Presumptive Taxation For Professionals under Section 44ADA

Special provision for computing profits and gains of profession on presumptive basis.

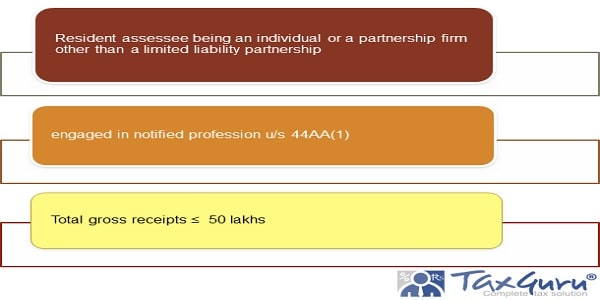

44ADA. (1) Notwithstanding anything contained in sections 28 to 43C, 14[in case of an assessee, being an individual or a partnership firm other than a limited liability partnership as defined under clause (n) of sub-section (1) of section 2 of the Limited Liability Partnership Act, 2008 (6 of 2009), who is a resident in India, and] is engaged in a profession referred to in sub-section (1) of section 44AA and whose total gross receipts do not exceed fifty lacs rupees in a previous year, a sum equal to fifty per cent of the total gross receipts of the assessee in the previous year on account of such profession or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the assessee, shall be deemed to be the profits and gains of such profession chargeable to tax under the head “Profits and gains of business or profession”.

(2) Any deduction allowable under the provisions of sections 30 to 38 shall, for the purposes of sub-section (1), be deemed to have been already given full effect to and no further deduction under those sections shall be allowed.

(3) The written down value of any asset used for the purposes of profession shall be deemed to have been calculated as if the assessee had claimed and had been actually allowed the deduction in respect of the depreciation for each of the relevant assessment years.

(4) Notwithstanding anything contained in the foregoing provisions of this section, an assessee who claims that his profits and gains from the profession are lower than the profits and gains specified in sub-section (1) and whose total income exceeds the maximum amount which is not chargeable to income-tax, shall be required to keep and maintain such books of account and other documents as required under sub-section (1) of section 44AA and get them audited and furnish a report of such audit as required under section 44AB.

Introduction

The Scheme of Presumptive Taxation for Professionals was introduced under Section 44ADA in the Finance Act 2016 and is applicable from Financial Year 2016-17 onwards.

Before 2016, the benefits of Presumptive Taxation were only given to Businesses under Section 44AD and to Transporters under Section 44AE. Specified professionals were specifically kept out of this scheme of Presumptive Taxation.

As Professionals were specifically kept out of the scheme of Presumptive Taxation, the only option available for Professionals was to compute their Income under the normal system of taxation. These professionals were also required to maintain all books of accounts, maintain a copy of invoices for all expenses and in some cases – they were also required to get their Tax Audit conducted.

So many complexities ended up discouraging the professionals from filing income tax returns. So as to simplify the taxation for Professional, the Presumptive Taxation for Professionals was introduced under Section 44ADA in Finance Act, 2016 which is applicable from Financial Year 2016-17 onwards. The scheme of presumptive taxation was extended to professionals by introduction of section 44ADA of the ITA w.e.f. Assessment Year 2017-18. It was made applicable to all assessees, being a resident in India, who is engaged in the profession referred to in sub-section (1) of section 44AA of the ITA.

However, in the memorandum explaining the provisions in the Bill, it is clarified that section 44ADA of the Act are applicable only to individual, Hindu Undivided Family and partnership firm, but not a Limited Liability Partnership (LLP). Accordingly, the Bill proposed to amend sub-section (1) of section 44ADA of the ITA to provide that the provisions of section 44ADA of the ITA shall apply only to an assessee, being an individual, Hindu Undivided Family or a partnership firm, other than a limited liability partnership, who is a resident in India.

However, the Finance Act, 2021 has surprisingly and without any explanation has excluded ‘Hindu Undivided Family’ from the list of assessee, who would be eligible to opt for the presumptive scheme.

The above amendment is applicable from the Assessment Year 2021-22.

