TDS on PAYMENT on Certain sum for PURCHASE of GOODS; conditions / compliances as under;

1. Purchase of goods covered and not Services

2. Rate of TDS; 0.1% of such sum exceeding Rs. 50 Lakh.

3. Who liable to deduct; a buyer whose total sales /gross receipts / turnover of the business > Rs. 10 crore in immediately preceding FYr purchasing any goods of Rs. 50 Lakh or more in any previous year from a resident seller, shall at the time of credit or payment whichever is earlier deduct TDS.

4. For determining limit of Turnover of Rs.10 Crore, shall be determined excluding GST collected on Sales.

5. the total amount of purchases, in absence of specific circular,TDS will be done inclusive of GST on goods. (although on Services, excluding GST is liable for TDS, because of specific CBDT issues a circular 23/2017 dt.19.7.2017).

6. Buyer liable to deduct TDS if the purchases in the Fyr (including purchases before 1st July, 2021) exceeds Rs. 50 Lakh

7. In respect of Fyr 2021-22, the purchases or payments made before 1st July, 2021 (even if it exceeds Rs. 50 Lakhs) shall not be liable to TDS u/s. 194Q.

8. However, to calculate Rs. 50 Lakh:- purchases before 1st July, 2021 shall be included to determine the applicability of TDS u/s. 194Q.

9. Threshold limit of Rs. 50 Lakh to be checked – EVERY YEAR FOR EVERY seller. The applicability Sec-194Q shall be determined with reference to purchases during a financial year.

10. If purchases made before 1st July, 2021 but payment has been made on or after 1st July, 2021 then no TDS at the time of payment.

11. If payment as an advance made before 1st July, 2021 but purchase invoice raised on or after 1st July, 2021 then no TDS at the time of recording of purchase invoice.

12. TDS deducted in the month, to be deposited on or before 7th of next month, and for March, can be deposited upto 30th April. paid through Challan No. 281 and details of TDS will be included in Quarterly TDS Statement Form No. 26Q

13. This section shall not apply to a transaction on which– (a) tax is deductible under any of the provisions of this Act; and (b) tax is collectible under the provisions of section 206C other than a transaction to which sub-section (1H) of section 206C applies.

14. If TCS u/s. 206(1H) as well as TDS u/s. 194Q is applicable on the same transaction, only TDS u/s 194Q will be applicable and TCS u/s. 206C(1H) will not be applicable.

15. All the transactions where seller not collected tax because the buyer has already deducted tax are required to be reported by seller in his TCS Statement in 27EQ

16. TDS u/s194Q is applicable on purchase of agricultural products / GST exempted items.

17. TDS u/s 194Q is required to be deducted on purchase of capital assets such as Plant and Machinery.

18. No TDS u/s 194Q, Since the Land & Building is an immovable property and not goods.

19. IF Buyer fails to deduct TDS u/s 194Q; then 30% of such sum will be disallowable u/s. 40(a)(ia). In such cases, buyer of goods may have to furnish Form No. 26A from the recipient to prevent disallowance u/s. 40(a)(ia). However, Interest @1% per month will still be payable from the date of purchase / payment upto the date of furnishing of return of income by the seller in accordance with the provisions of Section 201 of the Act.

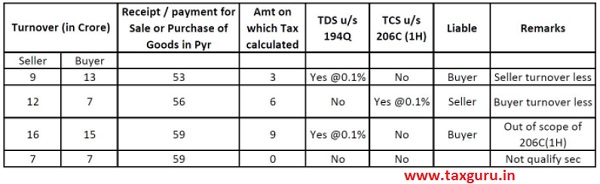

20. Applicability of TDS u/s. 194Q and TCS u/s. 206C(1H) on Transaction of Value (example below)

21. Seller may obtain Self Declaration from Buyer /customers (from whom receipt against sale of goods exceeds Rs. 50 Lakhs in a Fyr) that whether such buyer will deduct TDS u/s. 194Q or not.

21. Seller may obtain Self Declaration from Buyer /customers (from whom receipt against sale of goods exceeds Rs. 50 Lakhs in a Fyr) that whether such buyer will deduct TDS u/s. 194Q or not.

Sec 206AB

Special provision for TDS for NON-Filers of ITR; conditions / compliances as under; Sec 206AB

1. On any sum /Income / amount paid / payable / credited by a person (other than 192, 192A, 194B, 194BB,194LBC, 194N) to a Specified person, the tax shall be deducted at Higher of the following rates;

1. at TWICE the rate specified in the relevant provision of the act,

2. at TWICE the rate in force,

3. at the rate of FIVE per cent

2. Specified Person means a person who has not filed ITR for both of the two assessment years relevant to the two previous years immediately prior to the previous year in which tax is required to be deducted, for which the time limit of filing ITR u/s 139(1) has expired; and the aggregate of TDS and TCS in his case is Rs.50k or more in each of these two Pyr.

3. Specified person not include a NR who does not have a PE in India

4. If the provision of section 206AA / 206CC ;(requirement to furnish PAN) is applicable to a specified person, in addition to the provision of this section (i.e.206AB / 206CCA), the tax shall be deducted at higher of the two rates provided in this section and in section 206AA / 206CC.;

1. at the rate specified in the relevant provision of the act,

2. at the rate in force,

3. at the rate of TWENTY per cent