by the associate operator in cash or adjusted against the payment to be received at the time of harvesting of the bogus LTCG. The shares are initially shown to have been purchased by the beneficiaries and, after a year, shown to have been sold by them through purely accommodative transactions without an iota of genuineness. The initial transfer of shares in the name of beneficiary can be an ‘off market transaction’ or ‘online transaction’ and, thereafter, issue of ‘preferential shares’ at nominal rates or issue of bonus shares even though there is hardly any profit or business activity in these companies. Sometimes, the associate operators even incorporate new companies exclusively for this purpose and get them listed on BSE. The basic aim of their exercise is to allot the shares of listed companies to beneficiaries at a minimum price. The modus operandi may even involve a process of amalgamation of an unlisted company with an already listed company. The associate operators also entertain request for Short Term Capital Loss from beneficiaries who wish to reduce their taxable profits by setting off their profits against fictitious short term losses.

After allotting shares to the beneficiaries, the associate operator starts manipulating the share prices. Here it is pertinent to note that most of the investors at this point are those businessmen who want their unaccounted cash to be converted to bogus tax exempt LTCG. It is observed that the share prices of such companies are manipulated to raise the market price of share to astronomical proportions within the stipulated period of one year. [It is here that the surveillance mechanism of the Stock Exchange has either failed or the persons responsible for surveillance have consciously allowed the manipulations to happen]. The business activities which may be shown by such companies are mere paper transactions which cannot be substantiated at ground level. The share price is slowly but consistently manipulated northwards till the purported market price of the share attains the desired level. Despite extremely thin trading volume of shares on the Stock Exchange, the share prices are made to rise consistently through circuitous and prearranged transactions by manipulating the operations.

The rise & fall in price of shares is sharp and is not at all correlated & commensurate with the fundamentals of the company. The financials of the companies do not justify such phenomenal rise or sharp fall in the market price of shares. Enquiries further reveal that the funds for the purchase of shares which are off-loaded to book fictitious LTCG, as already mentioned above, are in fact provided by the beneficiaries in cash. The cash of beneficiaries is utilized to create dummy buyers by routing the same through various paper entities. When the time is ripe for the LTCG beneficiaries to reap LTCG, they are informed by the intermediary agent or his employees to provide cash for arranging the sale of the shares. This cash is then handed over to the contact persons of the operator/associate operator. These persons then receive RTGS in lieu of such cash from various small RTGS operators. This RTGS is then used to finance the dummy buyer of the shares to be sold by the beneficiary. Sometimes, this cash is even handed over to the persons interested to take entry of bogus Short Term Capital Loss in lieu of cheques of equal amount from them ostensibly for purchase of such shares at artificially inflated market price. In the process, their white money is converted into black and their taxable profit is reduced.

When the buyer [either dummy paper entity (after receipt of amount in its bank account) or Short Term Capital Loss aspirant] is ready, the associate operator or his employee gives a call to the intermediary agent or his employee to ask him to sell specific quantity of shares (depending on the amount of RTGS) at a specified price at the specific time. The intermediary agent or his employee, as the case may be, then either calls the broker of the beneficiary to sell the shares of the beneficiary or sends a message to the beneficiary to sell the shares as per the directions specified by the associate operator. The beneficiary then gives directions to his broker to sell the shares as per the quantity of shares and rate fixed & conveyed by the associate operator who had already arranged a dummy buyer for such shares. On such transactions, hefty commission is charged in cash by the intermediary for himself as well as for his associate operators.

Another fact that is to be noted in this scam is that the buyers of these manipulated shares are either paper companies which have no business/office/employees or they are good profit making entities who have profit in their profit & loss account and want to set off this profit against the short term loss that would appear to have been incurred when shares of these companies are sold after their prices are made to crash on the floor/portal of the Stock Exchange.

