Case Law Details

Gartner Ireland Ltd. Vs DCIT (ITAT Mumbai)

The case of Gartner Ireland Ltd. vs. DCIT (ITAT Mumbai) revolves around the classification of income received by Gartner Ireland Ltd. (GIL) from the sale of online subscription-based products to Gartner India Research & Advisory Services Pvt. Ltd. (Gartner India). The primary contention in this appeal is whether the income should be treated as business income or royalty income for tax purposes under the Income Tax Act, 1961 and the India-Ireland Double Taxation Avoidance Agreement (DTAA).

Background and Facts of the Case

Gartner Ireland Ltd., incorporated in Ireland, is engaged in distributing subscription-based research products globally, including in India. The products involve qualitative research and analysis in various sectors such as IT, finance, HR, marketing, etc. Gartner India acts as a reseller of these products in India, purchasing them from GIL and selling them further to Indian customers.

Issues Raised by the Assessee

1. Characterization of Income:

The crux of GIL’s appeal revolves around the characterization of its income. They argue that the income derived from the sale of subscription-based products should not be classified as royalty under Section 9(1)(vi) of the Income Tax Act and Article 12 of the Double Taxation Avoidance Agreement (DTAA).

- Legal Framework: GIL challenges the application of Section 9(1)(vi) of the Income Tax Act, which defines royalty broadly to include consideration for the transfer of all or any rights in respect of any copyright. They contend that their transactions with Gartner India do not involve the transfer of copyright or any rights to use copyright-protected material.

- Argument: GIL asserts that the subscription-based products they sell to Gartner India do not grant Gartner India the right to use copyrighted materials in a manner that would constitute royalty income. Instead, they argue that these transactions are more akin to the sale of goods or products where Gartner India acts as a distributor, purchasing the products and reselling them to end customers.

- Case Law and Precedents: The appeal likely cites relevant case law and precedents where similar transactions have been classified as business income rather than royalty income. They might emphasize cases where courts have distinguished between payments for use of copyright and payments for goods or services.

2. Business Income vs. Royalty:

GIL’s second main contention pertains to the classification of the income as business income rather than royalty income.

- Nature of Transaction: GIL argues that the transactions with Gartner India should be characterized as business income because they involve the sale of subscription-based products. These products do not grant Gartner India the right to use copyrighted material but rather provide access to services or products that GIL produces.

- No Transfer of Rights: Since there is no transfer of copyright or rights to use copyright, GIL asserts that the income generated from these transactions should not be treated as royalty under the DTAA or domestic tax law provisions.

- Principal-to-Principal Basis: They likely emphasize that Gartner India operates on a principal-to-principal basis, where they purchase products outright from GIL and then resell them. This relationship further supports the characterization of the income as business income rather than royalty.

3. Permanent Establishment (PE):

Another critical aspect of GIL’s appeal is the assertion that they do not have a Permanent Establishment (PE) in India.

- Definition and Implications: GIL argues that since they do not have a PE in India as defined under the DTAA, the income derived from their transactions with Gartner India should not be taxable in India.

- DTAA Application: They likely refer to the specific provisions of the DTAA between India and their home country (possibly the USA) to substantiate their claim that the absence of a PE precludes India from taxing the income.

- Supporting Evidence: GIL might provide factual evidence or legal arguments demonstrating that their activities in India do not meet the threshold for constituting a PE under the relevant tax treaty.

- Avoidance of Double Taxation: By asserting the absence of a PE, GIL seeks to ensure that the income is not taxed both in their home country and in India, thereby aligning with the principles of international tax law and the objectives of the DTAA.

Assessing Officer’s Position

The Assessing Officer (AO), backed by the Dispute Resolution Panel (DRP), held that the income qualifies as royalty under the Income Tax Act and the DTAA. Their argument hinges on the interpretation that the consideration received by GIL involves the right to use or access copyrighted material, thereby constituting royalty income. They also cited precedents and judicial decisions, including those from the Karnataka High Court, to support their position.

Arguments and Analysis

Nature of Transaction:

GIL argues that the transactions with Gartner India involve the straightforward sale of subscription-based products, which do not constitute a transfer of copyright or rights to use copyright-protected material. According to GIL’s interpretation, these transactions resemble a sale of goods where Gartner India acts as a distributor on a principal-to-principal basis. The crux of GIL’s argument lies in the assertion that no intellectual property rights are transferred to Gartner India as part of these transactions. They emphasize that the essence of their business dealings with Gartner India revolves around the sale and distribution of products rather than licensing intellectual property.

To support this contention, GIL may provide detailed contractual arrangements, invoices, and other commercial documents that outline the nature of their transactions with Gartner India. They might highlight specific clauses in these documents that indicate the absence of any rights to use or access copyrighted material by Gartner India. Furthermore, GIL could present industry practices and standards that distinguish between sales of products and licensing of intellectual property, reinforcing their argument that the income derived should be classified as business income rather than royalty income.