Eligible Profession:

Meaning of “Professional services”

“Professional services” means services rendered by a person in the course of carrying on legal, medical, engineering or architectural profession or the profession of accountancy or technical consultancy or interior decoration or advertising or such other profession as is notified by the CBDT for the purposes of section 44AA(1) of the Act.

Section 44AA(1) prescribes for compulsory maintenance of such books of accounts and other documents which will enable the Assessing Officer to compute his total income in accordance with the provisions of this Act. Sub-section(1) applies to the followings-

1. A person carrying on a legal profession.

2. A person carrying on a medical profession.

3. A person carrying on engineering or architectural profession.

4. A person carrying on the profession of accountancy.

5. A person carrying on the profession of technical consultancy.

6. A person carrying on the profession of interior decoration.

7. Any other profession as notified by the Board. The CBDT has notified the following professions u/s44AA(1) of the Act.

(1) A person carrying on the profession of an authorised representative or film artist. [Notification No. SO 17(E) dated 12-1-1977]

“Authorised representative” means a person who represents any other person, on payment of any fee or remuneration, before any tribunal or authority constituted or appointed by or under any law for the time being in force, but does not include an employee of the person so represented or a person carrying on a legal profession or a person carrying on the profession of accountancy.

“Film artist” means any person engaged in his professional capacity in the production of a cinematograph film, whether produced by him or by any other person, as –

(i) an actor ;

(ii) a cameraman ;

(iii) a director, including an assistant director ;

(iv) a music director, including an assistant music director ;

(v) an art director, including an assistant art director ;

(vi) a dance director, including an assistant dance director ;

(vii) an editor ;

(viii) a singer ;

(ix) a lyricist ;

(x) a story writer ;

(xi) a screen-play writer ;

(xii) a dialogue writer; and

(xiii) a dress designer.

Example: Jatinder Sharma who is a professional singer. He is a stage artist and not a Playback singer. He wants to opt the provision of section 44ADA of the Act. Can he do so?

Ans: It is to be noted that by virtue of [Notification No. SO 17(E) dated 12-1-1977], a person carrying on the profession of an authorized representative or film artist is an authorised professional u/s 44AA(1) of the Act. “Film artist” means any person engaged in his professional capacity in the production of a cinematograph film, whether produced by him or by any other person, as singer also. In this connection, it is clear that only those singers are professional u/s 44AA(1) of the Act who are engaged in their professional capacity in the production of a cinematograph film, whether produced by him or by any other person. Hence, stage singers are not professionals for the application of sec 44ADA of the Act. It is also to be noted that the persons who are the singers on religious/social occasions can’t opt the provisions of sec 44ADA of the Act as they are not singers for the purposes od sec 44ADA of the Act.

Whether a Model can opt the provisions of sec 44ADA

In the case of DCIT (TDS) Vs Kodak India (P) Ltd. (ITAT Mumbai) the issue under consideration is whether the services, the modeling, rendered by Ms. Katrina Kaif constitutes professional service and the fee paid to her for modeling with the purpose of marketing of the camera products of the assessee liable for TDS u/s 194J?

Undisputedly, Ms. Katrina Kaif has received the said fee not in connection with production of a cinematographic film and the same received admittedly for modeling. She has not received the sum for acting in an autographic Film. Receipts for all modeling and acting skills of an individual do not attract the said section 194J, unless, they are part of the production of a cinematographic film. In the original sense of the modeling, the same may be a profession and the receipts earned by such models may be professional receipts. But the fact is that modeling is not a defined or notified profession either in the Income Tax Act, 1961 or in the Notifications, In fact, there are many such un-notified professions and as such ones cannot be brought under the provisions of section 194J of the Act. In the instant, admittedly, the services rendered have nothing to do with the production of a cinematographic film. Further, before parting with the order, it is pertinent to mention that a person can have many skills i.e acting skills in Films, modeling skills for display of merchandise, singing skills etc. and such person can make earning out of such skills. It is not that total earning of that person in lieu of services rendered must attract the provisions of section 194J of the Act. Therefore, the taxable receipts u/s 194J of the Act are services-specific and not person specific. Therefore, the impugned payments made by the assessee to Matrix India on behalf of Ms. Katrina Kaif do not attract the provisions of section 194J of the Act.