Another fairly common phenomenon noticed in LTCG scam is that often the operators split the face value of shares after manipulating the market prices of the shares to a reasonably high level and repeat the operation to manipulate the prices again after splitting. The major reaping of bogus LTCG is generally done only after the split of face value of the shares.

In short Basic modus of providing bogus LTCG are here under:-

(a) Merger of Unlisted companies with Listed Entity:

This is the most preferred option for the persons willing to operate for the purpose of doing Long Term capital Gains. In case of the mergers with listed companies, the merger petition has to be filed with concerned stock exchange under clause 24F of the Listing Agreement, which gives its permission to go ahead with the merger scheme in consultation with SEBI. Here the main catch is valuation of shares of the companies. Since the Act provides for the valuation of shares at book value and the same has been approved by the Supreme Court in various decisions which has been discussed below after this para. Since, the Stock Exchange and SEBI keep close watch on price movement of shares, these people adopted the route of merger of private limited companies having huge premium thereby increasing their book value whereas the book value of the shares of listed companies were still Rs. 10/despite the fact that they were trading at considerably higher price. It can be understood by following example:

Listed company trading at 250/- per share (having book value of Rs. 10/- per share)

Unlisted companies allotted shares at a premium of 240/- per share thereby the increasing the book value of Rs. 250/- per share.

Now the swap ratio will be 1:25 i.e. holder of one share of unlisted company will get 25 shares of listed company according to scheme of amalgamation.

In case the transferee company is a listed company the valuation of shares to be done by an independent Chartered Accountants to decide the swap ratio of shares. Normally the court has nothing to say on valuation of shares of these companies and don’t change the swap ratio of shares. The swap ratio were being decided as per many prevailing methods and acceptable to the court.

Principles laid down by the Supreme Court in Hindustan Lever Employees’ Union v. Hindustan Lever Ltd., AIR 1995 SC 470

Valuation is an art, not an exact science

A combination of the yield method, asset value method and market value method was used was used. Courts not to generally question valuation done by independent professional expert and approved by the shareholders

Valuation of experts not to be set aside in the absence of fraud or malafides on the part of experts The Supreme Court in its decision in Miheer H. Mafatlal (supra) held that Once the exchange ratio has been worked out by a recognised firm of chartered accountants who are experts in the field of valuation and if no mistake can be pointed out in the said valuation, it is not for the court to substitute its exchange ratio especially when the same has been accepted without demur by the ratio, especially when the same has been accepted without demur by the overwhelming majority of the shareholders of the two companies.”

„ The above principles were uniformly followed by Court while sanctioning a scheme.

(b) Preferential Allotment of Equity Shares:-

A preferential issue is an issue of shares or of convertible securities by listed companies to a select group of persons under Section 81 of the Companies Act, 1956 which is neither a rights issue nor a public issue. This is a faster way for a company to raise equity capital. The issuer company has to comply with the Companies Act and the requirements contained in Chapter pertaining to preferential allotment in SEBI guidelines which inter-alia include pricing, disclosures in notice etc. Since it does not require any prior approval of SEBI, the operators chose to adopt this route for raising the capital as an alternate to the merger and chose to provide gain to a close group of people. The shares are bound to be in lock-in-period for a tenure of one year from the date of allotment, the operators chose to allot the shares to ultimate beneficiary only. During the tenure of this gap of one year they rig the price to promised level and reroute the transactions through shell companies.

(c) Allotment of Bonus Shares:-

This method can only be adopted by the companies having free reserves in their books in form of accumulated profits or Share Premium Account. The purpose of a company in issuing bonus shares is to reward or acknowledge the shareholders for being investors in the company. By issuing bonus shares, the company tries to increase the morale of the shareholders. It is a financial reward that the company gives to its shareholders. However in the cases of above type, the main purpose of issuing the bonus shares to the shareholders is to reduce their cost of acquisition, thereby increasing the quantum of Long Term Capital Gain. For Example, if a person buys the shares of a particular company at a price level of 100 and receives 9 shares as bonus, his cost of acquisition stands to Rs. 10/- per share.