Legal Precedents:

GIL’s case also involves challenging the applicability of previous legal precedents, particularly citing the Wipro Ltd. case where similar transactions were categorized as royalty income. They contend that the factual and legal contexts of their transactions with Gartner India differ significantly from those examined in previous cases. GIL likely argues that changes in their operational model, market conditions, and contractual arrangements with Gartner India necessitate a fresh evaluation under the current legal framework.

In presenting their arguments, GIL may analyze the specific judgments and rulings in the Wipro Ltd. case and other relevant precedents. They might identify key differences in factual scenarios, contractual terms, and the nature of products or services involved to distinguish their case. GIL could also challenge the legal reasoning applied in previous decisions, suggesting that those decisions may not appropriately address the nuances of their specific business model and contractual relationships.

DTAA Interpretation:

Central to GIL’s appeal is the interpretation of the Double Taxation Avoidance Agreement (DTAA) between India and Ireland regarding the classification of income from subscription-based products. GIL contends that the income derived from these products does not meet the definition of royalty as outlined in the DTAA. They argue that under the treaty provisions, royalty typically involves the right to use or access copyrighted material, which is not applicable in their case.

In their analysis, GIL would likely examine the specific language and definitions provided in the DTAA regarding royalty income. They may highlight any exclusions or exceptions that could potentially apply to their transactions with Gartner India. GIL might also provide expert opinions or interpretations of international tax law principles to support their position that the income derived should be classified as business income rather than royalty income under the DTAA.

Tribunal’s Decision

The Income Tax Appellate Tribunal (ITAT) Mumbai, after hearing both parties and examining the material on record, decided to remand the case back to the Assessing Officer for fresh consideration. The ITAT noted discrepancies in the evidence presented regarding the nature of transactions between GIL and Gartner India, especially in terms of whether there was an actual transfer of copyright or rights to use copyright.

Conclusion

In conclusion, while the appeal by Gartner Ireland Ltd. challenges the classification of its income from subscription-based products as royalty income, the ITAT Mumbai found merit in reviewing the case based on the specifics of the transactions and the applicability of legal precedents. The decision highlights the complexities involved in determining the tax treatment of digital transactions involving cross-border sales of subscription-based products, emphasizing the need for a nuanced understanding of copyright law and international tax treaties.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

This appeal by the assessee is directed against final assessment order dated 27.07.2022 , which has been passed by the Ld. Assistant Commissioner of Income-tax-International Taxation Circle 2(3)(2), Mumbai (in short ‘the Assessing Officer’) pursuant to the direction of the Ld. Dispute Resolution Panel (DRP) dated 15.06.2022 for assessment year 2019-2020.

2. The grounds raised by the assessee in its appeal are reproduced as under:

Ground No. 1: – Erroneous treatment of Business Income as “Royalty” Income

1.1 On the facts and circumstances of the case and in law, the Learned Deputy Commissioner of Income-tax – 2(3)(2) (Ld. AO) and further the DRP-1, Mumbai (hereinafter referred to as the DRP’) have erred in confirming that the entire income earned by way of sale of online subscription asked products amounting to Rs. 86,52,72,951 by the Appellant during the captioned year are taxable as Royalty under Section 9(1)(vi) of the Inco– me tax Act, 1961 and under Article 12 of India – Ireland Double Taxation Avoidance Agreement.

1.2 On the facts and circumstances of the case and in law, the Ld. AO and DRP have failed to appreciate that the consideration received by the Appellant is for non-exclusive / non-transferable copyrighted article i.e., online subscription–based products and is neither towards any use of copyright nor transfer of rights to use the copyright and accordingly, erred in considering the income earned by Appellant as Royalty.

1.3 The Appellant does not have any Permanent establishment (PE”) in India in accordance with Article 7 read with Article 5 of the DTAA between India and Ireland. Hence, the consideration received by Appellant by way of subscription / access fees for the sale of online subscription asked products is in the nature of business income not taxable in absence of PE in India.

Ground No. 2:– Erroneous levy of interest of Rs. 22,71,888 under Section 234D of the Act

2.1 On the facts and circumstances of the case and in law, the levy of interest under Section 234D of the Act is consequential in nature and should be deleted once the relief as sought under Ground No. 1 is allowed to the Appellant.

Ground No. 3: – Initiation of penalty proceedings under section 270A of the Act

3.1 On the facts and circumstances of the case and in law, the Ld. AO has erred in initiating penalty proceedings under section 270A of the Act.

Ground No. 4: – Initiation of penalty proceedings under section 271BA of the Act

4.1 On the facts and circumstances of the case and in law, the Ld. AO has erred in initiating penalty proceedings under section 271BA of the Act.