A model can’t opt the provisions of sec 44ADA of the Act on his income from modeling as a model is not a specified professional for the purposes of sec44ADA of the Act.

The profession of company secretary [Notification No. SO 2675 dated 25-9-1992]

“Company Secretary” means a person who is a member of the Institute of Company Secretaries of India in practice within the meaning of sub-section (2) of section 2 of the Company Secretaries Act, 1980 (56 of 1980).

The profession of information technology [Notification No. SO 385(E) dated 4-5-2001]

Interpretation of Fee for Professional Service

As per definition given under Income Tax Act,1961 following attributes are required to classify a service as “Professional Services”:

1. Service is provided by a person;

2. Service is provided in the course of carrying out any profession;

3. Such service falls under the list of professions given in definition itself or it falls under any other profession notified for Section 44AA. These attributes are discussed below in detail:

a. Service is provided by a person

It is to be noted that “Professional Service” is the one which is rendered by a person.

“person” includes—

(i) an individual,

(ii) a Hindu undivided family,

(iii) a company,

(iv) a firm,

(v) an association of persons or a body of individuals, whether incorporated or not,

(vi) a local authority, and

(vii) every artificial juridical person, not falling within any of the preceding sub-clauses.

So, as per definition given, a person can either be an individual or HUF or Firm or any other artificial person.

However, activities mentioned in the definition of FPS are more into intellectual and artistic nature and the same can be provided by a person only and not by any artificial person.

“In course of Carrying out any profession”

- Profession is a business type which requires intellectual skills only. Further, all professional institutions permit their member professionals to practise in the capacity of Individual or Firm (Proprietorship Firm or Partnership Firm or Limited Liability Partnership Firm). Rationale behind such a condition is that artificial persons have independent liability from its directors and employees. However, in case of profession, complete onus lies on a person providing service. Therefore, profit be differentiated from their associated liability and therefore, they are permitted to practise either in individual name or under name of firm.

It is to be noted that professional services will be applicable to the cases where services are provided by individual or firm of individuals. However, Hon’ble Delhi High Court and Bombay High Court have interpreted the term person used in the definition of professional services is not restricted to the individual or firm of individuals and can be extended even to artificial person or corporate bodies. However, both these decisions were issued in the contest of payment made by Third Party Administrators (‘TPA’) to Hospitals.

However, considering existing legal position as per above mentioned High Court decisions professional services rendered even by an artificial person and body corporate will be covered in the definition of professional service. It is to be noted that certain Sports personnel (Sports Persons, Umpires and Referees, Coaches and Trainers, Team Physicians and Physiotherapists, Event Managers, Commentators, Anchors and Sports Columnists) were notified as professionals by CBDT vide Notification No. 88/2008 dated 21-08-2008. However, this is notified under section 194J of the Income Tax Act, 1961 and not under section 44AA(1). Hence, for the purpose of section 44AA, they will be covered under section 44AA(2). These professionals are not entitled to opt for 44ADA.

Example: A City football Club has engaged Mr. X, a resident in India, as its coach at a remuneration of Rs.10 lacs per annum. The club wants to know from you whether it is liable to deduct tax at source from such remuneration.

Solution: Section 194J requires deduction of tax at source @10% from the amount credited or paid by way of fees for professional services, where such amount or aggregate of such amounts credited or paid to a person exceeds Rs.30,000 in the F.Y. 2021-22. As per Explanation (a) to section 194J, professional services include services rendered by a person in the course of carrying on such other profession as is notified by the CBDT for the purposes of section 194J.

Accordingly, the CBDT has, vide Notification No.88 dated 21.8.2008, in exercise of the powers conferred by clause (a) of the Explanation to section 194J notified the services rendered by coaches and trainers in relation to the sports activities as professional services for the purposes of section 194J.