(d) Splitting the shares :-

It is the most effective way to camouflage the price of shares. The shareholder does not get affected by any of such proceeding adopted by the company except the effect of Corporate Action of NSDL/CDSL thereby releasing old shares and getting the spitted shares in Demat Account. After split of shares the price of shares on the exchange goes down automatically in proportion with the ratio of split and one doesn’t see anything adverse happening in the scrip.

I hope this write up may be enough for the assessing officers as well as investigating officers to understand and act upon the evidences gathered and being the unaccounted income brought as LTCG to Tax.

Dhruva Purari Singh, IRS

DDIT (Inv.) Unit-2(3),

Kolkata.

Chapter-3

Brief Discussion on All Listed Penny Stocks (Scripts) used in Bogus LTCG Scam.

As discussed in previous chapter we have searched/ surveyed some 32 Share Broking Entities and more than 20 Entry operators. Out of the investigations of such high magnitude, we have unearthed and identified some 84 odd companies which are listed on Bombay Stock Exchange and are being used for providing bogus accommodation entry of Long Term Capital Gain/ Short Term Capital Loss. List of such identified penny Stocks, whose share prices have been apparently manipulated by the syndicate of operators, are as under:

(Detailed names, PAN, Entry operators and promoters of these scripts can be found in the LTCG Database, given in DVD separately..)

The above list is not comprehensive as similar racket is being carried out in many other listed companies.

As given above even SEBI has directed stock exchange to suspend trading in more than 26 Scripts listed in BSE. This is as per the inquiries conducted by SEBI. This step puts force to our conclusion that these penny stocks have been used in providing accommodation entry of Long Term Capital Gain.

We have called data from BSE. After analyzing the data we have identified beneficiaries of Rs. 38373.61.55.346/-. which are being reported subsequently.

In some case promoters/key entry operators of the penny stocks have been identified and their statements have been recorded.

All such scrips have been covered in the statements of entry operators and share brokers. These scrips are under monitoring of SEBI and orders against all such penny stocks by SEBI is expected soon. In some cases SEBI has already passed interim orders and barred the related parties from entering into market transactions.

Complete list of all the penny stocks along with their PAN number, amount of trade value, statements of the promoters of the scripts are given in soft format in DVD, marked as “LTCG Database”.

2. Basis of claiming such Stocks as Penny Stocks and involved in LTCG Scam:-

A. All such penny stock companies have been identified from the trading patterns of the share brokers, statements of entry operators and the post survey inquiries. They all have very common financial and trading patterns.

(1). Initial allotment of shares to beneficiaries is generally done through preferential allotment.

(2). The market price of shares of these companies rise to very high level within a span of one year.

(3). The trading volume of shares during the period, in which manipulations are done to raise the market price, is extremely thin.

4). Most of the purported investors are returned their initial investment amount in cash. Only small amount is retained by the operator as security. Thus, an inquiry would reveal that most of the capital receipts through preferential allotment or other means would have found their way out of system as cash.

(5). Most of these companies have no business at all. Few of the companies which have some business do not have the credentials to justify the sharp rise in Market Price of their shares.

(6). The sharp rise in market price of the shares of these entities is not supported by fundamentals of the company or any other genuine factors.

(7). An analysis in respect of persons involved in transactions apparently carried out in order to jack up the share prices has been done in respect of 84 companies. It has been noted that many common persons/entities were involved in trading in more than 1 LTCG companies during the period when the shares were made to rise which implies that they had contributed to such price rise.

(8). Names of most of the LTCG companies are changed during the period of the scam.

(9). Most of the companies split the face value of shares [this is probably done to avoid the eyes of market analysts].

(10). The volume of trade jumps manifold immediately when the market prices of shares reach at optimum level so as to result in LTCG assured to the beneficiaries. This maximum is reached around the time when the initial allottees have held the shares for one year or little more and, thus, their gain on sale of such shares would be eligible for exemption from Income Tax.