3. Briefly stated, facts of the case are that the assessee, Gartner Ireland ltd (GIL), is a company incorporated in the republic of Ireland and is a resident of Ireland for tax purpose in terms of Article 4 of Double Taxation Avoidance Agreement (DTAA) entered into between India and Ireland. The GIL as stated is, inter-alia, engaged in the business of sale of subscription based products and related services i.e. periodicals, reports and publications that highlight industry developments , review new products and technologies that provide independent research and insight on all aspect of a company’s business ( IT, Finance, HR, Marketing, Sales , Logistics etc). The Assessing Officer has produced a note of business activity of the assessee , which is extracted as under:

“Business activity:

2. Gartner Ireland Limited (hereinafter referred to as “GIL”) is a Company incorporated in the Republic of Ireland (Ireland) and is a resident of Ireland for tax purposes in terms of Article 4 of the Double Taxation Avoidance Agreement (DAA’) entered into between India and Ireland. GIL is engaged in the business of distributing Gartner Group’s Research Products in the form of subscriptions, both in Ireland and through its distributors, in those territories where the Gartner Group does not have a Tocat presence. The aforesaid subscription research products stated to consist of qualitative research and analysis that clarifies decision-making for Information Technology buyers, users and vendors, and helps clients stay ahead of IT trends. Industry areas covered in such subscriptions include technology and telecommunications including hardware, software and systems, services, IT management, market data and forecasts and vertical industry issues. Forms of research offered include statistical analysis, growth projections and market share rankings of suppliers and vendors of IT manufacturers and the financial community. GIL sells subscriptions to its Indian customers / subscribers to access Gartner’s research products over the internet from its data server which is located outside India. Research subscriptions were originally delivered through print media and other physical means of delivery; however; most clients now access research products over the Internet at www.gartner.com. GIL enters into a Services Agreement (hereinafter referred to as ‘SA’) with its India customers/ subscription for each Gartner service purchased, setting out the details of the services to be provided and the subscription fee applicable. The Indian subscribers pay the subscription/access fees to GIL in accordance with the SA. During the year the assessee has received a gross subscription fee of Rs 86,52,- 72,951/ from a number of Indian clients.”

3.1 During the year under consideration, there is a slight change in the process of access of subscription products by the customers as compared to earlier years; otherwise there is no change in product category. From this year, the assessee has introduced its subsidiary i.e. Gartner India Research and Advisory Services Pvt. Ltd. (for short ‘Gartner India’) as an intermediary for subscribing the ‘GIL’ product and now the Indian customers are required to buy the research product from the ‘Gartner India’ rather than ‘GIL’ directly. The assessee has entered into a ‘reseller agreeme’ nt with Gartner India w.e.f. the year under consideration.

3.2 For the year under consideration, the assessee filed return of income electronically on 29.11.2019 declaring total income of Rs.13,660/- along with claim for refund amounting to Rs.8,65,27,290/-. The return of income filed by the assessee was selected for scrutiny and statutory notices under the Income-tax Act, 1961 (in short the ‘Act’) were issued and complied with. The Assessing Officer issued a draft assessment order dated 25.09.2021 wherein he proposed that the revenue generated from sale of online subscription was in the nature of ‘royalty’ income in the hands of the assessee as against claim of the assessee that same was in the nature of business income and not taxable in India, in absence of any permanent establishment (PE) .

4. The assessee filed objections against draft order before the Ld. DRP, but the assessee could not succeed and the Ld. DRP following their predecessor in assessment year 2012 -13 and order of the Tribunal in the case of the assessee for assessment year 2013 -14 and 2014-15 [, where the Tribunal has followed the decision of Hon’ble Karnataka High Court in the case of CIT v. Wipro Ltd. (2011) 203 Taxman 621 (Karnataka) ] confirmed the addition of Rs.86,52,72,951/- proposed by the Assessing Officer. Pursuant to the directions of the Ld. DRP, the Assessing Officer has passed impugned final assessment order on 27.07.2022 making the addition of subscription fees as royalty income which was subjected to tax @ 10% on the gross basis as per Article 12 of the India-Ireland DTAA.

5. Aggrieved, the assessee is in appeal before the Tribunal by way of raising grounds as reproduced above.

6. Before us, the Ld. Counsel for the assessee filed a Paper Book containing pages 1 to 157 and also filed additional Paper Book containing pages 1 to 84.

7. The sole ground of the appeal of the assessee is in relation to income from sale of online subscription based product , which has been held by the lower authorities as ‘royalty’ as against claim of the assessee of the same as ‘business income’, not taxable in India in absence of any permanent establishment (PE) in India. The brief facts qua the issue in dispute are that during the year under consideration, the assessee has shown income from sale of subscription based research products/report for (i) resale by ‘Gartner India’ to its customers in India on a ‘principal to principal’ basis and (ii) for sale to ‘Gartner India’ for its internal use . The assessee is eligible to claim the tax treaty benefits which have not been disputed either by the Assessing Officer or by the Ld. DRP . During the year under consideration the assessee has sold subscription based product to Gartner India:

(i) of 79,90,95,490/- for resale by Gartner India pursuant to Reseller agreement:

(ii) for Gartner India’s sole internal use of Rs. 6,61,77,461 /- in accordance with Research access

7.1 Regarding the first component of income from sale of subscription based product for resale by the Gartner India to its Indian customers, the Ld. Counsel for the assessee submitted that assessee has entered into a reseller agreement with Gartner India w.e.f. 01.04.2014, under which, the ‘Gartner India’ purchases subscription based product for resale to its clients in India. The relevant clauses of reseller agreement which is available in Paper Book pages 47-59 of the Paper Book consisting of 157 pages, are extracted as under:

“Title – Reseller Agreement”

This Reseller Agreement (the Agreement) is made as of April 1, 2014 (The Effective Date), berween Gartner Ireland Limited… “GIL)… and Gartner India Research & Advisory Services Pvt Ltd …

Background …

B) GIL desire to appoint Gartner India, and Gartner India desires to act, as non-exclusive product reseller … of GIL’s products….

II) Appointment and Authority of Gartner India

GIL hereby appoints Gartner India as a non-exclusive reseller of the Products in the Territory only

VI. Trademarks, Trade names and Copyrights

6.01 No rights to Use or otherwise exploit …. Gartner India shall not have a right to exploit the copyrights embedded in the Products.

6.02 Claim on Trademarks, Tradenames and Copyrights: ..Gartner India shall not have any right to reproduce right, modify or adapt the copyrighted Products prior to resale

6.03 Ownership and Use of the Products: GIL retains the rights to supply the Products… Gartner India shall only supply the Products pursuant to this agreement… which provide that (i access to the Products will be restricted to the named individuals (each a “Named user”)…; (fil) the user IDs and passwords will be issued by GIL at the request of Gartner India and sent directly to the Named users….”

7.2 The Ld. Counsel for the assessee referred to above clauses and submitted that the ‘GIL’ sells products to ‘Gartner India’ and ‘Gartner India’ merely resells such products in India and thus the transaction was a pure sale/purchase of the products and in the nature of the business income, not taxable in absence of PE in India as per the beneficial provisions of the India-Ireland Tax Treaty. Further, the Ld. Counsel referred to Paper Book pages 46 to 48 of the Paper Book consisting 84 pages and submitted that Gartner India resold the products purchased from ‘GIL’ and has made substantial profits on the resale. Further, the Ld. Counsel submitted that Gartner India has paid GST @ 18% on sale of subscription based products purchased from ‘GIL’ to its customers. The Ld. Counsel referred to sample invoices raised by ‘Gartner India’ available on page 73 -74 of the Paper Book consisting of 84 pages. The Ld. Counsel further submitted that Gartner India has also paid GST @ 18% under reverse charge mechanism on purchase of subscription based products from ‘GIL’. The Ld. Counsel further submitted that a transfer pricing scrutiny was made on Gartner India for AY 2020-21 wherein transactions between assessee and ‘Gartner India’ were thoroughly scrutinized and the Ld. TPO was satisfied that transaction were at arm’s length and no adjustment was made.

8. On the other hand, the Ld. DR referred to the order of the lower authorities and submitted that in the case of Wipro Ltd. (supra), the Wipro Ltd. had subscribed online research product of the assessee and payment made by the Wipro Ltd. to the assessee has been upheld by the Hon’ble Karnataka High Court as in the nature of the ‘royalty’ income liable to be deduction of tax at source. He submitted that the Assessing Officer has also held the income from subscription of digital product as royalty u/s 9(1)(vi) alongwith Explanation 2(v) of Act read with Copyright Act and also under the relevant articles of the DTAA. The Ld. DR submitted that as per the definition of the royalty under Article 12 of India-Ireland Tax Treaty ‘use’ or ‘right to use’ of copyright underlying copyrighted digital products amounts to royalty. Further, the word ‘information’ concerning industrial, commercial or scientific experience also covers the case of the assessee because in the case of the assessee information has been collected based on the past experience in the field of industrial commercial or scientific field ,therefore, the case of the assessee squarely falls under the definition of the royalty. The Ld. DR referred to the finding of the DRP wherein the Ld DRP has followed decision of the Co-ordinate Bench in the case of the as sessee in ITA No. 7101/Mum/2010 for assessment year 2007 -08. The Ld. DR further referred to the decision of Co-ordinate Bench in assessee’s own case for AYs 2003 – 04, 2005-06, 2008-09, 2019 -10, 2010-11, 2011-12 and 2012 -13 wherein the issue has been decided against the assessee. The Ld. DR also referred to the decision of the Tribunal in ITA No. 6950/Mum/2017 and ITA No. 167/Mum/2018 for assessment year 2013-14 and 2014-15 wherein the Tribunal following the decision of the Hon’ble Karnataka High Court in the case of Wipro Ltd. (supra) concluded that subscription fee paid by the Wipro Ltd. to Gartner Group for license to use Gartner Database was in the nature of the royalty both under the DTAA and domestic laws. Accordingly, the Ld. DR submitted that issue in dispute being covered in favour of the Revenue, the grounds of appeal of the assessee need to be dismissed.