Therefore, the club is liable to deduct tax at source under section 194J from the remuneration payable to the Coach, Mr. Dev.

Applicability of provisions of Sec 44ADA in case TDS has been deducted u/s 194J

Shri Arthur Bernard Sebastine Pais V. Deputy Commissioner Of Income-Tax, CPC, Bengaluru – Bangalore ITAT (2019). In this case TDS was deducted u/s 194J. The assessee had offered income under 44AD. There was CPC mismatch and was assessed under sec 44ADA. The ITAT held that fees of technical services as enumerated in section 194J is a very broad term which encompasses any services in the nature of managerial, technical or consultancy services. Though the deduction of tax on fees paid to Assessee has been done u/s 194J as mandated by the Act, the services rendered by the Assessee do not fall under section 44AA(1) which is a pre-condition to tax the receipts @ 50% on presumptive basis under section 44ADA. The Assessee cannot be said to be providing technical consultancy as mentioned in section 44AA(1) of the Act.

Example: An Individual who is doing financial consultancy business and the service receiver while he is paying service charge, he is deducting TDS u/s 194J. Whether he can offer income u/s 44ADA? – Sec. 44ADA will be applicable only to the Notified Professions. It is an inclusive definition, it doesn’t cover financial consultancy business, hence he can’t offer income u/s 44ADA. – Notifications No. SO-18[E] dated 12.01.1977, No. SO 2675 dt.25.09.1992 and S.O. 385[E] dt.04.05.2001

Meaning of authorised representative-

Explanation to Rule 6F

Authorised representative means a person who represents any other person, on payment of any fee or remuneration before any Tribunal or authority constituted or appointed by or under any law for the time being in force, but does not include an employee of the person so represented or a person carrying on legal profession or a person carrying on the profession of accountancy.

Eligible Business-Financial consultancy

EXAMPLE: An Individual who is doing financial consultancy business and the service receiver while he is paying service charge, he is deducting TDS u/s 194 J. Whether he can offer income u/s 44ADA?

Ans. No. Sec. 44ADA will be applicable only to the Notified Professions. It is an inclusive definition, it doesn’t cover financial consultancy business, hence he can’t offer income u/s 44ADA

Presumptive rate of income: Presumptive rate of income would be a sum equal to 50% of the total gross receipts, or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the assessee.

Eligible Assessee: All the three conditions should be satisfied:

No further deduction would be allowed: Section 44ADA(2) :Under the scheme, the assessee will be deemed to have been allowed the deductions under section 30 to 38. Accordingly, no further deduction under those sections shall be allowed.

Written down value of the asset: Section 44ADA(3) :The written down value of any asset used for the purpose of the profession of the assessee will be deemed to have been calculated as if the assessee had claimed and had actually been allowed the deduction in respect of depreciation for the relevant assessment years.

Maintenance of books of accounts and audit:

A very interesting issue is that whether a professional who has opted presumptive system of taxation has to maintain books of account also. To resolve this issue firstly we have to see the provisions of section 44AA(1) of the Act .

Section 44ADA overrides section 28 to section 43C but does not override section 44AA. Section 44AA(1) provides for compulsory maintenance of books of accounts by a person carrying on specified profession. Further, section 44ADA can be opted only by a person carrying on a specified profession in section 44AA(1). Therefore, on the plain reading of the law, it appears that it is mandatory for a person carrying on a specified profession as per section 44AA(1) has to compulsorily maintain books of accounts even if such a person declares his income as per section 44ADA(1).

If this interpretation is invoked, then the purpose of simplification will get defeated. The purpose of introducing the presumptive taxation is to provide relief to small taxpayers from the burden of maintaining the detailed books of account and reducing the cost of compliances.

The memorandum to Finance Bill 2016 states that in order to rationalize the presumptive taxation scheme and to reduce the compliance burden of the small taxpayers having income from profession and to facilitate the ease of doing business, it is proposed to provide for presumptive taxation regime for professionals. It further states that the assessee will not be required to maintain books of account under sub-section (1) of section 44AA and get the accounts audited under section 44AB in respect of such income unless the assessee claims that the profits and gains from the aforesaid profession are lower than the profits and gains deemed to be his income under sub-section (1) of section 44ADA and his income exceeds the maximum amount which is not chargeable to income-tax.