(11). An analysis of share buyers of some of LTCG companies was done to see if there were common persons/ entities involved in buying the bogus inflated shares. It was noted that there were many common buyers [which were paper companies].

(12). The prices of the shares fall very sharply after the shares of LTCG beneficiaries have been off loaded through the pre-arranged transactions on the Stock Exchange floor/portal to the Short Term Loss seekers or dummy paper entities.

(13). The shares of these companies are not available for buy/sell to any person outside the syndicate. This is generally ensured by way of synchronized trading by the operators among st themselves and/or by utilizing the mechanism of upper/lower circuit of the Exchange.

B. A reason to believe also comes through analyzing the trading pattern of these Penny Stocks and their sharp rise and fall. Some of the trading patterns are being discussed here:-

ASHIKA CREDIT CAPITAL LTD [Scrip ID: ASHIKACR, Scrip Code: 590122]

It has been gathered that price of shares of this company rose from T 49 to ? 248.2in just 338 trading days during the period from 2/4/2012 to 11/12/2013. Thus, the market price of share effectively rose from ? 49 to f 248.2 i.e. nearly 5 times in a span of 2 year in 338 trading days only. The volume of trade increased 5 to 6 times during Dec,13. This gives a clear picture that this penny stock has been for providing accommodation entry of Bogus LTCG.

Page Contents

GOLDEN LEGAND LEASING & FINANCE LTD [Scrip ID: GOLD.LEG.LEAE, Scrip Code: 509024]

It has been gathered that price of shares was Rs. 11.39 on 29/01/2014 which rose to Rs. 356 on 18/11/2014 with very low volume i.e. price rigging further price of this script has fallen from ? 356 to ? 117.70 in just 85 trading days during the period from 18/11/2014 to 31/03/2015. Thus, the market price of share effectively fallen from ? 356 to ? 117.70 i.e. nearly 67% in a span of 4.5 Months, in 85 trading days only.

KARMA INDUSTRIES LTD [Scrip ID: KARMA, Scrip Code: 512585]

It has been gathered that price of shares of this company was Rs. 311 on 29/06/2011 which fallen to Rs. 48.5 on 26/09/2011 within the span of 3 months i.e.in just 50 trading days during the period. During the period between 26/09/2011 to 08/02/2012 price of script was moving around Rs. 50 only. Then again spurt in price was made at the fag end of financial year to Rs. 72 on 26/03/2012. Finally script started falling freely from Rs. 72 to Rs. 3.35 within the period of 26/03/2012 to 05/11/2012.

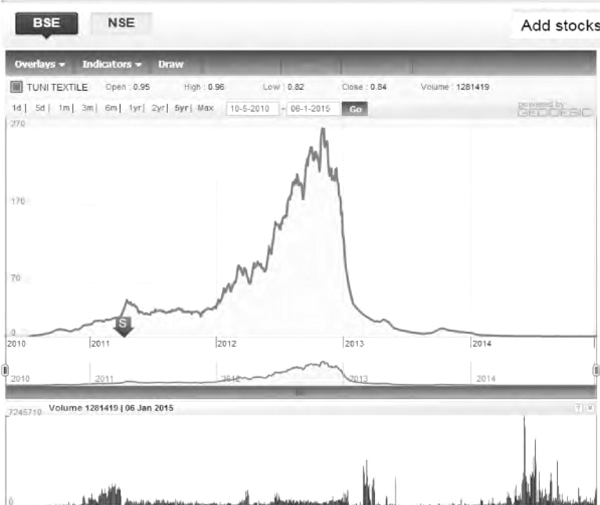

TUNI TEXTILE MILLS LTD. (Scrip ID: TUNI TEXTILE, Scrip Code: 531411)

This company was having market price of share at around ? 32 on 26 September 2011. Thereafter, by rigging the price was jacked up to ? 268.75 from ^ 32.45 in 13 months in November 2012. Thus within 13 months the price was jacked up nearly 8 times. After the bogus LTCG had been reaped the price was made to fall freely so that interested beneficiaries who had booked at high market price can avail bogus Short Term Capital Loss. On November 2012 script was trading at Rs. 268.75 which fallen to Rs. 23 in mid of March 2013 there by booking STCL.

