Preamble:

Place of Effective management means a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are, in substance, made.

PoEM is a newly emerged concept. It was firstly introduced via Indian Budget 2015 by our Honourable finance minister Arun Jaitley. As per the budget speech and mentioned in memorandum to the said Finance bill, there were basically two concepts behind introducing the PoEM (Place of Effective Management) concept in India.

1. The modification in the condition of residence in respect of company to align the provisions of the Income Tax Act, 1961 with the Double Taxation Avoidance Agreements (DTAAs) entered into by India with other countries and with the International Standards

2. To sever upon the planning of creating Shell companies outside India but being controlled and Managed from India.

India is not the only and first country to adopt PoEM concept. Russia, South Africa, China, Netherlands, Germany, UK, Australia, Singapore and various other countries are already following concept of POEM in one or other name since years.

Basically, the introduction of PoEM concept has casted radical impact on application of Section 6(3) which is related with determination of Residential status of Company. Such impact has been discussed as follow.

Applicability:

Even though the concept was introduced via Indian Budget, 2015 its applicability has been deferred from budget to Budget and finally it is applicable from financial year 2016-17 and onwards. This is to be check out with from year to year.

As per the circular no 08 dated on 23rd February 2017, such concept of PoEM shall not apply to a company having turnover or gross receipts of Rs. 50 Crores or less in a financial year.

Statutory Mandates: There are basically three statutory Mandates as under:

1. Section 6(3) of The Income Tax Act, 2016

2. Final guidelines for determination of POEM dated on 24th January, 2017

3. Circular no. 08 dated on 23rd February 2017

Before Amendment:

As per section 6(3), a company is said to be resident of India, if a company is having its incorporation in India. If the company is not incorporated in Indian but it is wholly managed from India. Then in such case, such company incorporated outside India would have been considered as resident in India even though incorporated outside India.

But in the application of above provision. It was very easy to cook a case by just taking a substantial decision outside India and proving that the company is not managed wholly from India but it is also partially from outside the Indian therefore such second clause of Section 6(3) was of no effect. But due to introduction of Concept of PoEM such planning is not going to remain in effect any more.

After Amendment:

As per section 6(3), a company is said to be resident in Indian, if a company is having its incorporation in India. If the company is not incorporated in Indian but if having PoEM in India. Then in such case, such company incorporated outside Indian would have been considered as resident in India.

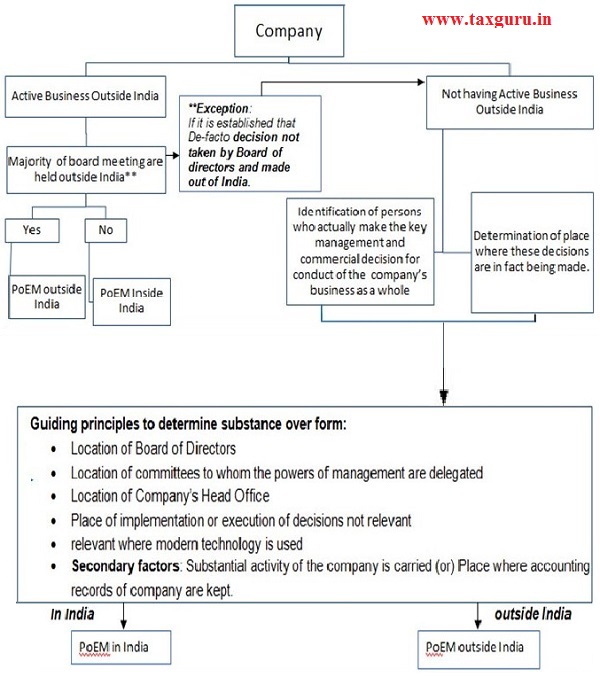

Determination of PoEM:

1. Determine place of Active business of the company.

A company shall be said to be engaged in “active business outside India” if the passive income [income* from the purchase and sale of goods is from / to its associated enterprises + royalty, dividend, capital gains, interest (not to be considered in case of banking or is a public financial institution) or rent] is not more than 50% of its total income; and

(i) less than 50% of its total assets (average of its value for tax purposes (in absence as per books of Accounts) in the country of incorporation of the company at the beginning and at end of the previous year) are situated in India; and

(ii) less than 50% of total number of employees (average of opening and closing number of employees) are situated in India or are resident in India; and

(iii) The payroll expenses (Average) incurred on such employees is less than 50% of its total payroll expenditure.

For the purpose of determining whether the company is engaged in active business outside India, the average of the data of the previous year and two years prior to that shall be taken into account. Where the accounting year for tax purposes, in accordance with laws of country of incorporation of the company, is different from the previous year, then, data of the accounting year that ends during the relevant previous year and two accounting years preceding it shall be considered.