Further, the ‘FAQs on Tax on Presumptive Taxation Scheme’ published on income tax portal clarifies the same in the following manner-

If a person adopts the presumptive taxation scheme of section 44ADA, then he is required to maintain books of account as per section 44AA?

In case of a person engaged in a specified profession as referred in sections 44AA(1) and opts for presumptive taxation scheme of sections 44ADA, the provision of sections 44AA relating to maintenance of books of account will not apply. In other words, if a person opts for the provisions of sections 44ADA and declares income @50% of the gross receipts, then he is not required to maintain the books of account in respect of the specified profession.

Even though the FAQ is not the law but still it can be an aid to interpretation on the issue. This view shall further fortify from the speech of the Finance Minister.

In the Budget Speech of the then Finance Minister while presenting the Union Budget 2016 stated as follows-

“At present about 33 lacs small business people avail of this (presumptive taxation scheme under section 44AD) benefit, which free them from the burden of maintaining detailed books of account and getting audit done.

I also propose to extend the presumptive taxation scheme to professionals with gross receipts up to Rs.50 lacs with the presumption of profit being 50% of the gross receipts.”

From the speech, it is also suggested that professionals opting the presumptive taxation scheme with gross receipts up to Rs.50 lacs with the presumption of profit being 50% of the gross receipts are not required to maintain books of accounts.

The legislative intent is very clear that such a professional is not required to maintain books of account under section 44AA. Although, it can be said that when the plain meaning of the words of the statute is unambiguous, there is no need to resort to external aid for interpretation. However, one should not forget that it is a beneficial provision provided to small taxpayers and hence is required to be interpreted liberally.

From the perusal of above section, it is clear that it is mandatory for the professional who is covered under Section 44ADA to maintain books of accounts even though he has opted for the presumptive taxation scheme. Although, the Memorandum to the Finance Bill, 2016 provides that an assessee opting for Section 44ADA would not be required to maintain books of account under Section 44AA(1), the same has not been brought out clearly in the Section 44AA. Section 44AA is silent in relation to the assessee who is covered by Section 44ADA. Moreover the provisions of Sec 44ADA overrides sec 28 to 43C and not sec 44AA of the Act. Hence, on combined reading of 44AA(1), 44AA(3) read with Rule 6F, the specified professionals would need to maintain books of account even if they opt for section 44ADA.

Option to claim lower profits: Section 44ADA(4):An assessee may claim that his profits and gains from the aforesaid profession are lower than the profits and gains deemed to be his income under section 44ADA(1); and if such total income exceeds the maximum amount which is not chargeable to income-tax, he has to maintain books of account under section 44AA and get them audited and furnish a report of such audit under section 44AB.

- Partner’s Salary, Remuneration, Interest even though charged under the head as income from „ Business or Profession „ can be taxed u/s 44ADA in the hands of the individual partner having professional income.

A question comes to our mind that whether the provisions of Section 44ADA shall be applicable to the remuneration and other receipts by a partner from a professional services firm? In this connection, it is to be noted that the Income Tax Act, 1961 vide Section 40(b) states that the firm is eligible to claim remuneration as deduction to the extent specified therein and such remuneration is deductible in hands of the firm. The balance amounts are subjected to tax as profits in the hands of the firm. In other words, the eligible remuneration is deductible in the hands of firm and taxable in hands of partners, the remainder (profit) is taxable in hands of the firm and exempted in the hands of partners u/s 10(2A).