KAILASH AUTO FINANCE LTD. (Scrip ID: KAILASH AUTO, Scrip Code: 511357)

Flash Back:- Kailash Auto Finance Ltd has informed BSE that in connection with Company Petition No. 11 of 2013, filed before the Honorable High Court of Judicature at Allahabad, the honorable Justice Pankaj Mithal on May 09, 2013 has approved the scheme of arrangement interalia, Merger of M/s. Panchshul Marketing Limited and M/s. Careful Projects Advisory Limited with Transferee Company M/s. Kailash Auto Finance Limited in the swap ratio of 1:1, having paid up value of Rs. 1.

Post merger of the companies price rigging was made up to the range of Rs. 40 to 45 in the month of May 2013 itself, the classical unlocking of value of transferee company which was valued at Rs. 1 before merger and get sold at price range of Rs. 40-45 thereby booking the LTCG to the tune of 40 times. Thereafter price of script was maintained at the range of Rs. 40-45 till May 2014 and during this period prospective booking of STCL was done during this period which resulted in final execution in the month of March 2015 at Rs. 4.5

NIKKI GLOBAL FINANCE LTD. (Scrip ID: NIKKIGL, Scrip Code: 531272)

This company was having market price of share at around ? 134 on 09 April 2012. Thereafter, by rigging the price was jacked up to ? 938.75 from ? 134 in 20 months in December 2013. Thus within 20 months the price was jacked up nearly 7 times. After the bogus LTCG had been reaped the price was made to fall freely so that interested beneficiaries who had booked at high market price can avail bogus Short Term Capital Loss. On December 2013 script was trading at Rs. 938.72 which fallen to Rs. 140 in mid of March 2014 there by booking STCL.

EINS EDUTECH LTD. (Scrip ID: EINSEDUTEC, Scrip Code: 511064)

Eins Edutech’s board of directors at its meeting held on December 17, 2013, has approved the Scheme of Arrangement under section 391 to 394 of the Companies Act, 1956 relating to merger of Uniglory Developers with itself. On 17/04/2014 stock was trading at Rs. 18 and with price rigging having very low volume stock was trading at Rs. 287.90 on 3/11/2014.With soft volume in trade price spurt to Rs. 478.30 on 10/03/2015 and announcement of stock split was made on 11/03/2015 thereby bringing face value of stock to Rs. 1.As on 15/04/2015 stock is trading at Rs. 50.50

Effectively stock which was trading on 17/04/2014 at the rate of Rs. 1.80 is now trading at Rs. 50.50, that means 2700 times spurt in price within the span of 1 year.

RAJLAXMI INDUSTRIES LTD. (Scrip ID: RAJLAXMI IND, Scrip Code: 512319)

During the period of March 2013 when script was trading @ Rs. 20, on 4/03/2013 company allotted 3 crores shares to non promoter group stating “The Board has resolved that 3,00,00,000 fully paid up equity shares at a price of Rs. 10/- each be allotted to persons other than the promoters, on preferential basis. The same has been approved by the shareholders at Extra Ordinary General Meeting”.

On 14/08/2013 Scheme of Arrangement u/s 391 to 393 of the Companies Act, 1956, for the Merger of two companies namely, M/s. Hirise Infra con Limited and M/s. Standings Fashion Trading Limited was announced, as on date stock was trading at Rs. 297.80.

From the above two event it is crystal clear that 3 crore shares allotted at par booked the LTCG on Aug 2013 after span of 17 months only, in between these period upward in price movement was 15 times.