Example: Romania is following Calendar Year system then for F.Y. 2016-17, the relevant financial year would be Calendar Year 2016.

* Here the term “Income” means either for tax purpose (As per their law) or if there is no such law then as per books of Accounts.

2. If active business of the company falls outside India, then check whether majority of Board meeting has been conducted within India, if it is so, then PoEM is to be said to be in India and vice versa. But if Board of Directors has delegated such authority to take key management and commercial decision to any other consultant, professional, committee then PoEM is to be determined as if the company is having active business inside India.

To determine who is taking key management and commercial decision, concept of substance over legal form shall apply.

3. If active business of the company doesn’t fall outside India, the company shall identify the person/s actually making the key management and commercial decision for conduct of the company’s business as a whole and place where these decisions are in fact made.

For this purpose, place of decision taken is more important than the place of its implementation. Mere formal holding of board meetings at a place would by itself not be conclusive for determination of POEM being located at that place.

The Head Office of the company may be the place where key decisions are taken. In case where the company is more decentralised, the company’s location of Head Office would be the place where senior management are primarily based or normally return to following travel to other location or meet when formulating or deciding key strategies and policies for the company as a whole.

In case where meeting is held via telephone or video conferencing, then head office would normally be the location where highest level of Management and their direct support staff is located. If it doesn’t lead to a certain decision regarding to the head office, then the place where the directors or the persons taking the decisions or majority of them usually reside may also be a relevant factor.

In case of Circular resolution, the place of location of the persons taking part into key decisions making process would be relevant. The decisions made by shareholder on matters which are reserved for shareholder decision under the company laws are not relevant for determination of a company’s place of effective management even if such decisions taken are of significant nature. If the shareholders limit the authority of board and senior managers of a company and thereby remove the company’s real authority to make decision then the shareholder guidance transforms into usurpation and such undue influence may result in effective management being exercised by the shareholder. Here the term ‘Decision’ doesn’t include day to day decision.

Residual Factor/Secondary Factors:

If any of the above mentioned factor doesn’t lead to clear identification of PoEM then, the place where main and substantial activity of the company is carried out or Place where the accounting records of the company are kept would be considered.

There are certain misconception regarding following factors about its impact on PoEM but actually which shall not have any impact on determination of PoEM.

Location of 100% holding company, PE of the company, Residence of one or more directors, Location of local management, location of support function are the factors, if they are in India, one may be misguided to concluded to determine PoEM in India but actually, they shall not affect the POEM at all.

It is reiterated that the above principles for determining the POEM are for guidance only. No single principle will be decisive in itself. The above principles are not to be seen with reference to any particular moment in time rather activities performed over a period of time, during the previous year, need to be considered. In other words a “snapshot” approach is not to be adopted. Further, based on the facts and circumstances if it is determined that during the previous year the POEM is in India and also outside India then POEM shall be presumed to be in India if it has been mainly /predominantly in India.

Assessment:

The Assessing Officer (AO) shall, before initiating any proceedings for holding a company incorporated outside India, on the basis of its POEM, as being resident in India, seek prior approval of the Principal Commissioner or the Commissioner, as the case may be. Further, in case the AO proposes to hold a company incorporated outside India, on the basis of its POEM, as being resident in India then any such finding shall be given by the AO after seeking prior approval of the collegium of three members consisting of the Principal Commissioners or the Commissioners, as the case may be, to be constituted by the Principal Chief Commissioner of the region concerned, in this regard. The collegium so constituted shall provide an opportunity of being heard to the company before issuing any directions in the matter.

Burning Issues:

1. How to prove nexus between goods sold to the associated enterprise from the goods purchased from Associated Enterprise for calculation of Passive Income?

2. In case of merger of a company during the relevant financial year, whether for merged company POEM is to be determine? Or cut-off date is to be taken on the last date of the relevant financial year?

Further, In case of merged entity (i.e entity remains in existence after merger), if during the three years’ merger has taken place, then it may so happen that data taken for the period before merger shall not include the data of merging entity (i.e entity which will not remain in existence after merger) whereas the data after merger shall include data of merging entity as well as merged entity, this may lead to inconstancy of the data in nature (i.e proportion of related party transactions). Which may not help to determine place of Active business properly and accordingly, may affect PoEM.

3. Which exchange rate is to be taken for converting the turnover of the company from foreign currency to INR? Whether as per AS 11 or as per their domestic law or the RBI reference rate or so…

4. How to detect such companies which are managed from India which is having complete day to day operation outside India and no financial transaction is conducted via India except for Key decision making?

5. In case where the company is not under any statutory obligation to maintain documentation as per its local statutes with regard to decision taken, then how to prove that decisions have been taken outside India?

Excellent Article