Hence, in the hands of the partner, the following will be the impact:

1. Remuneration which was allowed as deduction in firm will be taxable

2. Profit which was taxed in the hands of the firm will be exempt.

Now a question arises whether the remuneration and other income received from the firm can be called as ‘gross receipts’ for the purposes of Section 44ADA. Whether the share of profits of a partner can be considered as gross receipts for the purpose of Section 44ADA? The Mumbai Bench of the Income Tax Appellate Tribunal in the case of: ACIT v. India Magnum Fund (81 ITD 295) held that in order to trigger the provisions of Section 44AB, there should be first computation of profits and gains of business or profession i.e. computation of total income as per Section 4. As the income exempt under Section 10 does not form part of the total income, such exempt income cannot be subjected to the provisions of Section 44AB. Consequently, one may argue that share of partners profit which is exempt under section 10(2A) would not be considered for the purposes of the gross receipts This view is also supported by the guidance note issued by The Institute of Chartered Accountants of India on tax audit. As per the guidance note, gross receipts exclude partner’s share of profit which is exempt u/s 10(2A).

We are of the opinion that the provisions of Section 44ADA is applicable either for an individual or partner in a profession firm. This is also supported by certain judicial pronouncements (though not directly on the said issue) in the case of Sagar Dutta vs DCIT (ITAT Kolkata) and Usha A Narayanan vs Deputy Commissioner of Income Tax (ITAT Kolkata).

Sagar Dutta Vs. DCIT (2014) 45 taxmann.com 575 (Kol.Trib). Order dated 17 February, 2014

After considering the submissions of both the parties, we find that in the instant case penalty of Rs.37,080/- was imposed u/s 271B of the Act by the AO as the assessee failed to filed audit report u/s 44AB of the Act along with the return of income. It is not in dispute that the assessee received salary from M/s. Price Waterhouse which is a partnership firm and that the same was assessed to tax under the head profit an gains from business or profession. The total receipts from profession of the assessee was Rs.74,16,000/- which was exceeding Rs.10 lacs and therefore in view of the provision of section 44AB the assessee was required to get his audit report u/s 44AB of the Act and file the same along with the return of income within the due date prescribed u/s 139(1) of the Act. The assessee failed to do so. Therefore, the assessee was liable to levying of penalty u/s 271B of the Act @0.5% on total professional receipts of the assessee. We find that in the similar facts and circumstances of the case the Kolkata ‘A’ Bench of the Tribunal in the case of Amal Ganguli (supra) has confirmed the levy of penalty by observing as under :-

“. We have carefully considered the submissions of the ld. Representatives of the parties and the orders of the authorities below. We have also considered the provisions of section 44AB of the Act. There is no dispute to the fact that the assessee is a Chartered Accountant and is engaged in the profession. However, the assessee is a partner in the firm “Price Waterhouse” which is a firm of Chartered Accountants. We are of the considered view that the assessee is carrying on the profession of Chartered Accountant though not individual but as a partner. The assessee has received income by way of salary, allowance, commission and interest on capital from the firm. During the course of hearing, the ld. A.R. in reply to a query from the Bench admitted that the assessee is holding a certificate of practice to carry on the profession. Therefore, the assessee has received the above amount from the firm as a partner and he is a partner only because he is engaged in the business of Chartered Accountants and is eligible to carry on the profession of Chartered Accountant.

Thus we are of the considered view that the assessee has received the said amount as a professional fee as a partner from the firm. There is no dispute to the fact that the amount received by the assessee by way of salary, allowance, commission, interest from the firm is assessable under section 28(v) of the Act under the head “profits and gains of business or profession”. Since the receipt of the assessee is more than Rs.10 lacss, in the previous year relevant to the assessment year under consideration, we are of the considered view that the assessee is required to get his accounts audited as per section 44AB of the Act and to enclose a copy of the said report in the prescribed form before the specified date. The assessee has admittedly not got his accounts audited under section 44AB of the Act. Therefore, we hold that the ld. CIT (A) has rightly confirmed the action of the AO to impose penalty under section 271B of the Act of Rs.58,719/-. Hence, we uphold the order of the ld. CIT (A) and reject the grounds of appeal taken by the assessee.”

Usha A Narayanan Vs. DCIT. ITA NO: 703/Kol/2012. Order Dated 25/03/2013.(Kol. Trib).