On 02/09/2014 stock was trading at 323.80 and by the end of financial year i.e. 2014-15 stock was trading @ Rs. 66.40 on 26/03/2015, where this treasurer lost its shine by almost 80% within 7 months, when Indian stock market was in almost lifetime high. This clearly states market manipulation of shares.

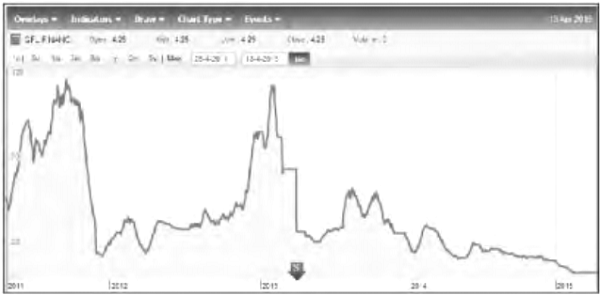

GFL FINANCIALS INDIA LTD. (Scrip ID: GFLFIN, Scrip Code: 531055)

This company was listed on BSE in the month of April 2011 with price range of Rs. 40. Thereafter, by rigging the price was jacked up to ? 115, thereafter price was made to fall freely so that interested beneficiaries who had booked at high market price can avail bogus Short Term Capital Loss in the month of November 2011 i.e. within the span of 2.5 months at the rate of ?15-16.

Again thereafter price rigging was repeated and stock was trading in the range of ? 110- 115 during the month of January 2013. Thus within 14 months the price was jacked up nearly 7 times.

HPC BIO SCIENCES LTD. (Scrip ID: HPCBIO, Scrip Code: 535217)

This company got listed in BSE on 14/08/2013 with Price around Rs. 85, price range of Rs. 85-110 was maintained till November 2013, by rigging the price was jacked up to ? 736 from ? 85 in 16 months in December 2014. Thus within 16 months the price was jacked up nearly 9 times. The bogus LTCG had been reaped and pre listing booking/ private placement of equity with the commitment of LTCG was done.

C. Analysis on the basis of Trade Pattern called from BSE:-

We wrote to BSE asking them to supply us trade data of above mentioned 84 scripts. Most of the trade data have been received and segregated for dissemination DGIT wise. While going through the data we found that, on purchase side (Loss booking side)of the trade, a certain number of share brokers present in the market have done most of the trading through a certain Jamakharchi companies. The same is being given here to prove our point:-