8.1 Regarding the second component of income for sale of subscription based product to Gartner India under research excess agreement for internal use by Gartner India, the Ld. Counsel for the assessee referred to research access agreement with Gartner India entered into w.e.f. January 2011, under which the ‘Gartner India’ purchases subscription based product from the assessee for its sole internal use and paid research excess fees. The relevant clauses of the research access agreement referred by the Ld. Counsel are reproduced as under:

“Title – ‘Research Access Agreement”

Background…

C…. GIL desires to provide Gartner India access to published research products and related research resources belonging to GIL or its licensors so that such information may be used by Garter India in providing consulting services to its clients.

III. Access and Payment for Access to Resources

3.01 Grant of Access…. GIL grants to Gartner India non-exclusive access to use the resources.

3.05 Restrictions on Use: Gartner India shall not have the right to transfer, license, pledge or otherwise use the Resources in a manner other than as stated in this agreement…

V. Confidentiality

General: Gartner India shall hold in confidence any and all information that it receives from GIL or from any affiliate of GIL or that it develops (“information”) and shall neither publish, disseminate nor disclose such Information to any third parties…”

8.2 The Ld. Counsel for assessee submitted that the subscription based products by assessee to ‘Gartner India’ are copyright and their access was restricted for internal use by ‘Gartner India’ only consequently there is no copyright given to Gartner India thus the said transaction was merely in the nature of sale of copyrighted article. The Ld. Counsel further submitted that the issue pertaining to sale of copyrighted Article for sole internal use versus sale of copyright is now settled in view of the decision of the Hon’ble Supreme Court in the case of Engineering Analysis and Centre of Excellence (2021) 125 taxmann.com 42 (SC) and decision of the Hon’ble Bombay High Court in the case of Director of Income-tax v. Dun & Breadstreet Information Services Pvt. Ltd. [2012] 20 taxmann.com 695 (Bom.).

8.3 With reference to the history of the case, the Ld. Counsel submitted that as far as sale of subscription based product to Gartner India for resale by Gartner India t o its customers in India is concerned, the reseller agreement has been entered into from 01.04.2014 with ‘Gartner India’ and therefore, the order of the Tribunal in earlier years would not apply in view of the change in the business model based on which income has been offered by the assessee on sale of subscription based products to ‘Garner India’ for resale. As far as the research access fee received from Gartner India for sale of subscription based products to be used solely by the Gartner India under research agreement effective from January 2011, the Ld. Counsel submitted that Hon’ble Karnataka High Court in the case of Wipro Ltd. (supra) followed its own ruling in the case of Samsung Electronics Co. Ltd. [2012] 345 ITR 494 (Kar.). The Ld. Counsel submitted that the Hon’ble Supreme Court in the case of Engineering Analysis and Centre of Excellence (supra) has reversed the ruling of the Hon’ble Karnataka High Court in the case of Samsung Electronics Company Ltd. (supra) and therefore, the decision of the Hon’ble Karnataka High Court in the case of Wipro Ltd. (supra) no longer apply in the case of assessee.

8.4 In view of the above arguments, the Ld. Counsel for assessee submitted that income from sale of subscription based products to Gartner India (i) of Rs.79,90,95,490/ – for resale by Gartner India on principle to principle basis under the reseller agreement and (ii) the income from sale of subscription based products for sole internal use of Gartner India of Rs.6,61,77,461/ – under research access agreement, are in the nature of business income and not royalty. Since the assessee did not have a PE in India, the said business income would not be taxable in India under the beneficial provisions of the Tax Treaty.

8.5 Regarding the research access fee, the Ld. DR submitted that from the documents submitted, it could not be deciphered whether the ‘Gartner India’ has further resold or provided consultancy based on the products purchased from the assessee which will be in the nature of use of the copyright in the products of the assessee and therefore, matter may be restored back for detailed verification of the use of the product or use of the copyright in those products by Gartner India.

9. We have heard rival submission of the parties on the issue in dispute and perused the relevant material on record. The issue in dispute before us is whether the income received by the assessee from Gartner India is assessable in the hands of the assessee as business income or Royalty. The term ‘Royalty’ has been defined under the DTAA as under:

ARTICLE 12 : Royalties and fees for technical services – 1. Royalties or fees for technical services arising in a Contracting State and paid to a resident of the other Contracting State may be taxed in that other State. 2. However, such royalties or fees for technical services may also be taxed in the Contracting State in which they arise, and according to the laws of that State, but if the recipient is the beneficial owner of the royalties or fees for technical services, the tax so charged shall not exceed 10 per cent of the gross amount of the royalties or fees for technical services. 3. (a) The term “royalties” as used in this Article means payments of any kind received as a consideration for the use of, or the right to use, any copyright of literary, artistic or scientific work including cinematograph films or films or tapes for radio o r television broadcasting, any patent, trade mark, design or model, plan, secret formula or process or for the use of or the right to use industrial, commercial or scientific equipment, other than an aircraft, or for information concerning industrial, commercial or scientific experience; (b) The term “fees for technical services” means payment of any kind in consideration for the rendering of any managerial, technical or consultancy services including the provision of services by technical or other personnel but does not include payments for services mentioned in Articles 14 and 15 of this Convention. 4. The provisions of paragraphs 1 and 2 shall not apply if the beneficial owner of the royalties or fees for technical services, being a resident of a Contracting State, carries on business in the other Contracting State in which the royalties or fees for technical services arise through a permanent establishment situated therein, or performs in that other State independent personal services from a fixed base situated therein, and the right or property in respect of which the royalties or fees for technical services are paid is effectively connected with such permanent establishment or fixed base. In such case the provisions of Article 7 or Article 14, as the case may be, shall apply. 5. Royalties or fees for technical services shall be deemed to arise in a Contracting State when the payer is that State itself, a political sub-division, a local authority or a resident of that State. Where, however, the person paying the royalties or fees for technical services, whether he is a resident of a Contracting State or not, has in a Contracting State a permanent establishment or a fixed base in connection with which the liability to pay the royalties or fees for technical services was incurred, and such royalties or fees for technical services are borne by such permanent establishment or fixed base, then such royalties or fees for technical services shall be deemed to arise in the State in which the permanent establishment or fixed base is situated. 6. Where, by reason of a special relationship between the payer and the beneficial owner or between both of them and some other person, the amount of the royalties or fees for technical services, having regard to the use, right o r information for which they are paid, exceeds the amount which would have been agreed upon by the payer and the beneficial owner in the absence of such relationship, the provisions of this Article shall apply only to the last-mentioned amount. In such case, the excess part of the payments shall remain taxable according to the laws of each Contracting State, due regard being had to the other provisions of this Convention.

9.1 The term ‘Royalty’ has been defined in Act under Explanatin-2 below the section 9 as under:

Explanation 2. – For the purposes of this clause, “royalty” means consideration (including any lump sum consideration but excluding any consideration which would be the income of the recipient chargeable under the head “Capital gains”) for-(i)the transfer of all or any rights (including the granting of a licence) in respect of a patent, invention, model, design, secret formula or process or trade mark or similar property; (ii)the imparting of any information concerning the working of, or the use of, a patent, invention, model, design, secret formula or process or trade-mark or similar property; (iii)the use of any patent, invention, model, design, secret formula or process or trade mark or similar property; (iv)the imparting of any information concerning technical, industrial, commercial or scientific knowledge, experience or skill;[(iv-a) the use or right to use, any industrial, commercial or scientific equipment but not including the amounts referred to in section 44-BB;] [ Inserted by Act 14 of 2001, Section 4 (w.e.f. 1.4.2002).](v)the transfer of all or any rights (including the granting of a licence) in respect of any copyright, literary, artistic or scientific work including films or video tapes for use in connection with television or tapes for use in connection with radio broadcasting, but not including consideration for the sale, distribution or exhibition of cinematographic films; or(vi)the rendering of any services in connection with the activities referred to in [sub-clauses (i) to (iv), (iva) and (v)] [ Substituted by Act 14 of 2001, Section 4, for ” sub-clauses (i) to (v)” (w.e.f. 1.4.2002).].

9.2 Therefore, the issue in dispute before us is whether the transaction of the assessee under reference, could be characterized in the nature of business income or Royalty income under the DTAA or under domestic law . As far as first component of the income i.e. income from sale of subscription to Gartner India for further resale to its customers , is concerned, the assessee has change d its business model w.e.f. year under consideration. Prior to assessment year under consideration , the assessee used to sale subscription of its digital research products to the customers directly , whereas in the year under consideration, according to the assessee, it has engaged Gartner India as intermediary . It is submitted that the assessee is sell ng its research products to Gartner India and Gartner India after charging certain markup , is further selling to customers in India.