The short issue in this appeal is whether or not penalty under section 44AB will also be attracted in the case in which the professional income of the assessee received from partnership firm of Chartered Accountants is taxable under the head “income from business or profession”. In the relevant previous year, the assessee, a Chartered Accountant, received Rs.32,76,000/- from M/s. Lovelock & Lewes of which she was a partner. In terms of section 28(v), the said income was taxable under the head “Profits & Gains from Business or Profession”. The Assessing Officer was of the view that the assessee ought to have obtained the audit report under section 44AB of the Income Tax Act and her failure to do so, invited penalty under section 271B of the Act.

The assessee’s contention, on the other hand, was that since the assessee was not carrying out any independent profession and the taxability of the said income received under the head “profits and gains from business or profession” was only due to technical requirement of section 28(v) of the Act the provisions of section 44AB are not attracted. The Assessing Officer rejected this plea of the assessee on the basis of a decision of this Tribunal in the case of Amal Ganguly (ITA No. 2135/Kol./2008, Assessment Year 2003-04) vide order dated 20.02.2009. The Assessing Officer was of the view that since the plea raised by the assessee is not acceptable to the jurisdictional Tribunal, the same cannot be accepted by him. Respectfully following the view of the Tribunal and thus holding that the assessee ought to have got her accounts audited under section 44AB of the Act, the Assessing Officer imposed penalty of Rs.16,380/- under section 271B of the Act.

Aggrieved, the assessee carried the matter in appeal before ld. CIT(Appeals) but without any success. Ld. CIT(Appeals) also took note of the decision of the Coordinate Bench of this Tribunal, which covered the issue against the assessee. The assessee is not satisfied and is in further appeal before us.

We see no reason to take any contrary view other than the view so taken by the Coordinate Bench of this Tribunal in the case of Amal Ganguly (supra). Respectfully following the said decision, we uphold the action of authorities below and decline to interfere in the matter.”

The following is evident from the above judgments:

1. In both the judgments, the tax payers were chartered accountants in partner capacity in a firm.

2. Both of them have received remuneration, salary, interest on capital and others more than the threshold limit specified under Section 44AB.

3. The department is of the view that since the gross receipts (remuneration, salary, interest on capital and others) were in excess of threshold limits specified under Section 44AB, the tax payers would have got their books of accounts and audited.

4. Since the tax payers failed to do so, the department has levied penalty under Section 271B amounting to 0.5% of the receipts.

5. The tax payer contention was that they were not carrying any profession in individual capacity but they were acting as partner and hence tax audit requirements does not attract.

Both the Tribunals relying on Amar Ganguly judgment stated that the tax audit will be applicable despite the individual is receiving amounts from firm. Hence, such amounts being in excess of threshold limit, the books of accounts need to be audited and confirmed the penalty.

Our Inference from the above judgments:

Based on the above judgments, the question that whether the salary, remuneration, profit, interest on capital and others received by partner from a partnership firm can be called as gross receipts for the purposes of 44ADA is answered in positive. If such amounts are not to be called as gross receipts, then there is no requirement for the Tribunals to state that such individuals would fall under ambit of Section 44AB.

In light of the above, the amounts received from the firm can be considered as gross receipts and accordingly provisions of Section 44ADA will be applicable. Hence, the benefit of 50% of gross receipts offering to income tax is possible.

Whether option of sec 44ADA optional or mandatory

Further, one more question that is to be answered is whether the provision of Section 44ADA is optional or mandatory, that is to say, is it mandatory for the partner whose gross receipts is less than Rs.50 lacs to apply the provisions of Section 44ADA or is it optional. Once the gross receipts are less than Rs.50 lacs the partner has to mandatorily offer 50% of such gross receipts for tax. In a case, where the partner thinks his expenditure is more than 50% or want to offer lower amounts of gross receipts for tax, he should then get his books of accounts audited as per provisions of sub-section (4) of Section 44ADA.