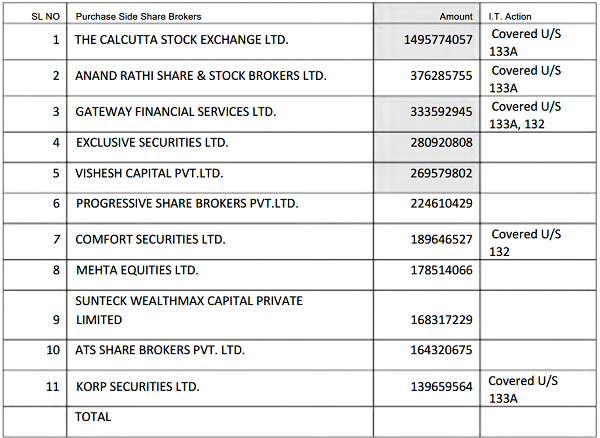

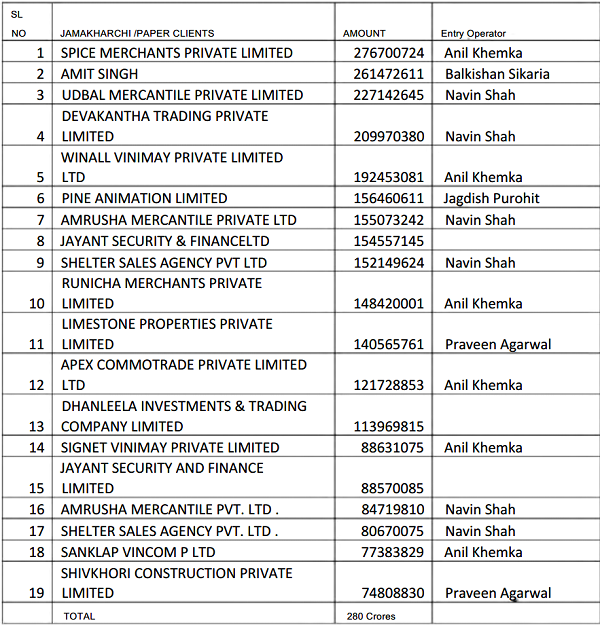

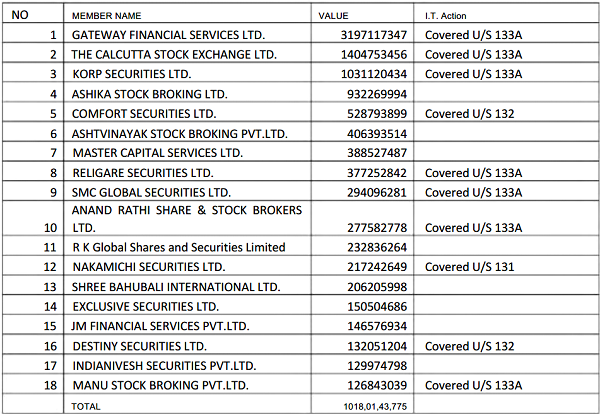

In the Script Radford Global Limited total trade of Rs. 506,92,91,489 /- have been done.

Now if you see the share Brokers details through whom most of the purchases have been done it appears that;

It is clear from the data given above that most of the purchases have done by these top 11 brokers and out of that 5 major brokers have been already covered in our action and they have accepted their active involvement in the scam.

Now if we see the purchasing/ loss booking companies in these scripts we see that most of the purchases on abnormally higher rates are done by identified paper/Jamakharchi companies.

Out of total trade of 500 crore Rs. More than half trades have been provided by above 19 companies. As you can see from the table that most of them have been identified and their statements have been recorded., where they have accepted the fact. Here it is pertinent to mention that Entry Operator Navin Shah have been covered by Mumbai Investigation wing.

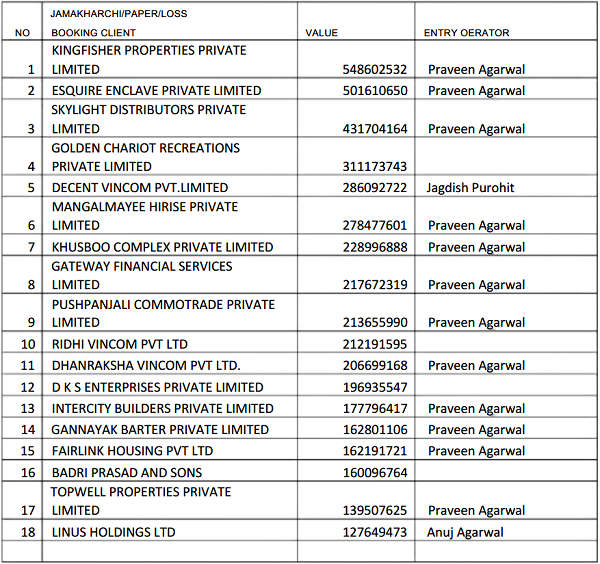

Let us take another example. In the Script Blue Circle Services Limited total trade of Rs. 1387,65,82,309/- have been done . Now if you see the share Brokers details through whom most of the purchases have been done it appears that most of them are actively involved in the scam and they have accepted the same.

Now if we see the purchasing/ loss booking companies in these scripts we see that most of the purchases on abnormally higher rates are done by identified paper/Jamakharchi companies.