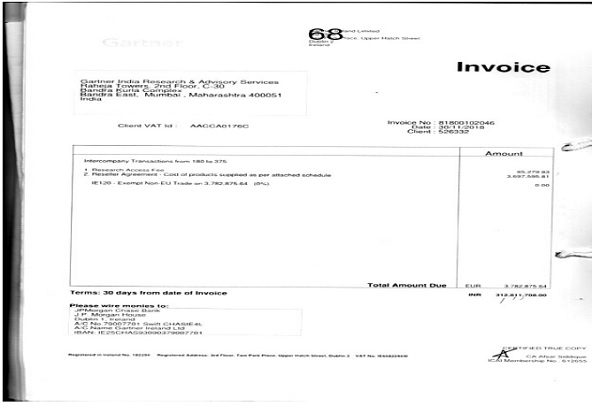

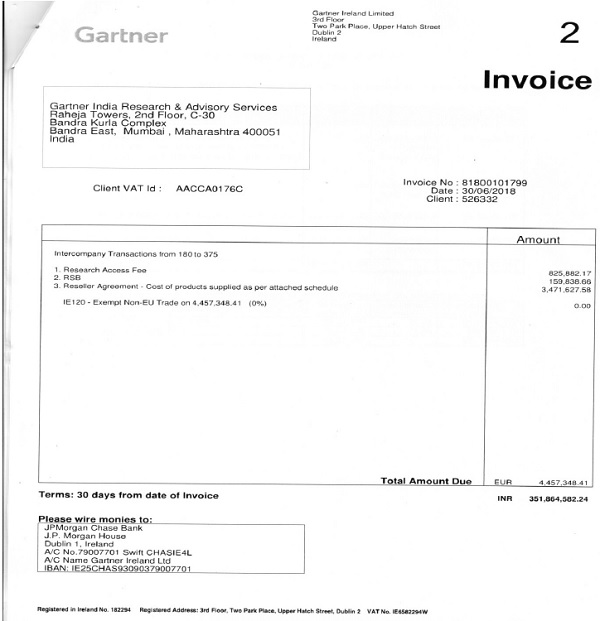

9.3 We have examined the financial of Gartner India furnished before us by the assessee vide additional paper book III. On perusal of profit and loss account ( PB-11). We find that Granter India has shown revenue from operations at Rs. 7,37,49,79,570/ -. Break up this revenue has been provided on PB -23, where revenue from sale of subscription based products has been reported at Rs. 2,52,64,68,624/-. The purchase of subscription has been reported at Rs. 35,78,90,830/ -(PB-23) . Though, the assessee claimed to have sold the subscription based products to its Indian subsidiary, but no stock of subscription based product is found in the books of ‘Gartner India’. In view of the above doubt arose in the claim of the assessee of sale of products to its subsidiary and further resale, the assessee was asked to correlate sale of each subscription based product to ‘Gartner India’ and further resale of the same product by Gartner India to end customer. Before us, the assessee has filed a copy of the sample invoice issued by the assessee on ‘Gartner India’. The relevant copy of the invoice available on PB-III/68 as extracted as under:

9.4 As part of schedule of above invoice, the assessee enclosed a list of periodicals (PB -III/69-72) which were sold under the above invoice. The list contains only product name from Sr No. 1 to 179. It is noted that the assessee has raised a consolidated invoice for all those products, but quantity of each product sold or sale price of each product was not provided. Therefore, the matter was fixed for clarification by the Bench and assessee was asked to supply basis of price for which each product was sold by the assessee to ‘Gartner India’. In next hearing, the assessee provided a basis of charging the ‘Gartner India’ for sale of products, which is reproduced as under:

Gartner Ireland Limited (‘the Appellant1 / ‘GIL’)

AY 2019-20

Statement of working of Gartner Ireland Invoices raised on Gartner India

| Particulars | Amount (INR) | Reference to Paper Books | |

| Gross Subscription-based product Revenue of Gartner India as per its P&L for the year ended 31 March 2019 | (A) | 3,06,99,26,300 | Pg No 23 as per paper book consisting of 84 pages submitted on 09 Nov 2023 |

| Less: Direct & Indirect

Operating Cost of Gartner India relating to Subscription-based product Revenues |

(B) | 2,15,78,01,737 | Pg No 37 as per paper book consisting of 84 pages submitted on 09 Nov 2023 -Segment expenses (295,68,97,227) includes operating cost (215,78,01,737) + cost of goods sold (79,90,95,490) |

| Less: Return on Subscription- based product sales to Gartner India @ 3.7% | (C) | 11,30,29,072 | Pg No 59 and 48 as per paper book consisting of 157 pages submitted on 10Oct2023 |

| Gartner Ireland’s Aggregate Billing to Gartner India in respect of the subscription- based products (excluding Research Access Fees) | (D)=(A)-(B)-(C) | 79,90,95,490 | Pg No 23 and 45 as per paper book consisting of 84 pages submitted on 09 Nov 2023 |

9.5 Further, the assessee submitted a sample copy of consolidated invoice raised for sale of subscription of products to ‘Gartner India’ for the period from 1/4/2018 to 30/6/2018 ( one quarter of the year ), which is extracted as under:

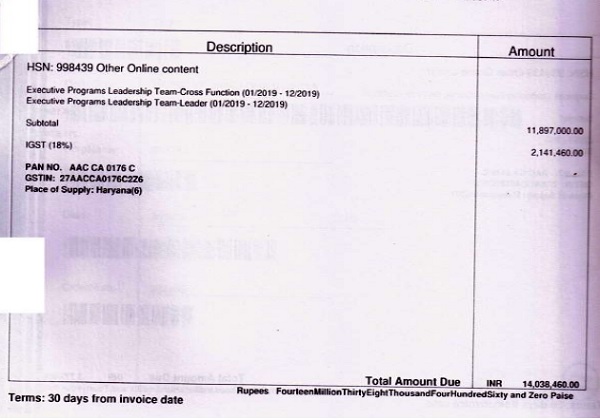

9.6 A copy of the invoice raised by ‘Gartner India’ to its customers is available on page 73 of the Paper Book . For ready reference same is reproduced as under :

