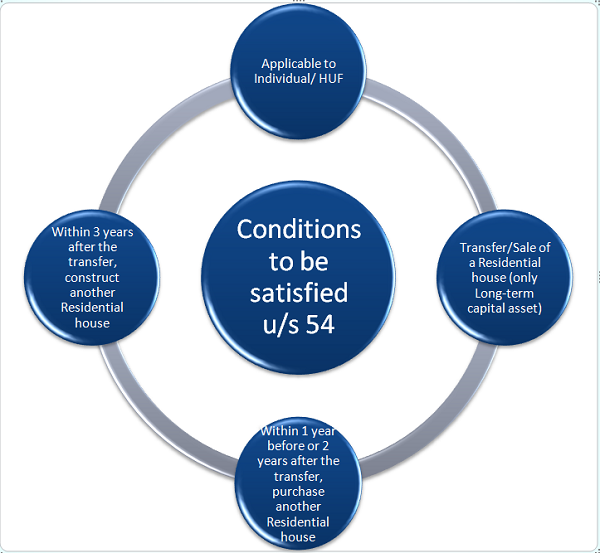

Sale of a residential house is taxable under the Income Tax Act. When you sell a house, you are required to pay capital gain tax on the profit received from the sale. The Income Tax Act,1961 provides relief from tax payment in such a case under Section 54 , subject to fulfilment of certain conditions. Let’s analyze, what does section 54 talk about and how we can apply it to save tax.

Here we go:

FOR YOUR KIND ATTENTION:

W.e.f. A.Y. 2020-21, an individual or HUF can claim exemption for investment house (i.e., can purchase or construct 2 house). This exemption ids available only if long term capital gain is upto Rs. 2 crores.

Points to be noted before we proceed:

1. The house must be purchased or constructed in India.

2. In case of compulsory acquisition, the period for purchase/ construction of new house will start from the date of receipt of compensation.

3. If exemption for investment in 2 houses is availed of, then this exemption cannot be availed again for the same or any other assessment year.

4. The new house must not be sold before completion of 3 years.

What if the new house is transferred/sold before 3 years complete?

The exemption claimed earlier shall stand withdrawn. Means, while calculating the capital gain on the sale of this new house, the exemption claimed earlier will be deducted from the cost of acquisition of new house.

So, if the 4 conditions mentioned above are satisfied, then you can claim capital gain exemption. But, HOW MUCH?

Lower of :

Amount of Capital gain vs Amount invested in purchase/ construction of new house

* Amount invested also includes the amount of capital gain which is unutilised and deposited in Capital Gain Deposit Account Scheme on or before the due date of filing return of income. Means you can claim exemption for deposited amount also. You can use the deposited amount within 2 or 3 years as mentioned in the section for purchase or construction of the house.

What if the amount deposited is not utilized for purchase/construction of new house?

The amount unutilised and already claimed as exemption will be taxed as long term capital gain for the year in which the period of 2 or 3 years expires.

Let’s analyze Sec.54 with some basic questions –

Q 1. What should be the period of holding of house property to consider it as Long term capital asset?

– 24 months

Q 2. Can a person other than an Individual / HUF claim such exemption?

– No

Q 3. An Individual sold a shop owned by him and purchased a new house. Can he claim exemption on capital gain u/s 54?

– No, asset sold must be a residential house.

Q 4. An Individual sold a house and purchased a plot of land. Then he constructed a house on it. Can he claim exemption on capital gain u/s 54?

– Yes, because it’s construction of residential house.

Q 5. An individual sold a residential house owned by him and purchased a shop. Can he claim exemption on capital gain u/s 54?

– No, asset purchased/constructed must be a residential house.

Q 6. An individual sold a residential house owned by him and purchased 2 houses in the previous year 2019-20. Capital gain amounted to Rs. 3 crores. Can he claim exemption on capital gain u/s 54?

– No, because the amount of capital gain exceeds Rs. 2 crores. Exemption for investment in 2 houses is available only if capital gain is up to Rs. 2 crores.

Q 7. An individual sold a residential house owned by him. Capital gain amounted to Rs. 5 lakhs. He deposited Rs. 5 lakhs in the Capital Gain Deposit Account Scheme as he was not able to utilize it for purchase/construction of residential house before the due date of filing return of income and claimed exemption u/s 54. Next year, he withdrew the money to purchase some gold. Will the exemption granted be revoked on purchase of gold from the money withdrawn from the scheme?

– Yes, exemption will be revoked and the exemption granted earlier will be charged to tax as long-term capital gain because of the fact that the withdrawn money was utilized for purchase of asset other than residential house.

Q 8. Can an individual/HUF claim capital gain exemption on purchase or construction of a residential house outside India?

– No, the house purchased or constructed must be situated in India.

Hope the article is helpful. Thanks for reading.

Author Bio

(Continued from previous post) What is the legal meaning of date of ownership? Is it from the date of allotment, or date of final payment or is it date of registration

After selling 1 house I have bought 2. From what date does the 3 year time limit start to enable sale,without violating exemption of capital gain? Is it after registration,which is not being done due to some property id issues of the builder, or is it after the date of final payment? Or is it from the date of allotment letter? Please clarify

My wife want to sale aresidential plot. out of long term capital gain she want to buy two residential plots in another city. The capital gain amount is less thaan2cr.

Is eligible for saving of capital gain.

First I purchase new Residential House with loan and then after within one year i will sold my old residential house. Can i Claim exemption.

Can i sell 1 residential house & 1 residential plot & with total combined value buy 1 residential house & avail the capital gain exemption benefit.

There are many confusions and doubts going on regarding the utilization of the Capital Gain amount utilization, hence I need clarity on the same.

Capital Gain Amount – Less than 2CR

Clarification required:-

1) Can I buy land from one party and house construction from another party (building contractor)?.

2) Can I utilize the capital gain amount to pay stamp duty, registration fee and cess for the land? (DD/Cheque to Sub-Registrar)

3) Can I utilize the capital gain amount to pay the cost of interior works like kitchen cabinets and wardrobes? (Rajat-B-Mehta-Vs.-ITO-ITAT-Ahmedabad)

Option 2 – Purchase of 2 apartments/flats (same building or different area) if the land and construction does not work out for me.

Request you to clary the above doubts.

If the residential house was sold in February 2018 for 60 lacs, Can I re-invest the amount in TWO houses instead of ONE for 30 lacs each & get exemption for capital gains. Or I need to invest in only ONE residential property?

Here are the answers to your queries:

1. “Date of ownership” is what that matters. So, first confirm the date of ownership and accordingly show it in the relevant return.

2. No, the property purchased must be a residential house property to avail the benefit, not a commercial property.

3. You can purchase a residential house within 2 years or construct within 3 years of sale.

4. You can invest in notified bonds under section 54EC within 6 months of sale up to a value of 50 lakhs rupees, Read section 54EC of the Income Tax Act for details.

Clarification required for Longterm Cap Gain on House Sale:

1) if the agreement is in March19 and the final payment & TDS is paid in April19, then it will be taken in year Ay 19-20 or Ay 20-21 for Tax returns

2) Can the person buy a commercial property after sale of House Property and avail the benefit of purchase

3) what is the timeline to invest on ready flat or shop or property under construction

4) what are the different option to invest other than property and take the benefit of not losing amount on taxes