As you can see that out of total trade of around one thousand crore 450 crores purchase have been done by these identified jamakharchi companies. Statement of the entry operator and the dummy directors can be found in the “LTCG Database”, given in DVD.

On the pattern given above we have analyzed all the scripts and found that the same pattern is true for each and every script covered in our report.

Chapter-4

Details of Share Brokers involved in the syndicate and their modus operandi.

A share broker is An individual or firm that charges a fee or commission for executing buy and sell orders submitted by an investor. Especially one employed by a member firm of a stock exchange, who buys and sells stocks and other securities for customers. They maintain detailed KYC norms for their clients. They are the bridges between stock market and investors.

As per the guidelines of SEBI and the stock exchanges, the brokers are supposed to comply with stringent KYC norms before registering any entity as their client. They are supposed to perform detailed background checks on their clients. However, it is seen that these share brokers have done trading for various paper/bogus companies. These paper/bogus entities have no business or establishment. This clearly implies that the share brokers are hands in glove with the paper/ bogus companies in the whole scheme. The share brokers receive cash commission for allowing these paper entities to trade through their terminal. In fact it has been learnt that these brokers perform the trading themselves on behalf of the paper/bogus entities. Many brokers have accepted this fact in their statements recorded by the directorate.

They are some share brokers who are willfully allowing entry operators to register their bogus companies as client with them, in lieu of cash commissions. While there is another type of brokers who not only let the entry operators do their dirty game through their trading terminals, but they also maintains their own lot of paper Jamakharchi companies and do all the work of entry operators.

For instance, when we survey Anand Rathi Shares & Stock Brokers Ltd, they instantly accepted that they have let entry operators like Deepak Patwari and Prawesh Beria, open accounts with them in the name of their paper/Jamakharchi companies.

Then there is second kind share broker like Korp Securities Ltd. Shri Anuj Agarwal of Korp Securities is a share broker cum entry operator. He not only works like a share brokers but he has also his own set off Jamakharchi/paper companies registered with him as share broker. In view of the above role of share brokers is not much distinguishable than entry operators. In fact, there are a lot of accommodation entry providers in the market, who not only manage penny stocks and bogus paper client companies, but they are share brokers also.

A. During our project Bogus LTCG/STCL, we have covered following share broking entities in our investigation report.

In many cases share brokers are not independent brokers listed with BSE, but they are sub brokers of other share brokers. In such cases we have taken the data for whole share broking entity.

Here, we can see that from total amount of trade of Rs. 38 thousand Crores in 84 scripts, these brokers have traded more than 15 thousand Crores on purchase side, i.e. loss booking side. A very noticeable point is that, these share brokers have not only accepted their active role in the scam but there have been many incriminating documents found and impounded from their premises, which suggest their active role. All the details of share broker along with their entry operators can be obtained from the “LTCG Database” given in DVD.

C. Broker wise Script wise analysis:

1. THE CALCUTTA STOCK EXCHANGE LTD.

This is the biggest share broker in our list. Here I want to clarify that Calcutta Stock Exchange as a broker is a set of many sub brokers. These sub brokers have taken BSE Terminal through Calcutta stock Exchange Ltd. Most of these sub brokers are involved in providing accommodation entry of LTCG, through floating Jamakharchi/bogus clients. Now, we have raided many such sub brokers, like Bikas Sureka, Anil Khemka, Amit Saraogi, Sauraj Jhunjhunwala, D. B. & Co, and Sajendra Mookim. All have accepted in their statements recorded that they are actively involved in providing accommodation entry of Long Term Capital Gain in lieu cash commission. Many such brokers were found to handling cash of beneficiaries, as impounded documents suggest.

Now if we see Calcutta stock exchange as a broker, then as a whole this broker have traded in such penny stocks as given below:-

2. GATEWAY FINANCIAL SERVICES LTD.