9.7 Before us, the Ld. Counsel for the assessee has referred to the reseller agreement and submitted that Indian customers approach the ‘Gartner India’ for purchase of subscription of the research product and the ‘Gartner India’ forward said request to the assessee and the assessee provide user ID and password directly to those customers for downloading the subscription from the website of the assessee. In the entire process, the assessee has shown to have sold the products to ‘Gartner India’ on quarterly basis. But in such quarterly invoices raised by the assessee on Gartner India , there is no mention of quantity of products sold , thus it can be inferred that assessee has charged for one product only or in other words we may say that assessee i.e. GIL has charged onetime quarterly fee to Gartner India for products having Sr No. 1 to 1, 79 whereas ‘Gartner India’ had option to resale the same product multiple times and actually sold the same product to multiple customers. Thus, in substance, the ‘Gartner India’ purchased not only the product but right of copying of the research products and selling the same to Indian customers multiple times, thus the transaction under reference of sale of subscription based research to ‘Gartner India’, for all practical purposes, can be characterized as in the nature of ‘sale of copyright’ in the database of research products of the assessee. Though the assessee has not specifically mentioned in its invoice as license fee for use of the copyright in the database but in substance it becomes fee in the nature for the use of the copyright in the digital product of the assessee . During the course of hearing, the ld Counsel for the assessee was specifically asked to correlate each invoice of resale by ‘Gartner India’ with corresponding sale invoice issued by the assessee, so as to prove the claim of the assessee that transaction of the assessee was a pure sale and purchase of products i.e. trading transaction, but the assessee failed in substantiating that quantity of research products sold to ‘Gartner India’ was equivalent to the quantity of products resold by ‘Gartner India’ to its customers. At least from the invoices raised by the assessee and submitted before us, it is not getting established that number of subscriptions sold by the Indian entity are equal to the number of subscription sold by the assessee as number of subscription are not mentioned in the invoices raised by the assessee. The assessee was asked to provide invoices raised in subsequent years also but no such invoices have been provided. If we try to compare sale of the digital products of assessee physical products i.e. magazine or a book in market, be like that the assessee had sold one copy of different physical magazines to Gartner India, and then Gartner India got copies of those printed and sold the same multiple times to its customers . It hardly matters whether the user ID and password for downloading of the report has been issue d by the assessee, because same has been done on behalf of Gartner India only. Therefore , in substance the assessee has sold not only the digital product but along with all copyrights there in, which squarely falls in the definition of royalty both under Article 12 of DTAA between India Ireland and provisions of the Act (domestic law).

9.8 Another argument by the Revenue is that the word information concerning industrial, commercial or scientific experience also covers the case of the assessee because in the case of the assessee information has been collected based on the past experience in the field of industrial commercial or scientific field ,therefore, the case of the assessee squarely falls under the definition of the royalty. But neither the assessee has filed any details of the products nor the lower authorities have examined the issue as how the research products could be characterized as information in the industrial, commercial or scientific field, which falls under the definition of ‘Royalty’ provided under the DTAA. Before us also no such information has been provided. In absence of any such information, this issue can’t be adjudicated by us. In fact and circumstances of the case, we feel it appropriate to restore the whole issue in dispute back to the file of the AO for verification of the transaction of sale of subscription to the Gartner India afresh keeping in view our observation above and in accordance with law. If required, the AO may also examine claim of the assessee of not having any PE in India.

9.9 As far as research access fee received from Gartner India is concerned though the assessee has claimed that same was for access of the database of the assessee for internal use by Gartner India in their business of consultancy but the Ld. DR has submitted that no enough information was filed by the assessee before the lower authorities to substantiate whether any copyright in the digital product has been exploited by Gartner India in the business of their preparation of research papers. Before us also no such documentation as how the Research fee paid has been utilised in each quarter, other than the general submission that such fee was paid for self consumption. Therefore, we feel it appropriate to restore this issue back to the file of the Assessing Officer for proper investigation and discovery of the true facts for determination of the issue whether there was any exploitation of the copyright of the assessee in the digital products sold to Gartner India under Research access fee.

9.10 The ground No.1 of appeal of the assessee is accordingly partly allowed for statistical purposes.

10. The ground No. 2 being consequential and therefore, same is dismisses as infructuous. The ground No. 3 and 4 are being premature at this stage therefore, same are dismissed as

11. In the result, the appeal filed by the assessee is partly allowed for statistical purposes.

Order pronounced in the open Court on 30/05/2024.