Day: May 1, 2019

20 articlesIncome Tax

Income Tax

No addition for unabated assessment unless incriminating materials unearthed during search

Income Tax

Income Tax

Omission by auditor Reasonable Cause for delay in claiming Refund

Corporate Law

Corporate Law

Delhi VAT on electrical equipment used in generation & distribution of electricity, supplied to DlSCOM

Income Tax

Income Tax

TDS not deductible on Payment Gateway Charges paid to Banks

Goods and Services Tax

Goods and Services Tax

GST on pure services provided to Central /State Govt or UT

Income Tax

Income Tax

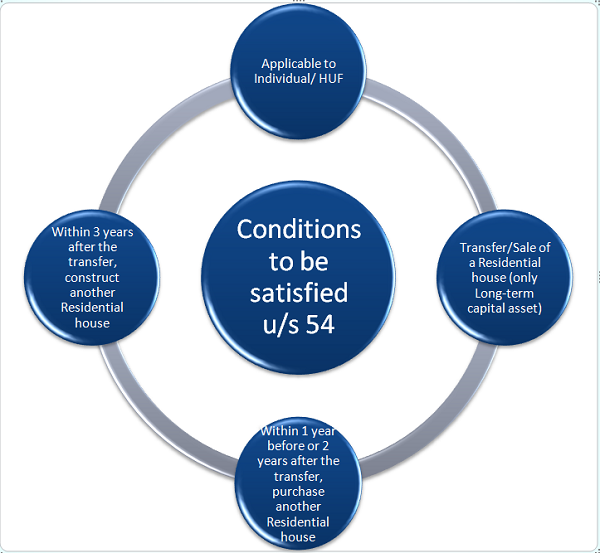

Invest in 2 Houses And Claim Capital Gain Exemption

CA, CS, CMA

CA, CS, CMA

How CS student can Prepare Company Law Paper?

Goods and Services Tax

Goods and Services Tax

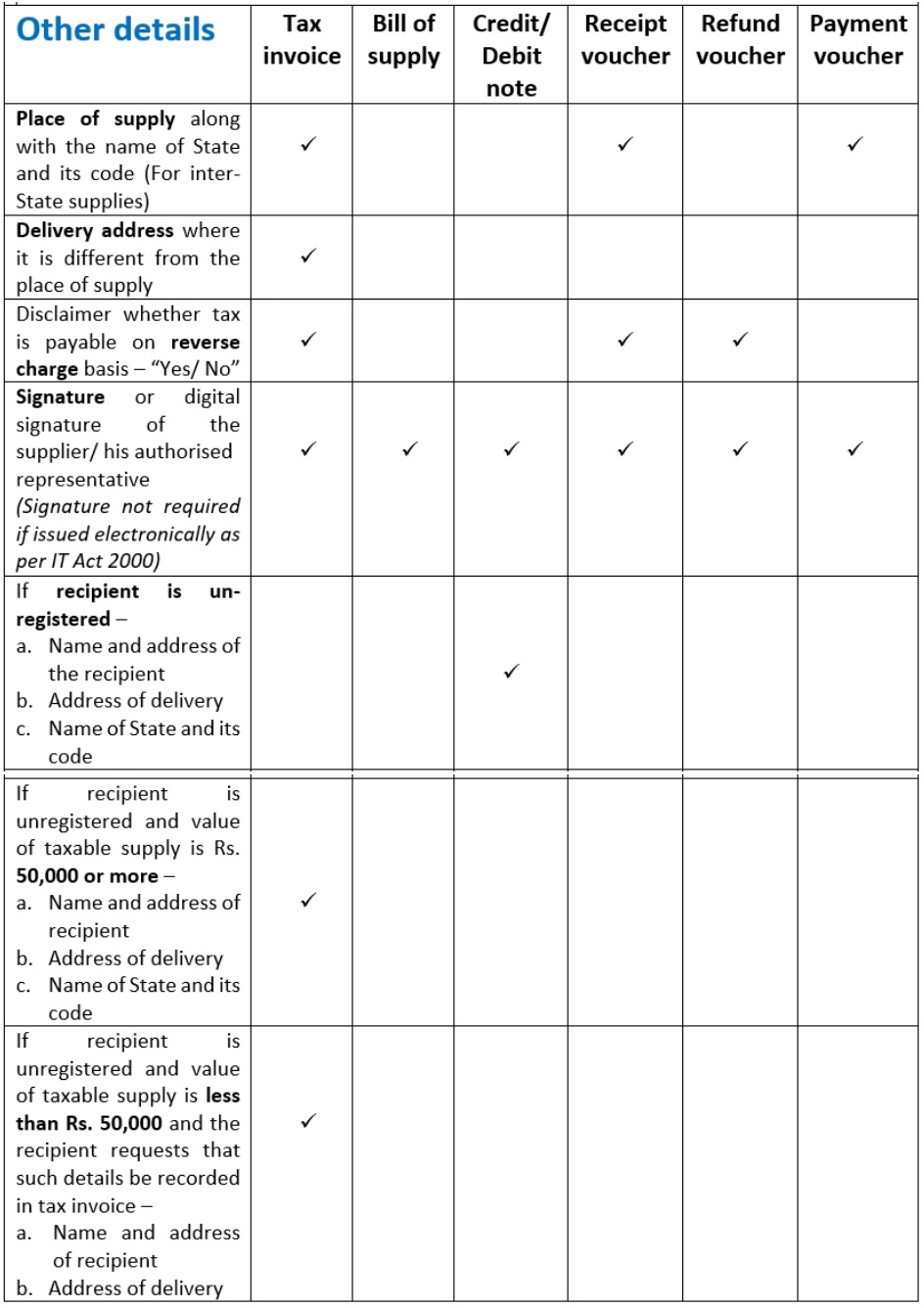

Important documents prescribed under GST

Goods and Services Tax

Goods and Services Tax

GST Payable under RCM on specified goods & services

Fema / RBI

Fema / RBI