Radiology & pathological laboratory run by a physician (M.D./ M.B.B.S. not specialized in radiology or Bio-chemistry) will be considered as profession or business for limits of tax audit?

s. 2(13) of the Income-tax Act, 1961 defines ‘business’ which includes any trade, commerce or manufacture or any adventure or concern in the nature of trade, commerce or manufacture. The word ‘business’ is one of wide import and it means activity carried on continuously and systematically by a person by the application of his labour or skill with a view to earning an income. While S. 2(36) of the Act defines ‘profession’ to include vocation. The Supreme Court in CIT vs. Manmohan Das (deceased) [59 ITR 699] has held that, the expression ‘profession’ involves the idea of an occupation requiring purely intellectual skill or manual skill controlled by the intellectual skill of the operator, as distinguished from an operation which is substantially the production or sale or arrangement for the production or sale of the commodities. So, from the facts of the case it is clear that radiology and pathology operated by a doctor who is not specialized would be a business. This view is supported by the Guidance Note on Tax Audit u/s. 44AB of the Income-tax Act, 1961, issued by the Institute of Chartered Accountants of India.

Presumptive Taxation in case of Partnership firms

Resident Partnership Firms are eligible to opt for presumptive taxation u/s 44AD or 44ADA or 44AE. Sec 44AD and 44AE were amended in 1997 w.e.f. 01/04/1994 to allow remuneration and interest to partners (subject to conditions and limits specified in section 40(b)) after determination of profits as per sec 44AD or 44AE. However, by Finance Act, 2016, second proviso to Section 44AD(2) has been omitted which provided for deduction under section 40(b) with regard to the salary and interest to partners. However, sec 44AE has not been amended. Hence, remuneration and interest to partners will not be allowed in sec 44AD of the Act. However, remuneration and interest to partners will be allowed if income is declared u/s 44AE. The provisions of sec 44ADA of the Act are silent for the allowance remuneration and interest on capital to partners. The professional firms can take this benefit as is explained in the following example.

Example : RSK & Associates, a firm of Chartered Accountants provides the following information:

| Receipts | Net Profit | 50% of receipt | Allowability of remuneration |

| Rs.40,00,000 | Rs.20,00,000 | Rs.20,00,000 | No remuneration and interest will be allowed as expense. |

| Rs.40,00,000 | Rs.24,00,000 | Rs.20,00,000 | Remuneration and interest can be allowed up to Rs.4,00,000, subject to sec 40(b) |

| Rs.40,00,000 | Rs.18,00,000 | Rs.20,00,000 | Sec 44ADA not applicable as profit is claimed to be less than 50% of receipts. RSK & Associates will be required to get their books of account audited u/s 44AB(d). Remuneration may allowed as per sec 40(b). |

Author Bio

If gross receipts are of 40 lakhs in bank account, but only Rs 10 lakhs are withdrawn and balance left is Rs 30 lakhs. Then under presumptive scheme 44ada how much income to be shown for calculating tax?

It’s an insightful article but I don’t concur with all the views shared in the article. There are various codes that are available in ITR 4 under sec 44ADA including individual artists and other cultural activities. Artists and professionals engaged as musicians, singers and painters are allowed to take advantage of this scheme. They are not notified professions under sec 44AA but department has allowed them to compute income under Sec 44ADA.

Sir whether only professionally qualified accountants (ie CA /CMA ) are eligible to opt under 44ADA in respect of the category “A person carrying on the profession of accountancy”?

Please refer the madras high court judgement on [2020] 122 taxmann.com 252 (Madras)

HIGH COURT OF MADRAS

Anandkumar

v.

Assistant Commissioner of Income Tax, Circle-2, Salem

T. S. SIVAGNANAM AND MRS. V. BHAVANI SUBBAROYAN, JJ.

TAX CASE APPEAL NO.388 OF 2019

DECEMBER 23, 2020

wherein it is held that Section 44AD is available only for an eligible assessee engaged in an eligible business, hence, interest and salary received by assessee not carrying on business independently but only as a partner in firm could not be construed as business income under section 28(v) and therefore not eligible for applying the presumptive interest rate of 8 per cent under section 44AD; only remuneration and salary, received from a firm, to extent of eligible under clause (b) of section 40, would be considered as profits and gains of business or profession of recipient partner .

Please let me have your views on this.